The Dagger

Sometimes a majority simply means that all the fools are on the same side. - Claude McDonald

Some are calling the upcoming U.S. presidential election the most important in American history. Both Democrats and Republicans claim that a victory for their opponent would spell disaster for the country and the economy. Whether or not that's true, there's no doubt that in the age of social media, this election is probably the most anticipated in history.

Currently, the race seems incredibly tight, and things could go either way. However, I want to shift your attention away from the U.S. presidential election for a moment because last weekend, another important election took place: the Austrian elections.

Now, I’m not here to bore you with a detailed analysis of Austrian politics, which you may not be particularly interested in, but rather to highlight an intriguing similarity between the election campaigns of Austria's current chancellor, Karl Nehammer of the Austrian People's Party (ÖVP), and Kamala Harris’s.

Like Harris, Nehammer has been part of the government since the last election, and both have a mixed track record. While Harris has been relatively low-profile, particularly after failing to deliver on immigration reform, Nehammer has consistently tried to portray himself as a leader who gets things done. But like Harris, he’s achieved little beyond lofty rhetoric.

Yet, when their respective campaigns kicked off, their tone shifted dramatically. They started speaking as if they had never been part of the very governments they served in. In Nehammer’s case, this is even more absurd than it is for Harris, given that his party, the ÖVP, has been part of almost every government coalition since 1986.

The ÖVP tried to position itself as the centrist party, painting its rivals—the Social Democrats and the far-right Freedom Party—as extremists. They promised to tackle illegal immigration, curb inflation, reignite the stagnant economy (Austria is facing a similar economic stagnation to Germany), and ensure national security, claiming they would prevent terrorist threats. You might recall that Taylor Swift canceled her concert in Vienna due to a terror threat.

Both Harris and Nehammer face the same challenge when making such claims: if they can deliver on these promises, why haven’t they done so already during their time in office? If the People's Party is truly the party of fiscal responsibility and economic competence, why did the previous government continue reckless spending and expand subsidies? Why didn’t Nehammer, in his role as Minister of the Interior, prevent the first and only terrorist attack on Austrian soil, even though all the necessary intelligence was available?

We may never fully understand these contradictions, but it seems the voters did. That’s likely why Nehammer and his party lost their first-place position. Voters weren’t as gullible as his campaign strategists may have hoped. They remembered that Nehammer had been chancellor and that his party had been in power for nearly 40 years, consistently failing to deliver on its pre-election promises. Despite polls suggesting a close race, the outcome was clear.

I have no idea whether Harris will succeed against Trump, but it’s possible that pretending not to have been part of the incumbent government could backfire, just as it did for Nehammer. We’ll see if Kamala Harris suffers the same fate as Karl “Karlmara” Nehammer. After all, as Abraham Lincoln once said:

You can fool some of the people all the time, and all of the people some of the time, but you can not fool all of the people all of the time.

Those who have been predicting an imminent recession in the U.S. have mainly cited the gap between Gross Domestic Product (GDP) and Gross Domestic Income (GDI). However, last week, the updated figures from the Bureau of Economic Analysis dashed those hopes.

Not only was real GDP revised upward, but real GDI also saw a significant upward revision, driven by a substantial increase in consumer spending and investment. As a result, the discrepancy between GDP and GDI shrank from over 2.5% to just 0.3%, consistent with pre-pandemic levels.

If you're a long-term reader of my work, you may recall that I mentioned this discrepancy before. The recent revisions demonstrate that while we often take initial releases at face value, they are ultimately just estimates that can change significantly with later updates. In this case, it's clear that the market was more concerned with GDP, largely ignoring the GDI discrepancy, except for those forecasting a recession.

Along with the rise in Gross Domestic Income, the personal savings rate was also revised upward, which has important implications for future spending. Previously, most economists and analysts believed that the excess savings built up during the pandemic due to government stimulus had been entirely depleted. Initially, the Bureau of Economic Analysis estimated that the savings rate had fallen to 2.9%, a near multi-decade low, comparable to the period just before the GFC.

