Prey

I believe and I say it is true Democratic feeling, that all the measures of the Government are directed to the purpose of making the rich richer and the poor poorer.

William Henry Harrison, 9th President of the United States

A golden key can open any door, one says. Although, things are a bit more complicated than that. After all, it is the state that legislates. But because the state is throwing around more and more money, the more one could conclude that there is something correct with that saying. However, different than most would assume.

Discussions about money are everywhere, no matter if one has it or if one has not. Nevertheless, we know so little about money. What is money? Even economic science cannot indefinitely answer that question. Yet, most people agree that money needs to be divisible, a store of value, and generally accepted.

Over the years, the influence of the state on money production has increased, partially because of the increasing number of laws and regulations. Still, even most proponents of laissez-faire would agree that there has to be a state that determines the economic framework, although most would say that the current state intervenes way too much nowadays.

If there is one characteristic of money to highlight, it probably makes the trade of goods and services more accessible. It was no other than Adam Smith, the founding father of economics, who realized that money is an important, if not the most important, characteristic of a modern economy with a great division of labor. Smith wrote in Wealth of Nations that money enabled this when the economy transitioned from a barter economy to a money economy. That barter was pre-existent, so to speak.

However, anthropologists would disagree with this thesis. They argue that there are no signs that something like a barter economy existed. Moreover, they say, the common pre-historic economy can be characterized as a gift economy.

Imagine you are a baker, and your neighbor is a butcher. One day, you smell that he is grilling some steaks and your appetite for steak increases. A few days ago, you brought some bread over. You visit him and start a conversation. Within the conversation, you tell him about the smell of the steaks and how delicious they look. As a result, the butcher asks you if you want some, as he has plenty. According to anthropologists, that is how the pre-historic societies worked. One helped the other out without a quid pro quo.

Is this disproving the theory of Adam Smith? At first sight, one tends to say yes. Second, however, it is not so easy. Firstly, pre-historic societies were organized in small groups, which means all trade partners knew each other rather well, more or less. The question is, would they trade similarly with an unknown person?

Here, catallactics comes into play. The term is not well known among economists, as it does not appear to people who study at universities. Once upon a time, theologists Richard Whately proposed the term instead of political economics. Later, the term was primarily used by proponents of the Viennese school of economics, especially Ludwig von Mises.

Catallactics describes the free interaction of people on markets. Implicitly, catallactics also means making the enemy your friend. That people can finish a specific trade without knowing each other or sharing the same goals.

Then, Adam Smith’s theory makes more sense because an intermediary good to trade makes trade with unknown people easier. The fact that there was no barter society in ancient history is unimportant. More important is whether an economy with a high division of labor existed before money was invented. According to the current state of knowledge, the answer would be no.

From this perspective, it is unsurprising that money emerged as an intermediary medium of exchange to enable trade with strangers and increase the marketability of goods produced. Increasing acceptance of a particular medium of exchange eventually caused the ruling class to declare it the common currency.

At this point, the influence of the state on money started, as it always tried to bend the rules in its favor. Significantly, one should add the history of money is directly linked to the history of credit. The classical liberal idea that loans are financed with savings never existed. Yet, one cannot dismiss that even back then, the wealthy (big business) and the ruling class entered a symbiosis to form the economic system as they imagined.

Over that time, which lasted for several decades, international trade grew substantially. Something that we know under the term globalization nowadays. The first height of globalization was the early 20th century until it ended abruptly with the beginning of the first world war.

The war changed everything. Instead of freedom and openness, resentment and protectionism arose, which finally ended in another world war. After the second world war, global trade was literally down and out. In Bretton-Woods, New Hampshire, nations came together to shape a new trade and currency system to revive it. That was when the dollar standard emerged, with the US dollar at the center of international trade.

In that system, the dollar was as good as gold, and one ounce of gold could be exchanged for 35 US dollars. Until 1971…

Economist Jeffrey E. Gartner, author of the book Three Days at Camp David: How a Secred Meeting in 1971 Transformed the Global Economy, described the events as follows:

When the Nixon administration came into office in 1969, they realize that the world economy had grown very, very big. Everybody wanted dollars, so the Federal Reserve was printing lots of dollars. As a result, there were four times as many dollars in circulation as there was gold in reserves.

…by 1971 the dollar was really overvalued. That meant imports were very cheap, and exports were very expensive. [The US] experienced our first trade deficit since the 19th century. We were experiencing employment problems. For the first time, the U.S. started to talk about losing competitiveness.

In the quoted interview, there is another point that many policymakers in Europe seem to neglect nowadays: how the United States, or States in general, make policy. One of the participants in the secret meeting at Camp David was John Connally, secretary of the Treasury. Garten continues [emphasis added]:

Most people in that period were very sympathetic to the existing global financial system. It had been extremely successful. Most people would have been very hesitant to take a sledgehammer to it. Connally had no hesitation to sever the link between the dollar and gold. He had no hesitation doing anything if he thought it would benefit the U.S. He just didn’t care about the rest of the world and Nixon knew that.

The rest is history. Nixon closed the gold window on August 15, 1971. The world adjusted from a dollar to a fiat standard. The US could use the dollar supremacy without limits, especially after Kissinger’s deal with the Saudis to trade oil exclusively in US dollars.

A variety of things that happened in that period are widely discussed. On the one hand, the fiat standard enabled central banks to fight every economic downturn by expanding the money supply. On the other hand, nations could fight the downturn with increased government spending, which pushed deficits higher while the cost of debt and interest decreased further.

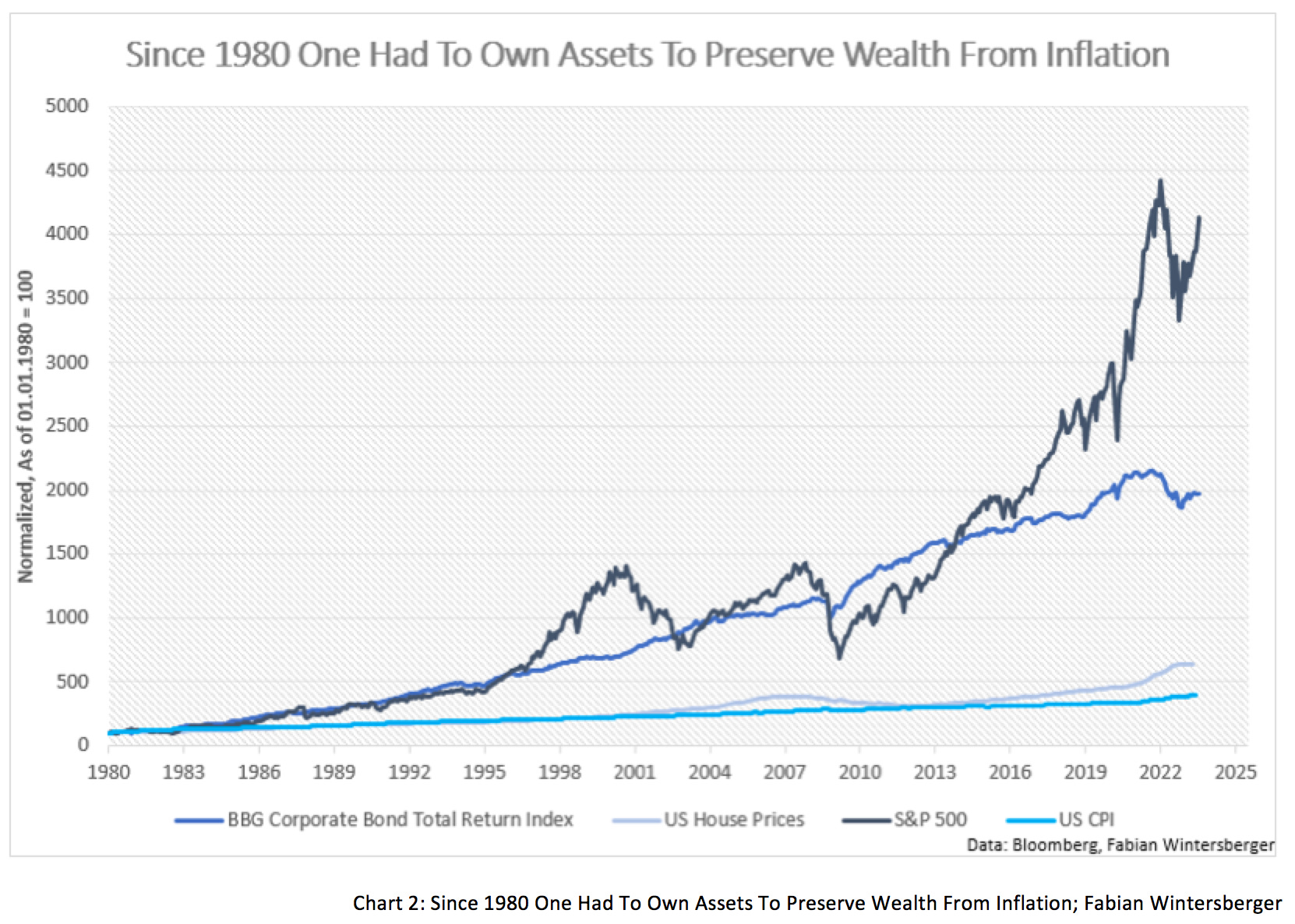

Another widely discussed aspect is the transition to the fiat standard, and the increased government spending became the start of a success story for global bond and equity markets. As interest rates edged lower since 1980, assets rose in value.

If one started investing in asset markets in 1980, one could multiply one’s capital, which led to the notion that everybody who wants to gain wealth must invest money in the stock market. As history since 1980 shows, one can only become wealthy if one invests in the stock market and, more importantly, can secure it from the dangers of inflation.

However, I want to discuss another aspect than the bubbles that central banks created or that the debt got out of hand. Let us remind what I wrote in the beginning about the functions of money. Money should be divisible, a store of value, and generally accepted.

JP Morgan once said that gold is money, and everything else is credit. Gold has contained purchasing power for millennia. An ounce of gold in ancient Rome bought the finest clothes, a Toga. Today, an ounce of gold buys a fine suit. Today, gold is a good store of value over generations.

