This Continuum

On Markets, Power, and Systemic Constraints

January isn’t even over, yet the geopolitical news cycle is moving faster than it has in a decade. The capture of Maduro, the attempted revolution in Iran, renewed attention on Greenland, and Trump’s rhetoric that the US “needs” Greenland for national security have all unfolded within a matter of weeks.

Once again, the US president threatened tariffs against opposing countries, causing renewed nervousness in financial markets. The EU signaled its readiness to fight back forcefully, discussing a wide range of countermeasures. For now, the situation has calmed again (more on that later), but it is worth examining the impact of a particular measure that was proposed.

Why Treasury “Leverage” Misunderstands the Dollar System

On Tuesday, news emerged that the Danish pension fund AkademikerPension will exit t its US Treasury holdings over concerns about US debt sustainability. A day later, Swedish pension fund Alecta announced that it would cut its Treasury holdings due to “increased risk and unpredictability.” Also on Tuesday, the Financial Times published an opinion piece by CFR member Rebecca Patterson, who argued that threatening to liquidate Europe’s US treasury holdings could serve as leverage in negotiations.

To unpack this, it must be said that these announcements sound significant on paper but are, in reality, largely irrelevant for price discovery in the US Treasury market. AkademikerPension’s holdings amount to roughly $100 million, and Alecta sold approximately $7.7–8.8 billion in total, less than 0.3% of all treasury debt outstanding.

While one could argue that this might be the beginning of a narrative that pushes Treasury yields higher, it is not the “leverage” that commentators like Patterson suggest. Purely in theory, large-scale selling of US Treasuries by European entities could trigger a short-term price spike. However, this view overlooks how the global financial system actually functions.

When Nixon closed the gold window in 1971, the system shifted from one with gold as the base layer of the monetary system to a dollar standard. Since then, the dollar has replaced gold as the core of the global financial system. As a result, any selling of USD assets abroad is constrained by the persistent demand for dollar assets that is embedded in the global financial infrastructure.

International trade runs on dollars, and countries that invoice trade in other currencies—such as the euro, the yen, or the Chinese yuan—still need to recycle those flows back into US dollars, primarily via US Treasuries, to participate in global markets. Even when trade settlement occurs outside the dollar, global liquidity, collateral, and reserve management remain overwhelmingly anchored in US Treasury markets.

As a consequence, European selling of US Treasuries is likely to be absorbed by other buyers attracted by more favorable prices. When European countries later need dollars again for international trade, the resulting price swing—driven by renewed demand—could be strong enough to force them to buy dollars back at a loss. In this sense, the supposed “leverage” is illusory and would likely hurt Europe far more than the US.

Tacos & Dips

Reports of Treasury selling and tariff threats triggered another bout of volatility in financial markets. Bond yields and equities both declined, with stock markets erasing all of their 2026 gains. Surprisingly, market participants once again took Trump’s rhetoric at face value, despite his long history of backing down.

After Trump’s speech at the WEF in Davos—where he ruled out military force—and a meeting with NATO Secretary General Rutte, Trump stated on Truth Social that tariffs are off the table for now. The sell-off in equities was halted once again, and markets rallied on the news. While details reportedly still need to be worked out, that reassurance was all market participants needed to hear.

This week’s “sell America” trade appears to have ended before it really began. Moreover, if last year’s “Liberation Day” episode is any guide, foreign sellers are likely to return quickly, as analyst Joseph Wang pointed out.

