The Sound of Truth

Economics is haunted by more fallacies than any other study known to man. This is no accident. The inherent difficulties of the subject would be great enough in any case, but they are multiplied a thousandfold by a factor that is insignificant in, say, physics, mathematics or medicine - the special pleading of selfish interests.

- Henry Hazlitt: Economics In One Lesson

It has been about 80 years since US-journalists Henry Hazlitt wrote his primer on economics, exposing 24 common economic fallacies.

Based on the essay What Is Seen And What Is Not Seen by French economist Frederic Bastiat, Hazlitt wonderfully shows that most economic policies do not look at the long-term effects of these policies on the whole economy.

What Is Seen And What Is Not Seen is about a Handyman who discovers one day that his son has destroyed one of his shop windows. As a result, he has to go to the glazier to buy a new window, which means that the glazier receives additional income. However, the first impression that the destruction of the window benefits the whole economy is shortsighted.

As Bastiat shows, the glazier’s income is what is seen. Yet, what is not seen is that the handyman could have used the money he spent on repairing the window for something else. But, instead of a window and an additional good, he must give up the additional good.

Still, over the last 80 years, the discussions on economic policies have hardly changed, as the latest discussions about price breaks and price caps on energy and housing so nicely show. However, there are not only discussions about economic policy. In recent weeks, various arguments have been made about economics within financial markets, and this week I want to discuss some of them to see if they are true.

Before I discuss three economic claims, I want to discuss two actual topics of this week. Let me start with the latest numbers on consumer price inflation in the United States and Germany this week (Currently, I plan to discuss them in more detail next week).

Year-over-Year, US consumer prices rose 5 %, while the consensus expected an increase of 5.1 %. In Germany, EU Harmonized CPI rose, as estimated at the end of March, by 7.8 % year-over-year.

