Four Years

Today is already the tomorrow which the bad economist yesterday urged us to ignore.– Henry Hazlitt

In January 1973, the Vietnam War ended, and a few months later, the Bretton Woods System collapsed. Throughout this period, Europeans learned a challenging lesson—Americans primarily prioritize their interests:

In that system, the dollar was as good as gold, and one ounce of gold could be exchanged for 35 US dollars. Until 1971…

Economist Jeffrey E. Gartner, author of the book Three Days at Camp David: How a Secred Meeting in 1971 Transformed the Global Economy, described the events as follows:

When the Nixon administration came into office in 1969, they realize that the world economy had grown very, very big. Everybody wanted dollars, so the Federal Reserve was printing lots of dollars. As a result, there were four times as many dollars in circulation as there was gold in reserves…by 1971 the dollar was really overvalued. That meant imports were very cheap, and exports were very expensive. [The US] experienced our first trade deficit since the 19th century. We were experiencing employment problems. For the first time, the U.S. started to talk about losing competitiveness.

In the quoted interview, there is another point that many policymakers in Europe seem to neglect nowadays: how the United States, or States in general, make policy. One of the participants in the secret meeting at Camp David was John Connally, secretary of the Treasury. Garten continues [emphasis added]:

Most people in that period were very sympathetic to the existing global financial system. It had been extremely successful. Most people would have been very hesitant to take a sledgehammer to it. Connally had no hesitation to sever the link between the dollar and gold. He had no hesitation doing anything if he thought it would benefit the U.S. He just didn’t care about the rest of the world and Nixon knew that.

Currently, Europe finds itself revisiting a familiar lesson as Joe Biden announces a pause in export approvals for Liquefied Natural Gas (LNG). While the Biden administration cites environmental concerns (likely seeking support from environmentalists for upcoming elections), a more pragmatic motive could be the effort to maintain affordable domestic energy prices.

Although there are no immediate consequences for European countries relying on LNG imports from the US, especially those who have moved away from Russian natural gas imports, European leaders should view this as a cautionary sign that the US may prioritize its political interests over EU partnerships.

Shifting the focus to financial markets and the economy, the situation remains challenging to interpret. Some published economic data appears robust, while other indicators suggest underlying weaknesses are growing.

Economically, a divergence persists between the US and the Eurozone. While the US demonstrates signs of resilience, the European economic landscape continues to appear bleak. Real GDP data indicates that the Eurozone economy essentially stagnated in 2023, with a mere 0.1% growth. Germany's economy contracted in Q4, though the third quarter saw a slight upward revision from -0.1% to 0%.

France experienced a 0.7% year-over-year GDP increase, aligning with expectations, while Spain and Italy surpassed forecasts. Italian GDP grew by 0.5% year-over-year, exceeding expectations by 0.3 percentage points, and Spanish GDP reached 2%, beating expectations by 0.4 percentage points. However, delving deeper into these figures suggests a need for cautious interpretation rather than a straightforward signal of economic strength in these countries.

Italian wage data for December displayed remarkable strength, with hourly wages growing by a staggering 7.9% compared to the previous year. However, the Italian National Statistic Office attributes this surge primarily to a significant increase in public administration wages, which rose by 22%. Consequently, government expenditures appear to be a substantial driver behind the higher-than-expected GDP growth.

In Spain, the GDP increase is also predominantly attributed to a growth in government expenditures. Compared to Q4 2019, private consumption remains unchanged, while public consumption has risen by more than 10% since Q4 2019. Despite appearing advantageous in the short term, the faster growth of Spanish government debt compared to GDP raises concerns. This dynamic may lead to challenges when economic growth eventually stalls again, resulting in higher debt-to-GDP ratios.

Consequently, it seems unlikely that any single country could compensate for the decline in German economic activity in the foreseeable future. Recent retail sales figures for Germany indicate a -4.4 % decrease compared to the previous year. At the same time, services activity has declined for four consecutive months at an accelerating pace, according to the latest PMI numbers. Furthermore, the survey signals weakening demand, suggesting that the recession is not likely to dissipate soon but rather intensify.

