The Stage

When Everyone Watches The Actors, Few Pay Attention To The Stage

All the world’s a stage, and all the men and women merely players. — William Shakespeare

“Nothing gets up in a straight line” is a widely known saying among investors, and this week was a reminder of that. Since last Wednesday, the S&P 500 lost 4.5%, the Dow Jones 3.2%, and the Nasdaq Composite more than 7%. European equities did only slightly better, with the DAX falling 4.7% and the Euro Stoxx 50 declining 2.1% from their recent highs.

As usual, the appearance of bears in financial media has risen alongside the decline in stock prices. Yet every correction over the past year has produced the same conclusion: fears of an imminent downturn continue to collide with an economy that remains far more resilient than expected.

For that reason, I believe three observations remain particularly important.

First, despite weaker sentiment surveys and a softening labor market, the US economy continues to display underlying strength. Aggregate income growth, tax receipts, and recent inflation data suggest that nominal demand remains considerably stronger than many investors assume.

Second, the ECB’s expected rate hike on Thursday (I am writing this note before the announcement) does not change the fact that it is fighting a fundamentally different battle than the Federal Reserve. While the US continues to wrestle with resilient nominal demand and sticky inflation, Europe’s challenges appear increasingly structural in nature.

Third, these diverging economic realities have important implications for financial markets. If the growth and inflation outlooks on both sides of the Atlantic continue to move apart, current expectations regarding future interest-rate paths may prove increasingly difficult to justify.

This week, I will discuss each of these themes in greater detail.

A Strong Economy That No One Feels?

While US Nonfarm Payrolls in May topped expectations and unemployment remained stable at 4.3%, much of the discussion shifted toward Wednesday’s CPI release. With inflation rising to 4.2% year-over-year, average real wage growth has once again turned negative. Many commentators see this as a sign of a weakening economy and a potential drag on consumer demand.

