The Forgotten One

The pain is necessary. Sometimes pain is the teacher we require, a hidden gift of healing and hope – Janet Jackson

When reflecting on past events, it's often noticeable that initially, our minds tend to recall predominantly negative occurrences. For instance, when contemplating economic history, our thoughts tend to gravitate toward events such as recessions, financial crises, or periods of inflation.

This phenomenon is known as the negativity bias, a deeply ingrained aspect of the human psyche:

Even when of equal intensity (e.g. unpleasant thoughts, emotions, or social interactions; harmful/traumatic events) have a greater effect on one’s psychological state and processes than neutral or positive things.

The effect is also a fundamental concept in behavioral economics. Researchers in this field have discovered that individuals tend to be more responsive to potential losses than gains, and this tendency can significantly influence human behavior. In the realm of investments, it can be inferred that people are often inclined to avoid risks. Some individuals are so risk-averse that they concentrate solely on the potential losses associated with a trade, even when the potential gains outweigh those potential losses.

As a result, policy actions following an economic crisis typically aim to prevent the recurrence of the negative events experienced. This may explain why most governments increase regulations after a financial crisis, often overlooking the adverse effects of these policies. For example, despite their intention to enhance consumer well-being, consumer protection measures can inadvertently limit the variety of available goods, leaving consumers with fewer options.

Another illustration is trade policies that protect domestic industries from foreign competition, especially when foreign producers offer similar goods at lower prices. However, the unintended consequences of such protectionist measures include higher prices, reduced variety, and decreased economic efficiency, as they diminish the incentive for domestic producers to innovate.

When considering the impact of the negativity bias on our perceptions of central banks, it becomes apparent that we tend to remember their flawed policies more than their successes. A substantial body of literature exists regarding the causes of various financial crises. Broadly speaking, these studies can be categorized into two groups: those that commend central banks for their swift response in lowering interest rates and increasing liquidity and those that argue that low interest rates and excessive liquidity were, in fact, significant contributors to the crises.

The latter group has consistently expressed disappointment with central banks and their leaders. Concerning the US Federal Reserve, there has been no Fed chair since Paul Volcker was willing to administer the necessary bitter medicine. Even Alan Greenspan, a disciple of Ayn Rand, abandoned his ideological beliefs when he assumed the chairmanship and primarily supported Wall Street during challenging times.

Subsequent chairs, such as Ben Bernanke and Janet Yellen, held little hope for a change in direction. Both favored an active role for the Fed rather than the opposite. The current chair, Jay Powell, was also perceived as inclined towards easy monetary policies based on his actions during the Repo crisis and the pandemic.

In mid-2021, it seemed like the Federal Reserve, the European Central Bank (ECB), and other central banks had decided to keep interest rates low indefinitely. Powell's renomination by Joe Biden reinforced this perception, and expectations among those advocating hard-money policies were at an all-time low. Interestingly, interventionist expectations were equally pessimistic, as they believed that Powell would not do enough to support objectives such as addressing climate change.

However, events in late 2021 caught many critics of the Fed's easy monetary policies over the past four decades by surprise. Firstly, Powell began to shift his rhetoric, officially discarding the notion that inflation would be transitory in November 2021. Yet, even then, most market participants believed that the Fed would respond cautiously and make only gradual increases in interest rates.

As it turned out, the market couldn't have been more wrong. The pivotal moment came when Congress confirmed Powell's reappointment. In a matter of weeks, Powell shifted from a cautiously hawkish stance to an extremely hawkish one. I distinctly remember thinking it was just tough talk and that the Federal Reserve had limited room to raise interest rates. I assumed that at the first sign of a significant drop in the S&P 500, Powell would pivot and return to NIRP.

Powell caught most market participants, myself included, completely off guard. By the summer of 2022, the Fed had raised interest rates from 0-0.25 % to 2.25-2.50 %, with three substantial increases of 75 basis points. During this period, the S&P 500 plummeted by a staggering 23 %, but it rebounded during the summer as market participants speculated that the Fed was nearing the end of its tightening cycle. Until the Jackson Hole symposium, it had risen 17 % from its lows. It was at Jackson Hole where Powell took a page from the Volcker playbook. During his speech, he reassured market participants once again that the Fed was committed to taking any necessary measures to bring inflation back to 2 % and that a significant rate hike was likely on the horizon.

