We Will Rise

This week several central bank meetings were scheduled: The Swedish Riksbank, the Bank of England, the Federal Reserve, and the Swiss National Bank, to name a few. Except for the Swiss National Bank, where inflation is still low despite supply-chain problems and turmoil in energy markets, all other central banks are confronted with the highest inflation rates since the 1980s.

Nevertheless, high inflation and economic stagnation did not hurt equity markets as hard as expected. It seems that many market participants still expect central banks to come to the rescue again.

With the Bank of Japan being the outlier, all big central banks have raised interest rates, but stock markets are still way above their 2020 lows. For equity traders and investors, the famous Greenspan Put seems alive and well, despite a different, inflationary market environment.

The title of today’s substack, We Will Rise, is from the Swedish Band Arch Enemy (even if you are not into the music, vocalist Angela Gossow will blow your mind, trust me!), which fits nicely because the Swedish Riksbank surprised markets with an interest rate increase of a whole percentage point.

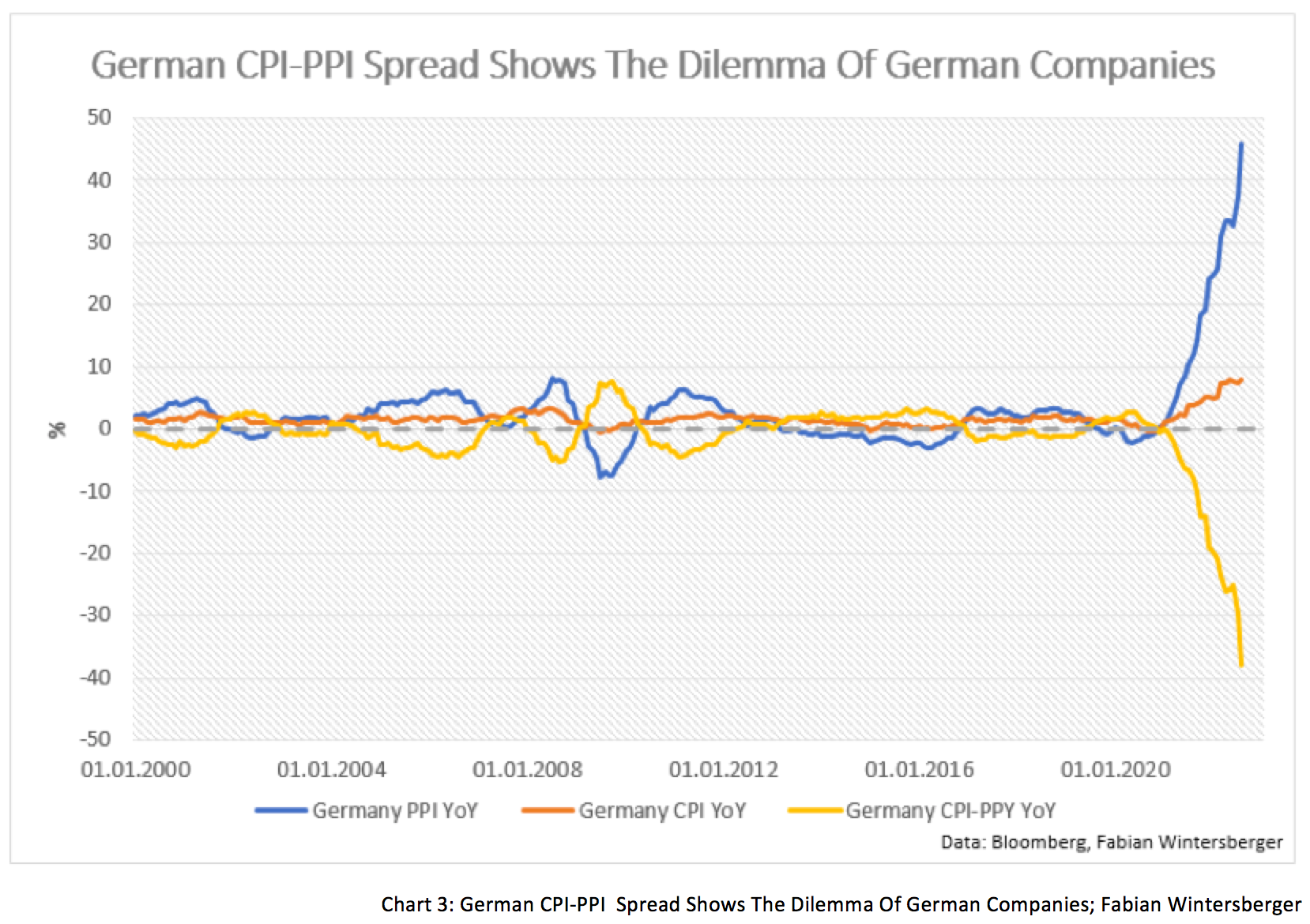

The hike seems justified given the high inflation rate in Sweden, one of the highest in Northern Europe. Inflation in Europe still has room upward, primarily because of the ongoing war in Ukraine. Recent producer price data from Germany supports this thesis, which rose significantly more than expected. Month-over-month producer price inflation was 7.9 %, the highest on record.

