Bow Down

Once you get into debt, it’s hell to get out. Don’t let credit card debt carry over. You can’t get ahead paying eighteen percent– Charlie Munger (1924-2023)

December 1, 1913, Michigan. The air buzzed with anticipation at Henry Ford's Ford Motor Company's production facility. It was a day that would alter the course of industrial history. Henry Ford, a visionary and pioneer in the automotive world, had gathered his team to unveil a radical idea that had the potential to transform the manufacturing landscape. Little did they know that the innovation about to be introduced would revolutionize their industry and impact the way goods were produced across various sectors.

As the morning unfolded, the workers at the Highland Park Plant witnessed the birth of the first modern assembly line. The concept was both simple and ingenious: rather than craftsmen laboriously handcrafting each component of an automobile, the chassis would now traverse a conveyor belt. Positioned along the line, workers would add specific components as the vehicle moved past them. It was a departure from the traditional approach, where workers moved to the car; now, the car moved to the workers. The rhythmic hum of the machinery set the stage for a transformative moment in manufacturing.

The impact was swift. The once arduous task of crafting a single Model T, which took over 12 hours, now took a mere 93 minutes. The efficiency gained from the assembly line translated into drastically reducing production costs. The affordability of the iconic Model T soared, making it accessible to a broader consumer base. By 1916, half of all cars in America were Model Ts, a testament to the far-reaching implications of this groundbreaking innovation.

The assembly line not only revolutionized the production process but also transformed the nature of work. Jobs became more specialized and repetitive, requiring less skill and training. While the assembly line increased efficiency, it also sparked debates about the dehumanization of work and the toll it took on workers' physical and mental well-being.

Henry Ford's innovation extended beyond the confines of his factories. Mass production and assembly line manufacturing principles became a model for industries worldwide. The assembly line method was adopted in automotive manufacturing and sectors such as electronics, appliances, and even food production.

The success of the assembly line reflected a broader shift toward industrialization and mass consumption in the early 20th century. It played a crucial role in shaping the consumer culture that would define the following decades. The assembly line made products more affordable and contributed to the rise of the middle class with the means to purchase these goods.

While the assembly line had immense economic benefits, it also brought challenges. Labor relations became a significant issue as workers sought better working conditions and fair wages. This led to the rise of labor unions and the establishment of workers' rights, shaping the future trajectory of industrial relations.

The Ford assembly line is often credited with ushering in the era of mass production, fundamentally changing how goods were manufactured and consumed. The principles of efficiency and standardization introduced by Ford continue to influence manufacturing practices today. It remains a landmark moment in industrial history, shaping the course of the 20th century and beyond.

It is an established historical fact that Ford's revolutionary shift in the production process yielded significant benefits for workers, shareholders, and consumers. In a pivotal move in 1926, Ford introduced the 40-hour workweek for his employees, a groundbreaking decision during that era. Shareholders reaped the rewards through increased profits, reduced production costs, and elevated market dominance. Simultaneously, consumers enjoyed the advantages of lower prices.

This transformative innovation also had a ripple effect on other businesses, empowering more individuals to travel independently and allocate additional funds to various goods and services. In essence, this innovation translated into economic success, not only in the United States but also reverberating elsewhere.

Today, there has been a notable shift in expectations. While there should be little debate that entrepreneurs and businesses are the primary drivers of higher economic well-being, a prevailing notion persists that government intervention is crucial for achieving better economic conditions. Paradoxically, in many cases, policymakers achieve outcomes contrary to their intended goals.

Currently, extensive discussions surround the state of the US economy, specifically focusing on the consumers’ conditions. It is widely acknowledged that consumers are the driving force behind the economy; when consumers spend, the economy thrives, and vice versa. The recent 'Black Friday' shopping event, typically a robust weekend for retail, presented a somewhat mixed picture, at least:

On Black Friday, retail spending increased by just 2.5% from last year, according to Mastercard SpendingPulse. Online sales increased 7.5% to $9.8 billion, and the overall weekend is expected to reach at least $37.2 billion in spending, an increase of 5% from last year, according to Adobe Analytics. TD Cowen went as far as lowering its holiday forecast in a note on Friday to 2%-3% year-over-year growth versus a previously estimated 4%-5% because of the slow start to the season.