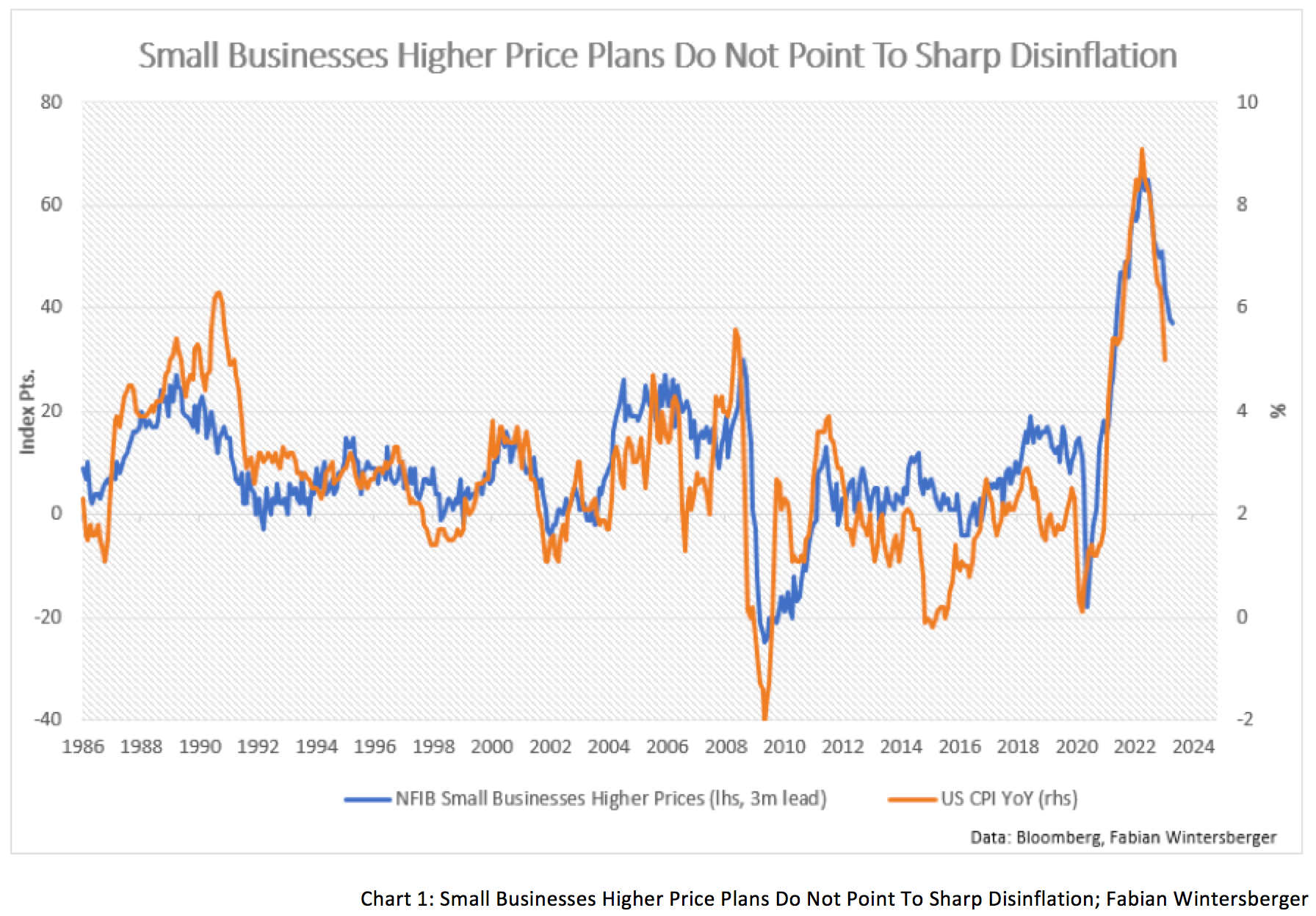

Now, let us look into the latest NFIB Small Business Economic Trends report from March. As long as small and medium businesses are the so-called backbone of Western economies, the sentiment of those businesses gives an overview of the overall state of the economy.

The report shows that sentiment among small businesses is terrible; Small Business Optimism Index is below its 49-year average for the 15th time in a row. However, it is also true that sentiment has been similarly bad during the first few years of the 2010s. Although businesses can fill open jobs a bit easier, job openings hard to fill are still historically high.

It is most difficult for them to fill jobs for skilled workers, most in construction, transportation, and wholesale branches. The lowest openings are in the financial sector. More than a quarter of the surveyed businesses said there are few applicants for skilled workers, and another quarter said they get no applicants.

Capital expenditures stayed within their historical average, although only 26 % plan capital expenditures in the next month, which is historically very weak. A small majority in the survey stated that they neither had higher nominal nor higher real sales during the latest months. About one-fifth noted that supply chain disruptions are still significantly influencing their business.

All this underlines that the sentiment among small and medium enterprises in the United States is weak, although the NFIB notes that the widely anticipated recession has not materialized. Further, the report states that optimism has been at recession levels for a year. But unexpectedly strong consumer spending has kept Main Street alive and supported strong labor demand.

Inflation is still the most critical problem for SMEs, although the number of businesses that plan price increases fell to the lowest since April 2021. Most price increases were made in wholesale, retail, construction, and finance. However, seasonally adjusted, the number of companies raising prices increased.

The NFIB Small Businesses Higher Prices Index has always been a good indicator of the future path of consumer price inflation. However, it does not support the sharp disinflation that so many analysts forecast.

This brings me to the first economic thesis I want to discuss this week, to find the Sound of Truth. Lately, I stumbled upon the argument that US Manufacturing prices are paid to deliver conclusions about the future path of consumer price inflation. One has to acknowledge that there has been some correlation after the GFC in 2008, although it has been weak. If one assumes the correlation to be valid, it points to massive disinflation in the coming months.

At first, there is the obvious question of whether prices for inputs determine prices for outputs, consumer goods. The idea traces back to classical economists like Adam Smith, David Ricardo, and Karl Marx, who assumed that the price of a good is determined by the work put in to build the product, the so-called labor theory of value.

However, as Eugen von Boehm-Bawerk showed, prices are not determined by costs but by supply and demand. While it is true that costs influence the supply offered on the market because suppliers who have costs above the price they can achieve by selling on the market will have to exit the market over time.

