The Pretender

Facts per se can neither prove nor refute anything. Everything is decided by the interpretation and explanation of the facts, by the ideas and the theories.– Ludwig von Mises

Narrative, the art of storytelling, forms a fundamental pillar in human communication and understanding. Through narrative, we make sense of the world around us, giving meaning to our experiences and shaping our perspectives. In economics, narratives also play a crucial role in shaping the perceptions and behaviors of individuals, businesses, and policymakers. Beyond mere numbers and equations, narratives provide context and meaning to economic phenomena, influencing decision-making processes and market dynamics.

Primarily, analysts and economists use data to underpin the narratives they wish to convey, emphasizing their views of the market. Others, however, claim to be solely data-dependent, and this isn't limited to central banks in their policymaking. These individuals search for correlations, reliable patterns observable throughout history.

Yet, despite the belief of many that analyzing the market solely through vast amounts of data is a scientific approach, they overlook a crucial point. The assumption that economics can be studied akin to the natural sciences disregards the fact that economics deals not with atoms or molecules but with human beings.

Humans can change their perspectives, preferences, and goals, unlike atoms or molecules. Despite modern economists thinking that formulating positive theories or hypotheses capable of predicting human phenomena is the scientific approach (see Friedman, 1966), they miss an essential aspect.

Nonetheless, it must be acknowledged that even for those who believe this is the correct approach to economics, the track record of these models in forecasting the economy during certain events, often referred to as "economic shocks," has been less than stellar. These shocks can completely invalidate the assumptions underlying such models.

Hence, examining data devoid of a proper deductive theory lacks significance. In the preface of "Theory and History," Murray Rothbard elucidates how the Austrian economist Ludwig von Mises delineated the distinctions between these two methodologies:

The “objective” or “truly scientific” behaviorist, he pointed out, would observe the empirical events: e.g., people rushing back and forth, aimlessly at certain predictable times of day. And that is all he would know. But the true student of human action would start from the fact that all human behavior is purposive, and he would see the purpose is to get from home to the train to work in the morning, the opposite at night, etc. It is obvious which one would discover and know more about human behavior, and therefore which one would be the genuine “scientist”.

Hence, while one might utilize specific data points to bolster a narrative and make a case, without a robust theory that logically and deductively explains the data, it essentially lacks meaning. Moreover, it's imperative not only to scrutinize the data itself but also to delve into its implications.

I'm reiterating this point because of the recent release of the Nonfarm Payroll report, which once again underscores the importance of economic theory, a facet often overlooked nowadays. Instead of employing a solid theoretical framework to interpret the data, narratives have proliferated.

Before delving deeper, let's examine the headline numbers. To be frank, they were exceptional, and that alone was sufficient for market participants to presume that the signals were clear: a sustained upward trajectory.

In January, the US economy saw a notable uptick in job creation, adding 353,000 jobs, surpassing the anticipated 185,000. Private payrolls surged by 317,000, well above the projected 170,000, while manufacturing payrolls also exceeded expectations, rising by 23,000 instead of the forecasted 3,000. The unemployment rate remained steady at 3.7%, while average hourly earnings experienced a yearly increase of 4.5%. On a monthly basis, average hourly earnings rose by 0.6%, contributing to the annual 4.5% increase.

In response to the NFP report, yields and the S&P 500 spiked, while commodities like gold and oil (WTI) sold off. This reaction indicates that market participants were taken aback by the overall robustness, suggesting that the US economy appears unstoppable with no sign of a recession in sight. On the currency front, the dollar strengthened as market participants adjusted their expectations, ruling out the possibility of the Federal Reserve cutting interest rates in the near future.

Furthermore, the December figures were revised upwards. According to the BLS, the US economy added 333,000 jobs in December, up from the previously estimated 216,000. Contrary to analyst expectations, the unemployment rate did not increase by 0.1 percentage point. Additionally, wage growth in December was revised up by 0.2 percentage points to 4.3%.

Collectively, these indicators suggest little reason to believe the US economy is on the brink of recession. However, it's worth noting that the labor market, while strong, typically lags behind other economic indicators when it comes to signaling a downturn.