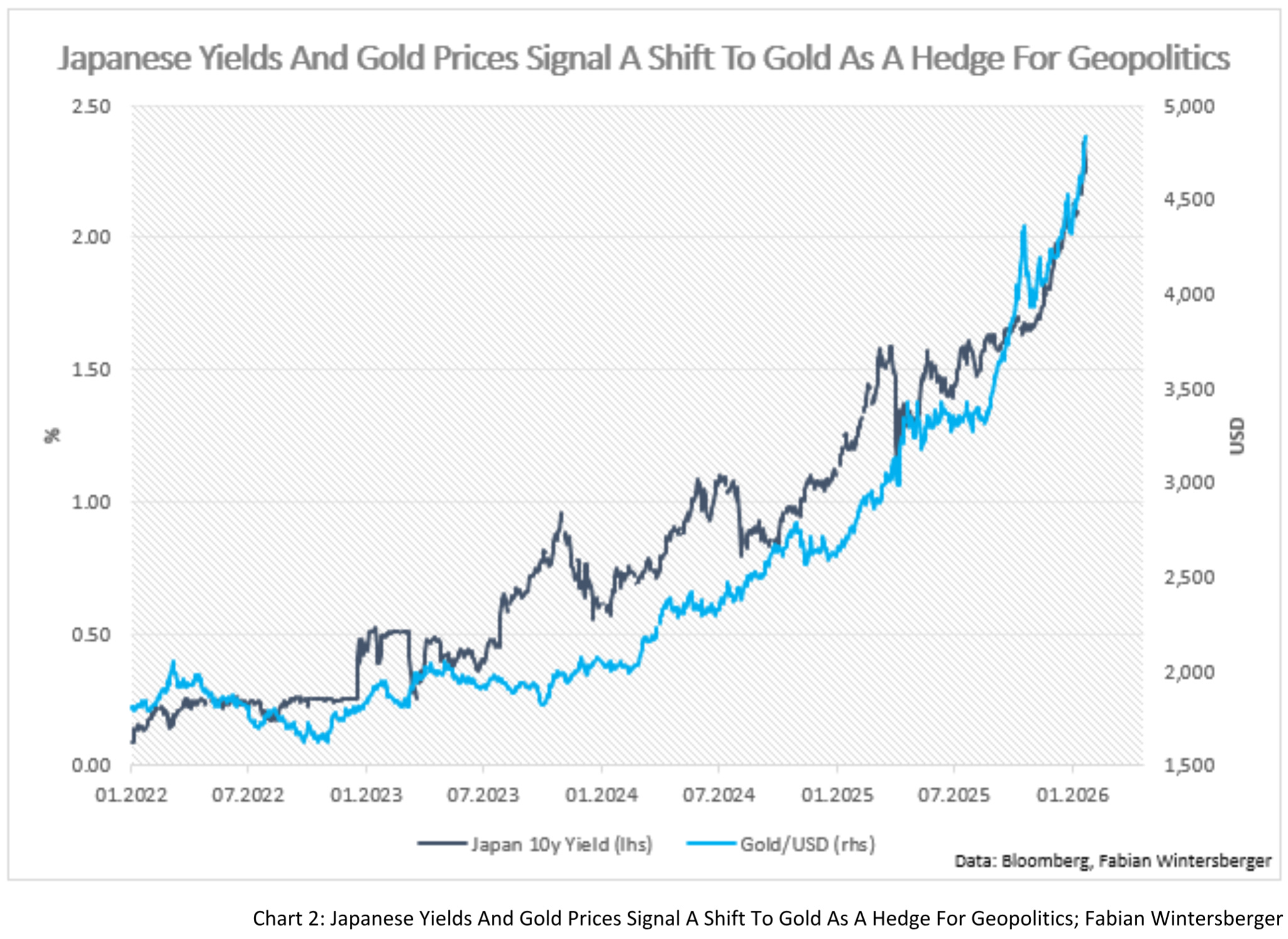

Higher Gold Prices, Higher Floor For Government Bond Yields

The week was also another strong one for precious metals. Gold rose by roughly 5%, while silver gained about 4.6%. At the same time, the renewed rise in long-term bond yields was again led by Japanese government bonds. Beyond the Bank of Japan’s more hawkish shift, Prime Minister Takaichi announced a snap election and large tax cuts to stimulate the economy—without explaining how they would be financed. Together, these factors put significant upward pressure on yields, likely contributing to the recent rise in precious metal prices.

This interpretation is supported by an S&P Global Study, which found that the usually inverse correlation between gold and bond yields tends to flip when geopolitical and global economic risks become more prominent. In times of heightened uncertainty and deficit concerns, investors increase allocations to precious metals as a hedge against debt sustainability risks. With equity markets rising, these allocations typically come at the expense of bonds, assuming a traditional 60/40 portfolio.