If one talks about inflation nowadays, everyone is referring to the Consumer Price Index. However, the CPI only tells half the truth because it is just the result of inflation. Classical economists define inflation as a rise in the quantity of money. Price inflation is just the result of monetary expansion if an equivalent increase in output does not accompany the rise in the amount of money.

The substantial increase in asset prices (stocks, bonds, real estate) could indicate that the dollar, the euro, or other fiat currencies have lost their function as a store of value. Instead, the expansionary monetary policy caused assets to become money substitutes and took over as the dominating store of value.

Gold does not pay interest was a widely used saying if one had talked about asset allocation during the 2010s. Stocks are too risky. One can lose money. If you spoke to middle-class members about where to put their savings, the most common answer you got was: Real estate is the best. It preserves value or becomes more valuable. Real estate is also called Betongold (=concrete gold) in the German-speaking area.

This notion, which was heavily supported by the media, changed the use of a good at the bottom of Maslow’s pyramid of needs. The primary use of houses and apartments was to meet the need for shelter. If one was rich, one might have possessed three homes to use for the year, but even the wealthy primarily bought real estate to use it.

Since Carl Menger, we know that the value of a good depends on how people value an additional unit of the good. Formerly, money was also used as a store of value. In times of negative real rates, however, one keeps losing money constantly if one keeps it in a checking account or at home. Therefore, the marginal utility of an additional money unit is higher in systems where money always inflates than in a system where the quantity is kept constant.

But continuous inflation has consequences for risk-taking. The people who used to save money in checking or savings accounts started to buy equities, bonds, and real estate. This leads to an increase in demand and, thus, higher prices. People who already own assets can use them as collateral to borrow and buy even more, pushing demand and prices further. Modern self-made men, like the Austrian Rene Benko, probably would not have been possible in high-interest rates environments.

