Supernova

When a star goes supernova, the explosion emits enough light to overshadow an entire solar system, even a galaxy. Such explosions can set off the creation of new stars.– Todd Nelsen

Sometimes, certain things in economics do not work as they should. Financial professionals often find themselves sitting in front of their screens, wondering why bad earnings, lowered guidance, or worse-than-expected economic data lead to increased asset prices instead of the expected drop.

This phenomenon is not new, and economists have observed occurrences that contradict the law of supply and demand. Typically, when the price of a good increases, demand decreases. However, in the real world, things sometimes behave differently. To delve deeper into this, let's journey back to Ireland in 1845, a time is commonly known as the “Irish Potato Famine”.

The years from 1845 to 1852 were marked by starvation and disease for the Irish people. Consistently poor potato crops decimated the population, with approximately one million people losing their lives and at least 2.1 million emigrating—a significant historical exodus. Potatoes were crucial for feeding both the population and livestock during this period.

Sir Robert Giffen, a 19th-century Scottish economist, later discovered that people increase their demand for certain essential goods even as prices rise instead of turning to substitute goods. The term "Giffen good" was coined by the British economist Alfred Marshall, who introduced the concept in his book "Principles of Economics" in 1890.

The “Irish Potato Famine” is a fundamental example of such goods because impoverished households that heavily relied on potatoes demanded more despite the rising prices of potatoes due to a reduced supply. Theoretically, three necessary conditions can lead to this situation: the good must be inferior, there must be a lack of close substitute goods, and it must constitute a significant portion of a buyer's income.

A few years after Marshall's publication, American economist Thorstein Veblen identified another exception to the law of supply and demand. This concept is quite similar to Giffen goods, but Veblen goods are luxury items, often seen as status symbols. Examples of Veblen goods include luxury cars, designer clothing, and high-end watches, which are considered desirable precisely because of their high price tags.

Veblen goods are associated with conspicuous consumption and the demand for luxury items, particularly among the wealthy. The Veblen effect highlights the role of conspicuous consumption, where individuals signal their wealth and status by purchasing high-priced items, further enhancing the product's desirability within a specific social group.

Both Giffen and Veblen goods challenge traditional economic theories, which state that higher prices should result in lower demand. However, do they genuinely disprove what is arguably the most fundamental law in economics: the law of supply and demand? I would argue that they do not, as economists often oversimplify this concept, leading to misunderstandings.

The problem is that if a good is a good by virtue of it being valuable toward some end, what defines the good is not the physical composition of it, but the use-value. – Per Bylund

For example, if you consider a watch as nothing more than a bracelet with a time-telling disc, you might question why people opt for a Rolex instead of an inexpensive timepiece. Similarly, when we consider technical capabilities alone, choosing an iPhone over a more affordable smartphone with superior features from a different manufacturer may seem irrational.

The rationale behind this is that these goods are not interchangeable. It's not merely about their physical attributes but also the intangible, non-measurable use-value that consumers attach to them. Take band shirts, for instance—they often have subpar quality and cost nearly as much as a high-quality shirt, but it's not about the fabric; it's about the band and the statement it makes within the associated community, signaling that you belong to that group.

November has proven to be a disappointment for economic data, and this disappointment extends beyond Europe, where it was somewhat expected, reaching even the United States. On November 1, the ISM numbers for Manufacturing, employment, and new orders fell short of expectations by a considerable margin. As some observers have noted, this underperformance may set the stage for the Federal Reserve to maintain interest rates at their FOMC meeting last week.

During the press conference, Jerome Powell maintained a hawkish stance but acknowledged the need for caution in future actions. He and his colleagues also recognized that the effects of monetary tightening are increasingly evident in the economic data. Furthermore, Powell admitted that the Fed, like many of us, had underestimated the strength of households and businesses regarding their balance sheets.

Despite this, nothing in Powell's speech or the subsequent Q&A session sounded explicitly dovish. Nevertheless, U.S. stock market indices rallied throughout the rest of the week. The Nasdaq surged by 4%, the S&P 500 rose by over 3%, the Dow Jones saw a roughly 2.5% increase, and the Russell 2000 also demonstrated a remarkable rally, emerging as the strongest among all indices by Friday, November 3.