As geopolitics continue to gain importance for financial markets, bond yields are likely to find a higher floor than in the past. This supports the view that even a strong bid for bonds may not be sufficient to push yields back down to pre-2020 levels.

Who Pays The Tariffs?

At Davos, Trump once again praised his tariff policies, arguing that “instead of raising taxes on domestic producers, we’re lowering them and raising tariffs on foreign nations to pay for the damage that they’ve caused.” While this rhetoric suggests that foreign countries bear the cost of tariffs, a growing body of evidence continues to support standard economic theory.

This week, Germany’s Ifo Institute published a new study examining how the burden of tariffs is distributed among exporters, importers, and US consumers. Unsurprisingly, the study found that the vast majority of the burden falls on US importers and consumers. Only about 4% of tariffs are absorbed by exporters, while the remaining 96% are borne by American buyers.

As a result, the US administration’s tax cuts amount to a near-zero-sum game for consumers, who ultimately face higher prices. In the US context, tariffs therefore function much like a consumption tax: they transfer wealth from consumers to the government, while Trump’s business tax cuts ensure that the burden ultimately shifts away from US firms.

Now, let us move beyond the news and turn to the implications for financial market price dynamics.

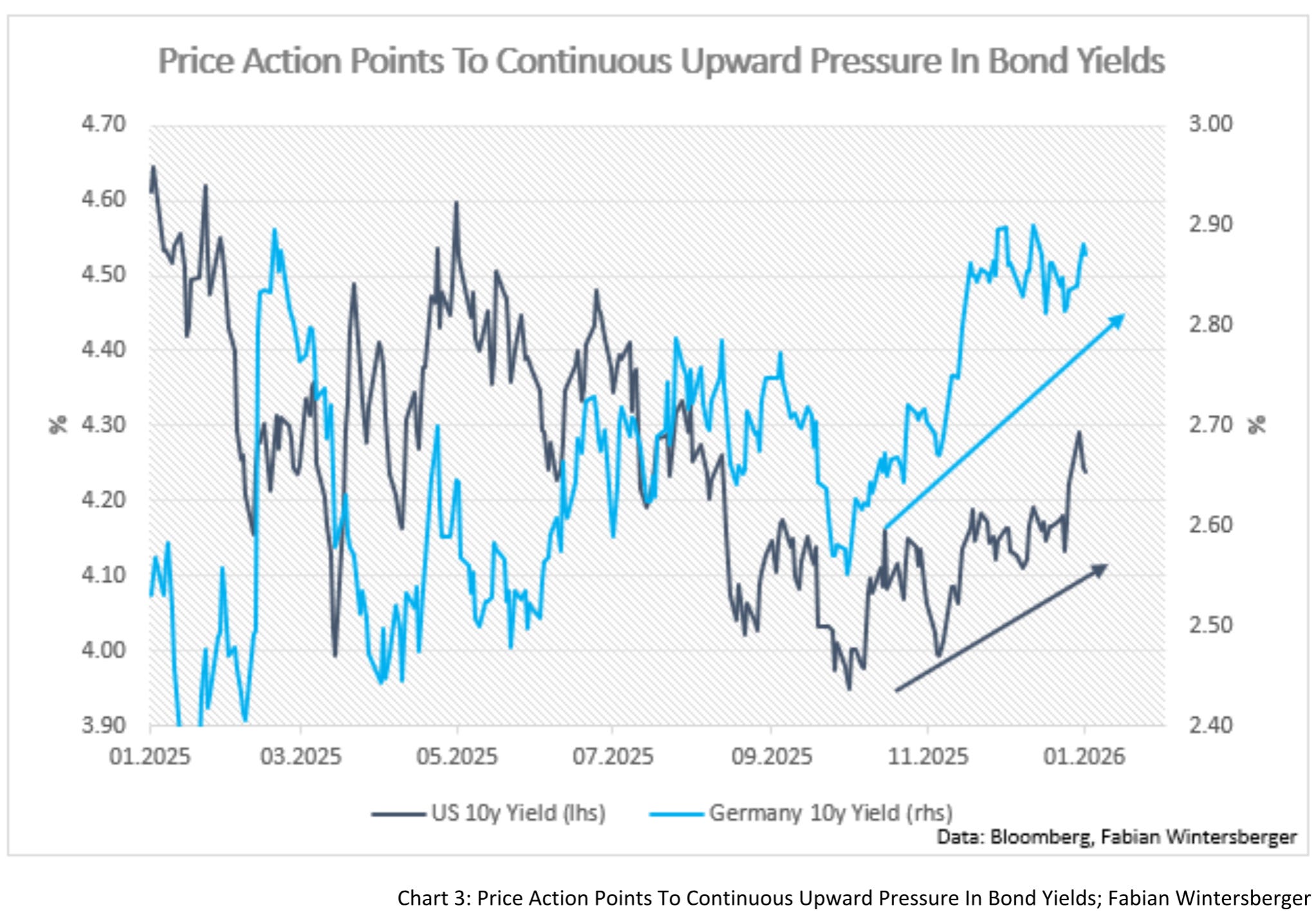

Bonds & Interest Rates

With the continued rise in long-term Japanese yields and the implications for precious metals discussed above, conditions in the bond market remain largely unchanged from last week. There is still no sign of a meaningful turnaround that would point to declining yields. On the contrary, price action suggests either a further rate increase or a continuation of the current sideways trend.

In addition, there is little to suggest that either the ECB or the Fed will need to deviate materially from market expectations regarding the future path of monetary policy. This further supports the outlook for stable to gradually rising yields.

Stocks

As discussed above, this week’s sell-off once again appears to have offered another opportunity to buy the dip. Price action continues to indicate that the broader upward trend in equities remains intact. Given Trump’s statement in Davos that the stock market could double during his term, it is difficult to adopt a bearish stance for now.

This administration places great importance on equity markets and is likely to use every available lever to support further gains. Betting against that implies betting that policymakers will refrain from running the economy hot in an attempt to grow out of the debt burden. At the same time, increasing market breadth and the weaker relative performance of the “Magnificent 7” continue to point toward a broadening rally.

FX

Following the latest Trump “TACO,” the outlook for EUR/USD remains broadly unchanged, with price action pointing toward a sideways range and a potential slight upside for the euro. As long as expectations of accelerating eurozone growth persist and the ECB maintains a more hawkish stance than the Fed, this dynamic is likely to continue.

Meanwhile, the Japanese yen remains under pressure for the reasons discussed above. Absent direct FX intervention, it is difficult to see significant upside for the yen in the near term. The current downtrend would first need to stabilize before the situation can be reassessed.