Since the start of 2021, there has been a 32% increase in outstanding revolving consumer credit. While this is occasionally viewed as an indicator of growing consumer confidence, it has drawbacks, potentially posing a challenge to financial health. Recent signals suggest a notable uptick in the latter aspect:

Rising delinquencies come as outstanding credit-card debt has reached a record of about $1.2 trillion this year, and the rate of interest being charged also has touched a record of about 23%, according to Deutsche Bank Research.

This sentiment is further echoed in a recent survey, where the overwhelming majority expressed a perception of worsening financial conditions since Joe Biden assumed office. Only 14% of voters believe they are better off financially since Biden's inauguration. However, is this perception accurate? According to Claudia Sahm, a former Federal Reserve economist, reality diverges significantly from the sentiments reflected in the survey numbers. In a recent blog post, Sahm presented data comparing the current scenario with pre-pandemic data.

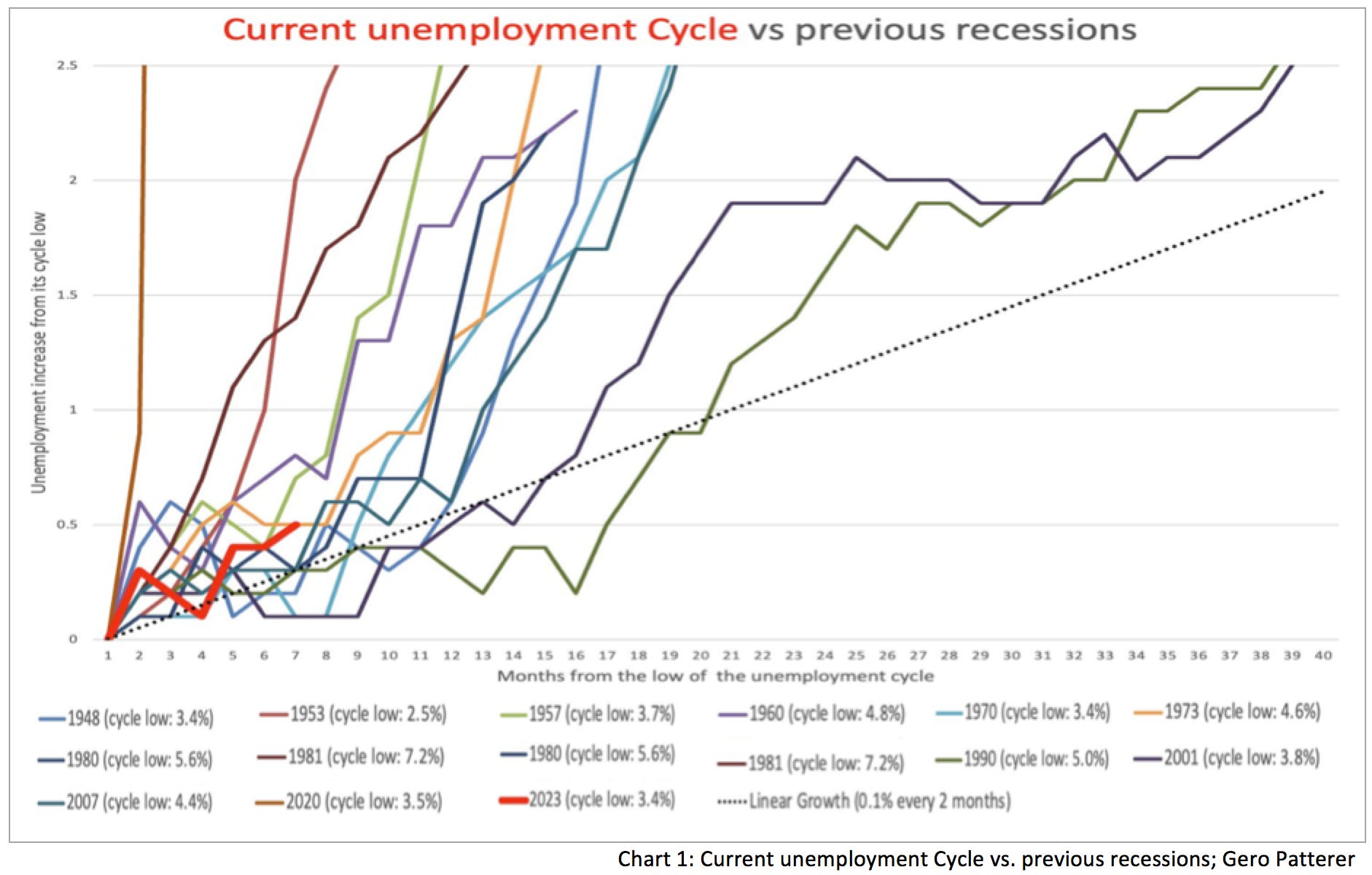

Initially, Sahm points to the latest unemployment data, which surprisingly remains below 4% despite increasing reports of economic frailty. In her analysis, she underscores that...

