VirUS

I like to say that we injected cocaine and heroin into the system, and now we're maintaining it on Ritalin. How's that? [LAUGHTER]

October 2022 was a good month for equity markets, and the Dow Jones Industrial Average even marked its best month since January 1976. Back then and today, the terms inflation and energy crisis dominated discussions about world economic development. However, in January of 1976, US inflation had nearly halved from its peak in October 1974, while today, it is still close to its cycle high from June. Meanwhile, Eurozone inflation accelerated to another high in October.

Although inflation remains high, Wall Street repeatedly calls for a Fed pivot (again). For example, RBC US chief economist Tom Porcelli wrote that the Fed would set the groundstone for smaller rate hikes down the road on Wednesday, and he should be proven right. Many investors were also betting on a pivot, given that global equity funds noted their most significant capital inflows since March, 23 billion US dollars.

The initial reaction after the FOMC decision was indeed pivotish. Stocks and bonds rallied because the statement said that the Fed would slow the pace of rate hikes at future meetings. For the fourth time, it raised interest rates by 75 basis points, and likely a 50 basis point hike will follow at the next meeting. However, the rally should be short-lived because Powell crushed all hopes for a pivot again at the following press conference. He declared that, although the Fed is planning to deliver smaller rate hikes, it will continue to raise interest rates for longer.

It is pretty obvious why so many people on Wall Street are calling for a Fed pivot. So far, 2022 has been the worst year on returns in decades for them. Central banks' monetary policy has infected the whole investment world with the easy money virus; despite inflation. That is why I decided to cover the topic of the year, inflation, this week.

While consumer price inflation remained low after 2008, many economists and analysts declared that this was the empirical evidence that monetary policy hardly affected actual inflation (CPI). Indeed, that would sound plausible if one assumed a linear relationship between money supply and CPI. But, as often, it is more complicated…

After the Great Financial Crisis in 2008, central banks tried to spur inflation through bond-buying programs. As we know today, the attempt utterly failed. What had not worked in Japan should not work in the United States or Europe. Yet, people who prophecized a vast rise in consumer price inflation were equally wrong.

Both camps wrongly assumed that inflation was linear and that QE would raise prices broadly. However, the newly created money never found its way into the real economy and kept circulating in financial markets. Artificially lowered interest rates made investments in the real economy and consumer goods less attractive than financial asset investments. Additionally, the central bank's intervention in financial markets leads to longer supply chains.

If analysts and economists had remembered Richard Cantillon, they would have known that. Cantillon observed that new currency units spread slowly through the economy and only raise prices where these currency units increase demand. After 2008, demand rose in asset markets.

Let us remind ourselves how Quantitative Easing works to understand the effect better. Besides lowering short-term rates via the central bank rate, central banks bought bonds on the secondary market. In the US, the Fed only bought treasuries and MBS (until 2020), while the ECB also purchased corporate bonds.

As a result, Central banks cause additional demand for bonds on the secondary market, and prices rise. If the Fed buys a bond, the bond appears on the asset side of its balance sheet, while the seller (banks, insurance companies, pension funds, …) gets newly created money (bank reserves) in exchange. Those reserves need to be reinvested in stocks or bonds, and that additional demand leads to further price increases.

Yet, bank reserves are not necessarily crucial for bank lending, particularly when the central banks flushed the system with them as they did after 2008. If a bank makes a loan, it simply adds money to the borrower's bank account and extends its balance sheet with another claim.

As I mentioned earlier, artificially lowered interest rates make financial investments more profitable than real economic investments. Banks are also incentivized to invest in asset markets, as lower rates make issuing a loan to a risky, real economic project less attractive.

Thus, we can conclude that this elevates asset prices and drives banks out of their classic loan-making business into financial speculation. Further, history assured them that whenever a problem occurs, central banks will show up and rescue markets. The result was more reckless behavior or moral hazard.

For as long as newly created money is circulated within asset markets, either through reinvestments or bond issuances for stock buyback programs, consumer prices rise only slightly. All in all, low-interest rates incentivize governments to increase spending and load up on more debt than when rates are higher. Governments mostly borrow money to spend on infrastructure projects, pensions, or other social security payments. Hence, only a tiny portion of the newly created money (or bank reserves) finds its way into the real economy, leading to little inflation.

However, manipulating interest rates has not solved the underlying problems beneath the surface. On the contrary, the policy kept businesses alive that otherwise would have been forced to exit the market. The result is a zombification of the economy, and more malinvestment as unprofitable projects suddenly became profitable because of suppressed interest rates.

As soon as central banks ended their bond-buying programs in the 2010s, trouble in financial markets occurred. Stock and bond prices stagnated and moved sideways because the continuous flow of new money suddenly stopped. However, the money was still contained within asset markets because of a lack of real alternatives. Chart 1 shows that every stop of QE sooner or later led to another, more extensive QE program.