Let us assume that prices for input goods fall but demand remains high because the price drop can be traced back to innovation in the production process. At first, the innovation will lead to higher profit margins for businesses, and only over time prices start to drop because companies have the incentive to lower prices to gain market share.

Yet, manufacturing prices rose because of supply-chain problems (=lower supply) and because businesses either decided to build up additional storage capacity or increase existing storage. Now that storages are full, demand for inputs decreases, and if storage starts to fall, manufacturers will demand more goods, and hence prices will rise again. This leads to the conclusion that the connection between manufacturing prices paid and consumer prices are relatively weak.

Additionally, monetary expansion created additional demand via transfer payments to consumers, and the money flew from consumers to manufacturers and suppliers of manufacturers. In addition to artificially increased demand, supply chain problems helped drive prices up, but those problems have improved. This led to rising profit margins, which are now passed back to workers via higher wages, as they want to be compensated for the price increases.

However, at some point, businesses cannot increase wages, and as a result, consumer demand falls. If demand goes down, prices fall, and so does the demand for input goods. Therefore one could assume that the relationship is the other way around and that falling consumer demand leads to falling manufacturing prices paid. However, if one zooms out, one sees that the correlation between consumer price inflation and manufacturing prices paid is a lot weaker than one might expect.

In March, while Silicone Valley Bank went bankrupt and First Republic Bank got rescued, a discussion emerged about fractional reserve banking. The reason is that these banks faced a lack of liquidity to pay out the clients who wanted to withdraw their money from their deposits.

A debate started, where some argued that fractional reserve banking already violates property rights because under if the saver and the borrower have claim rights to the same money simultaneously. However, I want to leave that aside here.

Much more interesting is the economic argument for fractional reserve banking, brought up by political scientist and Epsilon-Theory founder Ben Hunt. On Twitter, he wrote:

Fractional reserve banking is THE engine of entrepreneurialism and productive societal risk-taking. It is directly responsible for the standard of living, technology and medical care you enjoy to day…without the fractional reserve banking system, credit would only be available to the already rich. Mortgages, auto loans, credit cards, student loans, start-up loans... all of these would no longer be available if you moved to a fixed reserve banking system.

See, I think Ben Hunt is very smart, and I greatly respect him. His texts on Epsilon Theory are always entertaining and educational. Yet, his take on fractional reserve banking is a terrible misconception. Fractional reserve banking does not drive economic wealth.

Let us first look at the difference between a 100 % reserve system. In a fractional reserve system, the bank does not have to wait until a loan is repaid before handing out another loan. The bank can loan out so much money until the reserve limit is reached it can hand out many more loans than under a 100 % reserve regime.

An additional supply of loans and competition among banks leads to lower interest rates. The result is that many projects are realized at those lower rates, which otherwise would not have been realized because they seem profitable now. So, one might say this shows that fractional reserve banking boosts wealth.

However, this is a misconception. Credit creation in a fractional reserve system solely means that banks create additional units of money. It does not create additional resources, additional land, no additional factors of production. It only transfers purchasing power from savers to debtors, who can buy goods and services at old prices.

Further, production cannot be expanded as much as the supply of credit, and at one point, credit supply becomes scarce, at the latest, when the reserve limit is reached. A tighter credit supply leads to higher interest rates, fewer projects are financed, and some projects already in the making must be liquidated because they are unprofitable at higher interest rates.

The argument that no bank would lend to the average person without fractional reserve banking is not verifiable. Since banking exists, bankers check creditworthiness and assess the debtor’s ability to repay the loan by looking at his financial history.

Moreover, the fact that the industrial revolution coincides with the spread of fractional reserve banking is, in my opinion, only a spurious correlation, not causation.

Yet, what fractional reserve banking has accomplished is that it rewards additional risk-taking and thus creates rising systemic instability. Therefore, fractional reserve banking and the central bank as the lender of last resort are just two sides of a coin - both depend on each other. Contrary to Ben Hunt's claim, fractional reserve banking definitely is not the primary driver of entrepreneurship and wealth.