However, following the income data revisions, the savings rate was adjusted upward to 4.8%, aligning with the multi-decade average. This is significant because it suggests that incomes have risen enough that, on average, people are no longer dipping into their savings to maintain or increase their consumption levels.

As a result, one can now assume that the previous belief—that the excessive savings built up during the pandemic have already been depleted—may not hold. The money supply expansion during those years appears to generate income and fuel spending. Proponents of this view, such as Bob Elliot from Unlimited Funds, have referred to this as an "income-driven expansion."

Initially, I was skeptical about whether the current expansion was still driven by income. However, the upward revision of the savings rate has made me reconsider. It also reminded me of a paper by Straub et al., which estimated that the stimulus would take about five years to "trickle up" through income brackets before its effects are fully extracted from real economic activity.

Consequently, I wondered if this theory could also be framed from an Austrian economics perspective. Let’s assume an economy where the government distributes stimulus payments to everyone, financed by the Federal Reserve by expanding the money supply—similar to what happened during the pandemic.

During this period, everyone received a fixed amount of money to support the economy. This provided additional income or compensated those laid off due to government-imposed shutdowns. According to the BEA, around 20 million people were unemployed in April 2020, representing about 15% of the workforce. While the stimulus helped the unemployed, it also provided extra income for those who remained employed.

This led to an enormous spike in the savings rate, as many parts of the service sector were shut down, limiting people's ability to spend money as they typically would. Additionally, spending patterns shifted from services to goods, such as home furnishings, as people adapted to new circumstances.

As a result, demand—and consequently inflation—increased as producers raised prices. This created additional income for businesses, reflected in rising profit margins. However, as businesses generated more income and faced rising demand, they also adjusted by hiring more workers and transferring business income to wages. These new wage earners, in turn, used their income to purchase goods and services, causing the newly created money to circulate throughout the economy, driving up prices across the board.

In normal circumstances, one could argue that the effects of quantitative easing (QE) and monetary expansion are more limited, as they tend to influence specific sectors where workers consume a smaller portion of their income. In these cases, the money is more contained within certain parts of the economy, having a more muted effect on overall consumer spending.

This time, however, the stimulus was distributed broadly and disproportionately benefited low-income earners, who needed to spend the money on consumption. Their spending created income for others and drove income growth, alongside consumer price inflation. The critical question is what share of business earnings has been transferred to wage earners.

There seems to be sufficient money circulating in business accounts to support wage increases in a labor market that, while loosening, is far from deteriorating. For most people in the economy, rising wages are the primary driver of consumption. As Bob Elliot from Unlimited Funds pointed out:

With wage growth near 7% nominal, its not too hard for households to keep spending at 5-6% nominal.

The recent recovery in asset prices has also improved businesses' ability to offer rising wages, thanks to increased investment income. Overall, the private sector has reduced its debt levels, as rising incomes have decreased the relative debt burden.

While it was clear that the economy would need to normalize at some point, the substantial imbalances created by the U.S. government—through stimulus and sustained high spending—and by the Federal Reserve—by keeping interest rates too low for too long—could potentially lead to a second wave of economic growth.

I suspect that, as the money "trickles up," as Straub et al. describe, business owners and investors are reallocating part of that income back to low—and middle-income earners. As inflation declines but nominal spending remains high, this dynamic could lead to a pickup in real growth while the tight labor market normalizes and loosens only slightly.

This challenges the Federal Reserve, which has already initiated its easing cycle and plans to cut interest rates over the coming months and years. Steady nominal growth, rising real growth, and easier financial conditions set the stage for another wave of inflation, mainly if real economic growth runs into supply constraints that limit further expansion.

The Fed is betting on a labor market slowdown that may be further off than they anticipate—or fear. While falling CPI numbers have relieved the Fed, their belief that interest rates are highly restrictive and far above neutral could be a misinterpretation of the data.