That shows the main problem of such emergency measures. Arguably, it is okay to implement such a measure only once (although even that is debatable) to keep the system from collapsing. Yet, such policies do not solve any underlying problems; they merely buy some time. At one point, the imbalances need to discharge. But in that case, central banks usually show up again with another rescue package to save markets because it worked so well last time. But every following program needs to be bigger than the previous one and creates more imbalances.

In 2019, the Fed had to end QT because of market turbulence. Central banks and governments overreacted when markets got in severe trouble in the spring of 2020 because of the starting pandemic and expected lockdowns. Slashing interest rates down to zero, massive bond-buying programs and big loads of fiscal stimulus were implemented by central banks and governments. While central banks tried to calm down markets, governments subsidized workers stuck at home, sitting in lockdown.

Those policies flushed record sums of money into the financial and the real economy at the time when lockdowns put a big part of the economy on halt. However, because of the lockdown policies, that did not lead to consumer price inflation at first. People got a lot of money but had no place to spend it, and much of it flew into financial markets.

Then, when the restrictions were lifted step by step last year, the savings rate started to come down a bit, and people rushed back into consumption. Yet, the demand pick-up caused supply chain problems, and inflation started to rise substantially for the first time in years.

Central banks made a huge mistake in 2021 because their models suggested that those price increases were transitory and deflation would remain the much more significant threat down the road. Since 1980, the rise in globalization has led to deflationary tendencies in Europe and the United States. They imported consumption goods from new trading partners and exported newly created currency units (inflation). Primarily the United States benefited because of the dollar’s status as the world reserve currency during that period.

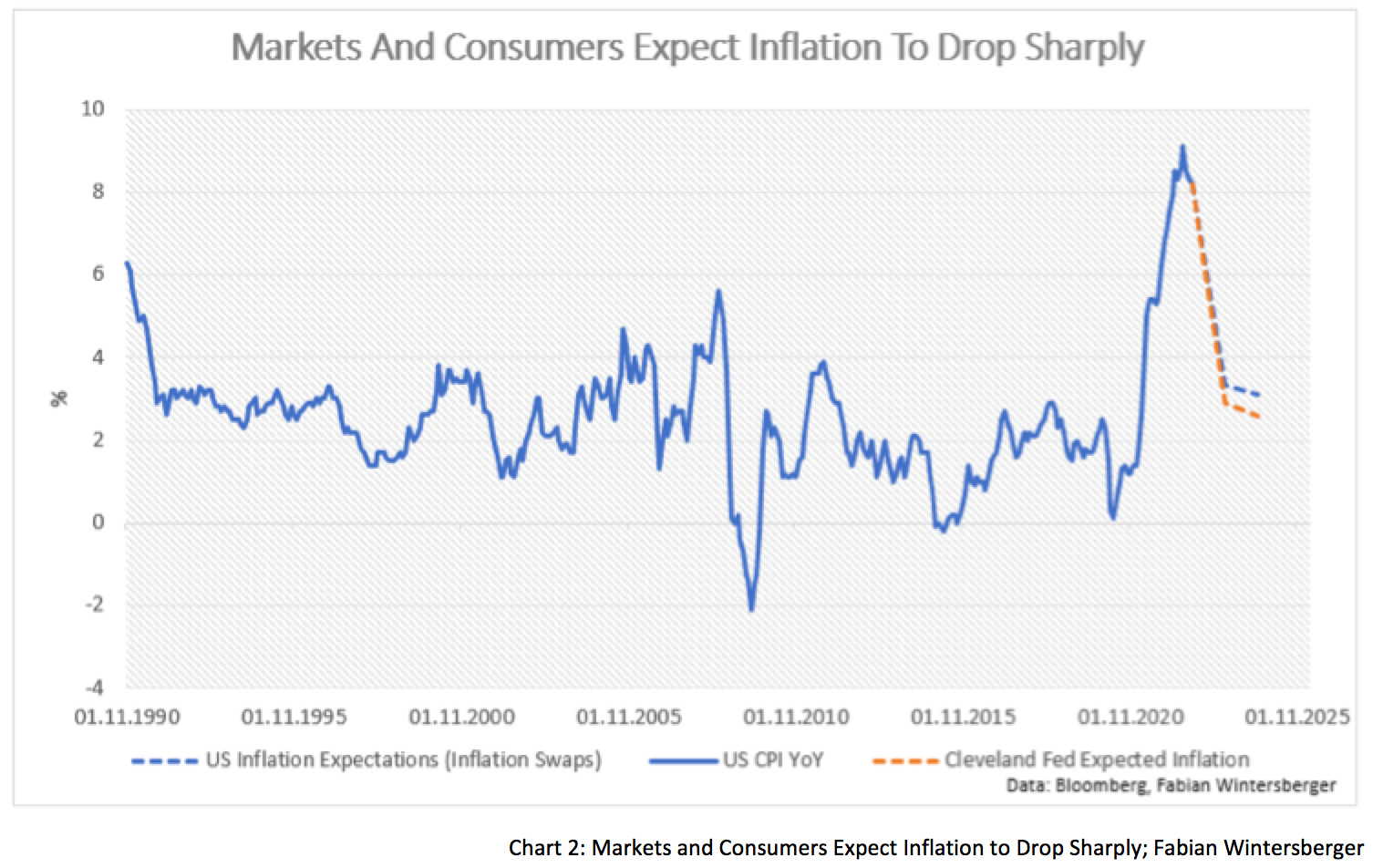

Nevertheless, inflation continued to rise until central banks finally threw in the towel and admitted they were wrong. To deliver on their mandate of stable prices, they had to tighten. The energy crisis, the Russian invasion, and the effects of the western sanctions fueled inflation further. With recession looming on the horizon, market participants are now assuming that it will help central banks in their fight against inflation.