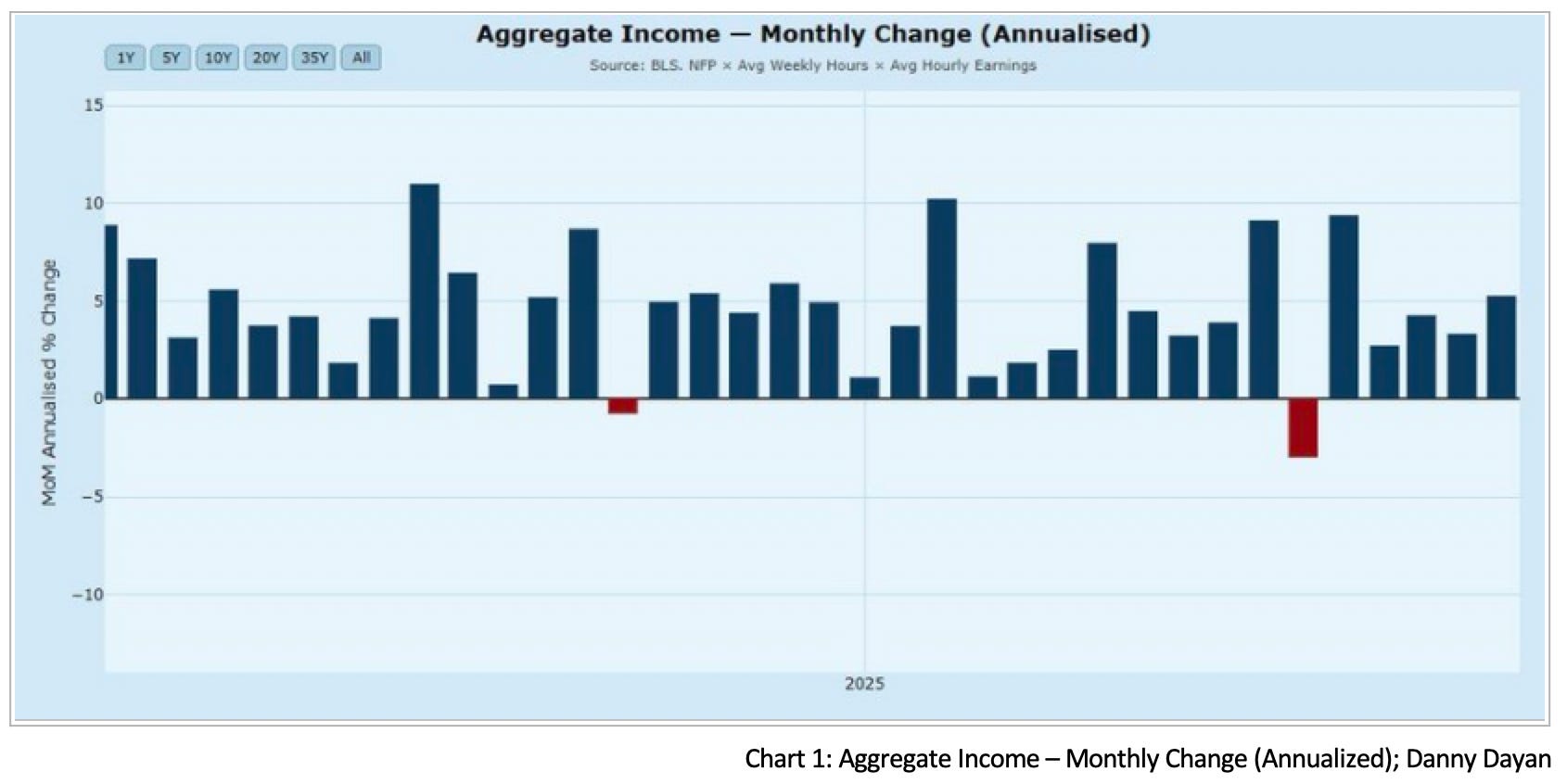

At first sight, it seems obvious. But I would caution against jumping to conclusions too quickly. First of all, wages alone don’t tell the whole story. Danny Dayan recently looked at aggregate income growth, where jobs, wages, and worked hours are combined into a broader measure of income. The result was a steady annualized increase of 5.1% — a figure that looks anything but recessionary.

