Descent

The consensus now seems to be that there is a 50-50 chance that the economy late this year or in 1974 will slide into a moderate landing– Morgan Guaranty Trust Survey, September 1973 – quoted from the NYT

The first issuance of state debt in the United States marked a significant milestone in its financial history, playing a crucial role in shaping its economic foundation. On December 5, 1791, the fledgling US government, under the leadership of Secretary of the Treasury Alexander Hamilton, initiated the issuance of federal bonds. This historic event unfolded in response to the pressing need to establish the financial stability of the newly formed nation.

One of the primary motivations behind the issuance of state debt was to address the Revolutionary War's lingering financial burdens. The United States, having recently gained independence, faced the challenge of funding its operations, compensating war veterans, and repaying loans received from foreign governments, particularly France. Hamilton envisioned consolidating and managing these obligations through a centralized financial system.

The creation of a national debt was not without controversy. Many were skeptical about accumulating debt, fearing its potential negative impact on the nation's fiscal health. However, in his famous Report on Public Credit, Hamilton argued that a well-managed national debt could be a blessing rather than a curse. He believed it would enhance the nation's creditworthiness, attract investment, and provide a stable foundation for economic growth.

The bonds issued as part of the inaugural debt offering carried an innovative feature – the promise of interest payments. This financial instrument served not only as a means to raise capital but also as a tool to establish trust among creditors. The federal government committed to promptly honoring its debt obligations, laying the groundwork for developing a reliable and credible financial system.

The success of the first state debt issue demonstrated the effectiveness of Hamilton's financial policies. Investors responded positively, and the bonds were oversubscribed, signaling confidence in the young nation's economic prospects. This event set a precedent for subsequent debt issuances and laid the groundwork for developing capital markets in the United States.

The revenue generated from the state debt issue played a pivotal role in funding critical government initiatives, including infrastructure development, establishing a national bank, and the assumption of state debts. It contributed significantly to the economic growth and stability of the United States during its formative years.

The issuance of state debt also had geopolitical implications. By responsibly managing its financial obligations, the United States demonstrated its commitment to fiscal responsibility to the international community. This, in turn, helped build diplomatic credibility and fostered positive relations with foreign creditors.

The success of the first state debt issue and subsequent financial innovations laid the groundwork for the development of modern financial markets in the United States. It set a precedent for responsible fiscal management, shaping the nation's economic policies for years to come. Hamilton's strategic vision and the subsequent establishment of a robust financial system played a crucial role in shaping the economic trajectory of the United States and establishing it as a financial powerhouse.

Quite a lot has changed since the United States' initial debt issuance. Following two world wars in the 20th century, the US dollar emerged as the world's primary reserve currency and the most widely used currency for international trade. The US dollar became the anchor in our globalized economy, solidifying the US as the preeminent global financial market.

Consequently, despite the heightened debt levels, there remains robust demand for US government-issued debt. Both domestic and international investors perceive US Treasury securities as a safe-haven asset, underscoring the US government's distinctive position in the global financial system.

As we approach the year's conclusion, the global economic landscape continues to present challenges. Nevertheless, equity markets in both the US and Europe showcase remarkable resilience, dismissing recent lackluster economic data. Indices in these regions have not only rebounded from their October lows but have also witnessed the German DAX achieving a new all-time high this week.

To be candid, I didn't anticipate such a robust performance from the German stock market. It seems that market participants embraced the recent, more dovish statements from ECB officials. With consumer price inflation declining faster than projected by the ECB staff, the likelihood of the interest rate hike cycle concluding has become highly probable.

Isabel Schnabel, once among the more hawkish members of the Governing Council, shared her perspective with Reuters:

The November flash release was a very pleasant surprise. Most importantly, underlying inflation, which has proven more stubborn, is now also falling more quickly than we had expected. This is quite remarkable. All in all, inflation developments have been encouraging.

Despite Schnabel's emphasis on future decisions by the Governing Council being data-dependent, there is growing confidence among market participants that the ECB will initiate interest rate cuts in 2024. The latest PMI data supports this assumption, and I contend that the rate cuts will likely be more substantial than the market currently anticipates.

