Not Falling

What's driving inflation and what's its future trajectory?

Rising prices or wages do not cause inflation; they only report it. They represent an essential form of economic speech, since money is just another form of information. – Walter Wriston

That week was dominated by inflation numbers that again shook the trajectory of various markets. We got the US CPI for January on Wednesday, and the final numbers for Germany and the UK followed on Thursday.

And again, the US inflation numbers meddled with the trajectory of various markets. However, the changes began with Friday's Nonfarm Payroll Report. In last week's "Weekly Wintersberger," I wrote:

Long-term interest rates could have more downsides, especially since US job openings were below expectations this week, but rates continued to decline. We'll see if the new NFP report on Friday can change the yield trajectory.

The numbers were mixed. The US economy added 143,000 jobs and missed analysts' expectations, who expected job growth of 175,000. Nevertheless, the unemployment rate fell from 4.1% to 4.0%, while economic forecasters expected no change. As a result, the initial drop in yields was quickly erased, leading to a rise in US long-term interest rates that closed only slightly lower.

Again, this underscores that the US economy is far from weakening and remains solid. At the moment, nothing suggests it might face severe troubles in the first half of this year. Hence, the Fed can stay very relaxed on its "full employment" mandate.

Optimism among small businesses remains at expansion levels as well, albeit the first euphoria around the re-election of Trump seems to fade a little bit. On Wednesday, the NFIB Small Business Optimism Index was released and showed a decline from 105.1 to 102.8 (exp. 104.7). However, the report's comment indicates that there's still widespread optimism:

Small business owners greeted the new year with a surge in optimism. Seventeen percent (seasonally adjusted) now view the current period as a good time to expand substantially, up from just 4 percent a few months ago... The economy enters 2025 in decent condition but with a slowing momentum.

To summarize, things point to a normalization, but nothing beyond that. Unemployment remains at record lows, and business optimism is good. However, regarding the inflation front, the situation is slightly different, as Wednesday's CPI numbers proved.

Again, inflation was hotter than analysts (including me) expected. Before the release, many inflation doves mentioned the alternative index "truflation" as a sign that inflation would drop further. Starting in February, this measure dropped substantially from 2.8% YoY inflation to almost 2%.

One has to see whether the BLS CPI measure follows going forward, but it definitely didn't happen in January. On the other hand, the BLS's January number is always a bit tricky to use when assessing the future trajectory of inflation because of all the weightings readjustments from the Bureau of Labor Statistics.

In January, inflation rose by 0.5% compared to the previous month, substantially more than analysts estimated, who estimated an increase of 0.3%. Core inflation rose 0.4% instead of the expected 0.3%. Just like in 2022 and 2023, the Fed has yet to grapple with another inflation surprise.

A quick look at the inflation chart shows that the Federal Reserve's progress on inflation has remained limited over almost two years. Year-over-year inflation is rotating around 3%. Annualized quarter and half-year numbers are also pointing in different directions. The 6-month annualized CPI has been accelerating since November, and the 3-month annualized CPI has accelerated from July onwards.

All these data points suggest that the Fed made a substantial mistake in September 2024 when it reduced interest rates by 50 bps and lowered them again in October and December. On the surface, these interest rate cuts seem to have started impacting inflation immediately.

The rise in inflation looks surprising from a monetarist perspective, which says that inflation is always a monetary phenomenon. According to them, inflation will follow prior changes in the quantity of money. As inflation remained significantly above the Fed's 2% goal, I argued that the lag of monetary policy seems to have widened after Covid.

However, one must remember that inflation and other economic numbers are difficult to assess, interpret, or forecast. If one solely looks at changes in the money supply, one could easily fall into the "linearity trap" where one thinks that changes in one data point can largely explain another. The current inflation trajectory disproves that simple thinking again.

What do I mean by that? Price changes are subject to a wide variety of variables. The money supply is a substantial factor in determining whether the rise in inflation is sustainable. However, I believe other factors outweigh the money supply over the short term.

