What Comes Around

Do you remember what happened in financial markets on January 7th, 2019? No? I have many deja-vus of those days when I look at stock indices nowadays.

Let us see what Business Insider wrote on January 7th, 2019:

China stock markets rally on Trump optimism before trade talks: ‘Good Things are going to happen’

‘I think good things are going to happen’ on a trade deal, US President Donald Trump told reporters on Sunday, according to the New York Times’

Stock markets are forward-looking. Ok, but I am still puzzled (I probably should not be) about the price action after some news headlines made markets rally again.

On Tuesday, the Ukrainian negotiators stated that it is talking with the Russian delegation about a potential ceasefire, conceivable neutrality of Ukraine, and possible security guarantees from other countries.

Markets celebrated, European indices rallied nearly 3 %, the S&P closed near +2 %. Oil prices collapsed, WTI traded below 100 dollars for a brief period (- 7.72 %).

Interest rates rose because a potential peace would diminish a lot of uncertainty, and thus central banks may be able to normalize interest rates faster.

The market is driven by news, and peace talks seem to be the new trade talks. Although I was puzzled about the price action, I was not surprised. The question is if the rally has any substance, and I doubt that.

Of course, it is a possibility that the West would end sanctions when Ukraine and Russia would agree on some peace treaty, but is there a probability?

The climate between the West and Russia is rough, and I cannot think of a scenario where sanctions would be lifted if there was peace. However, as everyone in Europe believes that Russia is excluded from international trade because of the western sanctions, you probably should look at the map.

The Western sanctions hurt the Russian economy, but western supremacy has decreased since 1990. Hence Russia is not isolated economically. In 1990, Brasil, China, India, Mexico, and Russia produced 18 % of global GDP, the EU and the United States 42 %. Now, those two blocks are responsible for the same portion of global GDP.

If it has not already begun, one should expect an economic war between the West and Russia. However, recent efforts to force Russia to end the invasion of Ukraine because the sanctions are driving up Russia’s economic costs do not seem to work. On the contrary: economic prices are also rising in Europe.

The Russian ruble fell dramatically when the sanctions were imposed and have brought Moscow to the edge of a currency crash. Nevertheless, the Kremlin is now trying to take counter-measures and wants future natural gas deliveries to be paid in rubles. As a result, the ruble is now near pre-war levels, although volatility remains possibly high.

On Monday, the G7 stated that payments in rubles for future delivery of oil and gas are not acceptable. The situation has become a chicken game, where the question remains who blinks first.

Whether a stop of oil and natural gas imports from Russia to Europe is bearable is widely discussed among German economists. According to their models, the majority say that an embargo will hurt the economy, but the situation could be manageable. However, all those New Keynesian models do not have a labor market or a financial sector, and therefore, I think those results are at least questionable.

In my opinion, a stop of oil and gas imports from Russia will not be manageable for Germany in the short run. An embargo will hit the industrial sector hard as it is dependent on Russian gas to run production. To compensate for Russian gas with LNG from the middle east or the US would take two to three years. Further, according to an article from Stefan Ulrich on the Bloomberg Terminal, there is not enough LNG to compensate for Russian gas.

The German Industry is warning that a stop of natural gas imports from Russia would lead to the shut down of production facilities, and thousands of jobs would be in danger, according to Frankfurter Allgemeine Zeitung.

It seems too soon to have the same euphoria about peace talks as the stock market. The following month gives some hints about the future, but I expect energy prices to remain stubbornly high in Europe.

Food price increases also will be around for a little longer. Although Ukraine produces only .9 % of global wheat, fertilizing has become very expensive. While I expect that the west will be able to deal with the situation somehow, the problem might lead to new refugee flows from the Near East and Africa. The fact that a considerable proportion of fertilizer is produced with Russian gas does not help either.

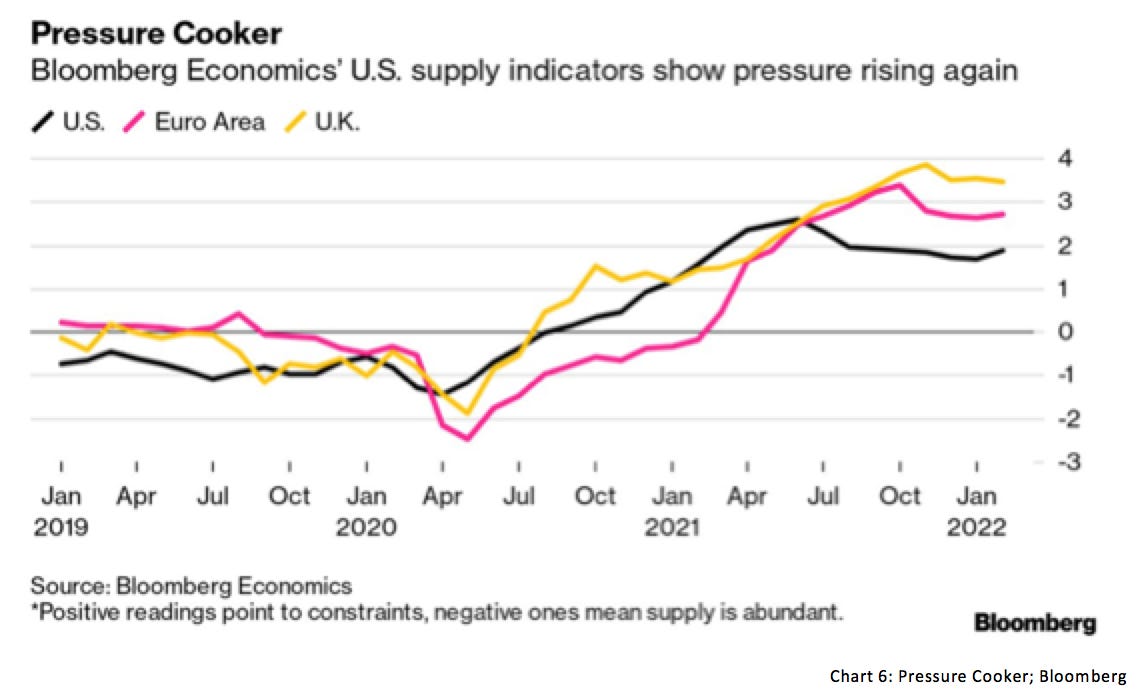

As I argued last week, commodity prices will stay at high levels due to the war, sanctions, and more prolonged uncertainty in the marketplace. Apart from the war, China’s new lockdowns due to the Omicron wave put pressure on supply chains.

Hence, prices will remain elevated for longer while some indicators point to the possibility of an economic slowdown that probably has already begun.

Despite PCE levels being consistently high, Service PCE is still way below the pre-crisis trend. However, compared to a GDP of 2.9 % in real terms in the Euro Area, the US economy grew by 5.9 % in real terms and thus is much stronger than the Euro Area economy because of significant stimulus payments to consumers.

While retailers hope that demand will remain high even despite vast sums of stimulus payments, everyone who has been experiencing supply-chain problems sales inventories is going through the roof, as Jeff Snider explains:

A flood of mostly foreign goods was requested, though many of those got stuck in the myriad entanglements of other COVID-based “frictions”, raising prices but also the itchy nervousness of suppliers in wholesale and retail positions.

Rather than wait out the logistical mess, and risk missing out, wholesalers and retailers seeing their prices rise so quickly for the first time since 2008 went insane. As I’ve been writing since last summer, they quite intentionally over-ordered, doubling, tripling, quadrupling up on goods just to hope some sufficient quantity made it through the gauntlet of port inadequacies, railroad turmoil, and a “shortage” of truckers whose only fault is that they don’t get paid to wait idle for those others.

On the other hand, falling real wages in the US may indicate that the rise in prices may be over soon, and higher supply and lower demand will lead to lower prices.

Additionally, the plans of central banks to hike interest rates aggressively are putting more fuel to the fire. Especially Joe Biden pressures the Fed to bring inflation down until the mid-terms.

The market has already priced the Fed’s aggressive standpoint, and rates at the short end have gone up and flattened the curve. Some parts of the yield curve are already inverse, indicating that economic growth might slow. This Tuesday, the US 2s10s spread turned negative, bid up again, and currently trades around the zero line. 2s10s have always been a good indicator to forecast a recession, and I would assume that the US economy will be in recession in 2023 at the latest.

However, as I feel that things happen much quicker in this cycle than they did in previous ones, I would instead expect that the recession already starts in Q3 or Q4 this year. Nevertheless, yield curve inversion is not a good indicator of stock market direction. Chart 7 from iCapital Investment Strategy shows that, on average, the S&P 500 reaches its cycle top 10 months after the inversion with an average return of 12 %.

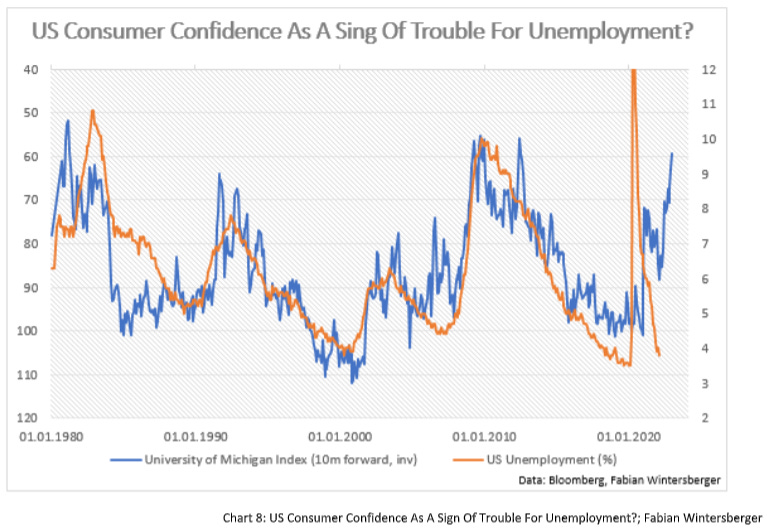

As the Index from the University of Michigan (approximately due to high price inflation) shows, negative consumer sentiment fits into this picture. The housing market, another leading indicator, is also signaling possible stress ahead as financial conditions are tightening.

Further, a decline in consumer confidence may lead to lay-offs due to lower than expected sales and hence a rise in unemployment. I would estimate that if the S&P 500 tops in 10 months due to the inversion in the yield curve, the unemployment rate could also be higher then.

If this is the case (especially in times like these, forecasts are challenging), it is 100 % sure that Joe Biden will blame it on Jay Powell and the Fed because of hiking interest rates too aggressively. However, a higher unemployment rate might be inevitable due to the drop in consumer sentiment.

So, What Comes Around? My tip is that the environment of rising prices, stable/rising equity prices, and rising rates continues for some more time before signs of a slowdown become so apparent that (at first) market participants and (later) central banks cannot ignore them anymore.

Or, as Il Nino sings: Everything that is real, comes around (comes around, comes around)

Have a great weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)