Salvation

Art D. Cashin Junior is a veteran of Wall Street. The current Managing Director of UBS Financial Services Inc. started his career in 1959 when he was 19. Aged 23, he became a member of the New York Stock Exchange when he became a partner of Herzig & Co. If you know that about Cashin, you probably can imagine that he experienced a lot of turbulence in financial markets.

And probably he had a deja-vu this week when news broke out about a missile that hit Polish soil near the Ukrainian border. Associated Press soon came out with another bummer, quoting a senior US intelligence official that a Russian rocket killed two people.

As the situation was presented, everyone assumed that this would lead to another level of escalation and that NATO’s Article 5 would come into motion because that would have been an attack against a NATO member state. The stock market lost all its gains after the news broke out and took a nosedive.

However, let me come back to Cashin. There was a very interesting anecdote of him from the Cuba-Crisis when there was a rumor that the Russians had launched rockets, which caused the stock market to make a similar nosedive as this week. Barry Ritholtz quotes Cashin in a blog post from 2017, where he (young Cashin) is talking to veteran trader Jack Moosehead:

I cleaned up my desk and raced to the Moosehead, as animated as only an 18 year-old can be. Jack was already there and as I burst through the door, I shouted: “Jack! Jack, there was a strong rumor that the missiles were flying and I tried to sell the market but failed.”

Jack said “Calm down kid! First buy me a drink and then sit down and listen to me.” I ordered the drink and meekly sat down.

Jack said – “Look kid, if you hear the missiles are flying, you buy them. You don’t sell them.”

“You buy them?” I said, somewhat puzzled.

“Sure you buy them!” said Jack. “Cause if you’re wrong, the trade will never clear. We’ll all be dead.”

That’s a lesson you won’t learn in the Wharton School.

While the big rally did not happen after it was clear that all the evidence was inaccurate and that a Ukrainian anti-aircraft missile crashed in Poland, the rationale for Moosehead’s advice is obvious: You bet on salvation and against the end of the world.