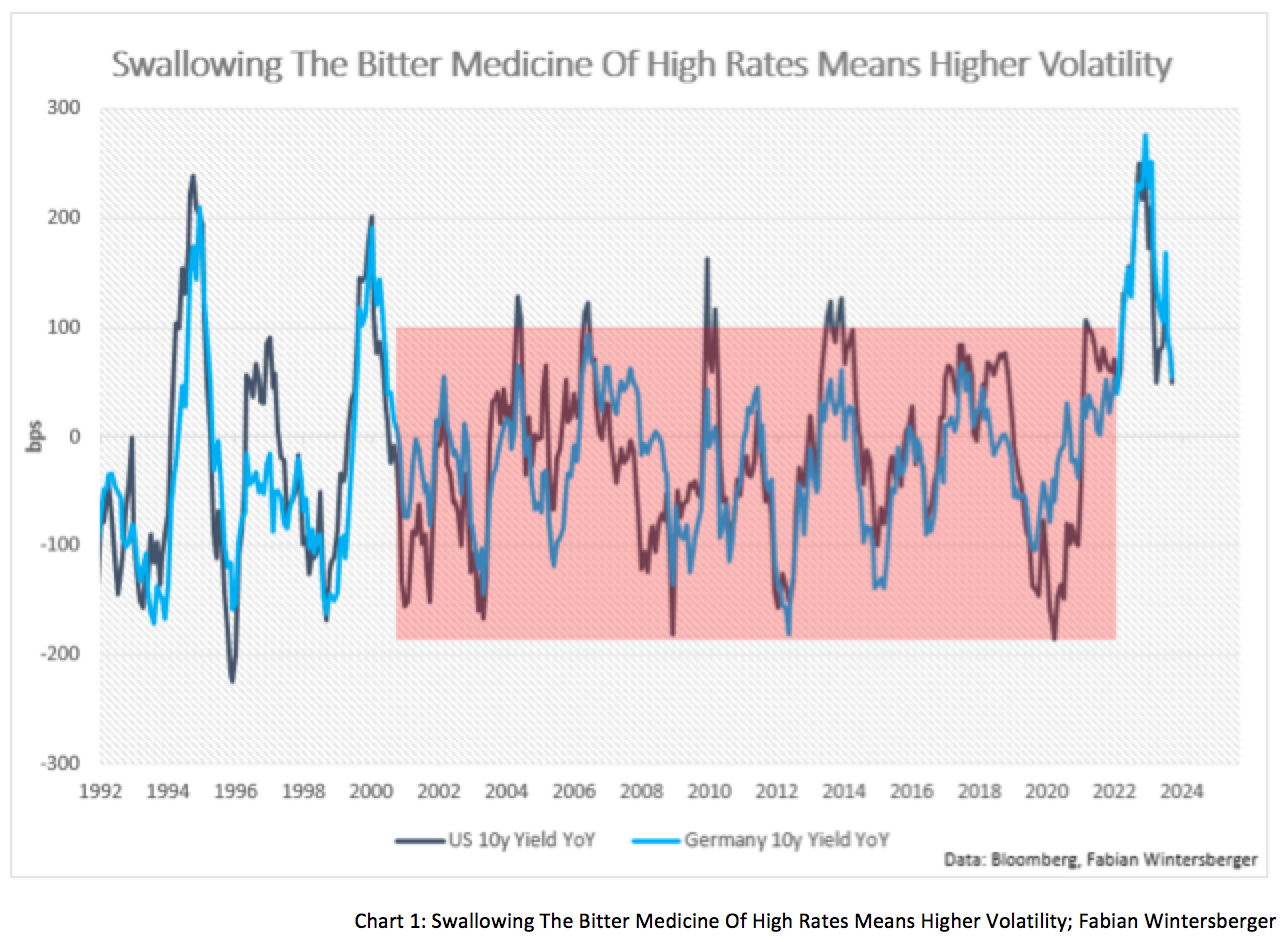

Powell's dismissal of any pivot at Jackson Hole in 2022 marked the end of two decades of artificially suppressed interest rate volatility. The imbalances built up during this period were finally being unwound, and so far, systemic risks had not materialized.

While Powell's actions initially enjoyed support from most Democrats, criticism began to mount in the months following the Jackson Hole symposium as mortgage rates continued to climb due to the Fed's ongoing interest rate hikes. Approximately a year ago, members of the Committee on Banking, Housing & Urban Affairs penned an open letter criticizing Powell for his unwavering stance, but he remained unmoved.

In an article I wrote roughly a year ago titled Breaking the Habit, I pondered whether Powell would finally end the so-called Fed Put. Despite Powell and other Fed members repeatedly advocating for higher interest rates over a more extended period, the market still believes that the Fed will reduce interest rates in the latter half of 2024.