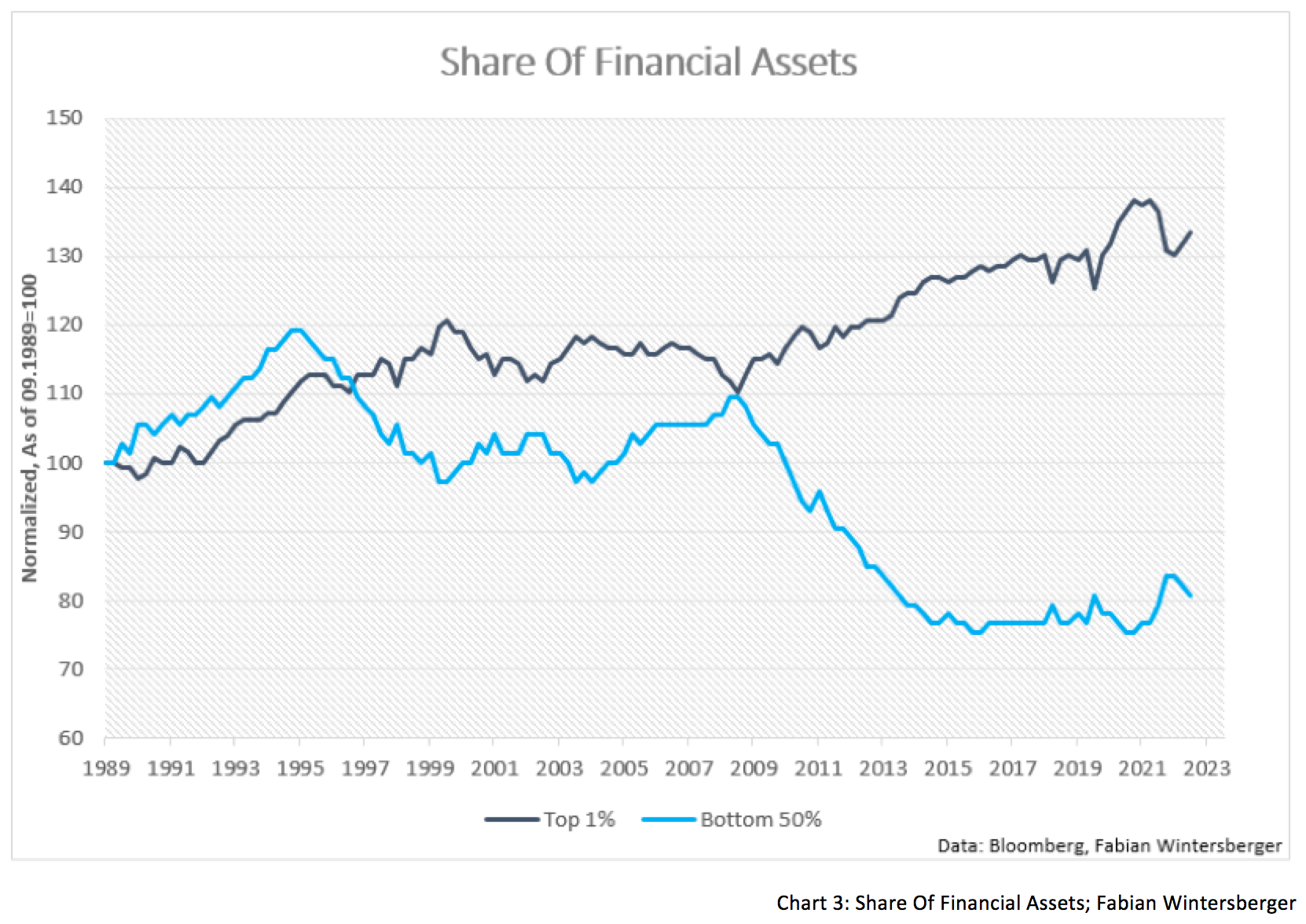

This development accelerated again after the Great Financial Crisis 2008, after central banks opened all monetary floodgates wide. Nowadays, the bottom 50 % own 20 % less of all financial assets than in 1989, while the top 1 % possesses about a third more.

While monetary expansion leads to a creeping expropriation of low- and middle-income groups, where many do not even have significant savings, people with high savings can navigate the storm. Many members of the baby boomer generation have built up some personal wealth, and the house/apartment they own (if they do not own more) has constantly risen in value because of the artificially elevated demand.

That poses the question of why those without significant savings did not protest against central banks’ monetary policy, which brings me to another effect of zero percent interest rates.

Firstly, low-interest rates led to enormous growth in consumer credit and benefited people with a high time preference, if it not even shaped many people’s time preference (see ‘The Zero Interest Rate Trap,’ by Ronnie Stoeferle, Rahim Taghizadegan & Gregor Hochreiter). I know the CEO of an event firm that organizes party trips to Croatia, who told me that the demand for vacation villas from people who live in cities (rent) increased substantially after they implemented some buy now, pay later scheme.

Secondly, people without savings but higher income could easily buy a home, given their income was high enough. During ZIRP and NIRP, it was not uncommon to buy with zero percent private equity; thus, they could still build/buy a home. Those who thought a fixed rate was too high could choose a variable rate, and the deal became even better.

While people with savings or higher incomes could navigate the storm to a certain degree, low-income earners were struck. They started to borrow money for consumption, which roughly said is nothing but lending the good for some time until the debt is repaid.

