Walk With Me In Hell

It’s been a turbulent week on and off financial markets. Because I write this piece before the ECB announces its rates decision, you will not get any information about that on the Weekly Wintersberger before next week. However (and you, dear reader, will already know), I expect a rate increase of 75 basis points if the ECB wants to be taken seriously in its inflation fight.

If one looks at Japan, one sees what happens to a currency if the central bank keeps monetary policy loose while the Federal Reserve tightens. The Bank of Japan is still buying loads of government bonds to prevent yields from rising. This week, the BoJ announced it would buy 550 billion yen of Japanese 10-year bonds. As a result, the exchange rate to the dollar fell, and the USD/JPY is now around 143.

But even if the ECB becomes very restrictive down the road, it might not be enough to prevent the currency from falling. The British pound is an excellent example because the Bank of England’s monetary policy is as restrictive as the Fed’s. However, that could not prevent the pound from falling. Nevertheless, a tightening ECB could at least fulfill its part in fighting a falling euro.

The problem in the UK comes from the fiscal side because the government is ramping up expenses to dampen the consequences of skyrocketing energy prices for its citizens. After Boris Johnson resigned, former foreign minister Liz Truss took over, and Truss announced another care package to dampen the consequences of inflation. It is expected that the government will spend at least 200 billion pounds. In comparison, the UK’s GDP in 2021 was 2.2 trillion pounds.

However, Truss also spoke about lowering taxes in recent statements. Lowering taxes while simultaneously ramping up government spending means higher government debt. The government can only fund its spending in two ways: via direct taxes or through the hidden inflation tax. The Office of Budget Responsibility calculated a stress test scenario where the UK’s debt/GDP ratio could hit 450% of GDP in 50 years.

And additionally, more government expenditures mean more future inflation. While central bank QE does not reach the real economy, transfer payments get into the real economy, fuelling inflation. If one calculates that energy prices will remain high and domestic production receives a hit, this would mean more inflation because more goods must be imported from abroad.

The same is happening all around Europe, where governments try to dampen the consequences of the sanctions with additional spending. European governments introduced price caps on energy to fight rising prices (translation: creating supply shortages). Polemically speaking, the ECB cannot hike rates faster than governments spend money.

We should remember that, since the pandemic began, governments have had indirect control over the money supply. Russel Napier has talked a lot about it, and the magic word is credit guarantees.

During the pandemic, many companies got loans because the government generously guaranteed them. For a bank, this means secure profits because it does not matter if the debtor is credit-worthy or not. Either the company can pay back the loan, or the government does.

As the crisis continues, the government will use the instrument more frequently (and honestly, they have to) to prevent insolvencies and mass unemployment. The catch is that this will not help the companies sell more goods because many of them will be forced to raise prices, leading to fewer sales. So, governments will also have to support consumers via transfer payments. Debt/GDP will skyrocket, and, as a result, yields will have to go up too.

Ursula von der Leyen held a press conference this week where she presented plans to fight the rise in energy prices. Her proposals mean deep interventions into the - already highly regulated - energy market. So to say, the EU-Commissions fights problems that result from intervention with more intervention. So, what did von der Leyen say?

The EU Commission wants to flatten the curve. It wants to lower energy consumption during peak hours. Peak hours are usually in the morning and the evening when people are at home. Von der Leyen wants to make it mandatory to save energy, although one has to wait for how this should work.

Further, von der Leyen proposed a windfall profit tax for energy producers earning high profits because of the Merit-Order system (where the last quantity of electricity produced determines the price). As far as I remember, the system was introduced to boost renewables because this way, clean energy producers could earn a much higher profit.

However, it is unclear why one should extra-tax energy companies when the energy supply is too low. A windfall profit tax might bring some money at first, but it will lead to a more insufficient energy supply in the future.

Of course, von der Leyen talked about RePowerEU. According to her, additional investment into renewables will lead to cheaper energy and energy autarchy. Although, she does not mention that it was mainly the fixation on renewables that made Germany dependent on Russian energy. Currently, it is simply not possible (that is what I am told) to run an electricity network solely on renewables like solar and wind. Further, Germany was a leader in the use of renewables but, in comparison, had one of the highest electricity prices in Europe.

