The Worst

Why the oil shock may push inflation higher - before monetary policy decides the outcome

I know the sentence has been a little overused lately, but once again, financial markets find themselves in “unprecedented times.” With the war against Iran now exceeding last year’s 12-day war, there is still no end in sight. The “quick victory” seems far away, although one can debate the definition of “quick” in that regard.

However, the market finally seems to be waking up to that fact. As I leave the military analysis to the experts, what matters for markets at the moment is simple: the war continues, and the Strait of Hormuz remains more or less closed, regardless of who is in charge of it. As a result, the world is exposed to a major chokepoint of the global oil supply.

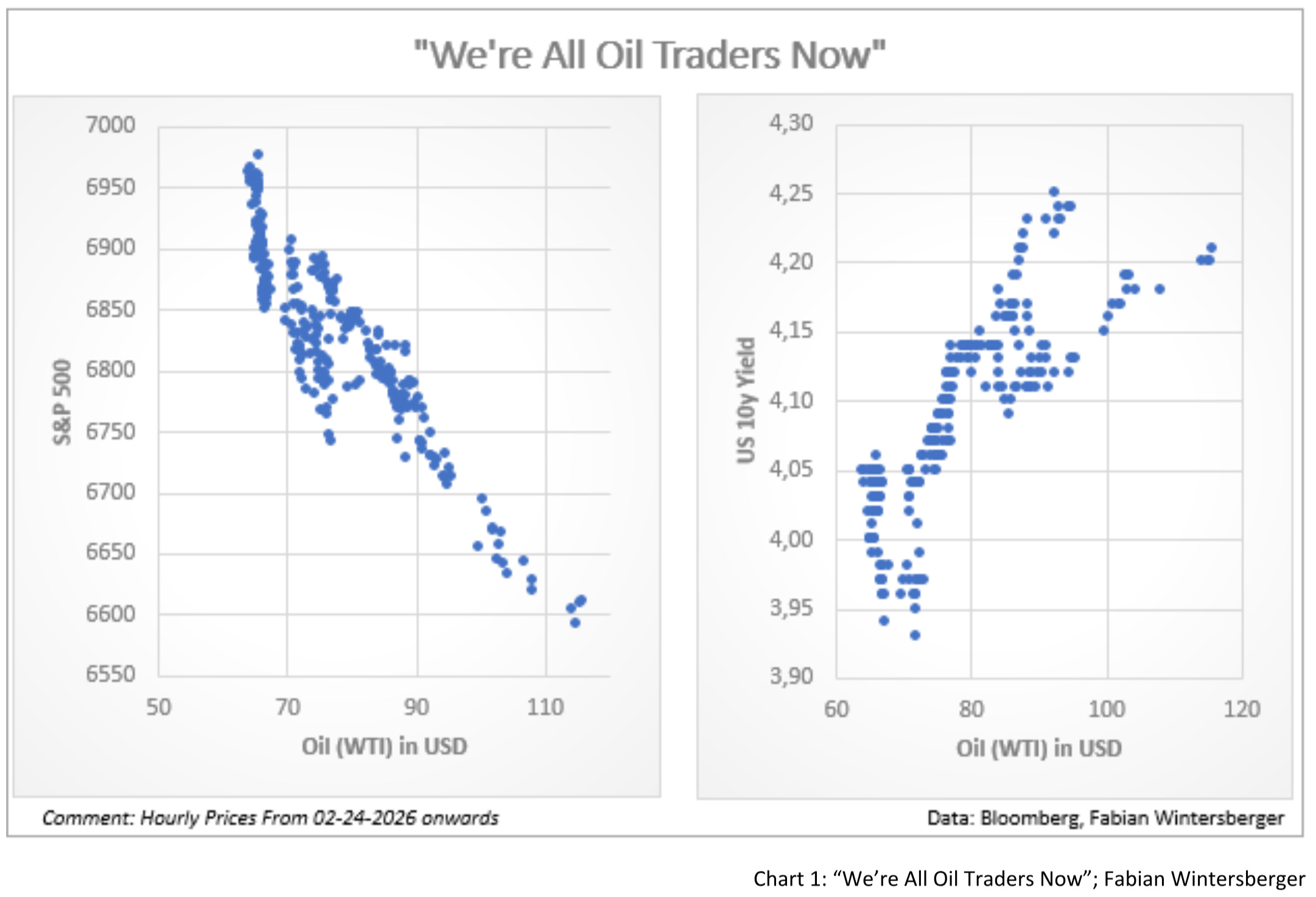

“We’re All Oil Traders Now”

The dominant price action with implications for every other financial asset is oil. The correlation of oil to stocks and stocks to bonds is now almost perfectly inverse. If oil goes up, bonds and stocks go down — and vice versa.