Although the Eurozone Composite PMI showed a marginal improvement from 43.8 to 44.2 in November, it still resides in a deep contraction territory. This reinforces my belief that the Eurozone economy is already in a state of recession:

The service sector maintained its downward slide in November. The modest improvement of the activity index does not leave much room for optimism regarding a swift recovery in the immediate future. The sombre outlook is reinforced by the fifth consecutive monthly shrinkage in new business, albeit at a slightly tempered rate in November. Business expectations were subsequently subdued, remaining well below the long-term average and showing a slight dip. As per our GDP nowcast, factoring in the latest PMI indicators, a fall in GDP is on the cards for the fourth quarter. If two consecutive quarters of negative growth define a recession, we find ourselves currently on the brink.

This viewpoint gains additional support from the latest German factory order data released this Wednesday. In October, there was a notable decline of -3.7% in month-over-month figures and a substantial -7.3% drop year-over-year. This marks the 20th consecutive month of annual contraction in German factory orders.

The struggle the German construction sector faces, grappling with the repercussions of elevated interest rates, is of particular significance. The S&P Global Construction PMI for Germany plummeted to 36.2 in November, reaching levels not seen since the pandemic's low in 2020.

While the current data aligns with a bearish outlook for the German economy, the DAX might extend its rally for a brief period, especially if there's a slight improvement in the upcoming weeks. However, caution is advised, given the prevailing uncertainty and the recent uptick was fueled by declining interest rates.

Beyond economic challenges, there's the recent verdict from the German Supreme Court regarding the government budget. Following the court ruling, the German coalition swiftly endorsed another supplementary budget to address the issue. Nonetheless, indications suggest that the new budget may once again breach the constitution, as reported by BILD:

Although the supplementary budget was officially approved last week, concerns arise that it might, once again, violate the constitution. This inference is drawn from the comprehensive eight-page statement provided by the auditors.

On a broader scale, it appears that the recent decline in consumer price inflation signals more than just a temporary fluctuation—it reflects an underlying economic weakness that will likely become more evident in the coming months. A key factor contributing to this is the impact of high interest rates, which have stifled private investment. Considering the Eurozone's existing recession and the substantial debt levels in some Eurozone countries, I anticipate that the ECB will implement more significant interest rate cuts than the current market expectations.

The pivotal question here is whether the US will follow suit. Despite the recent strong rally of the Euro against the dollar, this trend reversed this week. Following the latest statements by ECB officials, the prevailing belief that the ECB could outperform the Federal Reserve seems to be dissipating.

While I contend that these factors support the assumption that the ECB will pivot during the first half of 2024, the uncertainty lies in whether the Fed will take a similar stance. Despite the Eurozone's economy already being in a recession, the US economy performed more robustly and is still anticipated to grow in the fourth quarter.

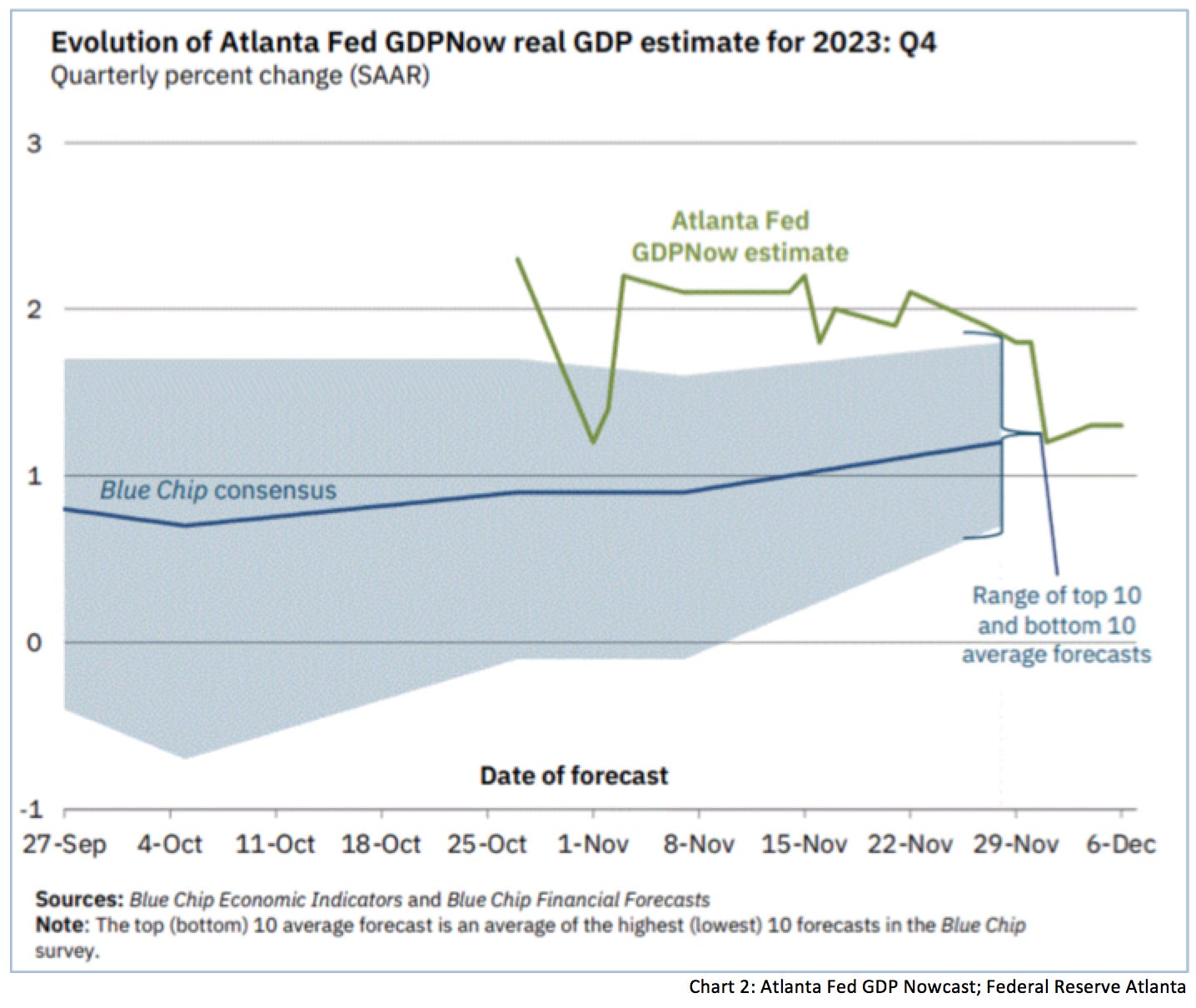

However, the Atlanta Fed's GDP Nowcast implies that the US economy is entering a rapid deceleration. Initially projecting an annualized quarterly GDP growth of 2.10% on November 21, the Nowcast plunged to 1.27%. This suggests that while the US economy might avoid a recession in this quarter, there's a likelihood it could enter one in the first or second quarter next year.

Ultimately, it becomes evident that the US economy is not impervious to the Federal Reserve’s interest rate hikes:

Retailers that cater to the upper middle class — including Apple, Coach and Nordstrom — have seen their biggest sales drop in two years.

The assumption that the US economy is decelerating finds support in the latest ISM survey, where respondents indicated that

[the] economy [is ]absolutely slowing down. Less optimism regarding the first quarter of 2024.

However, the US services sector maintains its expansion, with the S&P Global Services PMI at 50.8 and the ISM Services Index at 52.7. Conversely, ISM Manufacturing and Services Employment numbers hint at a gradual weakening labor market. The confirmation of this trend awaits scrutiny in this Friday’s Nonfarm Payroll Report.

Weaker labor market data has spurred a rally in US Treasuries this week, with a growing conviction among market participants that a slowing economy will prompt interest rate cuts.

Meanwhile, traders got another sign of job market cooling on Wednesday, as ADP data also came in below forecasts. Private payrolls increased by 103,000 in November, under the Dow Jones estimate of 128,000.

Treasury yields fell on Tuesday after JOLTs job openings figures for October came in lower than expected and indicated a cooling of the labor market — 8.73 million openings were recorded, a drop of 617,000 and far below the 9.4 million Dow Jones estimate.