A price cap on Russian gas might be truly symbolic, as Russia announced that it would send no gas via Nordstream 1 until the sanctions are lifted.

The best case is that the Russian economy is in such bad shape that it forced Putin to play this card. However, I am no expert in geopolitics and thus want to leave speculations to the experts.

Skyrocketing energy prices led to margin calls for a lot of energy producers. According to Bloomberg, European energy producers face margin calls of about 1.5 trillion dollars, which means that many companies have liquidity problems.

It is clear that governments will have to guarantee those, and in my opinion, they should do it. Most of these margin calls result from hedging; thus, if the producers deliver electricity at the expiry date, those margin calls disappear.

A lot of companies should brace for a hard winter. Many of them struggle already because their business got a hit during the pandemic. A German bakery recently reported that it now has to pay 2,588 euros for natural gas per month instead of 721 euros prior. Automotive supplier Dr. Schneider announced insolvency this week, and I fear it will not be the last company.

But it is not only natural gas. This week, Opec announced that it would cut oil production. Throw this in the mix with the US refilling its SPR. One can expect that the oil price will increase again at some point.

I am sure that Europe will have enough energy this winter (or I hope so). The bad news is that government interventionism will make problems more severe. Additionally, governments are on a spending spree again and forget that the times of low inflation are over.

Finally, let us have a look at financial markets again. Although gold has a tough time because of the Fed tightening, measured in GBP or euro, gold is still near all-time highs.

Equity prices are still far away from the bottom, in my opinion. The Fed will continue to hike rates, and the market is currently expecting another 75bps hike for the next meeting. However, historically, stocks bottomed when the Fed started to cut rates.

I have thought a lot about it, and I still cannot find a bullish case for bonds, especially for UK and EUR bonds. Expansionary fiscal policy to fight inflation will not help, and elevated energy prices will lead to lower production levels and support inflation, which could also push up long-term yields.

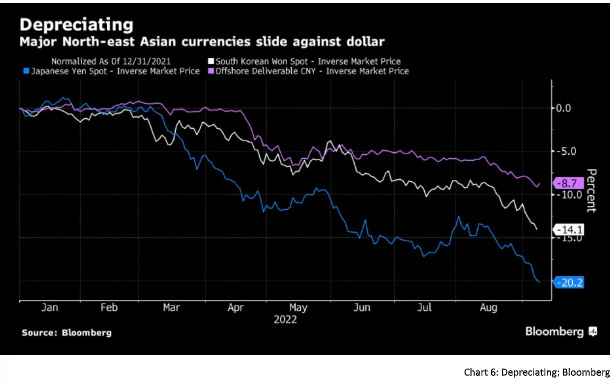

Regarding FX markets, the dollar will remain strong, eventually, currencies from resource-rich developing economies. Asian currencies will have a hard stand against the dollar. Since the beginning of the year, the exchange rate for the Chinese Yuan and the South Korean Won against the dollar has slid.

Housing is currently rolling over due to the rise in yields, suggesting that the good times are over. For the first time since 2020, American consumers expect falling house prices.

The picture in commodity markets is mixed. Lots of them have gone down recently, but I still expect that they will rise again down the road. However, expect possible price corrections.

The most dominant topic will be energy markets. Expect interventionist policies that will not improve the situation significantly. Sadly, the number of protests all around Europe will go up. Recently, 70 thousand people in Prague protested against rising energy costs.

European governments risk losing the public at some point, where more and more will question the sanctions. I do not think that the question is who suffers more from the sanctions, and it should be evident that they cause huge problems for the Russian economy.

However, the question is if the European public is willing to suffer as much as the Russians. If Europe stops consuming Russian energy, this would have enormous economic consequences, like more insolvencies and unemployment. As governments try to solve the problem from the fiscal side, you will see debt monetization at some point. Sadly, as interventionism does not solve any of the underlying issues, I fear there will be a rise in populism. With them, things will not turn for the better, I guess…

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)

T