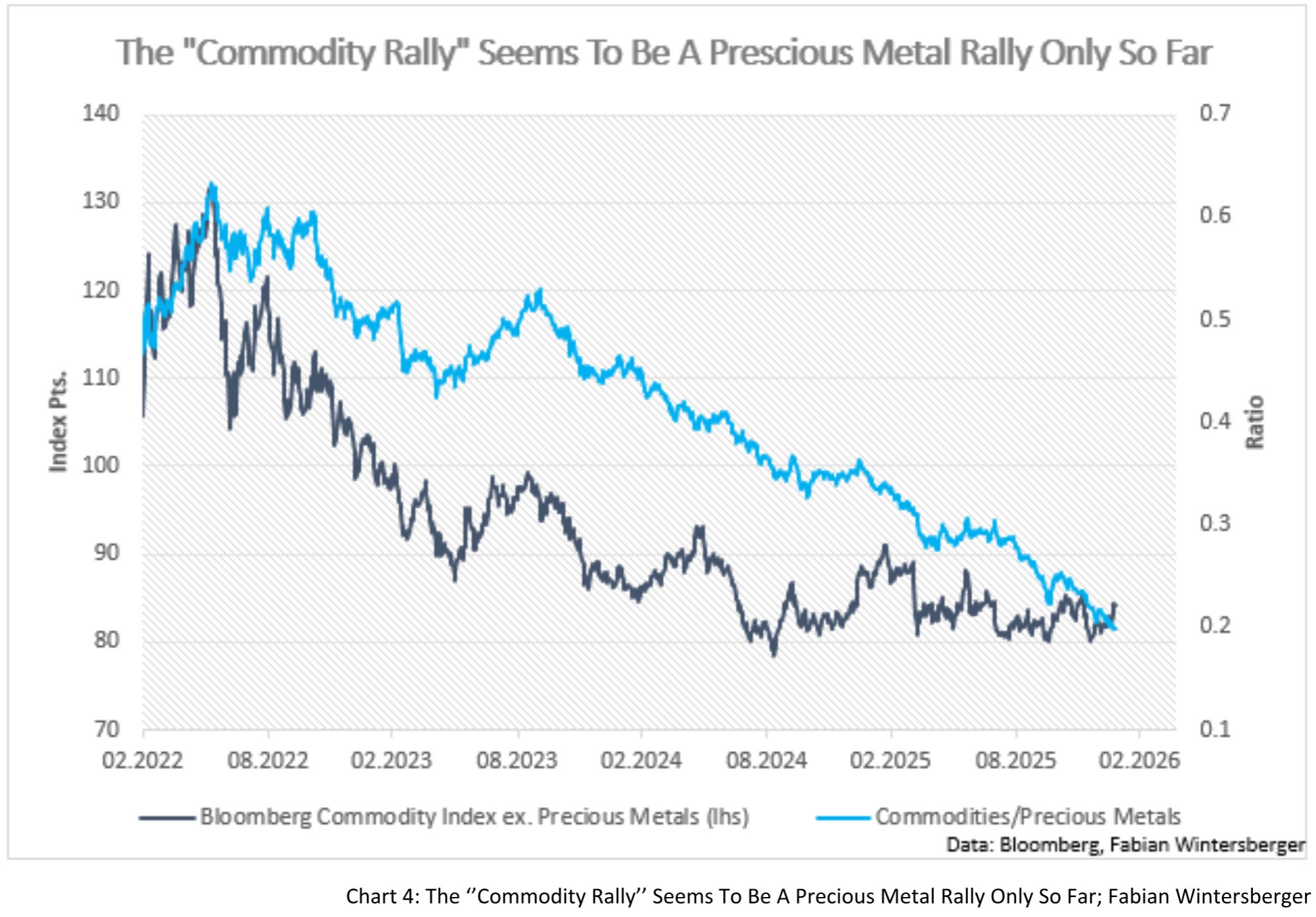

Commodities: Commodity Super-cycle Or Just Precious Metals

In commodity markets, many observers argue that we are on the verge of another commodity supercycle. So far, however, price action has been driven primarily by precious metals, as well as by natural gas and heating oil due to cold weather conditions. While it is certainly possible that commodity prices will rise more broadly over the coming years, the evidence so far does not suggest that such a cycle is imminent.

This view is supported by the continued downward trend in commodities excluding precious metals, as well as by the declining ratio of commodities to precious metals.

Overall Assessment & Conclusion

While the debate around Greenland influenced short-term price action, it ultimately proved to be little more than a distraction and is unlikely to alter the broader trajectory of financial markets. Conditions continue to favor equities over bonds, while precious metals may still have some room to run. Key levels to watch are $100 per ounce for silver and $5,000 per ounce for gold, where the rally could encounter resistance. That said, the broader trend for precious metals remains upward.

For now, markets remain firmly within their prevailing “continuum.” As long as this persists, pullbacks are likely to represent buying opportunities in equities. Trump’s Davos speech and the planned spending initiatives across Europe should continue to act as tailwinds for bullish sentiment. The key question is when rising long-term interest rates will begin to pose a meaningful headwind for growth and financial markets.

I can’t face this hell alone

Spiraling through this continual

Time has taken all I’ve known

Swallowing the life I used to knowThrowdown – This Continuum

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.

Eastern Europe would prefer to be annexed by the US rather than EU