Stalemate

What the Federal Reserve does is provide the blood supply, for the body of our capitalist economy. And what happened in 2008 is, all, the veins and the capillaries and the arteries collapsed. So every financial function had failed. It had collapsed and we had to restore them...And then the question was, What else can we do? And the committee came up with the idea of quantitative easing. - Richard Fisher in Age of Easy Money

When Ben Bernanke assured the world that the Fed would use all possible measures to fight the economic crisis, he did not exaggerate. What followed was one of the most prominent interventions in financial markets throughout history, when the Fed bought massive amounts of mortgage-backed securities and US treasury bonds from banks and other financial institutions to revitalize lending.

Today, it is widely accepted that those extraordinary measures supposedly saved financial markets from a total implosion. QE and the resulting liquidity injection into financial markets helped the banking system to survive and improved economic data.

Nevertheless, nobody knew the long-term effects of QE on the whole economy. In a new Fortune documentary (Age of Easy Money), a former member of the Fed Board of Governors, Sarah Bloom Raskin, gives an excellent description:

You know, view it as, like, an experimental drug that actually is doing some good things, but nobody quite knows how or why at the moment.

Yet, Quantitative Easing did not cause the banks to increase lending. They used the new reserves to buy the bonds they had just sold to the Fed.

Why would I go through the effort "of making a mortgage, "when I can just press a button and buy, you know, "millions, if not billions, "dollars of, of bonds, and, and ride that trade, "as the price of those, those assets are very consciously being inflated by the Fed? - Andrew Huszar

Over time, some people worried that the Fed policies would sharply increase consumer prices. However, despite the Fed’s monetary expansion, consumer price inflation remained steady and hovered around 2 %, mostly slightly below. In 2019, Bloomberg Business Week titled, “Is inflation dead?”. Nobody thought inflation would be a big deal in the coming decade.

Now, in the second quarter of 2023, inflation is the most discussed topic on international financial markets. Central banks have increased interest rates fastest in 40 years, although they intended to leave them near zero until 2024.

As the last few weeks have been inflation weeks, I want to discuss European and US consumer price inflation numbers and discuss how inflation could evolve going forward.

Let us start with the eurozone. HICP was 6.9 % year-over-year, 1.6 percentage points lower than in February. The reason is the fall in energy prices, the only component within the HICP that fell year-over-year. Food prices continue to rise sharply by 15.5 %, and month-over-month increases show no sign of weakening price pressures.

Core inflation also accelerated and was 1.3 % higher than in February, or 5.7 % higher than the previous year. Spain has the lowest consumer price inflation (3.3 %), mainly due to strong government interventions in energy markets. Core inflation in Spain is 7.5%, and only slightly below Austrian core inflation (8.2%).

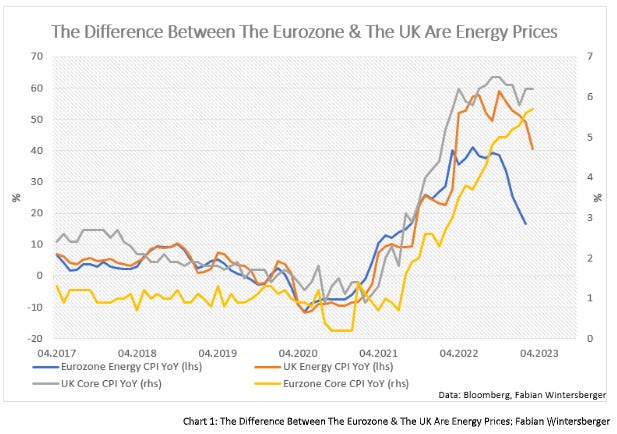

While Europe at least shows some cooling off of inflation, the situation in the UK remains tense. The latest inflation numbers showed that year-over-year inflation is still above 10 %, while core inflation is at similar levels to those in the eurozone.

The reason is energy price inflation, which is twofold as high in the UK as it is in the eurozone because the UK is particularly exposed to high gas prices: First, around 85% of households use gas boilers to heat their homes, and around 40% of electricity is generated in gas-fired power stations. Second, these are higher proportions than other European countries. Third, houses in the UK are poorly insulated compared to elsewhere on the continent. Recent analysis from the IMF showed that UK households have been the worst hit in Western Europe in terms of the impacts on spending power.

These numbers let one conclude that monetary policy needs to remain restrictive in both currency areas, the eurozone and the UK. While the ECB is eager to assure market participants that it will do everything necessary to bring inflation back down, the Bank of England did scale back on its rhetoric since the GILTs crisis. You probably remember statements like the terminal rate is lower than markets currently anticipate.