Despite the positive overall picture, some aspects of the report have drawn attention. While the total number of payrolls has surged compared to a year ago, the increase has been predominantly in part-time jobs, with the number of full-time jobs lower than a year ago. However, examining the total figures alone might be misleading, as the proportion of part-time jobs is lower than in 2019.

While it's possible that the share of part-time workers may increase in the future, it's too early to conclude that this signals a rapid cooling of the job market. This trend aligns with economic theory, as during economic slowdowns, businesses often lay off full-time workers and refrain from replacing them, leading to an increase in part-time employment, even if workers prefer full-time roles. Thus far, the rise in part-time jobs doesn't suggest a weakening labor market but rather indicates continued strength.

Nonetheless, it's challenging to discern any weakening trends when examining the changes in Nonfarm Payrolls by sector. The only sector that saw a decrease in payrolls (seasonally adjusted) is mining and logging. In all other sectors, job numbers increased, with some exceeding the prior 12-month average, notably in government, leisure and hospitality, and other services.

The most significant increases in January occurred in private education and health services, professional and business services, retail trade, and government. While the growth in professional and business services and retail trade supports the argument for ongoing economic expansion, the rise in government and private education and health services highlights an intriguing aspect of Nonfarm Payrolls—the disparity in job growth between native and foreign workers.

Many have suggested that the uptick in NFPs for private education and health services, as well as government positions, might be linked to the surge in illegal immigration at the southern border, necessitating additional personnel in these sectors. Notably, approximately 50% of job growth in 2023 occurred in government, social assistance, and healthcare, with government jobs alone accounting for about 25% of all NFP increases—a level last seen close to the Global Financial Crisis in 2008.

Arguably, the most concerning aspect of the NFP report was the decline in average weekly hours worked, which dropped from 34.3 to 34.1. The critical question here is whether this decline stems from increased productivity or individuals' inability to find desired employment, prompting them to reduce their working hours in favor of more leisure time, even at a lower wage.

Currently, many analysts are turning to PMIs to argue that the economic slowdown has ended and that the US economy is reverting to an expansionary phase. The coming months will be pivotal, as one would expect average weekly hours to rebound. Historically, PMIs have led average hours worked during economic expansions, while average weekly hours take the lead during slowdowns. However, there is currently a divergence between average weekly hours and PMIs.

Nonetheless, as I've previously highlighted, extrapolating labor market developments into the future is inherently challenging, as the labor market typically lags behind other economic indicators. This brings us back to the fundamental issue discussed earlier—the necessity for a consistent, logical theory to interpret the data rather than relying solely on correlations.

While extrapolating current labor market data may suggest an unstoppable US economy, it's crucial to consider the possibility of exogenous shocks that aren't accounted for in these models. These models often only offer explanations for rapid economic downturns in hindsight.

Indeed, economics revolves around humans who, unlike atoms, constantly adapt their behavior and actions to achieve certain ends. This dynamic nature makes it challenging for the econometric method to pinpoint turning points. As an observer of financial markets, one might notice that economists tend to be optimistic when things are going well and pessimistic when the outlook appears bleak. In this regard, they don't differ much from the common man.

Therefore, I'd like to take a step back and consider some additional data points beyond the job market. This week, Federal Reserve's Neil Kashkari argued that the yield curve is not a reliable recession indicator:

The yield curve at least in this current episode is not as reliable an indicator

Indeed, the spread between the US 10-year and the 3-month yield has never been inverted for such a prolonged period in 50 years. This may be why Kashkari makes that argument. However, it's essential to acknowledge that the lag effect of monetary policy varies widely throughout history, a factor that econometrics struggles to explain due to the sheer complexity of all influencing variables. Milton Friedman himself counters Kashkari's "it's different this time" argument:

I find it virtually impossible to conceive of an effective procedure when there is little basis for knowing whether the lag between action and effect will be 4 months or 29 months or somewhere in between.

Therefore, I argue that the mere fact that the yield curve inversion has persisted longer than it has in the last 50 years does not support the notion that it is unreliable this time. If it were unreliable this time, we would expect to see a significant increase in long-term yields, resulting in a bear steepener, where the long end rises faster than the short end.

Considering the rapid rise in the rate of change in the cost of capital since 2022 and the substantial increase in refinancing costs for businesses, I don't foresee this occurring. If that were the case, companies should utilize their improved financial position resulting from the high returns they receive for parking money in money market funds to reduce their refinancing requirements.

In January, US investment-grade companies issued a record $153 billion to refinance, a move heavily demanded by investors despite still deficient spreads. This indicates that investors have bought into the soft-landing narrative, as economic turmoil typically results in widened spreads.

To further explore why the US economy continues to defy expectations, we should look to other parts of the world. I would argue that America's strength is partly a result of economic weakness elsewhere. China is currently deleveraging and attempting to manage a controlled deflation of its bubbles. At the same time, Western Europe grapples with the conflict in Ukraine, increased regulation, and an energy policy that simultaneously slows economic activity. In contrast, the Biden Administration's massive deficits aim to incentivize companies to re-shore production to US soil.

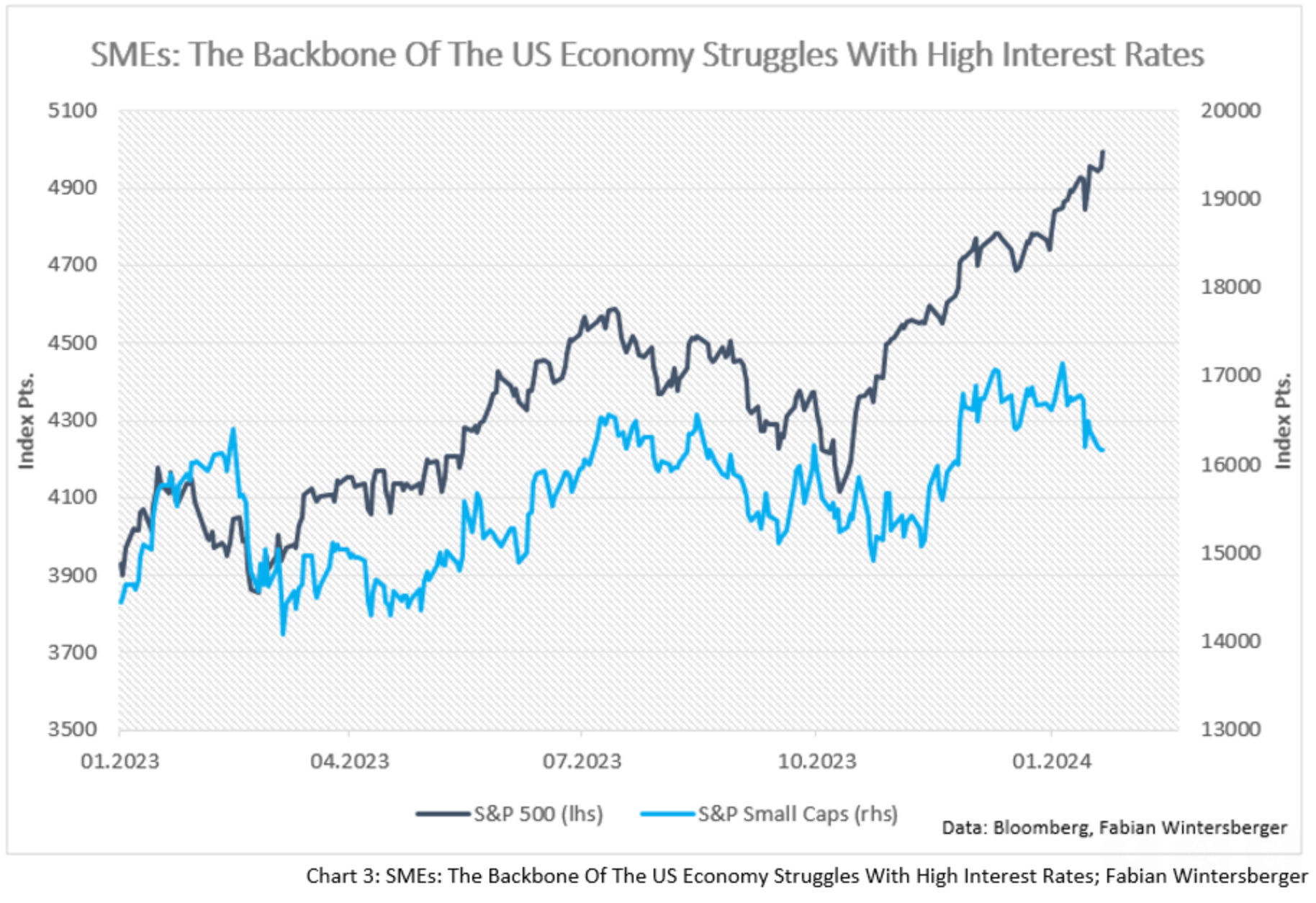

While this reshoring has stimulated short-term economic activity fueled by government spending, it may pose long-term challenges as increased investment leads to diminishing returns. Large corporations, benefiting from government aid through lobbying efforts, are the primary beneficiaries of such policies, leaving small and medium-sized enterprises (SMEs) behind. Higher interest rates further burden SMEs, as they rely more on short-term borrowing and lack access to long-term financing solutions available to larger companies.

If rates remain elevated for an extended period, SMEs will bear the brunt of the impact. Since March 2023, the S&P SmallCap 600 has stagnated, declining by 1.5%, while the S&P 500 has surged by 23%. This underscores the significant effect of high-interest rates on SMEs, which are crucial contributors to job creation and form the backbone of the US economy.

With all the data we've reviewed, let's now look ahead and consider what this could signify for the economy and financial markets moving forward.

Beginning with the US stock market, the robust NFP report from January undoubtedly dealt a blow to pessimists predicting an imminent recession in the US. Despite some concerning trends simmering beneath the surface, short-term indicators appear to support a bullish outlook on stocks. The S&P 500 and the Dow Jones have reached record highs this week, with the Nasdaq Composite close to surpassing its previous peak from December 2021. In the mid-term, I maintain a neutral stance, while long-term prospects lean toward bearish, in my opinion.