While one can conclude that market participants are indeed expecting a slowdown in US economic activity, there is a broad consensus that it will be just a bump in the road. The Fed will likely cut interest rates by about 100bps, and the economy will return on track. This scenario is currently priced in, making it challenging to profit by betting on this scenario.

While it is reasonable to infer that market participants anticipate a slowdown in US economic activity, the prevailing consensus suggests it will be a temporary setback. The expected response is a 100-basis-point cut in interest rates by the Fed, restoring the economy to its trajectory. This scenario is already factored into the market, making it challenging to profit from such a projection.

The mounting confidence in the realization of this scenario intensifies my skepticism. Glancing back at history, every hard landing was preceded by statements from politicians and central bankers suggesting a soft landing was increasingly likely. This week, Janet Yellen openly ridiculed those forecasting a recession:

In comments on the US economic outlook, Yellen took at swipe at economists who predicted only a recession would tame inflation and criticized her for continually saying she saw a path to a so-called soft landing.

“Economists who’ve said it’s going to require very high unemployment to get this done are eating their words,” she said. “It doesn’t seem at all like it’s requiring higher unemployment.”

I believe this statement will backfire, similar to her prediction in 2017 when she said that she didn’t think there would be another financial crisis in our lifetime. After all, her role as treasury secretary significantly contributed to this, running a 7% budget deficit during the latest economic expansion to sustain the momentum.