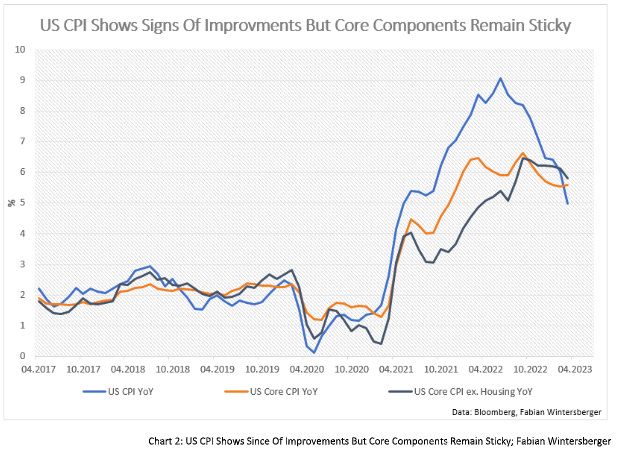

US inflation numbers show a significant weakening of consumer price inflation. Prices rose 0.1 % compared to the prior month, 5 % year-over-year (expected: 5.1 %), and annualized 3m inflation is 4 %. On the other hand, core inflation remains sticky and remains at 5.6 % year-over-year.

Like in Europe, the main component dragging CPI down is energy, which is 6.4 % lower year-over-year, although electricity rose 10.2 % over the same period. Transportation services are 13.9 % more expensive, and shelter inflation accelerated to 8.2 % year-over-year.

What will be the future path of consumer price inflation? There is a broad discussion going on at the moment. While some expect consumer price inflation to be a lot stickier than expected, others are calling for sharp disinflation in the coming months.

The Cleveland Fed’s 16 % Trimmed Mean and Median CPI show that inflation pressures have abated, and the trend is pointing lower. Therefore, one can expect continuously slowing consumer price inflation in the coming months.

Yet, the more important question is how fast consumer price inflation will slow. Shelter, lagging in the CPI (and accounts for 60 % of price increases in core inflation numbers), will fall in the coming months. In March, Median US asking rents were negative year-over-year for the first time since March 2020, which will feed through into CPI.

Another factor not supporting that is the latest rise in the Mannheim used vehicles value index, while official retail prices continued to decline. Currently, this is supporting lower CPI, although one should add that the item is only weighted 2.67 % in the CPI.

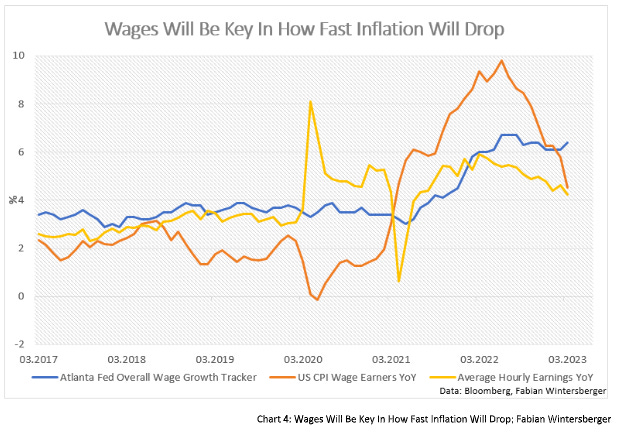

The main factor in answering the question of how inflation is moving forward is wages. While US CPI wage earners sharply declined from the top, other wage trackers do not reflect that. Especially the Atlanta Fed overall wage growth tracker points to continuing wage pressures.

A new study by Fed economist Michael Killey comes to a similar conclusion. Within his paper, he observed if using wage data can improve inflation forecasts, and he found that they are useful information to forecast the future path of CPI. However, the author also notes that it does not substantially increase forecast accuracy.

If wage growth remains high due to a lack of labor supply, increased wages will keep demand elevated compared to a situation with a higher supply of workers. Yet, the low unemployment rate does not point to a quick rise in worker supply in the near future at the moment.

Currently, US businesses that want to recruit new workers have to dig deep into their pockets. According to a survey by the NY Fed, the lowest wage for workers to accept a new job rose to 76,000 US dollars, up about 2,100 dollars from the survey in November 2022.

Therefore I do not expect consumer prices to drop significantly in the coming months. Unemployment is still deficient, and demand for goods and services is still too strong. Without a doubt, CPI will fall, if only because of the base effect. Still, Bank of America and JP Morgan pointed out that consumption in the US is still strong, which does not support the thesis that a recession is imminent.