…[as] of October 2023, it has been there for 21 months. That is the longest stretch since the late-1960s. That is very good.

The tightness in the labor market has undeniably bolstered the bargaining power of workers, particularly given the numerous unfilled job offerings as companies grapple with workforce shortages. The pandemic appears to have caused or exposed significant misallocations of workers across economies, and the economy is grappling to realign and address these challenges.

Without a doubt, the combination of a low unemployment rate and the challenge of finding available workers has significantly enhanced the bargaining power of employees. However, on the flip side, the increasing unemployment rate and the surge in continuing and initial jobless claims may signal an emerging weakness. As the uptick in unemployment tends to follow a nonlinear pattern during economic turmoil, it is noteworthy that the recent gradual increase does not deviate significantly from patterns observed in previous recessions.

Sahm contends that the new jobs created are 'more good jobs.' While assessing whether a job is 'good' is subjective, encompassing factors such as higher pay and well-being, a Gallup workplace report indicates a growing dissatisfaction with current jobs and workplaces. Well-being in the workplace significantly influences long-term productivity.

While Sahm's assertion that increased pay has been beneficial holds, the claim that these are categorically 'better jobs' is debatable. The belief that everyone can find happiness in their job is a widespread myth, as individuals pursue means to reach their goals. Some may prioritize a higher-paying job to afford preferred activities, making a larger paycheck beneficial for them.

A critical question arises: has the higher pay genuinely improved people's well-being in real terms? Sahm argues this is the case, particularly for the low-income group. Her analysis suggests that, compared to October 2019, only the upper-income quartiles have not experienced an improvement. According to her, low-wage workers enjoy a 4.5% higher real wage today.

Despite this positive outlook, there remains a disconnect between this reality and public perception. Sahm suggests that continuous negative news in the media distorts people's perception of reality. However, if most workers genuinely benefit, why doesn't it manifest in survey data?

Several factors contribute to this discrepancy. Firstly, there's an ongoing debate about whether the Consumer Price Index (CPI) accurately reflects the price increases consumers face. The Bureau of Labor Statistics (BLS) makes various adjustments in calculating price increases for different items, leading to disparities. For instance, the BLS reports health insurance down about 38% year-over-year, which seems improbable in reality.

In essence, consumer price indices, whether the European HICP or the US CPI, might not accurately capture the price changes faced by everyone due to the diverse consumption habits of individuals, each affected differently by price inflation.

That said, even when utilizing CPI data, one might draw different conclusions than Claudia Sahm. Her analysis starts from October 2019, presumably because the most recent CPI data available is from October 2023. Moreover, Sahm relies on the wage growth tracker from the Federal Reserve Atlanta, indicating a significantly higher real wage increase than the BLS's Average Hourly Earnings, currently standing at 0% YoY.

In addition, I contend that using October 2019 as a starting point may not accurately capture the consequences of inflation. In October 2019, US CPI YoY was close to 2%, slightly below the Atlanta Fed wage tracker and the BLS's Average Weekly Earnings. In the first half of 2020, CPI dropped to nearly zero year-over-year, positively influencing calculations when using October 2019 as a baseline.

When comparing the impacts of the latest consumer price inflation wave, I find it more accurate to use average weekly earnings, as they are also influenced by total hours worked. Workers may have opted to reduce working hours, a trend supported by the data.

Starting from May 2020 data, when consumer price inflation hit its lowest point, the result indicates that real weekly earnings have failed to keep pace with inflation since then. In May 2020, $100 in earnings could purchase goods valued at $100; in October 2023, the same $100 in earnings could buy goods worth $95. Moreover, the loss in real purchasing power has remained relatively constant since May 2022.

As a result, I find it debatable whether Claudia Sahm is accurate in asserting that wage earners are now better off than before the recent surge in inflation. Wages typically do not rise concurrently with consumer price inflation; there's often a lag. It's important to note that wage earners may face a deterioration in their financial well-being over time. This trend would persist even in a scenario the Fed terms' stable prices,' a condition where consumer prices steadily decrease close to 2% annually.

