Starting Over Again

The New Fed, Global Disinflation and the Next Test for Equity Markets.

No matter how hard the past, you can always begin again. — Buddha

For the last three months, markets have increasingly priced a world in which energy prices remain elevated, tensions in the Middle East continue to escalate, and inflation proves more persistent than many investors expected. Two weeks ago, it looked as if the conflict was entering a more dangerous phase, and markets started to worry.

But over the weekend, the picture changed dramatically. US President Trump announced that Washington and Tehran had reached a memorandum of understanding. Whether the agreement ultimately holds remains to be seen, but markets immediately focused on its most important implication: a significantly lower probability of an energy shock.

The drop in oil prices and increasing confidence within markets that this is the beginning of the end of the conflict have shifted the macroeconomic outlook. The new situation helps market participants put the latest US CPI and PPI reports into a different light.

All of these events unfolded just ahead of Wednesday’s FOMC meeting, the first headed by the new Fed Chair, Kevin Warsh. At the press conference, Warsh made it clear that this would be a different Fed from the one investors had become accustomed to under Jerome Powell.

Taken together, these developments raise three important questions. How different will Warsh’s Federal Reserve be from Powell’s? To what extent does the Memorandum of Understanding change the global inflation outlook? And if inflation fears continue to fade, can financial markets absorb the growing wave of equity issuance that lies ahead?

The New Fed: End Forward Guidance And Fix Inflation

It was no surprise that the Fed kept interest rates steady at 3.50 - 3.75%. Yet investors were far more interested in how and by how much Warsh’s approach would differ from Powell’s. As it turned out, quite significantly.

One of the most notable aspects of the meeting was Warsh’s apparent desire to end the Fed’s reliance on forward guidance. The new Chair repeatedly avoided discussing future policy decisions, declined to provide his own interest-rate projections, and instead emphasized the importance of incoming data. Markets were given remarkably little insight into how the committee currently thinks about the future path of monetary policy.

There was, however, one notable exception. Warsh repeatedly emphasized the Fed’s commitment to restoring price stability. Despite the recent decline in oil prices, policymakers appear unconvinced that the inflation problem has been solved. The latest retail sales report provides one possible explanation. While energy-driven inflation pressures may be fading, demand remains surprisingly resilient.

US retail sales numbers, which were published just hours before the FOMC decision, underscored that point. The headline number and the control group both came in significantly above expectations of 0.6% (actual: 0.9%) and 0.4% (actual: 0.7%).

The data reinforces a point I have made repeatedly in recent months. While the conflict in the Middle East and higher oil prices undoubtedly contributed to inflationary pressures, they were unlikely to be the sole driver. Consumer demand remains remarkably resilient, suggesting that the recent inflation impulse was at least partly demand-driven rather than merely the consequence of a temporary energy shock.

Warsh’s statement that the Fed, under his watch, will fix the inflation problem gave the press conference a slightly more hawkish tone than widely anticipated. Nevertheless, nothing Warsh said answered the question of whether he’ll be the inflation hawk he was during the aftermath of the GFC. He didn’t provide any projection regarding the Fed’s future policy path and essentially told markets to figure it out themselves by looking at the incoming data.

Yet although he talked about fixing the inflation problem, he didn’t lay out the conditions under which the Fed would actually raise interest rates. Instead, he repeated an argument he made prior to his election, namely that the Fed won’t have to choose between inflation and the labor market. He appears to believe that the US economy can continue to grow without necessarily generating the kind of inflationary pressures that would require further tightening.

As of writing, US 10-year Treasury yields are already back where they were before the press conference. On the short end of the curve, however, yields moved higher, with markets now pricing in a full rate hike this year. It is reasonable to expect that Trump’s Memorandum of Understanding and the subsequent decline in oil prices will exert downward pressure on inflation in the coming months. The question, however, is how powerful that effect will ultimately prove to be.

Still, the Memorandum of Understanding has important implications for global macro and the broader economic trajectory.

Memorandum of Understanding: Global Disinflation Ahead

Although many details of the Memorandum of Understanding remain unclear, Iranian and US representatives are expected to sign the agreement on Friday in Geneva, Switzerland. According to Bloomberg, the draft contains 14 points that both parties have already agreed upon.

One provision states that the US and Iran will negotiate a final agreement within a 60-day period, extendable by mutual consent. For markets, this may be more important than the unresolved details themselves. Investors are increasingly looking beyond the many aspects that remain undecided and focusing instead on the fact that there is now a visible path toward de-escalation.

If the leaked draft is accurate, the agreement contains several economic concessions to Iran. Allegedly, the US agreed to make frozen funds available to the Iranian central bank, issue a waiver on Iranian crude oil and petrochemical exports, and eventually lift sanctions.

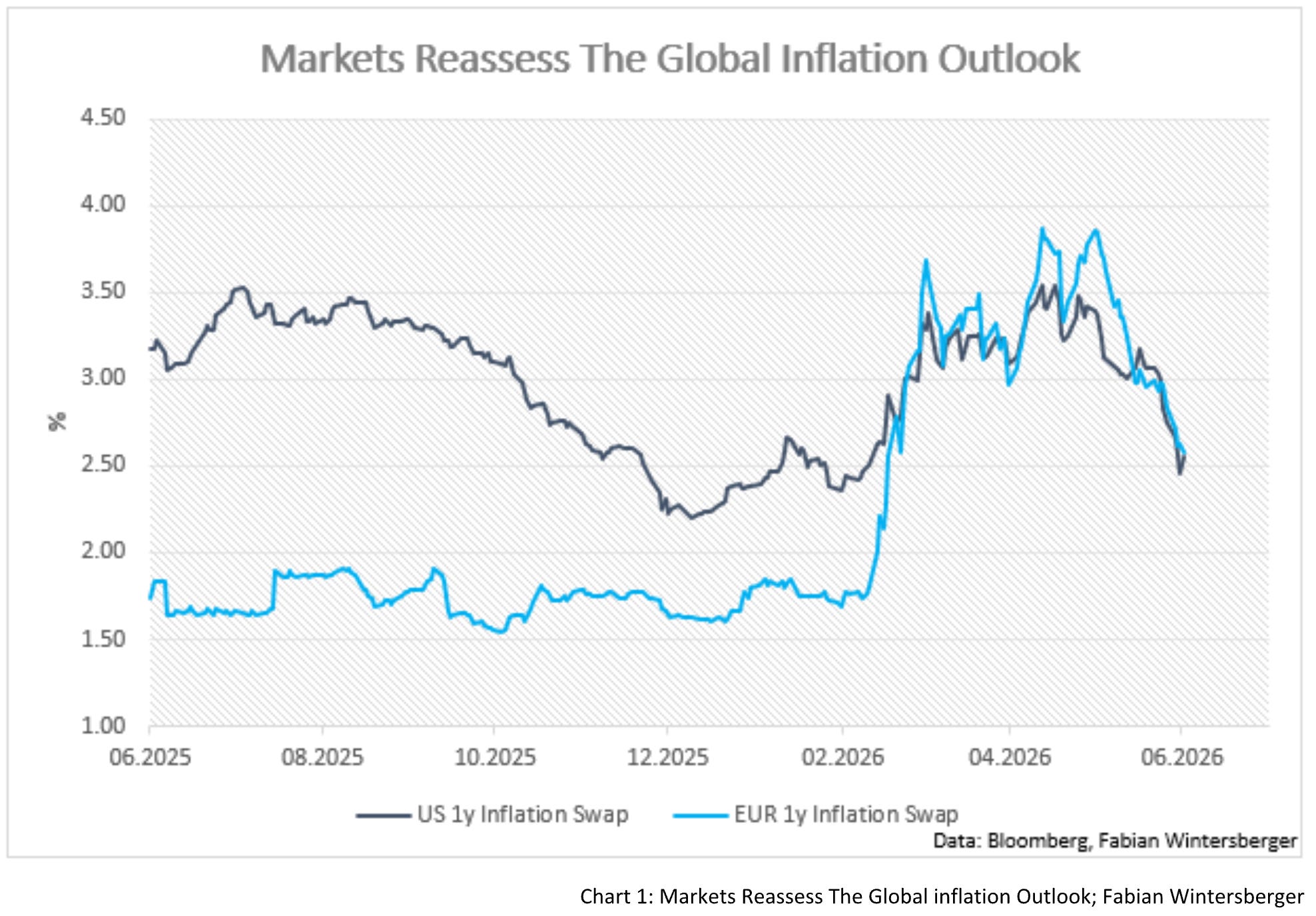

Regardless of the political implications, the economic implications are relatively straightforward. The agreement points toward an increase in global oil supply and therefore downward pressure on oil prices. Although some energy analysts still warn that global oil markets are not out of the woods yet, these developments are promising. Since the announcement, short-term inflation swap rates have moved sharply lower because of the expected disinflationary effects of a return to normal traffic through the Strait of Hormuz and an increase in global energy supply.

The drop in oil prices obviously benefits Asia and Europe more than the United States because both regions are net energy importers. Additionally, Europe does not experience the same degree of strong domestic demand as the US. As a result, the disinflationary impulse will likely be more pronounced in the Eurozone. Yet the euro failed to benefit substantially versus the dollar as markets started to increase the probability of a higher Fed Funds Rate.

Furthermore, the decline in inflation expectations led to a rise in real interest rates and thus a mild tightening of financial conditions. However, the effect appears too small to put meaningful pressure on financial asset prices. Overall, financial conditions remain accommodative and continue to support a further advance in equity markets.