The divergence between CPI and PPI makes it evident that German businesses are in a tough spot. The WSJ recently reported that many German producers are considering moving abroad because of high energy prices.

According to ECB governing council member Isabel Schnabel, the ECB still expects inflation to come down to its 2 % target by 2024. She said that a recession in the Eurozone would probably be the price to pay. However, all forecasts for Europe are currently highly uncertain, and Russia’s announcement of partial mobilization and referendums in the occupied areas of Ukraine probably caused another rise in economic uncertainty.

Still, I am doubtful that inflation in the US and the Eurozone will return to the Fed’s and ECB’s target rate of 2 % anytime soon. But before I go into more detail later, I would like to briefly review the FOMC decision from this week.

On Wednesday, the Fed raised the Fed Funds Rate by 75 basis points, as market participants expected. In his press conference, Jay Powell made clear that the Fed thinks that the Fed will have to tolerate higher unemployment and a probable recession to reach its goal. Powell’s statements let us suggest that a soft landing is very unlikely.

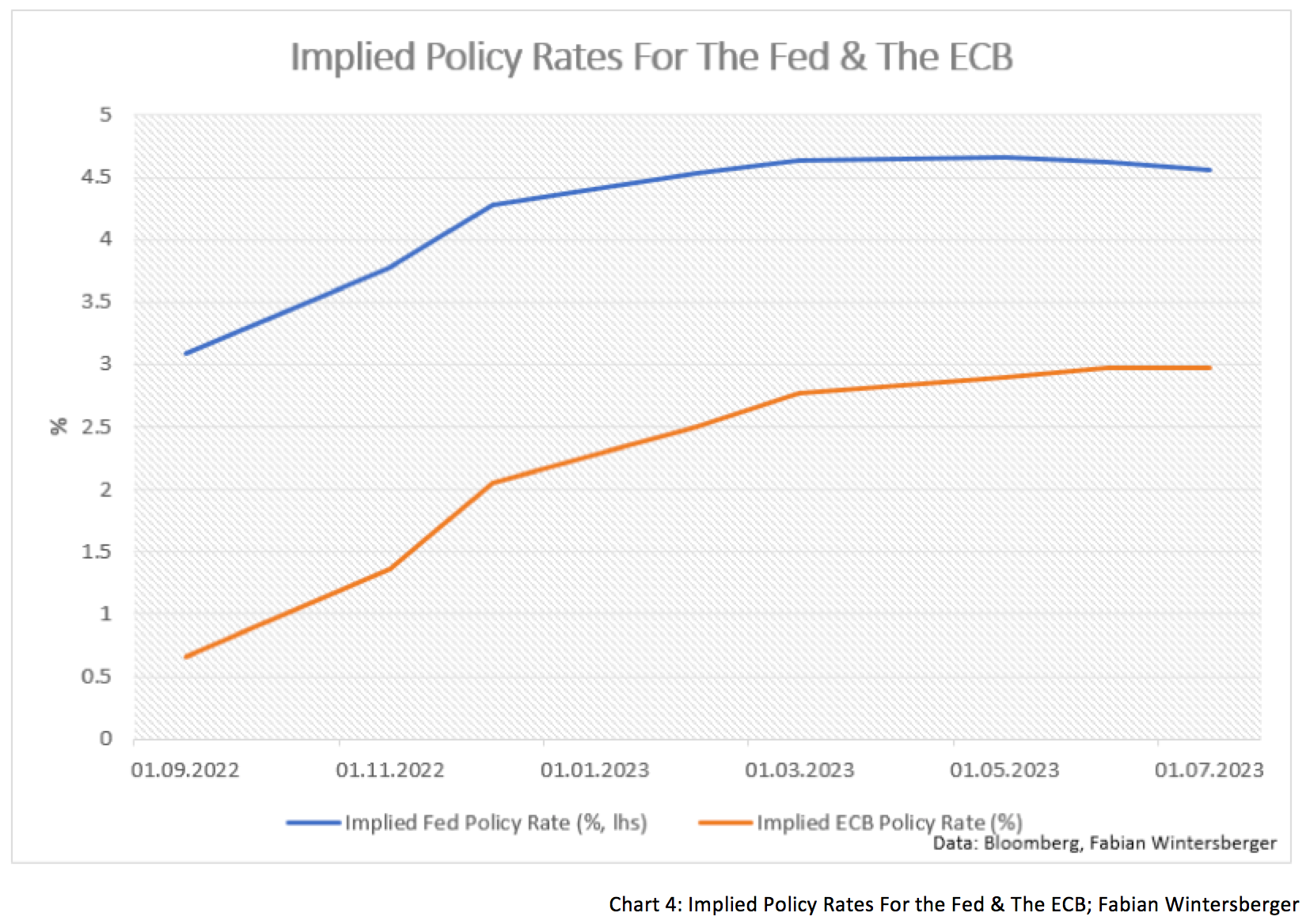

Markets now expect the FFR to rise above 4.5 % and an ECB rate at around 3 % next year.

Most economists expect consumer price inflation to return to 2 % within the next 12 to 36 months. That is how their models are created and assume that inflation over the long run is influenced by long-term inflation expectations, which - according to the models - are anchored at 2 %.