One is money demand, the inverse measure of velocity, which measures how quickly money is exchanged for goods and services. Money demand is high (velocity is low) when people prefer to hold money instead of spending it, and vice versa.

Moreover, I'd categorize "money demand" broader than most academics, including assets that serve an original "monetary purpose." For example, financial assets or real estate are nowadays a form of saving, as their price gains outweigh the losses caused by the devaluation of money.

If one uses this definition, it becomes clear that the reason why inflation didn't go down despite the contraction of the money supply is falling money demand (rising velocity). Interestingly, money velocity started to rise in early 2022, just when the consolidation of money supply growth ended, and the growth rate of money began to fall again.

That is in line with the observation that economic activity in the real economy remained high due to re-shoring, higher investment into the real economy, and low unemployment. When money remains in "money-like" areas, it doesn't affect inflation, but as soon as people start to sell or use the cash flow of fixed income to spend it on goods and services, the demand for goods and services, and hence prices, increases. Rising velocity outweighed the contraction of the money supply.

Further, the primary source of short-term inflation movements is the buying and selling of goods and services: supply and demand. The willingness to sell and the willingness to buy, which determine the price, are shaped by expectations. If inflation has been high, producers who experience cost increases will set their lowest price to sell higher.

Buyers will either have to adjust to specific price increases and continue buying, depleting their savings or cutting spending on certain products. During that period of price discovery, inflation could remain high, and only a drop in demand or additional supply can bring prices down again.

In addition, the BLS's weightings and hedonistic adjustments influence the measured inflation rate because they must create an "average rate" of inflation. Therefore, I suggest ignoring the noise and concentrating on the longer-term trend.

Based on that, I think that it is too soon to say that inflation is making a comeback, even though shorter-term measures of inflation, like 3-month and 6-month annualized inflation, are pointing to further increases. For now, velocity has stabilized, and money supply growth has just returned to 2010s levels.

Nevertheless, the road could remain bumpy. Unexpected supply chain issues, rising velocity and economic activity, or increased competition to find workers due to the low unemployment rate could be tailwinds for inflation. If that channels money away from "money-like" assets, stocks and bonds could suffer, and velocity could rise further.

Money supply growth will affect the inflation rate over a longer time frame; hence, I'd say that inflationary pressures on that front remain subdued for now. It's not unlikely that this week's inflation increases will suffer the same fate as those in the last two years when inflation continued to trend lower after the January inflation surprise.

If one looks at what happened in financial markets this week, the stock market regained the losses it suffered from the high CPI, which suggests that US stocks will follow the DAX further, which again reached another all-time high.

Bonds faced a trend change, with the sell-off beginning one day before the US CPI numbers were released. The market's inflation expectations were right, and "truflation" was wrong. US 10-year Treasuries couldn't break out, and the increasing worries about inflation will be a further headwind.

Any more bond-negative news next week could push the price of Treasuries lower, and Bunds will probably follow them after an initial consolidation phase. The overall picture has darkened as inflation worries persist and growth could remain strong. Silently, the US is also on course to raise the debt limit and cut taxes, which could support growth and interest rates.