This assumption, combined with surprisingly robust economic data in the US, has buoyed equity indices, mainly due to the stellar performance of the Magnificent 7. Moreover, the swift surge in interest rates has favored businesses that secured long-term funding and are currently parking cash in short-term treasuries. For now, this situation resembles the Fed's effect of lowering interest rates for businesses, although it will change over time as these issued bonds mature and require refinancing.

Consequently, economic growth remains robust, propelling nominal growth upwards and, as is customary, driving interest rates higher. However, another factor is challenging the Fed: the US’s profligate spending. Construction spending has soared thanks to substantial government subsidies for businesses investing in the United States. As I mentioned in Parallels, maintaining deficits at around 7.5% of GDP during an economic expansion is exceedingly high.

Although the data has never supported that assertion, Larry Summers has argued that an aging population leads to a savings surplus. The unwinding of ZIRP is now causing the exact opposite effect. Baby boomers initially benefited from declining interest rates from 1980 to 2021, along with asset appreciation. Now, they are reaping the rewards of higher rates due to increased interest income. Consequently, they account for approximately 22 % of consumer spending, a substantial 8-percentage point increase since 2005.

Friedrich von Hayek once stated that if central banks were to adopt a more stringent monetary policy, production patterns would shift from capital goods (higher-order goods) to consumption goods as consumer preferences change (shifting to goods of lower order). This is precisely what we're witnessing in today's economy: while the capital goods sector faces challenges, the consumer goods sector demonstrates greater resilience. However, these shifts are far from fully integrated into economic activity, as loose monetary policies have created imbalances that have yet to unload fully.

Now, it is paramount to consider how the Fed will respond if stocks begin to decline, as I anticipate they will in the coming months. Just as Powell abandoned the notion of "transitory" inflation about two years ago, he should now distance himself from comparisons to Paul Volcker.

As I mentioned in the introduction, a great deal has been written about the 1929 stock market crash and the Great Depression, as the consequences were catastrophic for both financial markets and the economy. While some monetarists contend that the depression resulted from insufficient action by the Fed after the crash, others argue that government intervention was necessary to sustain economic activity. However, Powell should not focus on 1929; he should examine what William P.G. Harding did in 1920-1921.

Because just as everyone recalls 1929, hardly anyone remembers the depression of 1920/21, often referred to as The Forgotten Depression. During that time, the government deficit was at a record high due to World War I, and inflation surged in the following years. Then, in 1920, the economy suddenly took a downturn, and unemployment spiked dramatically. I believe that if Powell truly wishes to leave a mark in history, he should closely scrutinize what transpired next. Before the crisis hit, unemployment stood at 4 %, a rate similar to today.

Focusing solely on the most recent change in nonfarm payrolls published last week, the labor market appears robust. In September, payrolls increased by 336,000, surpassing the estimated 187,000, contradicting the previous Wednesday's ADP report. This prompted the market to celebrate the positive numbers without delving into the underlying details.

EJ Antoni from the Heritage Foundation delved into the report and concluded that the labor market is not as strong as it may appear. There are still 5 million fewer people in the labor force compared to pre-pandemic levels. Adjusted for this, the actual unemployment rate falls more in the range of 6.3 % to 6.8 %. Furthermore, as Antoni pointed out, 22 % of all jobs created were government positions or roles that require support from the private sector.

Additionally, all the jobs added were part-time, while full-time positions were lost. This trend significantly contributes to the sluggish wage growth, leaving real weekly earnings nearly where they were in June 2022. I concur with Antoni that the underlying economic fundamentals remain weak. Moreover, I would argue that we might see further downward revisions of these figures and that the labor market will continue to deteriorate in the coming months.

Similar circumstances transpired before the recession of 1920, which ultimately evolved into the depression of 1921. Depending on the estimation, unemployment stood at around 1.4 % or 3 % in 1919. Suddenly, however, unemployment surged to 5.2 % in 1920 and 8.7 % to 11.7 % in 1921.

Observing statistics like these, one might assume that the Fed would have stepped in, lowering interest rates and the government increasing the deficit to combat the recession, as has been the case in more recent recessions. However, despite Herbert Hoover urging President Warren G. Harding to intervene, the US government and the Fed, under the leadership of William P.G. Harding, took the opposite approach.

Instead of "fiscal stimulus," Harding cut the government's budget nearly in half between 1920 and 1922. The rest of Harding's approach was equally laissez-faire. Tax rates were slashed for all income groups. The national debt was reduced by one-third. - Tom Woods

Could you imagine a scenario where the government cuts spending during a recession that eventually spirals into a depression? Such a prospect seems nearly unthinkable today, regardless of whether a Democrat or a Republican resides in the White House. On the contrary, things have escalated to an extent over the years that the current Biden Administration has embarked on a spending spree during the most recent economic expansion.