However, Sahm's perspective gains validity when considering the impact on consumers. The pandemic stimulus checks notably aided low-income workers, contributing to additional consumption compared to a scenario without the stimulus or debt reduction. Notably, household debt decreased during the pandemic, indicating that families used stimulus payments to reduce debt.

In essence, consumer spending experienced an upward push due to stimulus payments. What set these stimulus packages apart from previous ones was their nature as a form of 'helicopter money,' turning the conventional 'trickle-down' effect on its head and transforming it into a 'trickle-up' effect. Initially, spending increased, and prices followed suit. Consequently, when the stimulus packages concluded, and individuals spent the funds, consumers turned to consumer credit to finance purchases. The record-breaking consumer spending during Black Friday and Cyber Monday is a prime example. While consumers spent a remarkable amount, Adobe observed:

On Cyber Monday, 'Buy Now Pay Later' (BNPL) usage hit an all-time high, contributing $940 million in online spend, up a staggering 42.5% YoY. The number of items per order rose 11% YoY, as shoppers used BNPL for increasingly larger carts. Season to date (Nov. 1 to Nov. 27), BNPL has driven a total of $8.3 billion, up 17% YoY; November 2023 is expected to be the biggest month on record for the payment method.

The last set of stimulus checks, totaling $401 billion, was distributed in March 2021. Initially, personal consumption expenditures surpassed outstanding revolving consumer credit. However, approximately six months later, revolving consumer credit began to catch up and eventually exceeded personal consumption expenditures. This trend could signal that the current economic growth rate may not be sustainable and might reverse in the coming months.

Thus, one can conclude that, despite the impressive recovery in consumer spending, the data suggests that government handouts primarily propelled it. Once these subsidies ceased, consumers resumed increasing their debt spending, signaling a shift from the strength of the consumer to potential weakness.

Various reports from the latest Fed Beige Book already note that consumer spending is either stagnating or weakening. Although overall spending remains robust, the downward revision of personal consumption expenditures in Q3 from 4% to 3.6% supports that. While still a strong figure, it is a noteworthy trend to monitor.

In her analysis, Sahm also addresses the increase in financial wealth and the subsequent decrease in the debt burden. However, the declining debt burden can be attributed simply to inflation. With nominal wages on the rise, the real debt burden for debtors diminishes, allowing individuals to allocate a higher proportion of their income for other expenses.

In the United States, median homeowners earn approximately $7,200 per month, while the median payment is $2,800 monthly. Consequently, they can now spend about $784 more than in March 2020, adjusted for CPI. This effect is anticipated as inflation redistributes wealth from savers to debtors, supporting Claudia Sahm's perspective.