Friday brought another wave of discouraging U.S. economic data. First, we received the Nonfarm Payroll Report, which was a disappointment. Both total nonfarm and private payrolls fell short of expectations, and manufacturing payrolls declined three times more than the median estimate had suggested. Notably, this year has seen a recurring pattern where the initial NFP numbers are overestimated and require downward revisions.

Additionally, the unemployment rate has increased to 3.9%, and hourly earnings growth has decelerated to 2.4% annualized in October, or 4.1% compared to the previous year. The labor force participation rate dropped slightly from 62.8% to 62.7%. Clearly, the labor market is gradually cooling.

The ISM Services Report presented another disappointment, falling from 53.6 in September to 51.8 in October. Notably, new orders exceeded expectations, registering at 55.5 instead of the expected 51.1. This suggests that the service sector is showing signs of becoming uncertain, though it is still mildly expansionary.

Market observers have sounded the alarm regarding the increasing "Sahm-Rule" indicator, named after its inventor, Claudia Sahm. With unemployment rising to 3.9%, it has climbed 0.33 percentage points from its low earlier this year. Historically, a rise in the three-month average unemployment rate has signaled the onset of a recession.

However, Sahm has consistently emphasized that this indicator should not be used to predict a recession. Her usual recommendation has been for the government to implement specific fiscal support measures to stabilize the economy. In a recent Bloomberg Opinion piece, she pointed out that the labor market is sending mixed signals, and the indicator may not be accurate this time. Although I can't entirely agree with her, I highly value a well-articulated counter-argument to my base case on the U.S. economy.

As we progress further into the fourth quarter, businesses are lowering their earnings expectations. This is evident in the diminishing mentions of "strong demand" during earnings calls. The recent weak Chinese export numbers further support this weakening trend, indicating a waning demand.

Therefore, considering the latest FOMC press conference by Jerome Powell, I believe the market is correct in assuming that the Fed has concluded its interest rate hikes. However, market participants may still underestimate Powell regarding their assumptions about the future interest rate path.

As of the moment I'm writing (November 9), overnight index swaps imply a Fed Funds Rate of 4.72% for September, approximately 60 basis points lower than the current 5.35%. In my opinion, this expectation is likely to be incorrect. I see three possible scenarios: the Fed could either act with haste and cut rates more rapidly and deeply, maintain rates at their current levels, or reduce interest rates once while accelerating Quantitative Tightening.

However, these scenarios primarily impact financial markets in the mid-term rather than immediately. I have repeatedly outlined my bearish mid-term view on stocks and longer-term bonds in previous weeks, so that I won't reiterate it here.

Today, my focus is on the short-term, which is why I began this week's Weekly Wintersberger with the story about Giffen and Veblen goods. The incoming data suggests that the economy is cooling, consumption is slowing, and, consequently, the labor market is finally beginning to cool as private investment slows due to the rapid rise in interest rates. Yet, I'm contemplating the possibility of stocks experiencing a supernova moment as we approach year-end.

A supernova is a powerful and catastrophic explosion of a massive star at the end of its life cycle. During a supernova, the star briefly outshines an entire galaxy. It can release an enormous amount of energy and matter into space, forming new elements and often leaving behind a dense, compact remnant such as a neutron star or a black hole.