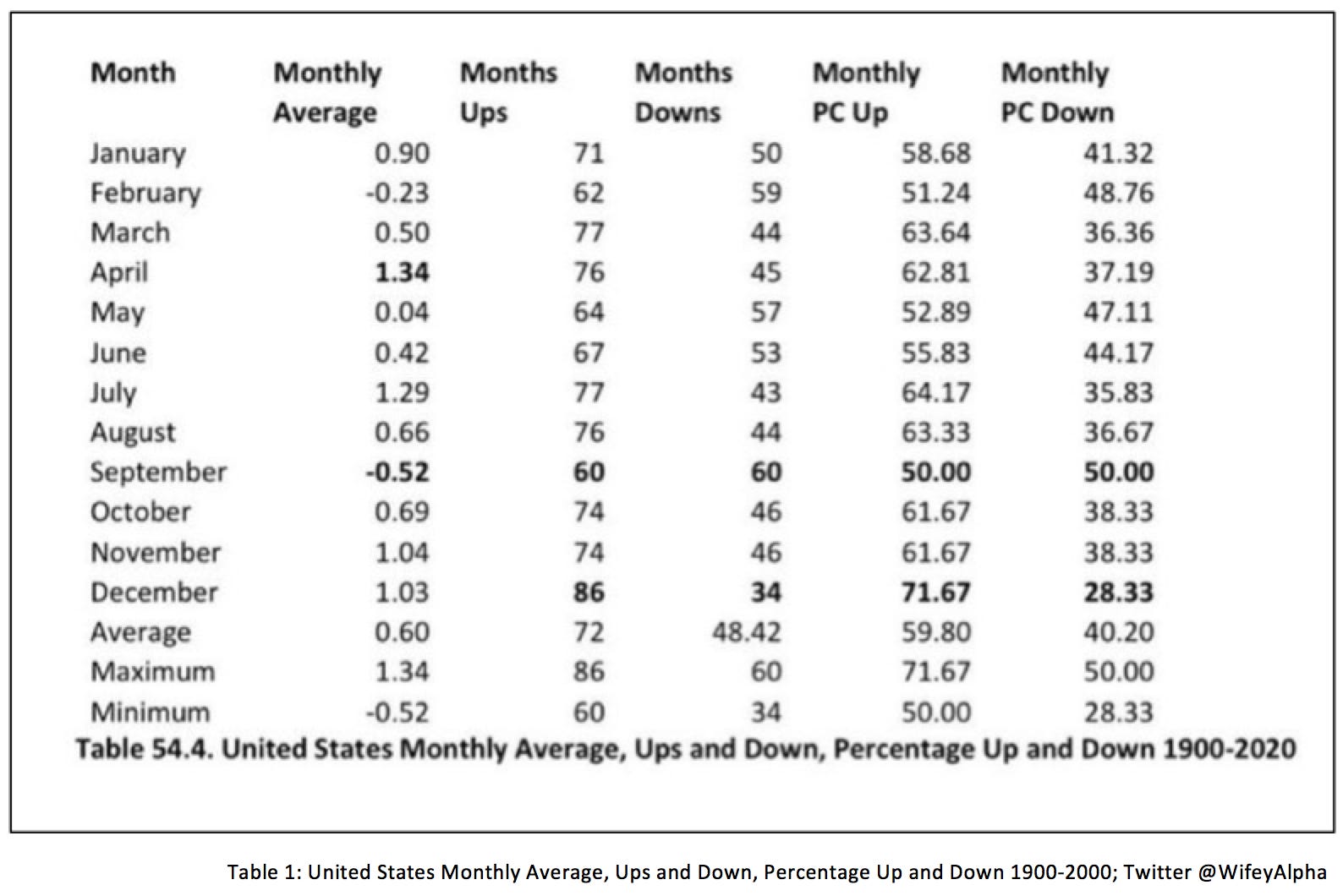

Although today’s text does not deal with the incident, I chose to use it to tell the anecdote because I wanted to write about salvation. I wrote two weeks ago that October was a good month for stocks, and so far, November has been so too. European and US stock markets are again up, and everyone hopes for a strong year-end rally.

Is this salvation for the stock market? Is that the end of the bear market? I would be cautious, although seasonality supports the assumption that we will see a rally until new years eve. Looking back in history, around 2/3rds of November and December since the beginning of the 20th Century were positive for stocks. It is a good argument that it is a corrective rally, at least in the current bear market.