In my opinion, it is doubtful we will see such a disinflationary impulse as expected by market participants. Why? Because the economy is very different from what it was pre-pandemic. People’s preferences have changed since covid, and globalization is on retreat because of Cold War 2.0. It seems that the deflationary forces that have been in place since 1980 are reversing.

If one analyzes all periods since 1940, when inflation rose above 8 %, one finds that it usually takes about two years for inflation to return to 2 %. In my view, the market may be underestimating the farther path of inflation.

The fastest return to 2 % happened when inflation peaked in 1951 because of the Korean war. However, the peak in inflation was not caused by a rise in the money supply but by behavioral changes of market participants. After the first inflation peak in the 1970s (1974), inflation did not return to 2 % and rose again from 1976 to 1980, when inflation peaked at 15 %.

Suppose one takes into account the change in preferences (home office, higher demand for durables) and rising production costs due to rising wage pressures and high energy prices. In that case, one could assume that the disinflationary effect could be similar to the 1970s. We will see, as QE and QT did not exist back then, and we do not know if governments will start financial repression at some point (very likely).

In his press conference on Wednesday, Powell clarified that the Fed would not pivot anytime soon. The Fed will continue to increase interest rates and QT. And in my opinion, this could have the side effect that consumer price inflation will stay elevated.

When the Fed does QT, it is shrinking its balance sheet by letting the bonds expire without reinvesting cash flows or via active selling in the market. In both cases, it means that the Fed stops elevating demand for bonds, and prices must fall, ceteris paribus.

In the case of active selling bonds back into the market, one can expect bond prices to decrease further. Actual data does not support the claim that the market is already resigning. Regularly, huge sums flow into the bond and stock market to buy on dips.

Transfer payments by governments helped to push markets up further. Now, as asset prices start to fall, this money may be escaping financial markets again. Real estate prices are also falling because of the significant rise in mortgage rates.

Now, the argument that QE is just an asset swap and does not increase the money supply may fall short. I agree; as long as markets only go up and rates are low, the money is trapped in the financial economy. However, it was created (by central banks) and is in the (financial) system.

Even if we assume that banks reinvest their QE reserves back into treasuries, we can assume that the supply of money rose afterward because the reserves will be able to buy more treasuries at a lower price. However, if all reserves are reinvested into bonds or stocks, there will be no consumer price inflation.

But given that markets are going down, is that probable? I think it is not and would further argue that it is likely that money starts to escape financial markets and flows into the real economy to elevate consumer price inflation, even though the inflation number continues to fall because of the base effect. Additionally, the market share of retail investors in the total market doubled between 2011 and 2021, from 10 to 20 %.

That development is just starting, with QT only a few months old, but it could point to a shift in demand from paper wealth assets to tangible economic goods.

Additionally, one cannot expect the US government to support the Fed in its fight against inflation. The Biden Administration announced that it plans to help families suffering from the latest increase in energy prices with another 13 billion dollars. In my opinion, without significant cuts in fiscal spending, the Fed will do hard to bring inflation back down to 2 %.

The final point I want to make is one I mentioned two weeks ago in The Signal Fire. Stuffed with reserves and without needing additional deposits, banks can make a fortune by expanding their loan books. A rise in bank lending is inflationary because bank money goes directly into the real economy.

It needs to be seen if one observes more evidence that the non-linear effects of QE get exposed by QT while the west is on the road to the recession. Still, it would again reveal how shortsighted monetary policy has become after 2008. Mainly, monetary policy was primarily justified by the threat of deflation and depression.

However, in 2004 economists from the Minneapolis Fed published a paper that concluded that

Our main finding is that the only episode in which we find evidence of a link between deflation and depression is the Great Depression (1929—34). We find virtually no evidence of such a link in any other period.

So, it seems that central bankers might have sharply overreacted in 2008 and infected the financial world with the cheap money virus, or, as Richard Fisher said, set the market on drugs.

However, one should bid farewell to the fact that central bankers are omniscient and capable of setting the optimal interest rate. The last few years, in particular, have impressively demonstrated how little central bankers actually know

They wanna make us believe, in everything that they preach,

Manipulate our trust, to feed the virus in us.

-Caliban - VirUS -

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)

"But every following program needs to be bigger than the previous one and creates more imbalances." The money quote, and the source of all the problems we currently face.

excellent summation Fabian, thanks and good weekend