In Europe, the Dax and the Eurostoxx 50 are also scaling all-time highs, buoyed by the strength of other economic regions that benefit European export-oriented businesses. The outlook mirrors that of the US stock market, with a probable neutral-to-bearish view in the mid-term.

Despite recent upticks in interest rates, my perspective on interest rates and government bonds remains unchanged. Short-term bonds continue to offer limited downside but good upside potential. Additionally, I remain bullish on long-term bonds, though my short-term outlook shifts to neutral-to-bullish. European bond yields continue to be heavily influenced by movements in US interest rates, potentially paving the way for another leg down in bond prices.

I expect the dollar to maintain its dominance in the FX markets, as the NFP data has pushed back expectations for rate cuts. However, while Isabel Schnabel recently suggested that the ECB will proceed cautiously and that the data does not necessarily imply imminent rate cuts, I anticipate that the ECB will be compelled to cut rates sooner than the Federal Reserve, driving the euro towards parity in the future.

While the market appears to have priced in a soft landing for the US economy almost perfectly, my outlook remains unchanged. I anticipate a hard landing later this year, accompanied by a continued slowdown in inflation. As outlined earlier, I believe that additional data points do not justify the possibility of a no-landing scenario and uninterrupted expansion compared to those supporting other outcomes.

Furthermore, issues in the US regional banking sector are now spreading to Europe, following their impact on Japan's Aozora Bank. This week, Germany's Deutsche Pfandbrief Bank AG saw its bonds drop due to its significant exposure to the sector, marking the largest real estate crisis since the GFC.

Nevertheless, for the time being, the US economy continues to masquerade as "The Pretender" of sustained economic strength, propped up by US government spending on one hand and ongoing economic frailties in other parts of the world on the other. However, without a solid theoretical framework, interpreting the data becomes meaningless, and theory suggests a reckoning that will culminate in the hard landing few anticipate.

What if I say I'm not like the others?

What if I say I'm not just another one of your plays?

You're the pretender

What if I say I will never surrender?Foo Fighters – The Pretender

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

(Please note that all posts reflect my personal opinions and do not represent the views of any individuals, institutions, or organizations I may or may not be professionally or personally affiliated with. They do not constitute investment advice, and my perspective may change in response to evolving facts.)