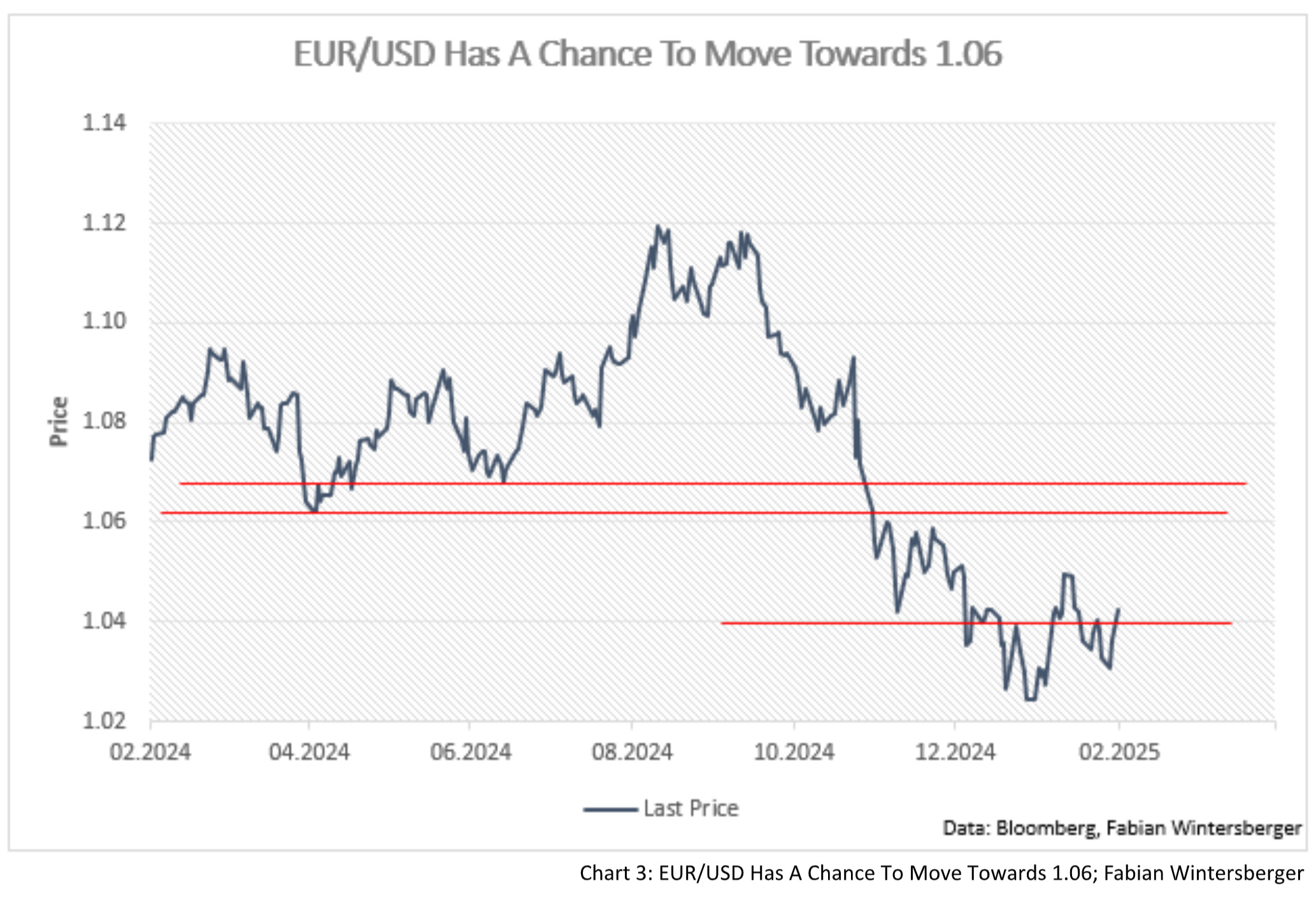

The euro appreciated against the dollar and is still around 1.04. As Trump tries to bring the dollar down, the euro seems to be approaching a phase of strength if it can sustainably climb above 1.045. Then, a rise to 1.05 and beyond is a possibility.

Gold continues to be strong and trades around last week's all-time high despite worries that yields could stay higher for longer. Recent news about increasing demands for physical delivery suggests that there could be a further tailwind for the price.

Oil started consolidating at the beginning of the week but lost all those gains after the CPI release. The price is now close to the $70 resistance, and a further decline could mean that the downward trajectory isn't over yet. Fundamentally, I think more things point to a lower oil price than a higher one.

Last week, I wrote that copper might break out, which it did. Copper Futures are currently trading around the October 2024 highs of $470. If it passes that resistance, prices could also increase towards $500.

To summarize the week, stocks, gold, commodities, and interest rates are similar: they are not falling. Continuously high interest rates could be the central theme for the coming weeks, which means that bonds are not the place to be at the moment.

I, I stand, not crawling, not falling down

I, I bleed, the demons that drag me downMudvayne - Not Falling

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you shared it on social media or gave the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. They do not constitute investment advice, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.