However, I want to note at this point that I am not against fractional reserve banking as long as it takes place within a free-market order where risk is borne by those who take it. In such a system, there is a higher incentive to keep a higher reserve anyway because banks do not want to risk bankruptcy.

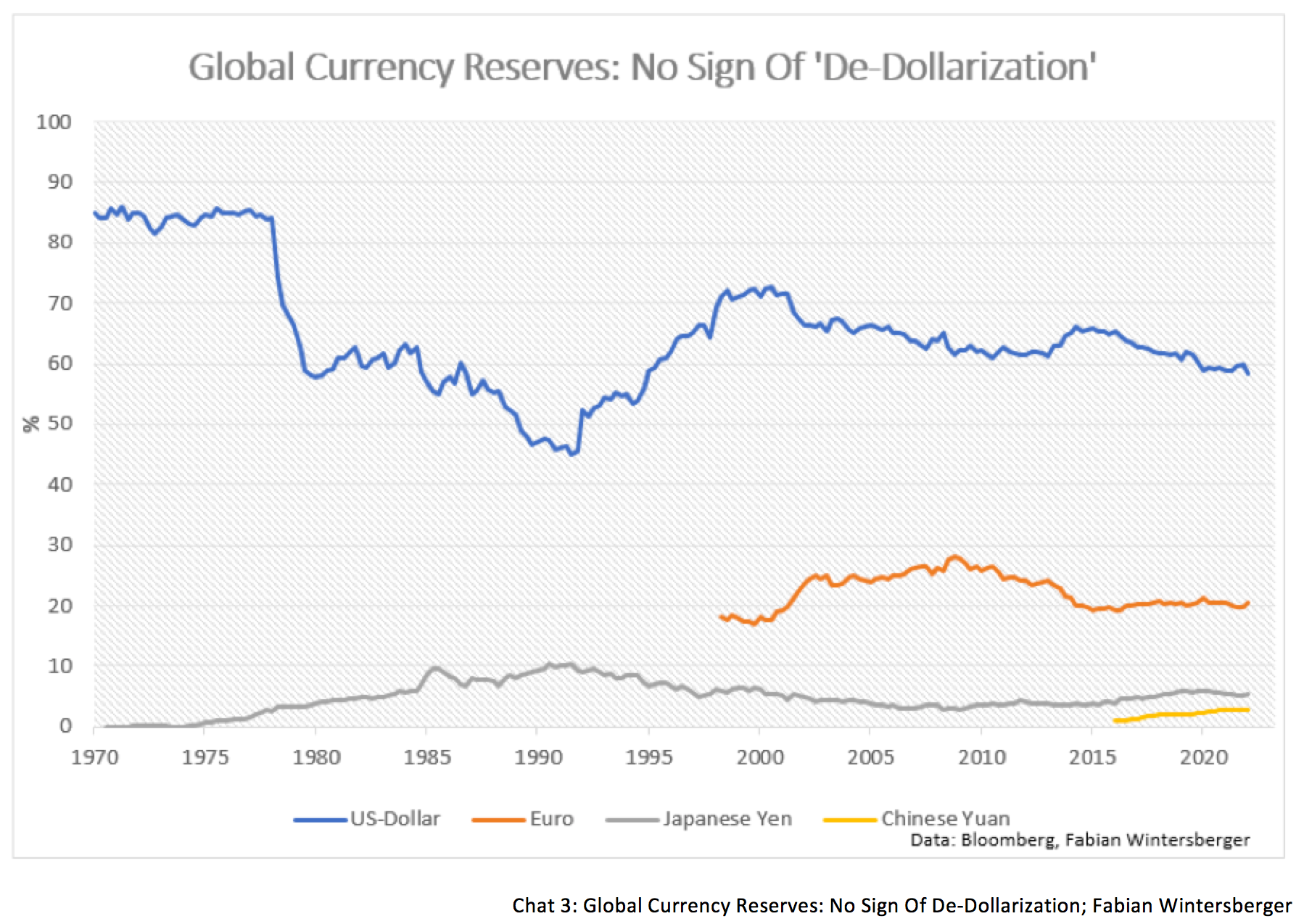

This brings me to the last topic currently debated among financial market participants: the demise of the dollar and its end as the world’s reserve currency. Fueled by the news, oil suppliers like Saudi Arabia and Iraq plan to facture future oil deliveries to China in the Chinese Yuan.

It is not the first time financial bloggers, commentators, and analysts have written about the end of the dollar as the leading reserve currency. When Russia faced Western sanctions because of the annexation of Crimea, it started to reduce its dollar reserves, and China began to create a Petro-Yuan in 2018.

Still, the topic remained relatively unnoticed. However, all that changed last year when Russia invaded Ukraine, and the Western world started to freeze Russian FX reserves to bring Russia to its knees.

Without a doubt, this signaled to other countries in Africa, Asia, and South America that the United States and Europe will not hesitate to freeze their FX reserves if they were considered a bad actor. These actions have undoubtedly forced those countries to think more about potential alternatives.

Will China’s actions cause an end to the petrodollar and undermine the US financial system and, therefore, the US economy? Will this result in a sharp dollar devaluation?

One should remember that the dollar's supremacy is not primarily caused by the fact that it is used to buy oil but because the dollar has become the center of the global financial order via the eurodollar system. Every global business relies on US dollars, as it has become the standard currency for international trade.

As we all know, old habits are hard to break, especially for currencies used in international trade. It is estimated that 65 trillion of hidden dollar debt is circulating globally, fueled by the age of easy money, which central banks implemented after the GFC in 2008.

To end the dollar systems, companies would need to pay down and reduce their dollar debt. The possibility of defaulting on the dollar debt is impossible because the companies rely on international capital.

Thus, the talks and posts about imminent de-dollarization are just nonsense. A look at global currency reserves shows that the latest decline in dollar reserves is minimal. The dollar’s share in international currency reserves is about as high as during the second half of the 1990s. No other currency, neither the Japanese Yen, the euro, nor the Chinese Yuan, has the potential to replace the dollar.

So, what about a shift from currency reserves to commodity reserves? Although I suspect that the importance of tangible assets will increase, I do not think that they have the potential to replace the dollar. One problem is that commodities must be delivered from one country to another when they trade—obviously, an enormous effort.

There is no difference between us and them,

if we all blindly seek truth from sentiments,

We have all heard, what we wanted to hear,

Truth that sounds right to our earsAs I Lay Dying - The Sound of Truth

There is probably no other science with so many different opinions about specific topics than economics. However, ultimately, we are all looking for The Sound of Truth.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! If you like my writing, you can subscribe and get every post directly into your inbox. Also, sharing it on social media or liking the position would be fantastic!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice)

We don't really have fractional reserve banking. We have credit creation banking where banks create deposits when making loans. The result? It's not the lender (= the ultimate holder of the deposit created) who makes the decision to lend. It's the bank.

What does it matter? Banks can create purchasing power much more elastically than would happen if you wait for the wealthy to lend.

Is that good or bad? It depends what the new credit is created for. If it's for productive business investment it's great - non inflationary growth. If it's for consumption or asset purchases it's bad as it causes consumer or asset inflation.

Once you have given up an anchor such as gold credit growth needs to be managed some other way. Central banks have decided to target consumer inflation, completely ignoring asset inflation. Effectively money held by investors is not counted by the fed. You can predict what will happen: banks will reorient towards lending for asset purchases, asset prices and debt will soar. Inequality will skyrocket etc.

So fundamentally the money creation process in the banking sector when combined with the 2% consumer inflation target virtually guarantees an asset/debt supernova which will ultimately destroy the currency. And the worst is - nobody seems to care.

It might be that they've hit the end of the road now though as asset inflation turns into consumer inflation when retiring asset holders and wage earners bid for the goods and services provided by a shrinking working population. That's when it will become clear that asset inflation is not wealth. You can't divide asset prices by consumer inflation to get real wealth - got to divide by asset inflation which has been running at ~8% per year.

regarding fractional reserve banking, as in most things, i suspect that it has helped the process of economic growth, but is certainly not the driving force, or perhaps it has helped accelerate the process. as to the dollar's reserve status, i agree completely and appreciate everybody who pushes bak against this narrative.