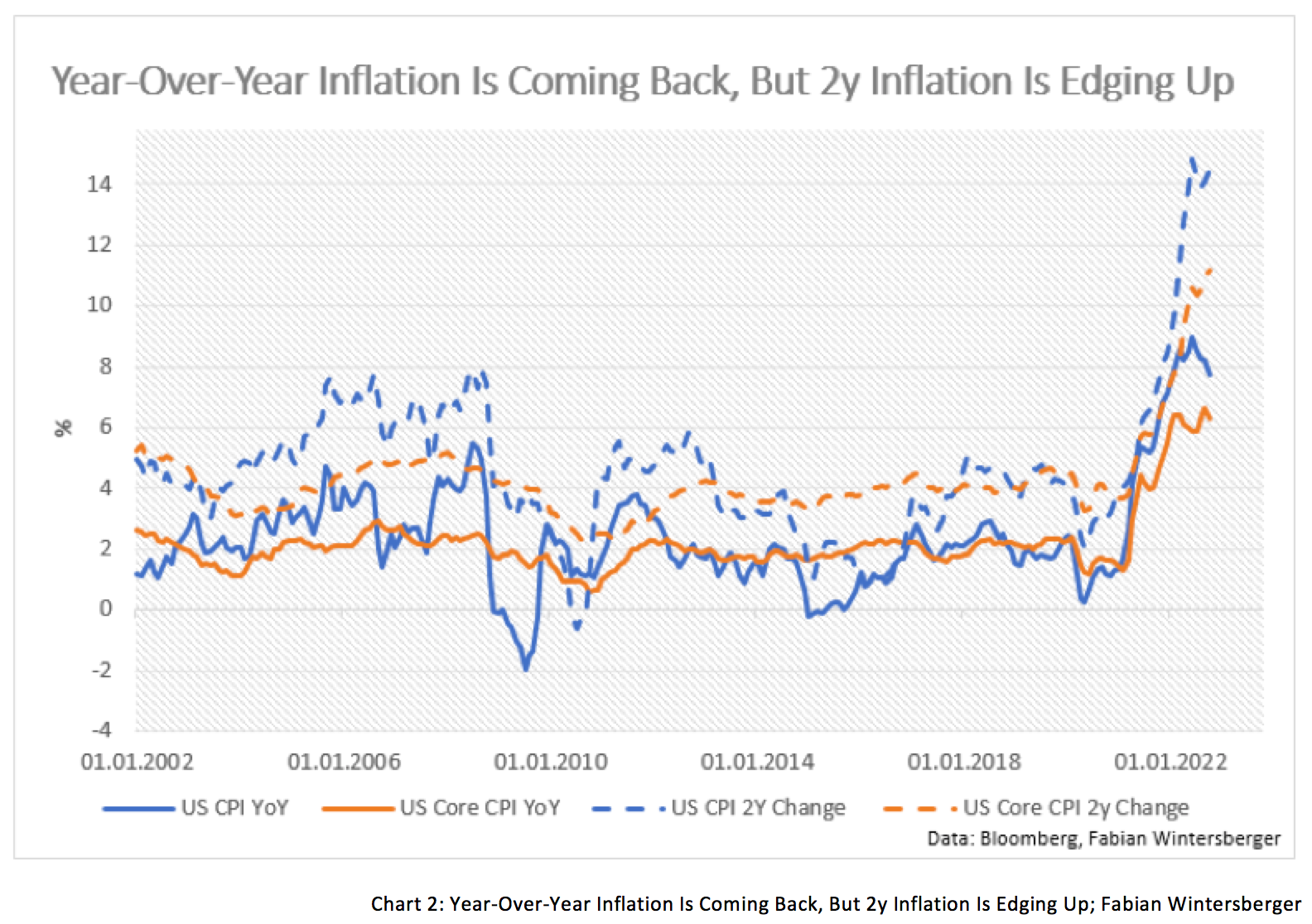

Last week, weaker-than-expected US inflation data from October led to calls for triumph among equity investors. Year-over-year inflation was 7.7 %, 0.2 percentage points below expectations; core inflation was 6.3 % instead of the expected 6.5 %.

Yeah, the Fed is going to pivot. We are winning!! What a market reaction. US 10y yields fell 30 basis points, and the stock market rallied. The S&P 500 rose 5 % that day. The US yield curve inverted further as market participants now think that the Fed will not keep rates high for long.

Are these CPI figures salvation? Is that the salvation market participants hope for since they misinterpreted Jerome Powell’s speech in June as dovish? While Year-over-Year inflation in the US has peaked, one should remember that it is mainly because of the base effect. Further, the lower-than-expected CPI measure can be traced back to an adjustment in healthcare cost measurement. The picture is slightly different if one looks at the 2y change of inflation, and 2-year changing inflation is reaccelerating.