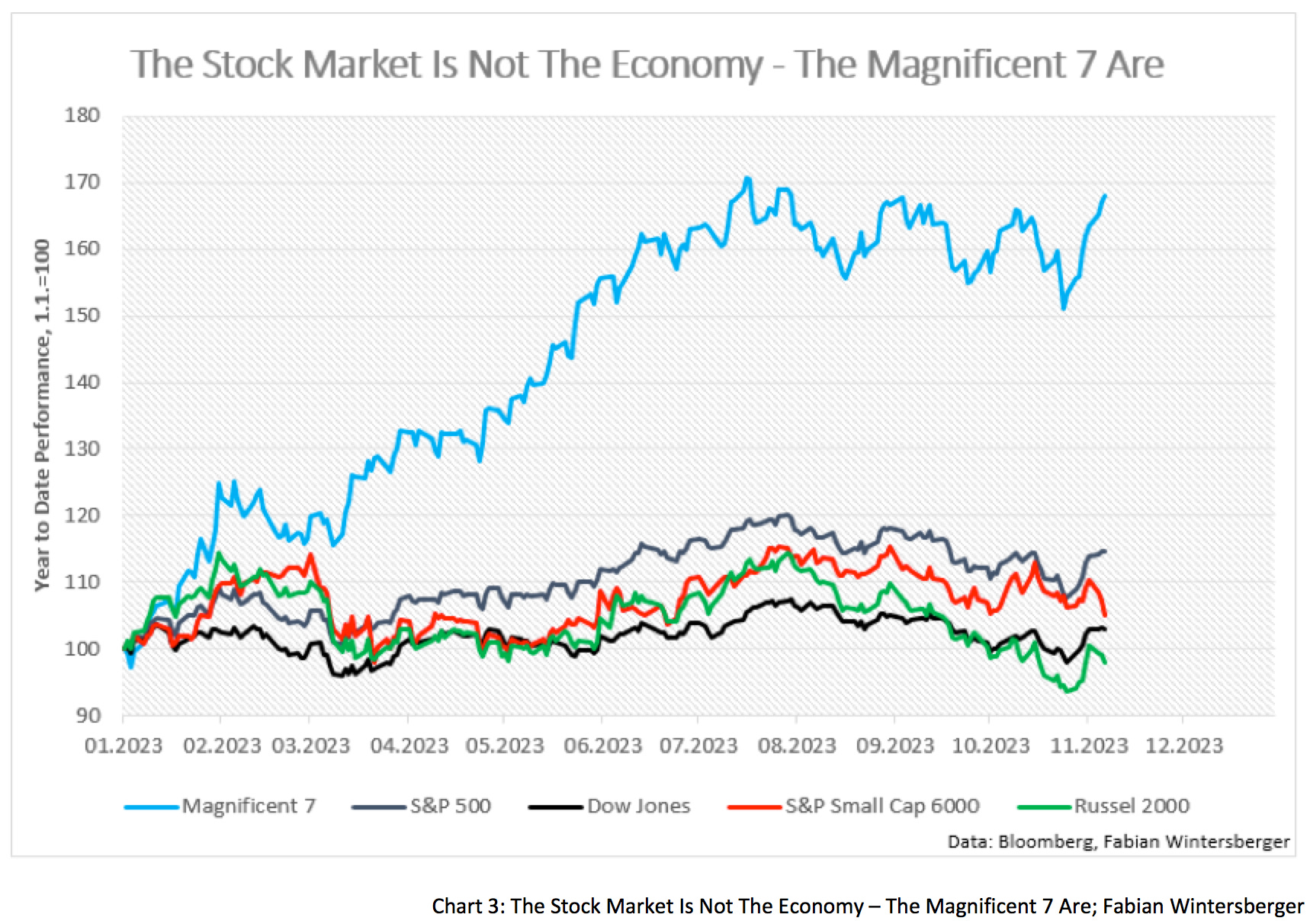

Remember what happened last week between the FOMC meeting and the NFP Report. Despite worsening market data, the stock market rallied. What could be the rationale behind this when most indicators point to a deteriorating economy? One key point is that the stock market is not the economy. Stock prices are influenced by past and present data as well as expectations for the future.

Small and medium enterprises employ most people in the U.S. workforce, and despite the positive surprises in economic data, the Russell 2000 index is roughly where it started the year. In contrast, the Magnificent 7 stocks propelled the entire S&P 500 this year and have seen significant gains. In the end, if it holds that the stock market is not the economy, it is because the Magnificent 7 represents a different reality.

Now, let's assume that the Fed is finished with raising interest rates. Let's assume that incoming economic data continues to darken across the board. What is the likely conclusion for investors? I would surmise it to be the same as in the last 40 years: the Fed is done with hiking rates, and significant cuts could soon follow.

In such a scenario, the stock market typically receives support or even experiences a rise due to the anticipation of rate cuts. Usually, the stock market tends to start selling off when the Fed initiates interest rate cuts for the first time, and this decline continues until the low point of the cutting cycle is reached.

When investors sell stocks, they often begin to purchase other assets. As the economic situation worsens and the demand for safe havens increases, investors traditionally turn to bonds and gold. For instance, they might sell stocks to buy bonds.

The current expectations among market participants are that the Fed can achieve a soft landing and that the economy is generally in good shape. Perhaps it cools down a bit, but then it's expected to recover. This aligns with what most investors seem to believe. Despite this optimism, they have been loading up on bonds throughout the year. Initially, this was driven by the anticipation of an impending recession. When that didn't materialize, and rates continued to rise, they believed that bonds offered an attractive risk/reward proposition due to convexity. According to the JP Morgan positioning survey, investors are inclined to buy stocks but are reluctant to sell their bond holdings.

If investors want to buy stocks but are reluctant to sell bonds, they can either deploy the cash they have on the sidelines or sell other stocks (or assets in general). If they choose to use their cash, they might opt for the Magnificent 7, given their past performance, which could further boost the value of these stocks.

However, if the assumption is that the Fed will shift its stance and cut interest rates aggressively soon, which stocks should benefit the most? Intuitively, the Magnificent 7 stocks may still benefit, but the upside potential in the short term seems limited, given the worsening economic data.

Another option that comes to mind is technology stocks, but many are currently not profitable. With interest rates remaining high, whether one would want to bet on a return of NIRP arises. This leads me to the Russell 2000 Index. While I might be mistaken, if the rate hikes earlier this year had a significant negative impact on the Russell, the anticipation of rate cuts might favor this index.

In the bond market, exposure is already relatively high. It's unclear whether there's much room for additional buying as long as investors want to increase their stock exposure. Nevertheless, weak economic data might benefit bonds in the short term.

Personally, I would pay more attention to the front end of the yield curve, as the downside appears limited here, considering that the Fed is likely finished with rate hikes or very close to the peak. The risk, however, is that investors might sell short-term bonds to buy stocks, so betting solely on a move in interest rates may not yield immediate returns.

On the long end of the yield curve, the risk remains the substantial issuance of U.S. treasury bonds in the future and the potential for yields not to drop significantly, given the existing exposure to the long end. I remain convinced that buying bonds when the Fed cuts rates is a more suitable time, especially as long as inflation remains above the 2% target, which is expected to persist until year-end.

The euro has also recently made some gains against the dollar, thanks to the pullback in oil prices and the easing of geopolitical tensions in the Middle East. Investors appear to believe that the conflict is now contained within the region. Consequently, the euro has shown signs of a short-term uptrend since October, maybe a short-time bullish signal.

The final question is whether the potential "Supernova" will also manifest in the European stock market. My intuition suggests that this is a possibility. However, there are a couple of factors to consider. On the one hand, Europe is already experiencing a recession. On the other hand, there are the EU's and Germany's economic policies and the energy price challenge. Nonetheless, on the energy supply front, the situation appears to be under control, with gas storage facilities across the continent being nearly 99% full.

Nevertheless, as economic data deteriorates, it will likely further favor the dollar and U.S. stocks. Additionally, there is a prevalent belief that the ECB will cut interest rates following the Federal Reserve Fed. I, however, hold an opposing view and believe that the market is overestimating Madame Lagarde while underestimating Jerome Powell's determination to redefine the Fed's approach.

Considering this, I believe the possibility of a near-term Supernova in the stock market isn't entirely far-fetched.

if God is real, there's no reason to cry

Tell me how it feels, tell me how it feels if death is a lie

What if I could? What if I could? What if I could let it go?

What if I could? What if I could? What if I could let it go?Ghostkid - Supernova

I wish you a wonderful weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

(Please note that all posts reflect my personal opinions and do not represent the views of any individuals, institutions, or organizations I may or may not be professionally or personally affiliated with. They do not constitute investment advice, and my perspective may change in response to evolving facts.)