The situation becomes even more intriguing when we delve into the actions taken by the Federal Reserve, which was still in its formative stages during that period. Between 1917 and 1920, the Fed increased the discount rate from 3.75% to nearly 5%. Then, when the recession of 1920 began, the Fed continued to raise rates, eventually reaching 7 %. These rates were maintained for approximately ten months, effectively transforming the recession into a full-blown depression. Money supply growth stood at about 20 % at the outset of 1920, only to contract by a staggering -8.7 % by September 1921.

In January 1921, industrial production had plummeted by 30 % compared to January 1920. Despite these staggering figures, neither the government nor the Federal Reserve came to the rescue. Yearly inflation had dropped from about 24 % in June 1920 to approximately -16 % in June 1921. Despite this severe deflation, the Fed remained on the sidelines, allowing the free market to operate, which, according to interventionists, was expected to result in a downward spiral and a prolonged depression.

However, this is precisely what didn't happen in the United States, in contrast to what occurred in Japan. Japan also faced a severe recession during that period and attempted to combat it through extensive government intervention. Japan battled deflation and abandoned the free market, but as a consequence, it endured years of industrial stagnation, eventually leading to a banking crisis in 1927.

In the effort to avert losses on inventory representing one year’s production, Japan lost seven years – Benjamin Anderson

Allowing the free market to operate proved to be the correct course of action in the United States. The initial signs of recovery were already discernible in the latter part of 1921, and the unemployment rate began to decline significantly, reaching 2.4% in 1923. As the economist Benjamin Anderson aptly noted:

The rally in business production and employment that started in August 1921 was soundly based on a drastic cleaning up of credit weakness, a drastic reduction in the costs of production, and on the free play of private enterprise. It was not based on governmental policy designed to make business good.

While there is a valid argument that such a policy could potentially result in a catastrophic outcome due to the unprecedented levels of debt relative to GDP, it's worth remembering that a similar concern existed in 1920. Admittedly, the debt-to-GDP ratio was much lower at that time, but even so, the 30 % debt-to-GDP ratio was considered exceptionally high by the standards of that era.

It's worth remembering that failing to repay debts may temporarily impede future goods production, but the goods already produced don't vanish; they merely change hands. This is why the economy rebounded quite rapidly in 1921. Prices and wages adjusted, and the market naturally corrected itself.

Whether Jay Powell will have the courage to withstand the calls for intervention and a return to easy monetary policy if he genuinely intends to follow the Harding playbook is uncertain. To be honest, I'm not sure. Still, if his goal is to eliminate the Fed Put, it should entail something along those lines. The BTFP implemented during the regional banking turmoil this fall suggests it might involve a mix where the Fed attempts to mitigate the effects on financial markets. Whether this strategy will be successful remains to be seen.

In my view, the Fed is done with raising interest rates but may shift its focus to how long rates will remain at their current levels. I suspect it will try doing that for an extended period, much like the William P.G. Harding Fed did in 1920. However, it's essential to understand that this won't result in a seamless economic transformation. As Jerome Powell mentioned last year, there will be some challenges.

The stock market is in a unique situation because if the Fed maintains rates at these levels, equity prices will need to come down. Should the Fed change course and lower rates, history suggests they will continue to drop until they reach the low point of the cutting cycle. Panic could ensue when it becomes apparent that the Fed won't rush to rescue the stock market in case of a crash, and the real economy is holding up better than expected due to improved household balance sheets.

Another factor to consider is that, unlike Harding, the US government has no plans to reduce spending. The only scenario that might compel such action is if the Fed remains resolute in maintaining high interest rates. Some commentators have already broached the possibility that this could be Powell's next move.

Personally, I wouldn't rule it out, especially given what has transpired over the last 1.5 years. After 2019, hopes for Powell to be the Fed chair who abolishes the Fed put and raises rates to a level where the market can self-adjust were at an all-time low. Since then, Powell deserves credit for his actions, even though, as he often remarks, the job is not done yet.

Let's hope that if he succeeds, he won't be forgotten like William P.G. Harding.

Lost in a sea of sadness,

Blind in this place of darkness

If I fall, would you be there to raise me up

Or will I be the forgotten one?Times of Grace – The Forgotten One

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

(Please note that all posts reflect my personal opinions and do not represent the views of any individuals, institutions, or organizations I may or may not be professionally or personally affiliated with. They do not constitute investment advice, and my perspective may change in response to evolving facts.)