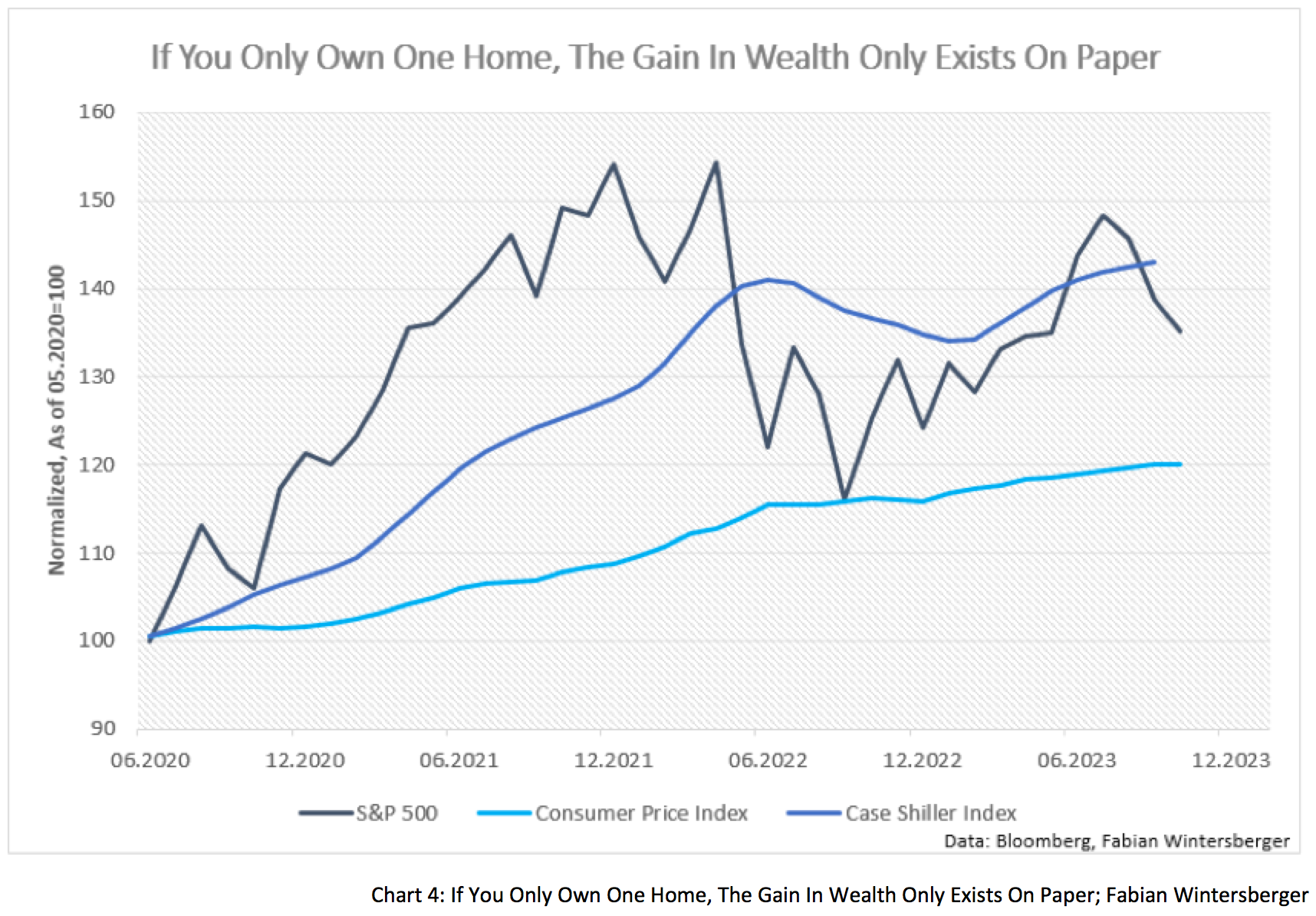

The surge in financial wealth stems from the straightforward increase in asset prices. While the increase in wealth is apparent when considering the appreciation of home values, this doesn't necessarily translate to overall betterment for most families, as many only own one home. Home prices in the US have risen by about 22% in real terms since May 2020.

Therefore, although median family wealth has increased, this gain is primarily due to rising home prices driven by inflation. This increase in wealth might only benefit families considering downsizing, as those seeking a similar or larger home may find their gain disappearing, especially when factoring in higher interest rates for new mortgages.

While the situation for most families in the United States may not be as dire as current fear-mongering suggests, it likely isn't significantly better than before the pandemic, as indicated by Claudia Sahm. In fact, one can anticipate a mixed scenario at present, with the potential for a worsening situation in the future—especially if the Federal Reserve maintains higher interest rates for an extended period. If consumers continue to finance their consumption through debt, and if interest rates remain unchanged, consumers will inevitably need to bow down and grapple with reality.

You will never know, it’s the price I pay

Look into my eyes, we’re not the same

Yeah, this is where you fall apart,

Yeah, this is where you breakI Prevail – Bow Down

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

(Please note that all posts reflect my personal opinions and do not represent the views of any individuals, institutions, or organizations I may or may not be professionally or personally affiliated with. They do not constitute investment advice, and my perspective may change in response to evolving facts.)

I believe it is important to remember that Claudia Sahm is also arguing a political point. She is a notable left leaning economist and trying to make the case to offset the current negative perceptions with data. It does not surprise me that she chose a starting point to flatter the analysis at all.

That said, I would argue the widespread negativity is more likely a function, not of the fact that CPI last month was 3.0%, but that the price level is 20% higher than prior to President Biden's election. A rise in prices of that magnitude in such a short period of time means that everybody can remember when things were cheaper, not that long ago. going to the supermarket and seeing the Charmin that used to be $5.99 for the 8 pack now costing $9.99 is very obvious to one and all, and contributes to the negative overall sentiment. Even if CPI continues to decline, until price levels start to fall, I do not expect to see positivity return, no matter how many numbers Claudia Sahm publishes!