The economic trajectory of the Eurozone will increasingly impact the European Central Bank's (ECB) monetary policy. In the recent governing council meeting, interest rates were maintained at current levels. Despite this, ECB President Christine Lagarde expressed optimism regarding economic activity, indicating an expectation for improvement in the situation:

The euro area economy is likely to have stagnated in the final quarter of 2023. The incoming data continue to signal weakness in the near term. However, some forward-looking survey indicators point to a pick-up in growth further ahead.

Lagarde highlighted the Eurozone's robust labor market and reiterated the need for governments to scale back support measures to mitigate inflationary pressures. Notably, the strength of the labor market owes much to government support schemes, potentially hindering labor mobility and efficient worker allocation as individuals remain tied to unproductive workplaces.

Should the ECB's assumption of an economic activity upswing prove incorrect, Lagarde's call for reduced government spending may lose its footing. In such a scenario, governments are more likely to press the ECB for substantial intervention, even if inflation has not reached the 2% target. I anticipate more and possibly earlier rate cuts this year than the market currently expects.

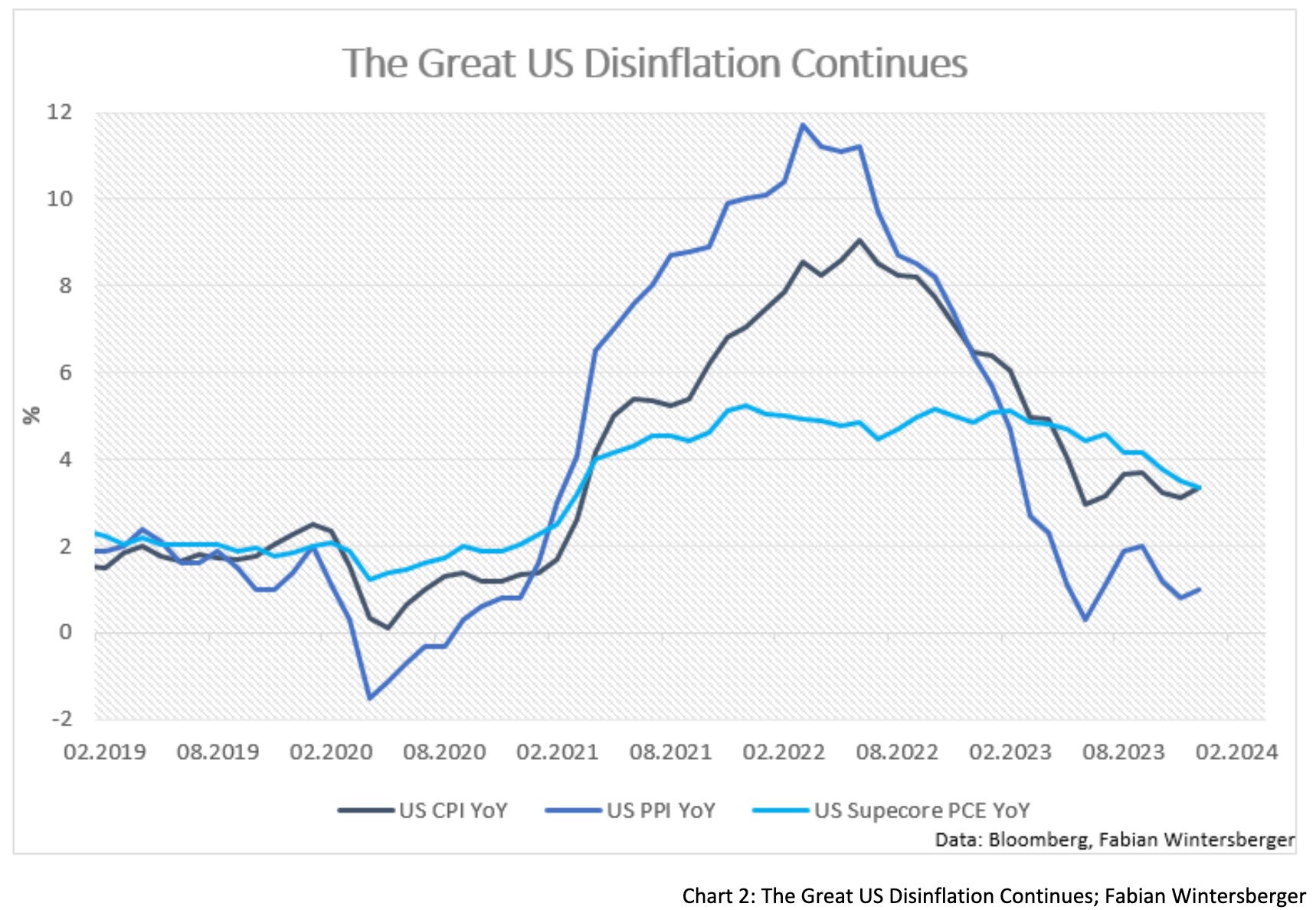

Concerns have arisen about a potential resurgence in consumer prices, particularly among those who believe that the money supply has minimal influence on inflation rates. This anxiety intensified as Spain's inflation rate unexpectedly climbed to 3.4% in January, surpassing expectations by 0.4 percentage points. However, this increase is likely attributed to the phase-out of tax breaks implemented during the energy crisis.

Overall, January's inflation figures align with the trends suggested by the evolution of the money supply—continuous disinflation, likely stemming from economic weakness. While ongoing geopolitical developments might introduce some volatility due to emerging imbalances, the unmistakable trend is downward, although Eurozone HICP was slightly above expectations at 2.8% year-over-year.

The decline in consumer price inflation and steadfast nominal interest rates will further tighten bank credit by translating into a rise in real interest rates. Investment activity in the Eurozone appears increasingly at risk, exacerbated by the EU and its members' reliance on extensive regulation. It seems that EU officials believe comprehensive regulation provides a competitive advantage over other economic regions.

The unfortunate reality, however, is that regulation is the sole domain where Europe currently holds a leading position. In a recent opinion piece in the Wall Street Journal, Greg Ip stated:

Never before has “America innovates, China replicates, Europe regulates” so aptly captured each region’s comparative advantage.