However, a recent working paper from Iván Werning (MIT) hardly finds evidence for the theory that long-term inflation expectations mold future inflation. Werning found that mostly short-term inflation expectations influence inflation, and thus, one could make a case for much more active central banks.

Although neoclassic and neo-Keynesian economists always talk about the importance of inflation expectations, I think that critics of the theory are right that inflation expectations hardly play a role in consumer prices. As I wrote in Nothing But Mistakes:

[N]obody will buy more goods and services as intended because of a rise in inflation expectations. Nobody will turn up the air conditioner more because one expects electricity prices to rise, and nobody will rent an additional home because his rent increases. The only place where expectations play a role is in asset markets, but they do not have much to do with the CPI.

Currently, most market participants expect two things: firstly, they expect a central bank-induced recession; secondly, they hope this will lead to sharply falling consumer prices. Further, they assume this will eventually lead to rising bond prices.

However, while I think their first assumption is correct, I am not sure that their second is. A deflationary spiral accompanied all recessions of the last 40 years, but I think several underlying factors have changed. Nobody seems to believe that stagflation will stay for longer.

In the abovementioned interview, Isabel Schnabel said the labor market is still robust. The Eurozone unemployment rate is currently at 6.7%, a record low. Nonetheless, I would argue that there are some reasons for that. As the pandemic started, many European countries followed Germany’s example and implemented Kurzarbeit (short-time work).

Kurzarbeit means that workers work fewer hours, and the government partially subsidizes wages. That prevents a rise in unemployment, like in the GFC when German unemployment did not move much. Yet, those programs are supposed to be temporary, but since Covid, they have become permanent. Germany recently said it will prolong easier access to the scheme until the end of this year.

The rate of change of US CPI might fall a bit in the coming months (although one could even make some arguments against that), but it seems highly unlikely in the current economic environment that the rate of change will fall back to 2 %.

However, market participants expect exactly that, which is why US 10y yields are still below 4 %. But if inflation will not return to 2 %, then I would argue that a) bond yields are still too low, and b) stock markets are too high. Interestingly, most investors still expect a Fed Pivot somewhere next year.

If rates are too low at the long end of the curve, if there is no pivot, and inflation does not fall back to 2 %, how is the situation if the Fed actually pivots? Assume consumer prices fall back to 5 % rapidly, and a recession kicks in. Further, let us assume that the Fed gets cold feet and loosens again while the Biden administration is handing out money.

Firstly, stock markets would bottom and start a rally, together with bonds. But we must remember that as the government spends more money on the real economy, this is fueling inflation again. Even if the Fed did not loosen, this would mean that bond yields would rise again, even if they fall briefly before that. That is what Powell wants to avoid, what he talked about endlessly for the last few months.

If we look at the Arthur Burns Pivot from the 1970s, we will find out that that was exactly what happened. When the Fed cut rates in 1974, 10y yields fell slightly to take off afterward because inflation took off again.

Because of that, I think most market participants underestimate the persistence of current inflation. Undoubtedly, most of us were surprised when the war started in February, pushing inflation slightly higher than otherwise. However, one should not forget that the US and European economic structure has changed rapidly during the last two years. Just think of the rise in remote work and the consequences this had on human action and preferences, for example.

Additionally, rate hikes need to result in a fall in demand to influence future price inflation, and I would argue that the government could also influence inflation. Yet, politicians are still caught believing that every crisis can be solved with additional government spending.

In an inflation regime, that is not the case. In the end, inflation is primarily influenced by the amount of money in the real economy and the number of goods it can purchase. However, some economists claim that this hardly plays a role because QE did not lead to inflation. They forget that QE remained within financial markets, but that additional fiscal spending directly goes into the real economy. And governments LOVE to spend.

You probably never heard of the Employee Retention Credit, a part of the American RescuePlan, which makes it possible for businesses to get a tax credit if Covid has had a negative effect on their business. For example, one business that operates a small convenience store with 12 employees (mostly part-time) got a refund of $110,000, more than they actually paid.

As long as governments do not cut back on spending, inflation will remain high because demand will remain elevated despite the central bank’s tightening. That is like playing with fire because higher interest rates mean higher rates for refinancing government debt. As a result, credit risks for countries rise, and thus, investors may ask for even higher yields.

I think yields will have more room to rise, and we will experience another significant sell-off in the stock market. The bear market has just begun, although bonds have a considerable advantage against equities, as Jim Bianco explained so nicely in his latest appearance on MacroVoices:

If you go back and you look at the charts in the 70s, the bond market was all rates were going up and it was terrible, yes. But coupons were so high, you always got a positive return from the bond market. So even if you bought them and rates went up, you lost on price. But you had such a big coupon, at the end of the year, you made money every year in the bond market… As there's an old adage in the bond market, there are no bad bonds, there's only bad prices.

I want to close this week’s post with a chart by Bank of America, which also speaks against the assumption that inflation will go away quickly. During 1980 and 2020, all advanced economies which experienced inflation rates above 5 %, on average, it took ten years until inflation declined back to 2 %.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)