Yet there is one development that deserves more attention. The latest IPO of SpaceX and the growing pipeline of companies preparing to go public point to a factor that could become increasingly important in the months ahead: equity issuance.

Equity Issuance As A Potential Danger For The Rally?

So far, the IPO of SpaceX has been extremely successful. After only five days on the market, the stock price has already increased by 42%, pointing to significant demand for the shares. However, what is notable is that although the S&P 500 moved higher, much of the increase was concentrated within the AI sector. Excluding AI-related companies, the index is actually down 1.12% since last Friday.

That indicates a rotation away from the broader market and into AI stocks. However, an increase in the total supply of equities needs to be accompanied by an equal increase in demand. If demand is not growing, prices elsewhere in the market would need to adjust lower. Since the pandemic, the increase in demand for equity issuance has primarily been driven by the rise in retail participation. Essentially, the latest rally in equity prices was largely carried by retail investors while institutional investors remained cautious and heavily hedged.

Due to the improving situation in the Middle East, those institutional investors are beginning to step back into the market and push prices higher. Can they absorb the growing pipeline of equity issuance in the medium to longer term?

That question is far from settled in my opinion. However, the increasing willingness of the Trump administration to take stakes in companies operating in areas linked to national security changes the calculation. Investors no longer need to assume that every strategically important company will be left entirely to market forces.

Whether through direct ownership, subsidies, guarantees or procurement contracts, the government is becoming an increasingly important source of demand for capital-intensive projects. The consequences are subtle but important. As the probability of government support rises, the perceived bankruptcy risk of strategically important businesses falls. That, in turn, lowers the risk premium investors demand and makes long-duration capital investments easier to finance.

Viewed through that lens, the extreme valuations of many companies may not make sense from a purely fundamental perspective, but they become easier to understand from a political one. Even if private capital flows slow, the US government has already shown that it stands ready to provide capital to strategically important industries. Markets are becoming increasingly aware of that reality. As a result, the rally may still have further room to run.

Market Assessment

The Memorandum of Understanding and the prospect of an eventual end to the conflict in the Middle East have shifted the global macroeconomic outlook. The decline in oil prices, or at least the expectation that energy prices will continue to normalize toward pre-crisis levels, introduces a meaningful disinflationary impulse into the global economy.

That should serve as a tailwind for both stocks and government bonds, potentially paving the way for further price gains. Because the recent pickup in US consumer prices appears to have been driven not only by energy but also by resilient demand, the upside for US Treasuries may ultimately be more limited than for European government bonds. Europe stands to benefit more from lower energy prices while facing less inflationary pressure from domestic demand.

At the same time, the widening gap in expected interest-rate paths between the United States and the Eurozone should continue to support the dollar versus the euro. EUR/USD is currently wrestling with the 1.16 level, and the combination of a stronger Fed outlook and a more pronounced disinflationary impulse in Europe points to the possibility of further downside in the currency pair.

Increasing expectations of tighter monetary policy also continue to exert pressure on tangible assets such as gold and Bitcoin in the short term. While both assets have already corrected from recent highs, another leg lower cannot be ruled out if markets continue to push back expectations for future rate cuts.

Overall, however, the dominant force remains the improvement in the global inflation outlook. As long as financial conditions remain broadly accommodative and economic activity holds up, the path of least resistance for risk assets appears to remain higher.

Conclusion

The global macroeconomic environment experienced a meaningful shift over the past week. With the agreement on a Memorandum of Understanding between the United States and Iran, inflation expectations declined significantly, suggesting that a short-term high in interest rates may already be behind us and that disinflationary forces are beginning to reassert themselves.

Simultaneously, Kevin Warsh appears determined to move the Federal Reserve away from the era of extensive forward guidance while placing greater emphasis on inflation than on labor-market conditions. Whether that ultimately results in a more hawkish Fed remains to be seen, but it is already clear that markets will have to rely more heavily on incoming data and less on central-bank guidance.

If the disinflationary force resulting from the Memorandum of Understanding outweighs the continuously strong demand in the US economy, the Fed might eventually find itself in a position to cut rates rather than raise them. In that scenario, policymakers may increasingly point to measures of underlying inflation that are less affected by short-term swings in energy prices.

Although that would lead to a further loosening of financial conditions that risks re-igniting another acceleration of inflation, it would also support asset prices, which are becoming increasingly important for the overall state of both the US and the global economy.

With the potential end of the conflict in the Middle East, the global macro landscape has found a reason for renewed optimism. For markets, it may be time to start over again and reassess many of the assumptions that dominated the last few months.

I gave it all, but you couldn’t get enough

Leaving with only memories of pain I can’t erase

You’re gone, I’ll never let this go

I would have given everything to start, to start it over againSaosin- Starting Over Again

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.