In the case of Germany, which strives to be at the forefront of the Green Transition, there appears to be a funding gap for renewable energy in 2024 despite having a clear strategy. The Frankfurter Allgemeine Zeitung reported that this shortfall may exceed double the expected amount, reaching 17 billion euros. The bottom line is that, despite record government spending, there still seems to be a shortage of funds—a risky situation, especially when economic activity is contracting.

In contrast, the situation in the US remains much more favorable than in Europe. While European manufacturing is contracting, the Inflation Reduction Act has attracted investments due to guaranteed subsidies, and it continues to drive manufacturing construction. Over the past 12 months, construction spending by manufacturers has doubled. It appears that the US is, in a way, benefiting from the economic policies of the EU, supporting the remarkable resilience of the US economy.

S&P Global US PMIs are still in expansionary territory, although other manufacturing indices recently surprised significantly on the downside. The Richmond Fed Manufacturing Index and the Kansas City Fed Manufacturing Activity fell short of expectations. Regional manufacturing surveys indicate a potential further decline in the ISM Manufacturing Index.

Various indicators continue to send mixed signals, providing fodder for pessimists and optimists, as each can selectively choose data to support their narrative. While some manufacturing data suggests increasing weakness, the labor market remains tight and supportive. Initial jobless claims and continuing claims remain low, and job opening numbers were stronger than expected.

However, quit rates suggest a slight cooling in the labor market, falling to the lowest monthly level in three years (seasonally adjusted). A decline in worker resignations implies they may find it harder to secure higher-paying jobs elsewhere. Consequently, the drop in the Employment Cost Index this week was anticipated, suggesting that the fear of a wage-price spiral remains more fiction than reality.

Personal Consumption Expenditures remain unchanged from a month earlier at 2.6%, with core PCE slightly down on a year-over-year basis. Powell's preferred measure, core PCE Services excluding Housing, continues to decline. I still see no likelihood of inflation re-acceleration despite the notion that money demand has fallen, or, in other words, money velocity has picked up a bit.

Fourth-quarter GDP was another robust beat at 3.3% annualized compared to the expected 2%. Strong GDP growth with falling price pressures suggests that there is likely no imminent drop in the broader stock market, although some small caps have faced challenges recently, as seen in the weak Russell 2000.

Nevertheless, it is noteworthy that the Q4 GDP number appears again to be a result of excessive government spending. In Q3, the budget deficit was slightly higher than nominal GDP; in Q4, nominal GDP was 328.7 billion dollars. In comparison, the budget deficit rose by 509.9 billion dollars, meaning that GDP was only 2/3 of the budget deficit.

