State of Unrest

Despite increasing volatility and uncertainty, gravitational market forces remain

Economics is like gravity: Ignore it and you will be in for some rude surprises. - Charles Wheelan

The past few weeks have been a wild ride for markets. Amid the excitement-or disappointment—sparked by statements from Trump and his administration, it’s easy to lose sight of the underlying forces driving prices with fundamental impact.

As I see it, these statements may fuel volatility and short-term price swings, but they don’t dictate the market’s broader trajectory. Fundamentals are like gravity in markets. Despite sentiment-driven price action, the true state of market conditions serves as the guiding star, leading markets toward convergence once the noise subsides.

It’s often said that markets don’t move in straight lines, highlighting a key distinction between market behavior and the laws of physics. While both human action and physics follow fundamental laws, human behavior is far less predictable due to factors such as emotions and sentiments. Market participants act on emotion, whereas gravitational forces simply react. This is why econometric models always include an “error term.”

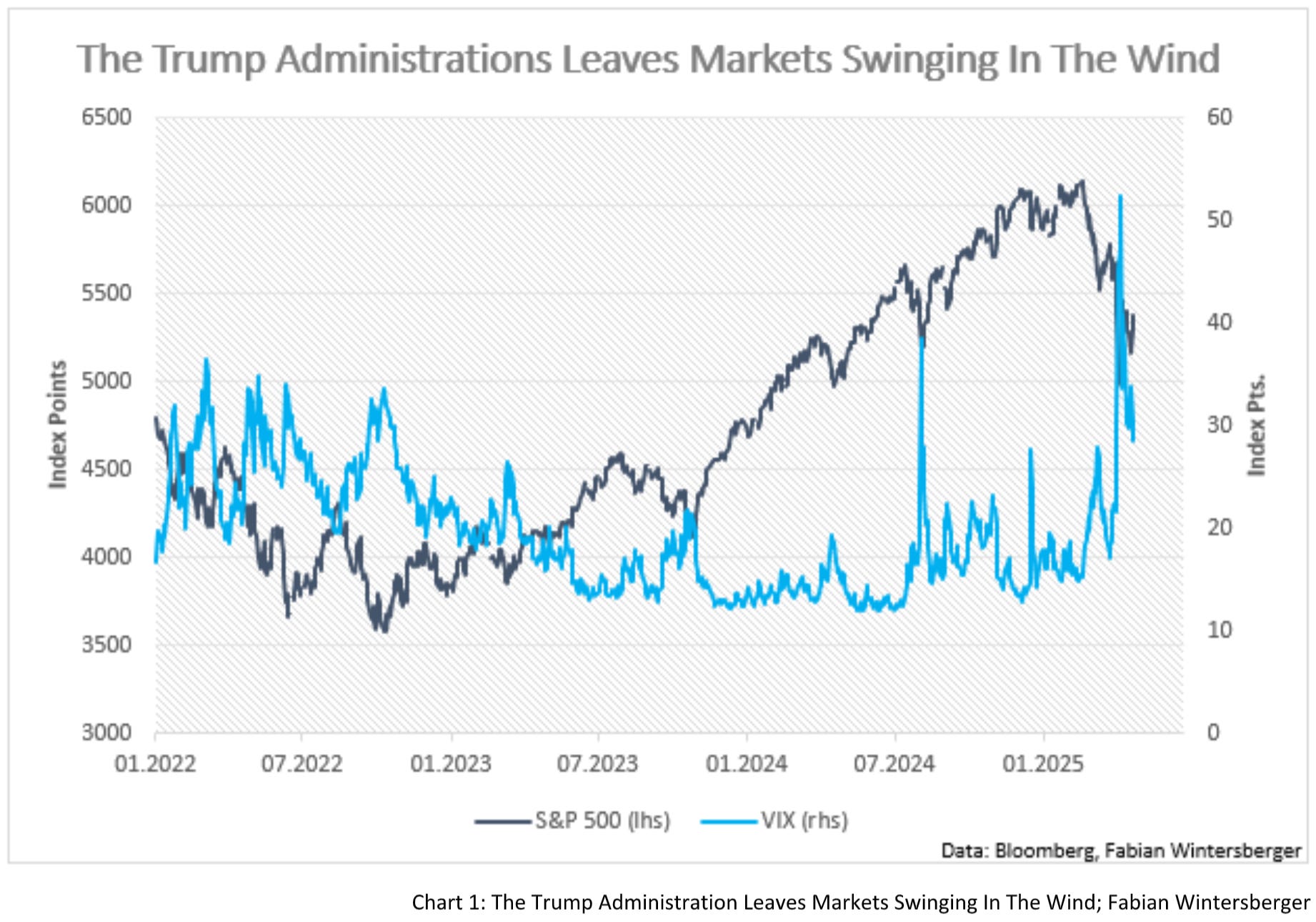

Sentiment and narratives can significantly influence prices, but connecting the dots is essential to gauge where prices might head. Recent equity moves illustrate this. One day, Trump or one of his tariff hawks appears on TV, dashing hopes of de-escalation and triggering market drops. Next, Scott Bessent calms nerves, and the market rallies. A glance at the VIX underscores the confusion gripping markets amid this uncertainty.

Yet, the complexity of human behavior means prices may not settle where expected, even if your conclusions are spot on at a given moment. Facts evolve, requiring analysts, investors, and traders to adjust to new information as it emerges.

Let’s start with yesterday’s PMIs for the Eurozone and the US. Given the tariff-induced uncertainty, one might have expected these indicators to miss expectations significantly. Surprisingly, the miss was minor, despite the turbulence caused by Trump’s “Liberation Day.”

The Eurozone Composite PMI came in at 50.1, just below the expected 50.2. The Services PMI was 49.7 (expected 50.5), while the Manufacturing PMI surprised at 48.7, beating the anticipated 47.4. The report offers mixed signals: most manufacturers boosted production, slowed job cuts, and improved profit margins, benefiting from easing inflation pressures and lower energy prices tied to heightened US recession fears—a boon for European manufacturing.

French and German PMI reports also highlight tailwinds, with manufacturers poised to gain from announced increases in defense and infrastructure spending. The commentary suggests this spending will eventually lift the services sector, albeit with a lag.

Compared to the pessimism surrounding Europe at the start of the year, these numbers hint that fiscal spending could create a favorable environment for manufacturing, as businesses adapt to rising demand for defense goods and an ECB ready to cut rates further if needed. The Manufacturing PMI’s steady improvement recalls the recovery following the 2010s sovereign debt crisis.

While Europe shows signs of clawing its way out of the mud with loose fiscal policies, the US paints a different picture. S&P Global Chief Business Economist Chris Williamson notes in his PMI commentary that output growth, business confidence, and optimism are waning, while inflationary pressures rise. His remarks on inflation deserve attention:

Tariffs are increasingly cited as the primary driver of higher prices, though labor costs continue to climb, prompting companies to raise selling prices at the fastest pace in over a year. In manufacturing, prices have increased by the steepest margin in nearly two and a half years. These higher prices will likely fuel consumer inflation, potentially limiting the Federal Reserve’s ability to cut rates when a slowing economy needs a boost.

This suggests that, despite money supply and demand not signaling concerns about inflation, the near-term inflation path could be bumpy. As noted earlier, sentiment and adjustments can create disequilibria, resulting in prices exceeding their fundamental equilibrium levels. This could lead to volatile inflation in the months ahead, making the Fed’s decisions more complicated.

If this scenario unfolds, the Fed may delay action until the labor market weakens significantly. So far, that’s not the case, and I suspect employment impacts may lag longer than in past cycles.

Two weeks ago, I suggested that the fallout from Trump’s tariff policies might resemble the 2020 turmoil more than typical slowdowns. First, the impact stems from deliberate policy choices. Second, uncertainty disrupts global supply chains. Since then, several commentators have echoed this analogy.

Trump’s push to reshape the global economy has alarmed big businesses, particularly due to potential disruptions to their supply chains. Axios reported:

The CEOs of Walmart, Target, and Home Depot privately warned Trump that his tariff and trade policies could disrupt supply chains, raise prices, and empty shelves, according to sources familiar with the meeting. “The big box CEOs told him prices are steady now but will rise. And this wasn’t about food. He was told shelves will be empty,” an administration official said.

This may have prompted the administration’s softer tone since Tuesday, when they suggested the actual tariff rate on China would be far below the previously floated 145%.

Still, unlike the overnight disruptions of 2020, these changes may unfold gradually. This points to a prolonged GDP decline rather than an abrupt one, consistent with empirical data on the economic impact of populism.

Such a slow decline supports my view that labor market effects could lag longer. Businesses, recalling the struggles they faced with rehiring after 2020, may delay layoffs as long as possible, keeping the labor market tighter for longer while inflation remains volatile and the Fed remains on hold.

In conclusion, while volatility persists, short-term market moves may remain sharp, driven by sentiment and emotion. Yet, the gravitational pull of fundamentals endures.

For now, American exceptionalism in the stock market seems to have faded. The Trump administration has made foreign investors wary of dollar assets. Europe’s expansionary fiscal policies, compared to fiscal drag in the US, should further tilt the balance. Consequently, I expect long-term interest rates in the Eurozone to rise, reflecting increased government bond supply from larger deficits, while the US may see lower long-term rates. However, a potential US CPI spike in the coming months could shake things up.

On the dollar, I’m skeptical of claims that it’s losing its status as the global reserve currency. That may happen eventually, but not imminently. For the dollar index to regain strength, it needs to break above 100.

A stronger dollar could halt oil’s current downtrend. While oil was positively correlated with EUR/USD in the 2010s, the correlation turned negative post-2020. A falling EUR/USD could push oil prices toward $ 80, while a stronger EUR might keep them lower.

Though the odds of a US recession have risen, it’s too early to say whether one will materialize or remain confined to the US. Regardless, the market’s gravitational forces will shape the path ahead, but the journey may be one of “State of Unrest.”

State of unrest, witness what you’ve created

Pathogenic, unabated, we are chaos detonated

State of unrest, witness what you’ve created

We are chaos detonated

Kreator & Lamb of God - State of Unrest

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you shared it on social media or gave the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. They do not constitute investment advice, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.