The economic data currently supports the framework outlined earlier and points toward a reflationary environment. As I mentioned last week, while this might not lead to rising inflation, it could result in inflation falling more slowly than suggested by current monetary aggregates.

Income growth remains strong, and declining short-term interest rates make it easier for businesses—particularly SMEs—to borrow. Unlike large corporations that can refinance over the long term, SMEs mostly have to borrow short-term and would benefit from lower short-term rates. As the Fed controls short-term interest rates, reductions in the Fed Funds Rate provide much-needed relief to these smaller businesses while less impacting larger corporations that tend to borrow at longer maturities.

However, large corporations that have invested heavily in short-term yield instruments will see declining interest income as the Fed cuts rates. This could present challenges for big-cap stocks in the months ahead. That said, the recent improved market breadth suggests that small caps could benefit if the market successfully pushes the Fed to cut rates as much as expected.

The implication is that while some large-cap stocks may continue to rise, it seems unlikely they outperform SMEs, which stand to benefit more from lower short-term rates. However, if real growth picks up and nominal growth holds steady at around 5%, the long end of the yield curve is likely to rise again as long-term growth prospects improve.

This would catch many investors off guard, particularly those who have loaded up on long-term bonds and interpret Fed rate cuts as a sign of an imminent recession or significant economic slowdown. Following the rate cut, the recent bond market movement suggests that the "long bond" trade may already be overcrowded, offering limited upside.

The key risk here is that a more substantial reduction in interest rates than the market anticipates would be required to justify a long bond position. For example, with the U.S. 10-year yield at 3.8%, the Fed would need to cut rates to at least 2.75% for yield spreads to return to their historical average. If you believe in the upside potential of long-term bonds, you would need to see much deeper cuts.

Given the current economic data, I remain unconvinced that long bond positions offer a favorable risk-reward balance. Short-term or corporate bonds, on the other hand, could be more attractive and offer better yields. In my view, a return to economic normalization is already largely priced in, and the data doesn't currently support a recession trade.