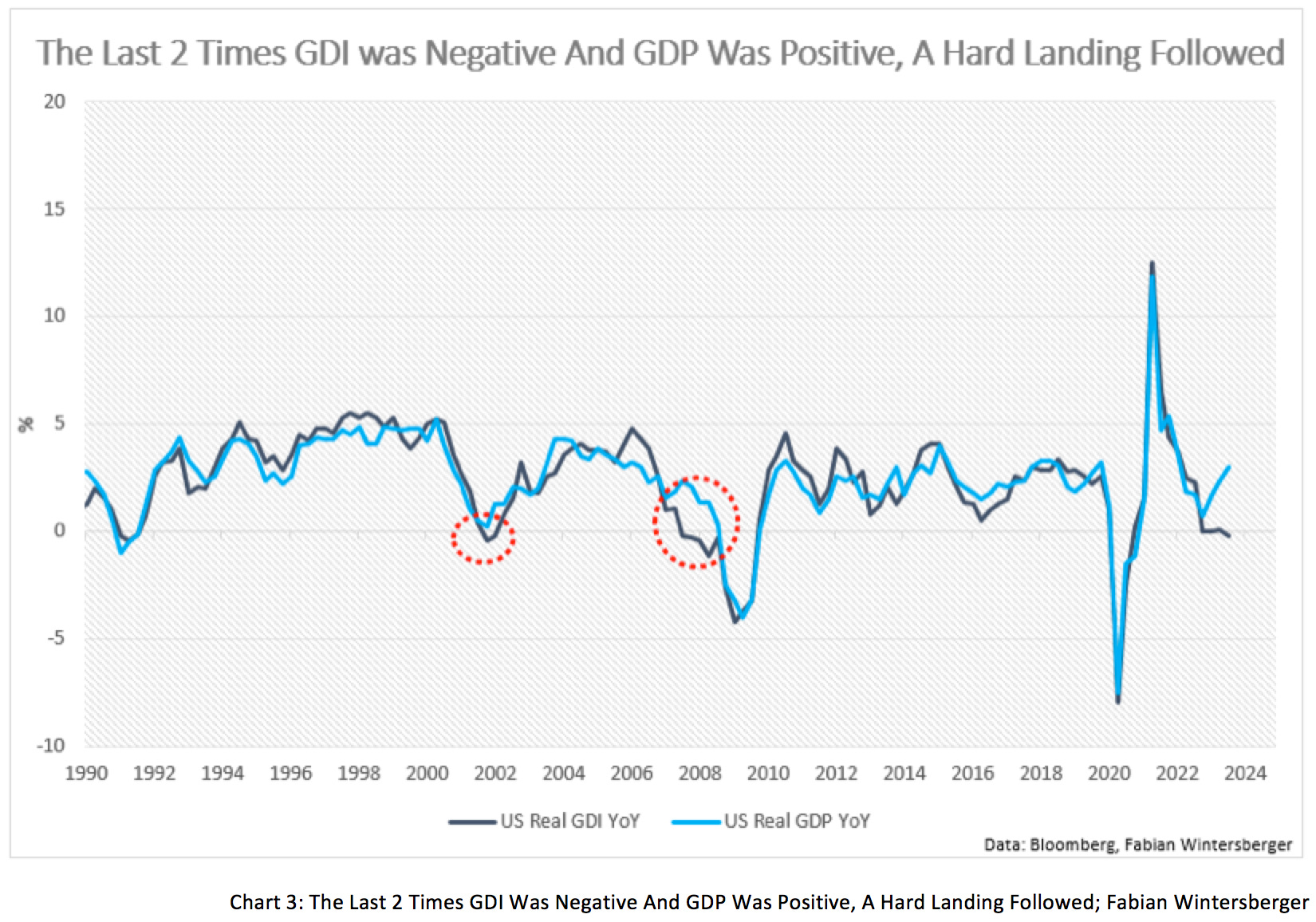

Beyond evaluating the current economic state through output numbers, one could scrutinize income. While Gross Domestic Product gauges the total value of goods and services produced, Gross Domestic Income measures aggregate income received across all economic sectors.

In theory, GDI and GDP should closely correlate, but the present divergence suggests a slowdown in corporate profits and wages while consumers persist in spending, displaying a degree of resilience. This aligns with my assumption last week that consumers strive to sustain consumption by depleting savings or resorting to increased borrowing. Similar divergences in the past have heralded a hard landing.

If my assumptions are correct and the US economy has a hard landing in the coming quarters (I consider my recession forecast for Q4 slightly off), the question is how the Fed will react. Most market participants and observers would argue that the Fed will do what it has always done in recent years: slash interest rates and implement massive Q.E.

However, after being wrong about Powell for the first half of 2021, I am not sure whether Powell will really do what market participants believe, at least not until there’s some sort of systemic risk that cannot be solved differently.

It's a widely held belief that the US government wouldn't cut back on spending in the event of a hard landing. However, the US government is already running a 7% rolling budget deficit during a growing economy and rising interest rates. If the Fed cuts rates and the government deficit surges, it could potentially trigger another significant inflation wave.

I'd reckon Jerome Powell is aware of this, too. What if he maintains high interest rates to compel the government to adopt a more fiscally prudent approach? The recent drop in long-term interest rates could unwind sharply in such a scenario, propelling long-term yields to new highs. Additionally, if the Fed resorts to Q.E. and ZIRP, as some suggest, it might initially push down long-term rates, but subsequently, they could rise again due to increasing inflation expectations.

While Powell might eventually find himself with no other option than to concede, my gut feeling is that he will attempt something Alan Greenspan was never successful at—pressuring the government into a more responsible fiscal policy.

Meanwhile, gold reached a new all-time high this week before experiencing a sharp sell-off. It has rebounded and is trading at $2,235, but given the outlined scenario, I believe it could dip lower before recovering.

In the currency markets, this would imply a resurgence in the dollar. The recent rally in EUR/USD has already started to falter, and if there's a slight rebound, it might present a good entry point for a short position, which could be expanded if it rises above 1.10. Nonetheless, the Euro's rally might be approaching its end.

Considering everyone expects a soft landing and few anticipate economic improvement next year, people might be in for another surprise.

They said it's coming for all of us

But we fell on our swords and we never got up

When it feels like the walls are closing in, maybe they are

And we're afraid to see it, we'll deny our descentSylosis – Descent

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

(Please note that all posts reflect my personal opinions and do not represent the views of any individuals, institutions, or organizations I may or may not be professionally or personally affiliated with. They do not constitute investment advice, and my perspective may change in response to evolving facts.)

It is remarkable how mainstream the soft-landing story has become, especially given the history that shows it is a highly infrequent event. certainly, Friday's NFP data was a positive for the soft-landing thesis, but it would seem not so positive for the 125bps of rate cuts.

to my mind, 125bps is the least likely outcome where we either get a token 25 or 50 throughout 2024 or we get 350-400 as a full-blown recession shows up.