Another aspect to consider is that the high real GDP number is influenced by the low GDP deflator, which was surprisingly 1.5% this quarter compared to 3.3% last quarter, roughly in line with the 3-month annualized CPI. While statistically, this assumption seems correct statistically, it's important to note the various adjustment methods in the background that tend to understate the real general price level.

Despite these considerations, as this is the available data, one must work with it, suggesting an extremely resilient US economy, especially when compared to Europe. Consequently, the FOMC decision and press conference this week were highly anticipated.

As expected, the Fed left interest rates at current levels. Although the opening statement underwent significant changes, the main message remained consistent—indicating that the economy continues to expand, the labor market remains resilient, and the Fed will assess upcoming data to determine its future course of action.

Chairman Powell reiterated the need for further evidence that inflation is returning to the Fed's 2% target. He emphasized that it is premature to speculate about the timing of the first cut. Surprisingly for many, he categorically ruled out the possibility of a rate cut in March.

While interest rates experienced minor movements during the press conference, they closed relatively unchanged compared to pre-FOMC decision levels. In contrast, the stock market dropped, with the S&P 500 down approximately 500 points. Gold also saw a slight decline, presumably due to Powell's dismissal of a March cut.

Concerning the current data, this assessment appears accurate, but it remains contingent on developments until March to draw a final conclusion about whether it was a mere bluff. Nevertheless, if the past two years have demonstrated anything likely, one should not underestimate Jerome Powell.

This week, the Fed announced that it will conclude its Bank Term Funding Program on March 11, as planned. However, in light of Wednesday's news, it seems some banks might require support for a longer duration.

New York Community Bancorp’s decisions to slash its dividend and stockpile reserves sent its stock down a record 38% and dragged the KBW Regional Banking Index to its worst day since the collapse of Silicon Valley Bank last March.

Therefore, I anticipate that economic conditions will persist in being challenging and possibly worsen in the future. However, the deceleration in the US is likely much less pronounced than the sustained downturn in the European economy. Positive developments in Europe remain elusive, reinforcing my expectation that the ECB will act before the Fed.

Short-term bonds still appear compelling due to their limited downside, but it also seems that duration could benefit in the weeks and months ahead, especially in Europe. With both the ECB and the Fed adopting a more cautious stance, I align with the belief that the currently priced-in rate cuts are insufficient, a viewpoint supported by the ongoing downtrend in inflation.

What implications does this hold for the stock market? Honestly, I maintain a more neutral stance, but the chart patterns of US and European indices continue to present a challenge to bearish sentiments. The market's uncertainty about the trajectory of rate cuts opens the possibility that weaker-than-expected data in the future could drive prices even higher, in my opinion.

Gold surprised everyone last year by remaining relatively unaffected by rising real yields. Therefore, I would posit that, from an investing perspective, it still makes sense to allocate funds to gold. The rationale behind this lies in the fact that even if central banks refrain from cutting interest rates, the downside for gold is likely limited because sustained government spending cannot indefinitely support GDP. Conversely, monetary policy should benefit gold if it takes a more expansionary turn,

Regarding currencies, my preference continues to lean towards the dollar against other currencies, excluding the yen. However, the yen might emerge as a significant story later in the year, so I believe there's no immediate rush to enter into a trade at the moment.

Currently, the US economy appears to maintain its resilience moving forward, although some clouds are beginning to appear on the horizon. Nevertheless, four years into the third decade of the 21st Century, exercising caution about the future is not unwarranted. Implementing proper risk management will continue to be crucial!

Sometimes I'm just holding on to all the good times that we've spent

I never quite knew what they meant (holding on)

I hold my heart to the sun, this dream is what I've become

Ever closer, please don't wake me upBuried In Verona – Four Years

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

(Please note that all posts reflect my personal opinions and do not represent the views of any individuals, institutions, or organizations I may or may not be professionally or personally affiliated with. They do not constitute investment advice, and my perspective may change in response to evolving facts.)

and all this was before today's blowout NFP! as I continue to write, the data is a Rorschach test for whatever you want to make it. but I agree that Europe will continue to fare far worse than the US