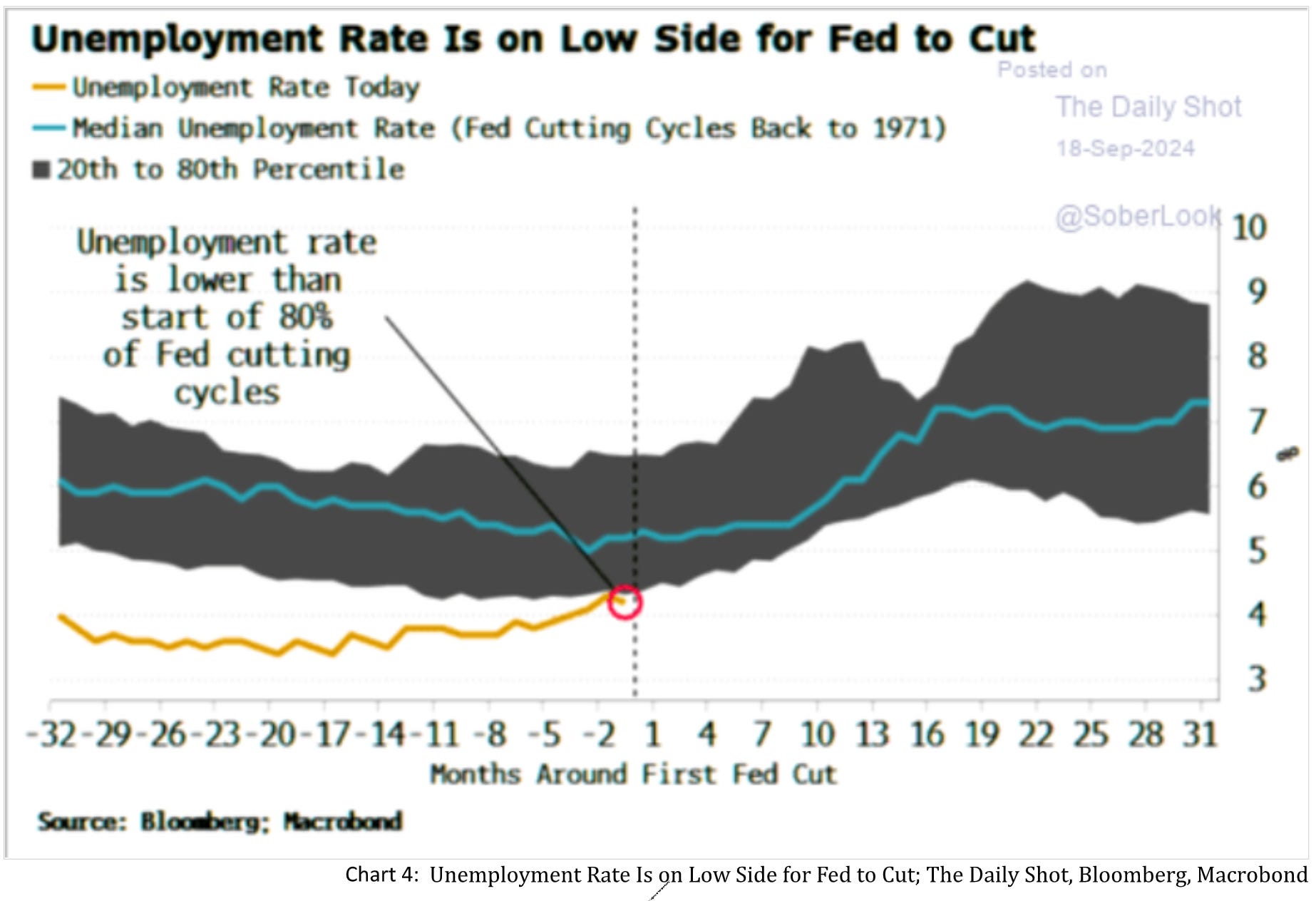

The Fed has indeed emphasized the need to loosen the labor market, and its rate cuts aim to prevent unemployment from rising too much due to what it perceives as very restrictive interest rates. However, unemployment is so low that it is lower than at the start of 80% of the previous Fed cutting cycle. The economy is still performing too well to justify significant interest rate cuts at this time.

With unemployment still low and the economy continuing to benefit from income-driven expansion fueled by earlier monetary stimulus, it's difficult to see the Federal Reserve cutting interest rates as much as the market anticipates. As a result, I believe the recent bond rally could reverse quickly if it hasn't already begun. Considering the current data, it’s reasonable to expect investors to start demanding higher term premiums for holding long-term bonds. From a trading perspective, it's hard to justify being long bonds at the moment.

Whether a potential bear-steepening of the yield curve will immediately weigh on stocks is less certain. I sense that there's a high probability the stock market rally will continue, possibly culminating in a blow-off top heading into year-end, especially if the Fed scales back its rate-cut forecasts and only cuts rates modestly.

With rising interest rates, the U.S. dollar index has bounced back from its late-September low, appreciating against both the euro and the yen. Europe appears to be drifting from stagnation into recession, and Asia continues to face challenges, although recent stimulus measures from China have provided some relief.

Given these dynamics, I wouldn’t be surprised to see further dollar appreciation, especially with the recent increase in geopolitical tensions in the Middle East. If the conflict escalates to the point of disrupting trade, short-term disequilibria could push CPI numbers higher in the near term.

The effects of rising interest rates and a stronger dollar will likely be felt in the coming months. As we move into next year, with earnings expectations still high, rising yields could potentially be the dagger that triggers a correction in stock prices.

And I feel this all too slow

And I've been here for so long

And I feel so empty

As you walk awayRoadrunner United - The Dagger

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. They do not constitute investment advice, and my perspective may change over time in response to evolving facts. It is strongly recommended to seek independent advice and conduct your own research before making investment decisions.