If the trend continues, US CPI should settle somewhere between 3 and 4 %. Market participants are now starting to price out expected rate cuts, pushing the dollar higher.

Europe will also experience slowing consumer price inflation in the coming months. Similar to the US, it is the base effect that helps slow the rate of change. However, the situation in Europe is a bit more complex than in the US because of Europe’s decisive intervention in energy markets, which caused market distortions.

Monthly inflation rates are still high, core inflation rose 1.3 % month-over-month, and headline inflation was 0.9 %. Thus, as one can expect that HICP will slow down further, core consumer price inflation might continue to accelerate. In my opinion, if the ECB really wants to fight inflation, a rate hike of 50bps should be unquestionable.

Nevertheless, another 50bps increase is highly controversial within the governing council and far from being a done deal. Goldman Sachs and most economists expect only a 25 bps rate hike in May, followed by two more and a terminal rate of 3.75 %.

If consumer price inflation remains stickier than expected in the coming months, it seems not so far-fetched that the ECB probably would have to raise interest rates above 4 %. Germany switched off the remaining nuclear power plants, which will probably elevate electricity prices, just like Eon announced for Northrhein Westphalia.

Another point could be expansionary fiscal policies from European governments. Again the ECB has pointed out that fiscal policy is pushing inflation rates up. However, one should add that the ECB is also playing a role here because it manages government bond spreads with its PEPP reinvestments, which supports expansionary fiscal policies.

As a result, it is likely that the ECB (and the same is true for the BoE) probably has to act more restrictive and tighten financial conditions more, which might be a problem for the zombie companies in the eurozone (about 7.5 %).

Interestingly, the share of zombie companies has been cut in half since 2020, assumingly because of the extensive government handouts to businesses. This shifted the debt burden away from businesses to the state.

Government debt also is widely discussed in the United States because the country will reach its debt limit soon. As tax revenues were surprisingly weak, the debt limit may be reached sooner, in the first half of June.

In both cases, this could lead to rising long-term interest rates. However, at the moment, equity markets do not seem to bother. Respectively, they interpret bad and good news as good news for stocks. But the more restrictive monetary policy becomes or remains, the more trouble it means for equities.

Currently, European government debt levels are not the focus of market participants. On the contrary, the latest turbulence of US regional banks has supported the assumptions of many that the coming recession will start in the US.

Yet, I would like to remind you to think back to the Great Finacial Crisis, where back-then French finance minister Christine Lagarde said that the turmoil in the banking sector was an American problem and European banks were in good shape.

We all know what happened afterward. The EU had to bring enormous fiscal packages on the way to bail out the banks. The problem transferred from banks to nations, and when markets started to focus on government debt levels, the turmoil that followed led to social unrest throughout Europe.

As we all know, recessions happen suddenly and unexpectedly. Even if economic data is not pointing to a severe recession, downward revisions or a sudden worsening of the economic environment can never be ruled out, especially not in times of high uncertainty.

One can assume a sharp drop in consumer price inflation if the recession happens sooner than expected. However, central banks will react by cutting interest rates, and nations will increase fiscal spending. As a result, the disinflationary impulse will be short-lived and only mark the beginning of the coming inflation wave.

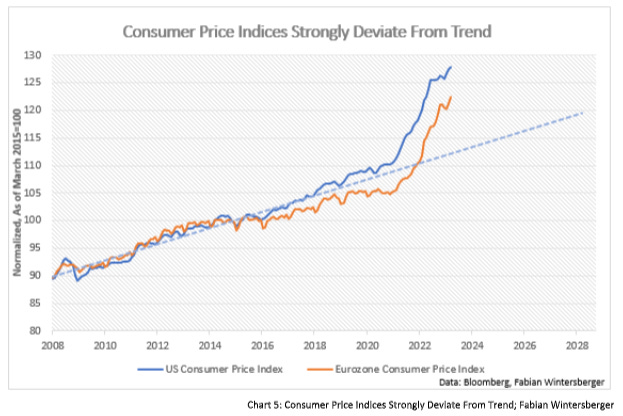

But even a deflationary shock will not bring consumer prices to their long-term trend. Since 2020, there has been a substantial deviation from it. To get consumer prices back down to their long-term trend, prices would need to remain constant for the rest of the decade.

And I say (now gimme your best shot)

Wait a lifetime to pull it off

And I say (is that all that you’ve got?)

Wake up in no time in blow it off…Soilwork - Stalemate

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! If you like my writing, you can subscribe and get every post directly into your inbox. Also, sharing it on social media or liking the position would be fantastic!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice)