They're All Around Us

From oil shocks to AI hype: the hidden system tying it all together

The problem is not that planners are ignorant, but that they cannot know what they need to know.— Friedrich August von Hayek

Markets breathed a sigh of relief this week when Trump didn’t follow through on his threat to bomb Iran back into the “Stone Age [sic!].” But if one hoped for more clarity on how this war is going to continue, or end, I have to disappoint you.

The only clear takeaway is that the White House doesn’t like oil prices above $100 per barrel, nor falling stocks and bonds. It’s quite astonishing how financial markets increasingly appear to dictate Trump’s decisions, even as the war itself looks increasingly prone to spiraling out of control.

In the grand scheme of things, however, the region still appears far from reaching any meaningful peace agreement. The bigger picture suggests that major economic disruptions may lie ahead and markets will have to adjust. The difficulty is that things can unfold in multiple directions. With AI, geopolitical turmoil, and a shift away from free trade toward more economic planning, the outlook feels more uncertain than, to keep with Trump, “ever before.”

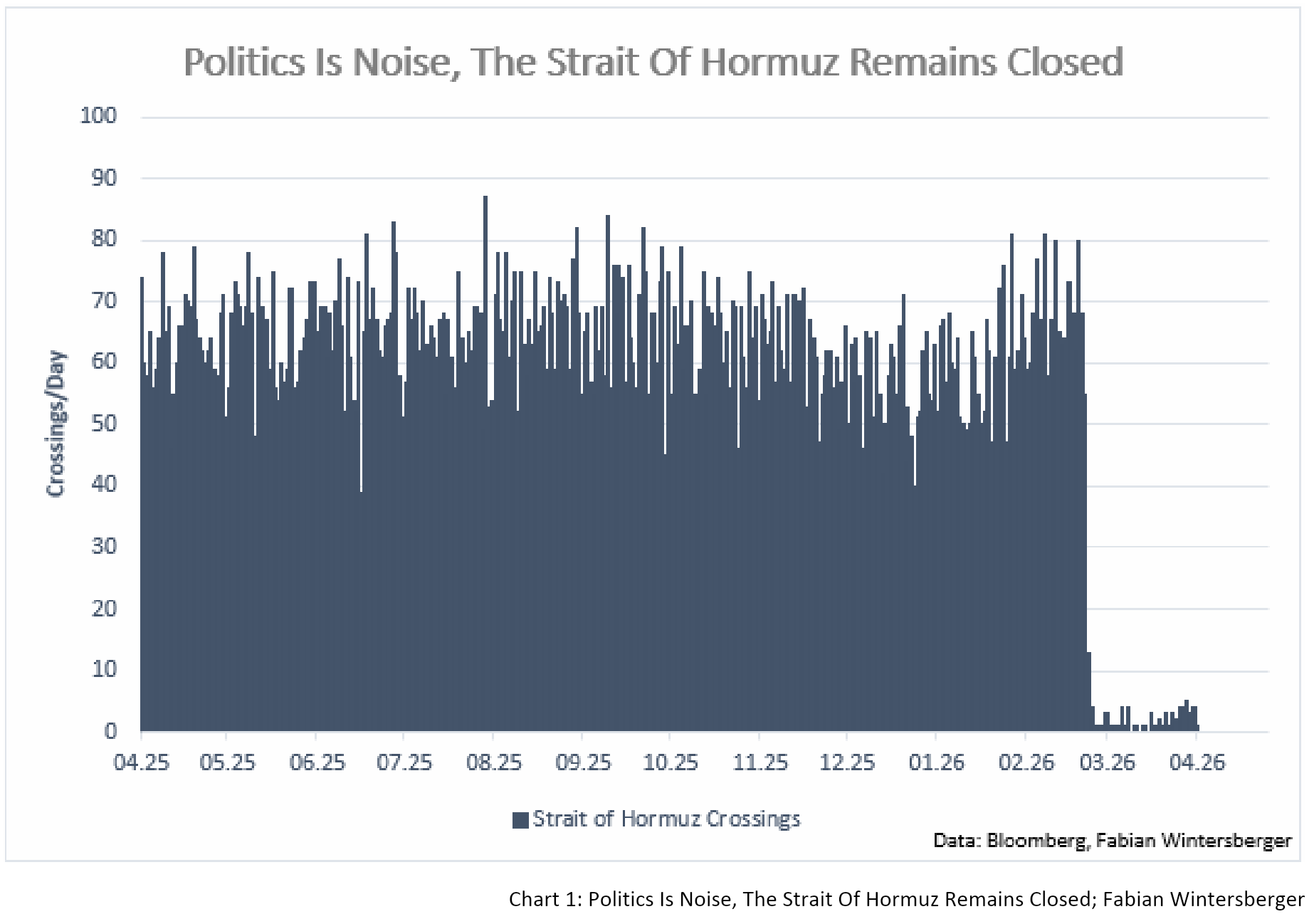

Cease, Fire, Ceasefire, or Peace Is Noise, Oil Is Still In An Upward Trend

My fear of troops on the ground didn’t materialize, at least not yet. Trump’s threat turned into another TACO, but one should be thankful for that. On Tuesday evening, just minutes before his deadline expired, Trump announced a ceasefire with Iran and, more importantly for markets, that the Strait of Hormuz would soon reopen.

Stocks and bonds exploded higher on the news and gapped up on Wednesday. Oil crashed more than 10 percent overnight, with Brent falling to almost $90 per barrel. It was more than just relief; it looked like a turning point, where markets began to look through the bad news. At least, it seemed that way.

As of writing, another day has passed, and the ceasefire appears to have as many holes as Swiss cheese. Attacks on Iran have not stopped, Israel continues to strike Lebanon, and Iran continues to attack Israel.

Iran has already accused Israel of violating the ceasefire, while Israel claims that Lebanon is not included in the agreement. Trump posted that he agrees with the 10-point plan proposed by Iran, but his press secretary, Karoline Leavitt, said it was thrown “into the trash.” As with so much in this war, no one really seems to know what is actually going on.

What is certain, however, is that the Strait of Hormuz remains closed, for now. That makes the market’s euphoria look premature. As long as the Strait remains closed, the problem has not gone away. It may be talked down in paper markets, but in the physical world, the constraint remains.