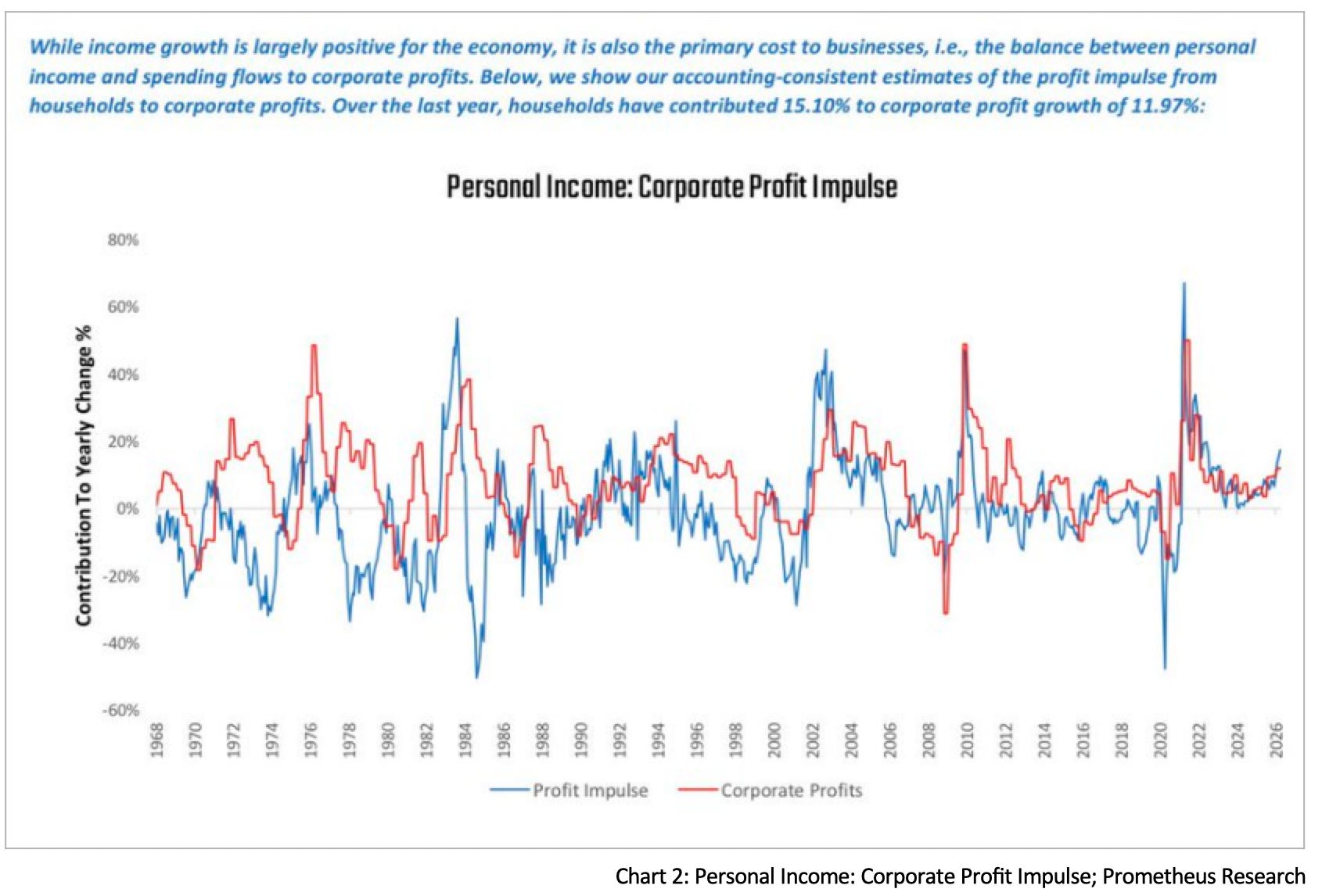

The point to make here is that the flows of income have changed. Despite the decline in real wage growth, it doesn’t mean that the money has disappeared from the economy. It simply means that the transmission mechanism has changed. If real wages are falling, then the share of corporate profits tends to rise, because labor costs are increasing more slowly than final prices.

Chart 2 shows consumption impulses from wages and profits, suggesting that this mechanism is indeed in place right now.

To sum it up, consumption can continue to rise despite falling real wages when corporate profits outpace GDP growth. One has to keep in mind that the economy knows no difference between producers and consumers. Each individual is a producer and a consumer at the same time, buying and selling goods and services in the marketplace.

Of course, this mechanism reaches its limits when businesses can no longer pass higher costs on to consumers. Yet recent inflation and retail sales data suggest otherwise. The latest Redbook Index accelerated from 9.0% to 9.1% year-over-year, adding another data point that supports the notion of a resilient economy. Business formations remain elevated while bankruptcies have declined this year.

Does that sound like an economy on the verge of recession? I’d argue that it clearly doesn’t.

There is, however, an important qualification to that conclusion. While many macro indicators point toward a resilient economy, the latest NFIB survey suggests that small businesses are not sharing equally in that strength. Growth expectations have weakened, hiring plans continue to deteriorate, and uncertainty remains elevated. Yet at the same time, pricing intentions have accelerated sharply.

This creates an interesting divergence. If the labor market were truly the dominant driver of inflation, one might expect weaker hiring demand to coincide with easing price pressures. Instead, firms appear increasingly willing to raise prices despite becoming more cautious about expanding payrolls.

The NFIB report raises an important question: why are firms becoming more willing to raise prices even as hiring plans deteriorate? The answer may tell us more about the strength of nominal demand than about the state of the labor market itself.

The lesson is that a weak/negative wage growth does not automatically imply weak demand. Income can reach consumers through different channels, and businesses appear increasingly confident that customers will absorb higher prices. For that reason, I remain skeptical of recession calls. The economy may not feel particularly strong, but the underlying data continue to suggest that it is stronger than many investors assume.