Simultaneously, ZIRP made it harder to accumulate savings. The fact that entry barriers in the stock market have diminished increasingly, and hence these people can now make micro-investments in the stock market at meager fees is positive. However, it is also a sign that the bull market that lasted for decades is slowly approaching its end. The plan of the German government to save people’s rent by investing it in stocks is another warning signal.

Those who do now own property depend on others to make it accessible to them. As it has become harder and harder to build up wealth, not even to mention to keep your current standard of living because of inflation, the affected people turn to parties who tell them that more distribution of wealth is the solution. The number of those people will increase further if interest rates stay higher for longer, and some people may be unable to pay off their debt for various reasons.

Today, the times of low inflation rates are over. Central banks have increased interest rates sharply to fight inflation. This is another punch in the face for people experiencing poverty, while those who can buy bonds can now earn interest rate payments above the inflation rate (for specific durations). If they lent for a fixed rate, they profit even more.

That is enough to conclude that many people might be on the brink of losing their middle-class life. If (as it is heavily discussed in Austria and Germany) wealth taxes are implemented on top of debt, the pace will just increase. The interweaving between big business and big government, corporatism, means that the middle class will have to pay this tax and hence be hit the hardest.

Finally, one can say that money has lost its function as a store of value over the years, making it harder to buy property. While those with high incomes and savings could increase their wealth, the lower people became dependent on easy money.

Such developments made it possible for something like Bitcoin to emerge. The exceptional thing about Bitcoin is that it combines the characteristics of fiat and commodity money. Holding it is as cheap as it is for fiat, while the quantity is capped at 21 million. If the acceptance of Bitcoin increases, the chance that more people will develop to have a lower time preference again and cut back on consumption. It supports building up savings and wealth.

This is a thorn in the eyes of central banks, who gained power and influence over the years. Although not elected, they sit at the table next to politicians and plan the future. But that will only continue if they are still needed. As a result, one should not wonder that the BIS is calling for creating a global ledger for Central Bank Digital Currencies. They call this improving the old, enabling the new.

Yet, the chapter reads as if the BIS accepted that Bitcoin is the future of money. However, Bitcoin is something that the central bankers do not control. Therefore, one should not be surprised that they demonize it and lump it in with the latest turbulence on exchanges for security tokens like FTX, while on the other hand, they praise the technology.

Somehow, the reports remind one of the centrally planned economic systems. The BIS argues that trust in money is higher when created from a public institution instead of a private one. Therefore one can only have perfect digital currency if it is issued and controlled by central banks. Like if one declares that tables and chairs from carpenters are not bad, and how they build them is excellent, but it would be much better if made in state factories.

Interestingly, privacy for the users is mentioned in the article, but only about third parties who currently offer payment and data systems. That CBDC would mean total control, as Agustin Carstens once said, is kept a secret.

The commercial banks, however, have still not grasped that CBDC will make them obsolete at some point, or put differently, they will not be too big to fail for longer. With CBDC, it is easy to transfer the deposits from the bank to the central bank while letting the bank itself go bust. And we do not even talk about the implications of active macroeconomic policy that CDBC makes possible for central banks after banks were regulated and nudged into a direction where some might blow up if interest rates rose again.

Somehow it seems that the implementation of CBDC is just another stage of the foray of corporatism, which ends in total control and the end of liberalism. While big businesses and governments own everything, the rest is doomed to rent and kept in dependency. You will own nothing, and you will be pretend that you are happy.

Tearing at the scar, she’s open wide

Screaming ´til her lungs collapse (Inside)

Behind her cold and vacant eyes,

Her innocence that dies inside... (Dies Inside!)The Agony Scene - Prey

Now, it is time for a short summer break. The next Weekly Wintersberger will be published on September 7. Have a fabulous weekend & a glorious summer!

Fabian Wintersberger

Thank you for reading! If you like my writing, you can subscribe and get every post directly into your inbox. Also, sharing it on social media or liking the position would be fantastic!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice. I may change my view the next day if the facts change)

Fabian, first have a wonderful vacation. Second, the thing with which I disagree is that CBDCs will run directly from central banks to individuals. They are not configured for the retail banking mess that would create. Rather, I believe commercial banks will be the conduit as they already have the relationships and have done the KYC for their clients. This means that the commercial banks will wind up in a very different role, no longer creating money by lending directly, rather merely being account servicers and collecting a fee for doing so.

But I agree, and fear, that CBDCs are on their way and that people will need to find an alternative means of exchange in order to maintain their privacy. Perhaps gold coins will make a comeback! Or tally sticks