Additionally, the assumption that the US is less vulnerable to disruptions in the Middle East than the rest of the world appears questionable. On a relative basis, gasoline prices in the U.S. have risen more than in other regions. According to Goldman Sachs, the U.S. still depends on certain oil products from the Middle East. Although the U.S. is a net energy exporter, oil is not a uniform commodity—refining configurations and product demand matter. The idea that the U.S. can simply dismiss Middle East disruptions is increasingly proving false.

The backwardation in the oil market, where near-term futures trade above longer-dated ones, does not imply that the crisis will resolve soon. It reflects extremely strong current demand relative to future expectations. You want the barrel today, not tomorrow, because storage is being drawn down amid supply disruptions. Basic economics suggests something has to give, either in paper or in physical markets: rising demand, through front-loaded purchases, and constrained supply due to near-zero transit through Hormuz imply higher prices.

Every day that passes without oil shipments through the Strait intensifies this dynamic. In that sense, I expect oil price action to continue pushing higher. As long as the bullish trend remains intact and the crisis is not truly resolved, every dip in oil is a potential buying opportunity, in my view.

The AI Boom: A Productivity Miracle Or Malinvestment?

It is widely recognized that a drop in energy supply has crippling effects on markets. Less energy consumption means less productive output and therefore drags on the economy. Substituting energy with other factors of production is difficult, because energy is required for everything: machines need power, humans need food, and food production itself requires energy.

The way out would be if, on a relative basis, increasing artificial intelligence usage were cheaper than human labor. That might be true in the case of “reliable AI,” but how reliable is AI really? If it can produce reports faster but still requires human oversight, then it adds cost rather than reduces it, especially if output growth does not compensate for the additional burden.

Investing in AI may still seem reasonable if the energy constraint is eventually resolved. However, a recent Bloomberg article by Merryn Somerset Webb argues that the current AI boom rests on fragile foundations. The real bottleneck is data, which is finite and increasingly polluted by AI-generated content.

More importantly, large language models are inherently flawed. One can think of their outputs like those of an econometric model. They process inputs and generate probabilistic answers rather than verified truths, making errors unavoidable and often undetectable. This confines their usefulness to low-stakes, verifiable tasks rather than mission-critical applications.

Webb concludes that the massive spending by hyperscalers on data centers looks increasingly like a misallocation of capital. Scaling does not resolve these structural limitations, and meaningful progress may require entirely new approaches. With cheaper alternatives already available, investors may be better off avoiding hyperscalers and favoring more cautious players.

Huge investment into AI infrastructure could therefore turn out to be malinvestment, where costs exceed the benefits. It channels capital into the AI economy, often via government involvement and central planning, while it may be needed elsewhere.

This ties into the broader trend toward more government-guided economic production. It creates unstable, short-term equilibria that require constant policy intervention, leading to higher volatility and economic inefficiency. Within the global “dollar prison,” these losses ultimately need to be absorbed, likely through future monetary expansion. And that brings us to central banks.

Central Banks, Stagflation And The Reaction Function

One could easily forget that there are other things besides the war, like the March ISM report, the Nonfarm Payrolls we got last Friday, and the new US CPI report that will come out this Friday. And that leads to the question of how central banks, or in this case the Fed, will have to deal with all of that.

The March ISM Services report points to an economy that is still expanding, but in a more stagflationary way. On the production side, activity and new orders still point to growth, suggesting services output remains resilient and GDP is still expanding. But that growth is becoming less efficient: activity has slowed sharply, employment has slipped into contraction, supplier deliveries have worsened, and firms are stockpiling against supply disruptions. In short, production is still growing, but with more friction, more uncertainty, and weaker labor demand.

What’s worrying is that the prices paid index surged to 70.7, its largest monthly jump in more than 13 years, while respondents repeatedly cited higher oil, fuel, freight, metals, and logistics costs tied to the Iran conflict and supply chain disruptions. That combination, still positive output but slowing activity, falling employment, delayed deliveries, and sharply rising costs, is classic stagflationary pressure: the economy is not collapsing, but growth is getting more constrained while inflationary impulses are intensifying.

The question is what that means for the Fed. Should it look through this “supply-driven” inflation, or will it? The market has largely priced out any hopes for rate cuts in 2026. But with Warsh coming in at some point, presumably, the question is whether that could change the Fed’s reaction function.

On the one hand, one can argue that the situation has changed with the war. On the other hand, one could argue that his appointment points to a more politicized Fed, and thus a bias to move forward with rate cuts anyway, despite the expected short term rise in consumer prices.

I tend to think that a Warsh led Federal Reserve will be more likely to cut rates than to wait and see. But there’s another issue tied to the second half of the Fed’s mandate: employment. A Fed note from April 2 suggests that breakeven job growth is close to zero, which means that even modest job gains could tighten the labor market further and keep unemployment low. At the same time, jobless claims data suggest that workers are not being laid off as quickly as they are able to transition into new jobs. The result is a tight labor market with persistently low unemployment despite weak job growth.

It’s difficult terrain to navigate: above target inflation and a tight labor market would normally rule out rate cuts. But in an environment where government guided investment requires continued capital inflows, there is pressure to push rates below equilibrium to sustain the cycle.

As long as Powell remains at the Fed, I see no rate cuts coming. But with Warsh coming in, the tides could turn. And if they do, I’m sure they’ll find a reason to cut, despite the fact that any weakness caused by malinvestment will ultimately require even lower rates. As a result, I’d argue that the market is underestimating the rising political influence at the Fed, and that rate cuts later this year cannot be ruled out.

Market Assessment

The market assessment has not changed meaningfully, despite the sharp upward move in stocks and bonds after the ceasefire. My short-term outlook for bonds and stocks remains bearish, although I continue to think it is better to stay out of the market and be ready to deploy capital once the dust settles.

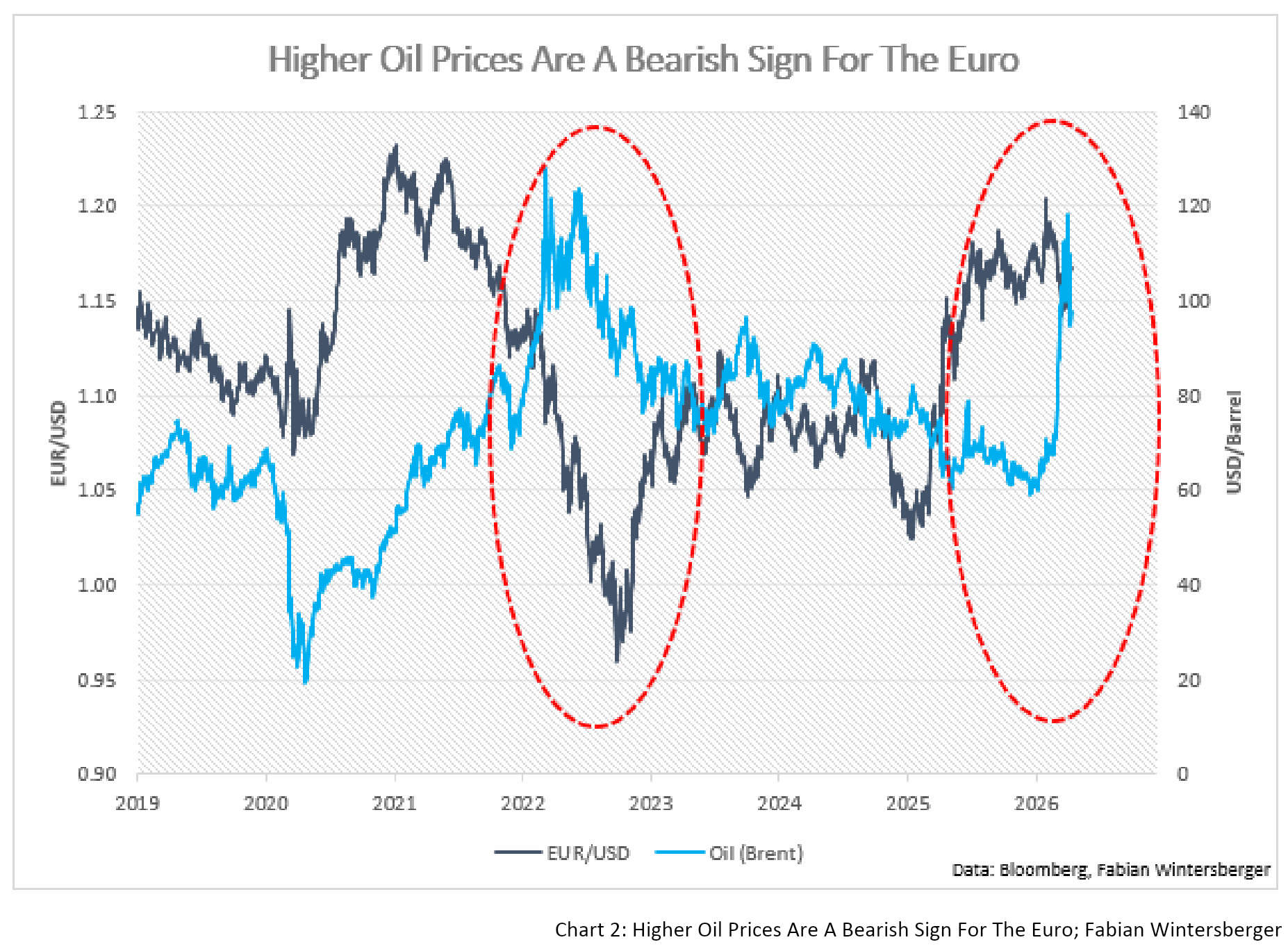

What’s particularly interesting is the FX side, especially the link to oil prices. If the assumption of oil prices staying above $100 turns out to be correct, that would have bearish implications for EUR/USD, as Europe has maneuvered itself into a corner when it comes to energy imports.

Conclusion

With the ceasefire in place, but disagreement about its terms and no reopening of the Strait of Hormuz, the broader picture remains unchanged. If one assumes that disruption was part of the strategy all along, alongside increased US control over supply choke points, that would fit into the broader theme of expanding government control over economic outcomes.

But that relies on lower interest rates to fund domestic AI investment and to reduce the cost of subsidizing it. While no one is paying attention, the signs increasingly point to a weaponization of the dollar, forcing the rest of the world to absorb part of that transition toward US production and investment. As discussed, that is a shaky foundation, but I have little doubt the US will attempt to push it through.

For now, the noise is enough to distract markets. But the interventions, “they’re all around us.”

When your spirit’s black and blue

And your heroes all desert you

Will you curse what’s coming true?

And the hate won’t count you out

It’ll leave you in the shadowsThey’re all around us

Poppy - They’re All Around Us

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.

Good read bud.