Monday in particular was wild and volatile. From the Sunday open, oil spiked to almost $120 before crashing back to around $85. The initial move higher reflected the realization that the Strait of Hormuz had indeed closed and that Iran was attacking ships attempting to pass through the strait.

The move into the European open was extreme, but things then calmed somewhat, with a modest countermove during the day — until Donald Trump entered the stage. He declared de facto victory, saying the war would be over within a week, the Strait of Hormuz would reopen, and the US would guarantee safe passage. That was enough. Just as with his tariff statements in the past, markets reacted immediately to his remarks.

The next day, the price hovered around the $85–90 range before dropping sharply after Energy Secretary Chris Wright posted on X that the US Navy had successfully escorted an oil tanker through the strait. Oil (WTI) prices quickly fell to $80 as a result.

Yet there was a problem: the statement later proved incorrect, and Wright deleted it shortly afterwards. Whether it was a lie or simple incompetence no longer matters much. What matters is that credibility appears to have been damaged significantly. On Wednesday, Trump repeated almost the same message as on Monday — and the market barely reacted. Despite the statement and the IEA’s decision to release a record 400 million barrels onto the market, oil prices moved higher. As of writing, they are back above $90.

And the reason is simple: as the Iranians say, the Strait of Hormuz remains closed to “enemies.” The oil is not flowing — and it hasn’t for 12 days.

That brings us to the bigger question: what happens if the disruption lasts longer than markets currently expect?

In a recent episode of Bloomberg’s Odd Lots podcast, oil analyst Rory Johnston discussed what a prolonged disruption in the Strait of Hormuz could mean for energy markets. His argument is that the real problem would not simply be a temporary loss of supply, but the breakdown of the physical logistics that keep the global oil system running. Roughly a fifth of the world’s oil moves through that narrow waterway. If the flow stops or becomes unreliable, tanker routes, insurance coverage, refinery supply chains, and inventories all begin to unravel.

In such a scenario, the first stress would likely appear not in crude itself but in refined products such as diesel, gasoline, and jet fuel, which tend to have tighter markets and fewer buffers. Prices would then become the rationing mechanism. That is why Johnston argues that oil could theoretically spike toward $200 a barrel in a prolonged disruption—not as a prediction, but as the kind of price level historically required to destroy enough demand when the system suddenly loses a major supply artery.

With no clear path to an end that would satisfy all three participants in the war, I doubt the market has fully grasped what could happen then. It feels reminiscent of February 2020, when markets strongly downplayed the economic disruptions from Covid.

Rising Oil Prices & Inflation: An Uncertain Path Ahead

While the US CPI numbers released on Wednesday were probably among the least important in a long time, given everything that has started to unfold in March, the question remains whether the disruption in the oil market and the rise in oil prices will affect consumer price inflation. This may sound somewhat theoretical, but it matters for the coming market developments — and helps explain why ECB hawks, for example, are already talking about a potential rate hike in the near future because of the war.

Central banks operate within a New-Keynesian framework, which is essentially a symbiosis of neoclassical microeconomics and Keynesian ideas. In that framework, macroeconomic dynamics are largely modeled by feeding macro data into micro-econometric structures and aggregating the results into what is then called “macroeconomics.”

Within that framework, economists distinguish between “demand-pull” and “cost-push” inflation, arguing that rising consumer prices either stem from demand outstripping supply or from rising costs on the supply side. Monetary factors tend to play only a limited role in these models, as policy is typically modeled through the interest rate rather than through changes in the quantity or value of money itself. Hence, central banks fight inflation by increasing interest rates — the price of credit — rather than by directly restricting the supply of money.

Within this framework, the cure for inflation is simple: to drive down prices, interest rates must rise.

As oil prices affect almost all products supplied to the market, the assumption is that this “cost-push” inflation spreads widely through the economy. The market knows this, and interest rate expectations therefore adjust to higher inflation — at least according to mainstream models.

This assumption is widely criticized by monetarists, such as Steve Hanke. Within the monetarist framework, where the price level results from the relationship between the quantity of money, the demand for money, and how fast it circulates through the economy, a rise in oil prices alone cannot lead to inflation. As one factor of production becomes more expensive, relative prices for other goods, services, and factors of production must adjust. Oil prices may rise, but other prices will fall, meaning the overall price level does not necessarily increase.

Although that’s a logical argument — and one can roughly agree with it — it is also a mechanical one that misses another important point: human actions and perceptions about the future. If businesses and households begin to expect higher prices, their behavior changes — from wage negotiations to inventory decisions.

Both theories therefore miss an important point: transition phases. The New-Keynesian assumption that money is not dominant can hold in the short term, when businesses and households form expectations and prices change in response to them. These expectations are guesses that can be over- or understated, but over time they tend to move toward a price equilibrium consistent with monetary conditions.

My analysis therefore suggests that in the short term consumer price inflation could rise higher than expected. In the Eurozone that could mean the ECB raises rates again, while in the US it could mean that rate-cut hopes diminish. In this phase, expectation shifts often create strong but uncertain reactions that lead to disequilibria and higher price volatility.

In the medium and longer term, central bank actions become decisive and determine whether the rise in consumer prices evolves into another inflationary wave. Much of that will depend on how output evolves.

Within this uncertainty, and with falling supply, steady interest rates can effectively turn into financial and monetary tightening, forcing central banks to react. When financial stress appears, central banks will open the gates again and swap money for bonds, increasing the quantity of money in the economy. At that point, the perception of higher prices — which initially was not based on monetary factors — can become reinforced by monetary expansion.

While it remains to be seen how this evolves, current events and the appointment of Kevin Warsh have changed my assumptions regarding the path of inflation.

I think the Fed may concentrate on unemployment and treat inflation as secondary, overlooking that the break-even rate for job growth is close to zero. This could create a supportive monetary environment while the economic foundations are shaken by disruptions in the oil market.

The ECB may or may not raise interest rates, but it still makes the policy mistake of assuming that short-term inflation — driven by expectation-based disequilibria — must be stamped out with steady or higher rates. That risks an overreaction and eventually a policy reversal, following the Fed in lowering rates regardless of inflation.

While this is not set in stone, my expectation now is that inflation could begin rising again later this year if there is no major economic disruption. If growth stalls, consumer price inflation may dip temporarily — only to be followed by stronger monetary expansion that ultimately drives inflation higher.

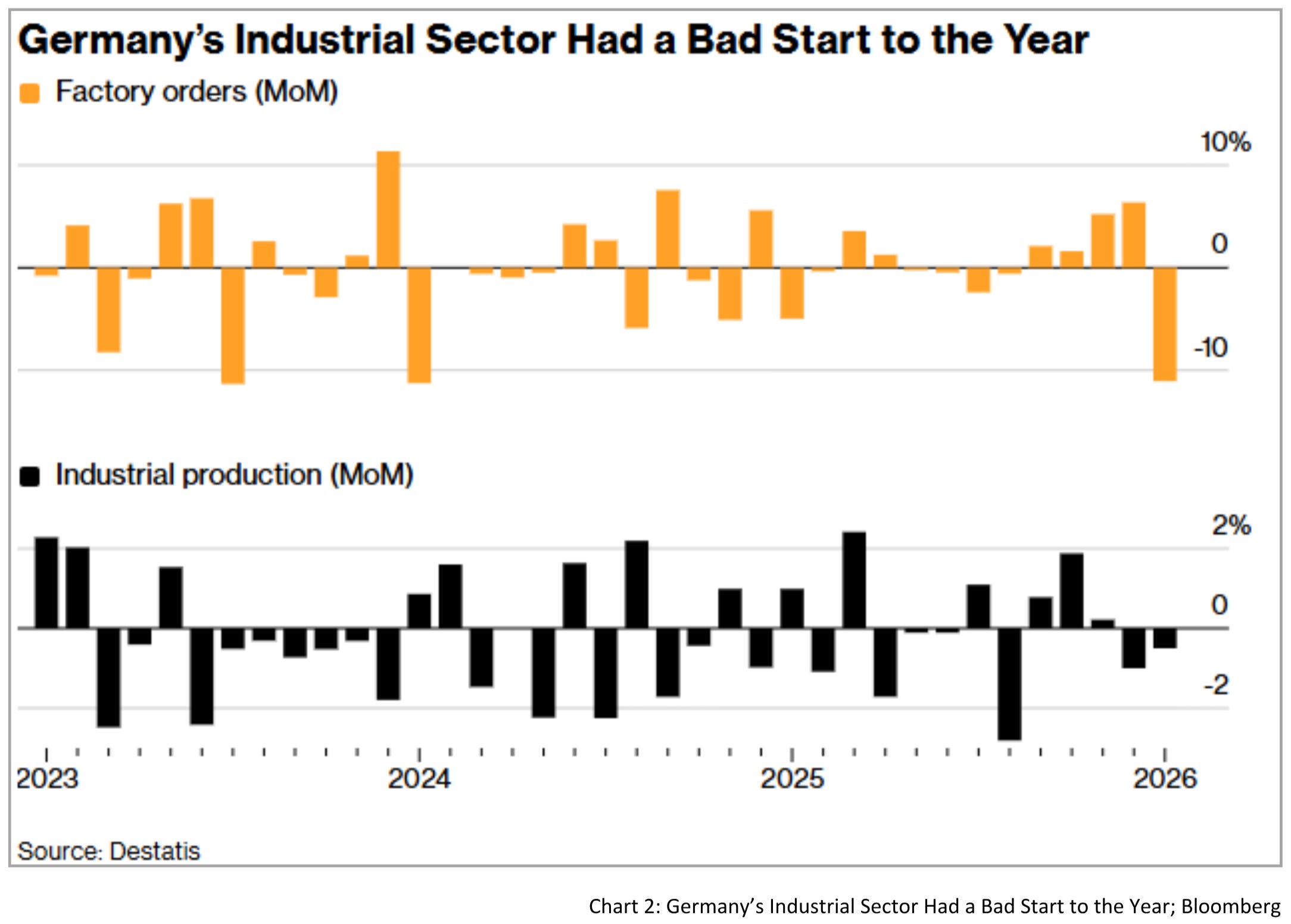

Is The German Recovery Dead Before It Started?

All these things are happening at probably the most unfavorable time for the German economy and hopes that the stimulus package will pave the way for a sustainable recovery. Factory orders in January dropped 11.1% compared to December 2025, causing a huge miss versus expectations of a 13.2% YoY increase, ending up at only 3.7%.

And these numbers were recorded before the latest oil shock, which now threatens to hit Europe’s energy-dependent economy at exactly the wrong moment. They also support the skepticism I previously expressed about the high expectations for German growth. We have to remember that this big miss happened before the war and the still-evolving energy shock. As a net energy importer, Europe is strongly dependent on energy imports, and the closure of the Strait of Hormuz hurts Europe significantly, especially in the LNG space. Since Europeans moved away from Russian natural gas, they have become more dependent on LNG imports from the Gulf and the US, leaving the US in a strong position when it comes to supplying Europe with natural gas.

Fuel prices are already rising in Germany, exposing consumers to short-term price increases. Financial conditions are worsening quickly, and therefore I expect growth to remain stagnant this year, while the government’s spending spree fuels further increases in consumer price inflation.

Now, let’s assess the further trajectory for markets.

Bonds & Interest Rates

Since the start of the war, interest rates have moved only one way. As mentioned before, everything seems to be connected with the move in oil prices right now. And as oil prices were dropping on Monday, bonds got bid higher, albeit the rise in bond prices wasn’t enormously strong and rather small. Whether that means the bond market sees a bigger problem remains to be seen.

Nevertheless, the price action doesn’t support that the rise in yields is coming to an end, especially with many potential problems in the oil market that are still evolving. I was neutral on bonds last week, but since then I have developed a negative view on bonds as long as the disruptions in the oil market continue and the war goes on.

Stocks

Despite all the things that happened, the stock market has shown strong resilience so far. However, the price action indicates that the bullish sentiment is getting smaller, despite the recent dip-buying that is still going on. I’m not at the phase to say that one should be outright bearish on stocks, but I would become much more cautious at the moment.

Equities are usually the last market where reality breaks through, which might be a reason why they have held up quite well. However, the situation of a prolonged war could become a problem for stocks in the near future. The S&P needs to defend the 6,700 area while the DAX looks even more vulnerable and could move towards 23,000.

FX, Gold & Bitcoin

My assessment regarding the dollar remains unchanged. As the market sliced through the 1.16 resistance in EUR/USD, I think that there’s more potential downside for the Euro, as the market wakes up to the fact that with the war, growth expectations in the Eurozone should go lower, not higher.

The dollar remains the safe haven within the FX space. Gold and Bitcoin, on the other hand, have remained extremely resilient since the war started, as they remain largely unchanged. My view on gold remains largely constructive, while Bitcoin still has to prove that the bottom is in, and I remain neutral for now

Conclusion

War always produces a lot of noise, but this one also creates many consequences. Markets remain under pressure as long as the Strait of Hormuz remains closed. It also touches areas such as private credit, where various funds recently experienced markdowns. While I cannot say whether this becomes a bigger problem, it’s definitely something to keep an eye on.

The clearest buy signal one can hope for is probably a reopening of the Strait of Hormuz and the end of the war. However, the closure of the Strait doesn’t only affect oil markets, but also helium, fertilizers, and therefore has the potential to develop into something much bigger. However, that’s not something to forecast but something to prepare for. Hope for the best, prepare for “the worst.”

Can I ever learn to live with the worst

Inside my mind?

Feels like nothing ever seems to work

It doesn’t matter how hard I try

To fight it, will I survive it,

And come out alive?Our Promise – The Worst

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.