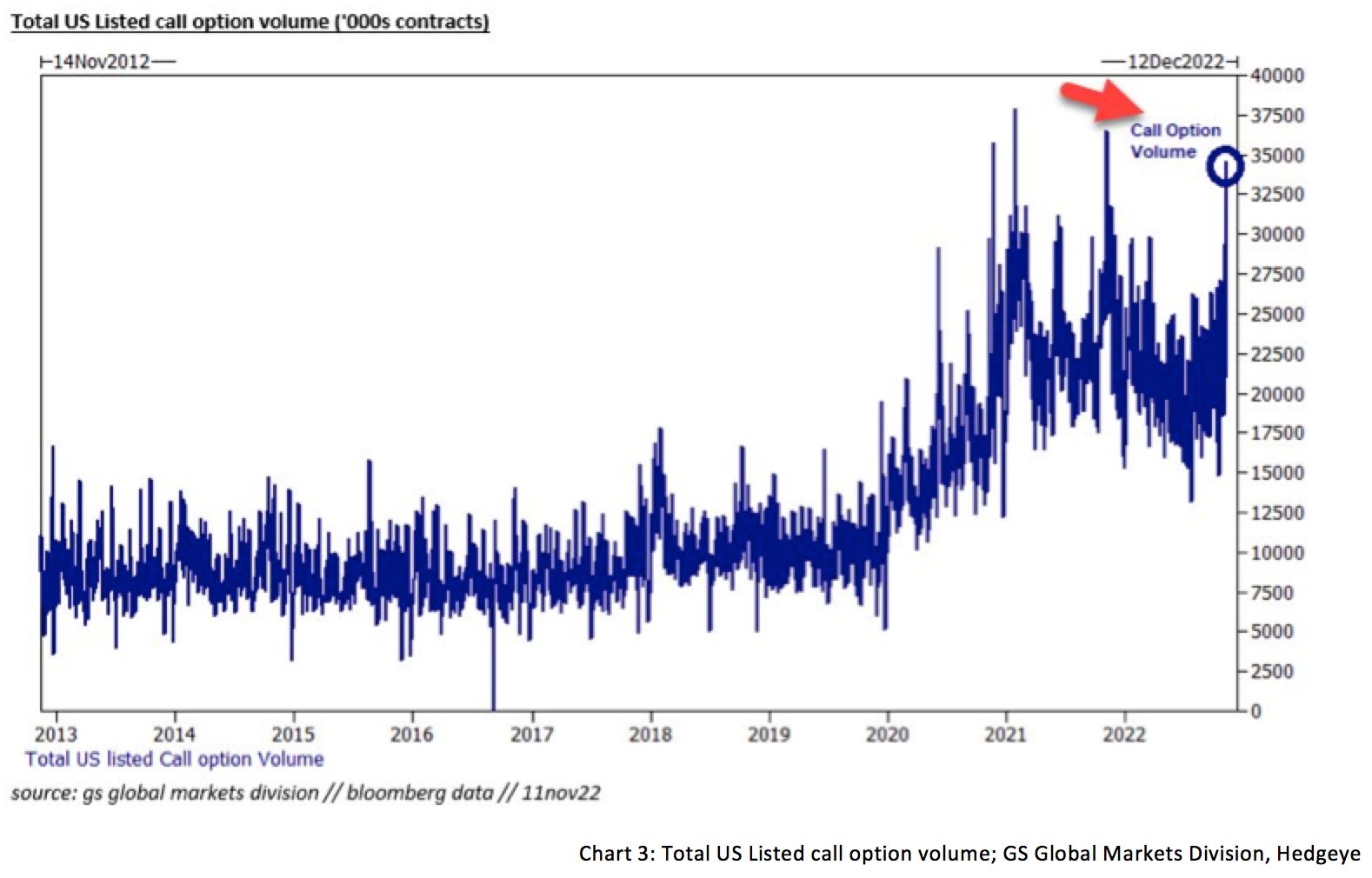

I am unsure if those who forecast a coming melt-up in stocks will be proven right. The argument that everyone is bearish and, therefore, one has to be bullish is not supported by call-option volume, at least. If everyone is bearish, people are not positioned that way.

The salvation market participants are hoping for is more-or-less a Fed pivot, or more specifically, a sooner-than-expected pivot. However, as I wrote last week, a pivot is not the turning point for the stock market; it is the end of the easing cycle.

During the last months, Fed officials (Jerome Powell and others) again clarified that they wanted tighter financial conditions. However, since the latest published US CPI, financial conditions have eased again, which is not what the Fed wants to see.

Additionally, the US labor market remains very tight. Currently, unemployment is at a historic low (3.7 %). Businesses compete for a tight labor supply, resulting in higher wage rates. The Fed fears this might lead to more inflation in consumer prices, a wage-price spiral. Kansas City Fed chief, Esther George, said this week that to bring inflation down, the Fed needs to slow down economic activity.

However, this week’s released US retail sales also beat expectations and thus do not support a Fed pivot either. The salvation the bulls hope for will not happen at the next FOMC meeting in December. One can easily assume that interest rates will remain higher for longer, and a statement from Patrick Harker (Philadelphia Fed) from this week confirms this. Apart from that, consumer inflation expectations are rising again as well, as a report from the New York Fed shows.

One waits for salvation, not only in the United States. China, the driving engine of the world economy, has stuttered since the pandemic began in 2020. The reason is China’s zero-covid policy which led to a sharp decline in economic activity. The country suffers from a popping housing bubble that puts pressure on Chinese property developers, despite more and more frequent verbal intervention from the Peoples Bank of China to calm down markets. At some points, words must be followed by deeds.