The weakness of wage growth as a source of consumption is increasingly being replaced by corporate profits and government spending, which more than make up for it.

The ECB Is Fighting A Different Fight

While the market seems to underestimate economic resilience in the US, Europe remains on a diverging path. The continent is considerably more vulnerable to the energy supply shock stemming from the war with Iran. So far, the full severity of that shock has been avoided through the release of strategic reserves and inventory drawdowns.

But the longer the disruption in the Middle East persists, the harder it becomes to keep the system afloat. Europe’s economy runs on diesel, and domestic production is insufficient to satisfy demand. Bloomberg recently reported that diesel and jet fuel arrivals have fallen for two consecutive months, tightening supply further.

Yet despite the larger exposure to the energy shock, inflation in the Euro Area remains roughly one percentage point below the US. While part of this is a matter of methodology, the weakness of domestic consumption suggests that the Eurozone is already experiencing a degree of demand destruction as a consequence of higher prices.

That is an important difference. In the US, inflation continues to coexist with resilient nominal demand. In Europe, inflation increasingly appears to coexist with weak demand.

In other words, the Fed and the ECB are fighting different battles.

The Federal Reserve is attempting to restrain an economy that continues to generate strong income growth and resilient spending. The ECB, by contrast, is raising rates in an environment where producers already struggle to pass higher costs on to consumers.

I have little doubt that the ECB will succeed in dampening demand further. The question is whether this cure ultimately proves more damaging than the disease itself. The German spending package has not generated a meaningful recovery but merely helped to keep the economy from slipping deeper into stagnation. Additional rate hikes will make borrowing more expensive for households and businesses alike, while doing little to address the underlying causes of Europe’s weakness.

That weakness is largely beyond the ECB’s control. Higher interest rates do not create additional energy supply. They do not reduce the regulatory burden on businesses. They do not reverse years of bureaucratic expansion or improve productivity growth.

The energy situation illustrates the problem. Due to the rise in oil prices, the European cap on Russian oil would automatically increase from $44.10 to roughly $65 per barrel, above the collectively agreed threshold of $60. Yet policymakers are discussing keeping the cap at the current level instead.

If the primary objective is to weaken the Russian economy, that policy may be justified. The question is whether the European economy can sustain the resulting reduction in supply for much longer. Europe’s growing dependence on Middle Eastern imports is itself the consequence of abandoning Russia as a supplier. The current supply shock has simply exposed another vulnerability in the system.

The bottom line is that the ECB is fighting a supply problem, while the Federal Reserve is facing a combination of strong underlying consumer demand and rising prices. The difference matters because higher interest rates can suppress demand, but they cannot create additional energy supply. As a result, Europe risks paying the economic cost of tighter monetary policy without addressing the root cause of the problem.

Forget the 2008-Crisis-Framework

The divergence between the United States and Europe highlights a broader problem. Investors often focus on the most visible risks while neglecting the mechanisms operating beneath the surface.

Regarding the US, investors focus on falling real wages and sentiment data while ignoring the resilience of nominal demand, arguing that the economy is on the verge of a collapse because households get squeezed. For Europe, the discussion remains centered on inflation while the politically induced supply constraints are either hardly discussed or pushed further into the future to address.

But problems mostly emerge beneath the surface, not out of the obvious. Human action adapts, systems evolve, and past problems are apparently solved while the solutions merely enable the emergence of a blind spot somewhere else. A new BIS working paper suggests that such a blind spot may exist within financial markets themselves.

If we think of financial crises, everyone thinks about bank failures, mortgage losses, and the freezing of interbank lending. After 2008, regulators worked hard to address the problems that led to the Global Financial Crisis and to avoid a similar event in the future by strengthening the banking system.

But as regulations appear, systems evolve and markets adapt. When banks become more heavily regulated and lending becomes more complicated, someone inevitably finds a blind spot and steps up to supply the loans that banks no longer provide to marginal borrowers. Over the years, it has been widely reported that lending growth has increasingly shifted toward Non-Depository Financial Institutions (NDFIs), often referred to as “shadow banks” because they do not collect public deposits.

Examples include pension funds, hedge funds, mortgage companies, ABS issuers, and money market funds. One consequence of post-2008 regulation was the continued migration of lending activity toward these institutions, which increasingly perform functions that were traditionally dominated by commercial banks.

The BIS paper examines more than 3,500 US money market funds and arrives at an interesting conclusion. Periods of rapidly rising asset prices tend to encourage behavior that makes the financial system more fragile. As collateral values increase, leverage expands and market participants become increasingly dependent on the continued availability of high-quality collateral, such as Treasury bills and US Treasuries.

Put differently, the source of instability shifts away from the banking sector.

It’s no longer primarily about whether banks make bad loans. Instead, it is about institutions whose business models depend on elevated asset prices and on collateral continuing to circulate smoothly throughout the financial system.

Modern financial markets increasingly operate through layers of collateral claims. It is not merely the asset itself that provides liquidity, but the ability to create additional claims on top of it. During boom periods, rising asset prices support more leverage and more collateral creation. During downturns, the process works in reverse as market participants scramble for the highest-quality collateral while lower-quality collateral loses value.

However, the conclusion here is not that another crisis is imminent. The BIS paper is a reminder that financial fragility accumulates during periods of optimism rather than periods of stress. The strongest economies and the strongest markets frequently create the conditions for their own vulnerabilities.

My point here is not that investors should prepare for a repeat of the Global Financial Crisis. Rather, they should spend less time looking for the last crisis and more time understanding how the financial system has evolved since then. The next period of instability is unlikely to emerge from the exact same place as 2008. Instead, investors should pay close attention to where leverage, collateral, and liquidity risks are quietly building beneath the surface.

Market Assessment

Despite the latest correction in the stock market, my market outlook remains broadly unchanged. Economic data continues to suggest a stronger US economy than most assume. Europe, on the other hand, continues to struggle with the supply-side challenges discussed earlier. I think that US assets likely continue to outperform European ones. Given those developments, the dollar looks poised for more upside versus the euro.

Bonds failed to make a move higher and remain under pressure, and therefore seem to be a worse hedge than oil, although oil has become less sensitive to recent news of a worsening situation in the Middle East.

Gold and Bitcoin continue to sell off. Regardless of the potential reasons, the price action suggests that there’s potentially more downside.

Conclusion

If there’s a recurring lesson in financial markets, it’s that it is rarely the widely discussed things that matter most.

Investors worry about falling real wages in the US. The ECB worries about rising inflation in the Eurozone while policymakers pay relatively little attention to the supply constraints that many of their own policies have helped create. In financial markets, we continue to focus on the sectors that created problems in the past while paying less attention to the places where leverage and liquidity risks have migrated as a result of regulatory changes.

But surface-level observations rarely tell the whole story. Economics is not physics, where experiments can be reproduced over and over again. People adapt, systems evolve, and incentives change over time. It is not that the consensus is always wrong. Quite the opposite. My point is simply that opportunities and risks are often found outside the narratives that dominate the headlines.

We also tend to spend far more time discussing the negatives than the positives. Perhaps that is because pessimism often sounds more sophisticated than optimism. Yet successful investing is rarely about anticipating disaster around every corner. It is about recognizing risks while also understanding the forces that continue to move the system forward.

For now, I do not believe that markets have reached a top. Positioning remains supportive, the US economy continues to display underlying resilience, and the AI investment boom still appears to have considerable momentum behind it. However, one question increasingly captures my attention: not whether the AI revolution is real, but whether there is enough capital available to fund everybody who wants to participate in it.

History suggests that financial fragility often emerges during periods of optimism rather than pessimism.

Markets are rarely constrained by imagination. More often, they are constrained by resources.

Resources set the stage.

Who is the crowd that peers through the cage

As we perform here upon the stage?

Tell me a lie in a beautiful way

I believe in answers just not todayAvenged Sevenfold- The Stage

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.

The biggest risk America faces is government default given the wide and widening government deficit, the dollar is holding on by a thin thread.