Especially domestic consumption is very weak in China, and retail sales have stagnated since December 2019, another result of China’s zero-covid policy. Further, weak demand from China contributed to the fact that commodity prices remained dampened and fell in recent weeks despite the multiple crises we are in.

Last week, rumors broke out that China is eventually considering ending its zero-covid approach. That led to a rally in the Hang-Seng Index and commodity prices, as China is the world’s biggest importer of commodities.

Despite all hopes, there is no end in sight for China’s approach to slow the spread. Bloomberg reports that Goldman Sachs and UBS expect China to end its zero-covid policy no sooner than in the second quarter of 2023. If that is accurate, economic activity in China will not recover for the next several months.

Therfore, one can assume that this has implications for the price development of commodities, especially metals and energy. As long as the most prominent commodity importer is producing below capacity, this means a headwind for commodity prices.

So, Europe's headwind for energy and commodity prices is only helping a little bit. Although prices have come down sharply from the summer highs, consumer prices know only one direction on the continent: upwards. Energy prices are much higher than before the war. Political measures such as windfall profit taxes only support prices because it raises costs for energy producers and possibly lowers supply. If governments put price caps in motion, inflation gets tamed on the surface at the expense of supply shortages. As soon as those caps are lifted, prices will continue to rise—no salvation for European consumers.

Warm temperatures help Europe on the energy front because it needs less energy for heating. In Germany, gas storage is now 100 % full, as Bundesnetzagentur reported this week. Yet, another storm seems to be brewing under the surface, as rising diesel prices might become a problem soon. Before the crisis, Europe imported most of its diesel from Russian refineries, and only a tiny portion was produced domestically, mostly with Russian oil. With the end of winter and the coming embargo against Russian oil, the situation in Europe might get more severe again.

At least the sell-off of the British pound and the euro has halted, and the rise in the exchange rates against the dollar relaxed the inflation pressures from the currency side a bit. The euro is above parity again, and the GBP is at 1.17. The reason could be found in the lower-than-expected US CPI numbers.

The hope for salvation, a Fed pause, and the BoE and the ECB continuing to raise rates to fight inflation means that market participants expect that both central banks will tighten monetary policy (they continue to raise rates). At the same time, the Fed will slow the pace.

However, I would be skeptical about that because of two reasons. Firstly, I think the hope of market participants for a pivot or a pause at a lower-than-expected rate is still premature. Secondly, I would be very cautious about assuming that the European central banks (ECB & BoE) can follow through on their tightening paths until inflation is under control. Remember, the ECB still believes that in an environment where inflation is above 10 %, 2 % is still the neutral level.

As a result, I consider the latest dollar correction as a sign of coming dollar weakness. On the contrary, a weaker dollar raises import prices for the US and could fuel inflation, leading to a more active and aggressive Fed again.

As one sees, the hope for real salvation seems farther away than some market participants might wish. That is true for Asia, Europe, and the United States. Seasonality might seed some hope over the short term and should support equity and bond markets because there is a positive correlation when 3-year annualized inflation is above 3 %.

Endless nights filled with misery, sick of familiar patterns,

Bruise after cut, can’t wash away my scars

This is the night of salvation, on the night of salvationChimaira - Salvation

Yet, everyone should remember that the hope for salvation, for a savior, often leads to more bad than good. The latest example is the case of FTX and Sam Bankman-Fried. As the title this week is salvation, it is hard to end the Weekly Wintersberger without at least commenting shortly on it.

SBF, who started as an altruist, as a philanthropic capitalist who wanted to use his money for the well-being of humanity, now ends up as someone who deceived investors and stole deposits from his clients.

As far as I can evaluate, SBF was seen as someone who might end the Wild West in the crypto space and transform the sector into calmer waters. However, as it turns out, his striving for regulation and his lobbying efforts in DC mainly aimed to cover up the (alleged) fraud that he and his business were. Thus, I think it is a mistake if one wants to say that this is a crypto scam. In reality, it is just a Ponzi scheme fraud with a crypto wrapper, as Marc Cohodes said.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice)