Rational Eyes

Policy, Markets, and the Price of Misdiagnosing Reality

Finally, a week in markets that was not overshadowed by geopolitical turmoil — at least relative to recent weeks. That said, there was still plenty to digest across financial markets and the broader economy. We received a range of economic data from both Europe and the U.S., and the Federal Open Market Committee met to announce its decision on the federal funds rate.

Powell Is Still Fighting, But Opening Door For Future Cuts

Unsurprisingly — and already priced into markets — the Federal Reserve left interest rates unchanged on Wednesday. In his opening statement, Chair Powell said the U.S. economy is entering 2026 on a solid footing: growth remains firm, consumers are resilient, and business investment continues to expand, even as the Fed acknowledges ongoing weakness in housing.

On inflation, Powell struck a notably conditional tone. He pointed out that there has been no net progress over the past twelve months, arguing that this was largely due to tariff-driven price increases for goods. Crucially, he framed this as a one-time price-level shift rather than persistent inflation — a distinction that provides a clear justification for potential future rate cuts.

He also played down concerns about the labor market, suggesting the data show signs of stabilization. According to Powell, the labor market appears to have found a new equilibrium — partly due to frozen immigration — in which zero job growth does not necessarily imply recessionary conditions.

Other remarks were equally telling. Powell refused to comment on the recent dollar weakness, reiterated that the U.S. debt path remains unsustainable, downplayed the gold rally as a signal of lost credibility, and strongly defended Fed independence, warning that once credibility is lost, it is difficult to restore.

The most important takeaway from the press conference was the Fed’s willingness to open the door to future rate cuts. However, as long as Powell remains chair, the two dissenters from Wednesday’s decision — Stephen Miran and Christopher Waller — are unlikely to succeed in pushing for deeper easing. In my view, Powell’s stance appears considerably more balanced than that of Miran and Waller.

New Fed Chair? - The Fateful Economics Of Rick Rieder

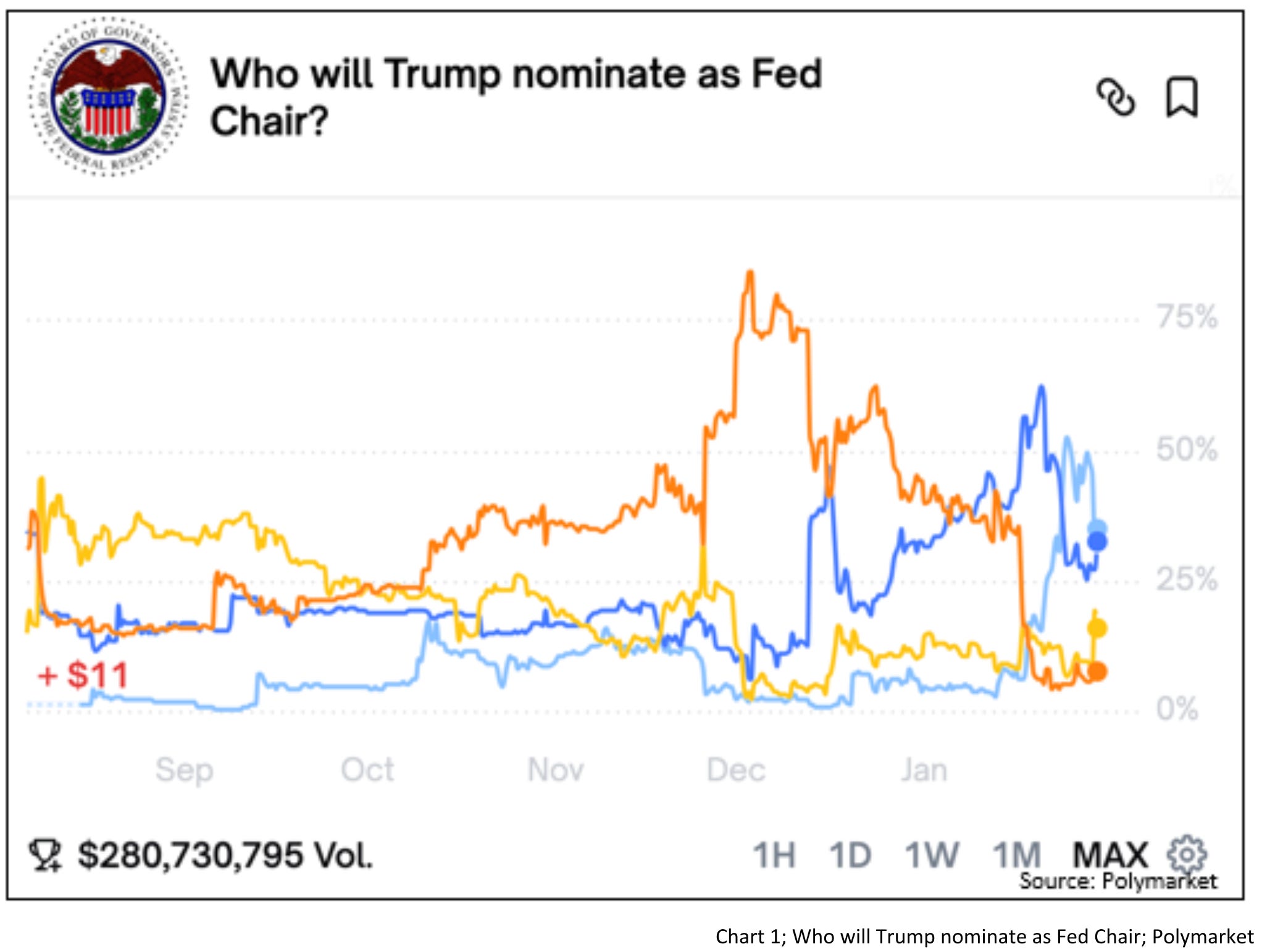

The race for the next Fed chair remains wide open, according to prediction markets. While President Donald Trump has offered few concrete signals — even at Davos — betting odds have shifted meaningfully in recent weeks. Data from Polymarket show former frontrunner Kevin Warsh losing ground to Rick Rieder, chief investment officer of global fixed income at BlackRock. As Rieder remains largely unknown outside financial markets, his economic views warrant closer examination.

Rieder’s approach differs sharply from the Fed’s traditional model-driven framework. He favors real-time, bottom-up signals over abstract forecasting models. As Axios reported, in a January 9 note on jobs data, he argued that a productivity surge is dampening labor demand — leaving the job market weaker than headline figures suggest.

Some of Rieder’s statements help explain why he may be emerging as a favored candidate. In a CNBC interview, he argued the Fed has room to lower the federal funds rate by as much as 100 basis points, pointing to benefits for housing and debt service, while acknowledging that lower rates would reduce interest income for savers. He also stressed that high rates can exacerbate inflation by raising financing costs across the economy — from housing to government borrowing — a warning that tightening can backfire when inflation is cost-driven rather than demand-led.

Rieder has also argued that the Fed should rely on a broader toolkit than the policy rate alone. Beyond rates, he points to balance-sheet policy (QT/QE), forward guidance, and financial conditions management through liquidity and regulatory tools that target stress points directly rather than suppressing the entire economy. In essence, his framework calls for diagnosis before dosage: use rates when demand is overheating, but rely more heavily on targeted instruments when inflation stems from supply constraints—preserving credibility while avoiding self-inflicted inflation.

Against that backdrop, it becomes clearer why Trump recently hinted that the next Fed chair may need to “think differently” about rates and growth — and why markets are increasingly pricing Rieder as more than just an outsider.

To sum up, Rieder personifies many of Trump’s stated preferences: lower rates, lower housing costs, and a Fed chair more aligned with the administration’s growth priorities. Yet in substance, Rieder is not proposing a radical break with mainstream macroeconomic thinking. His arguments echo strands that have long been present in New Keynesian and post-crisis policy debates: that high interest rates are a blunt and often ineffective tool when inflation is not demand-driven, and that monetary policy should be calibrated carefully to avoid amplifying cost pressures or destabilizing the real economy.

In practical terms, this would imply a bias toward easier financial conditions—supportive of asset prices and favorable to government financing—even as inflation remains above target. Whether Rieder ultimately prevails remains uncertain, particularly as betting odds have recently narrowed again. But his rise underscores a broader shift: markets increasingly expect a Fed leadership more tolerant of running the economy hot, more attentive to financial conditions, and less inclined to lean aggressively against inflation with rate hikes alone.

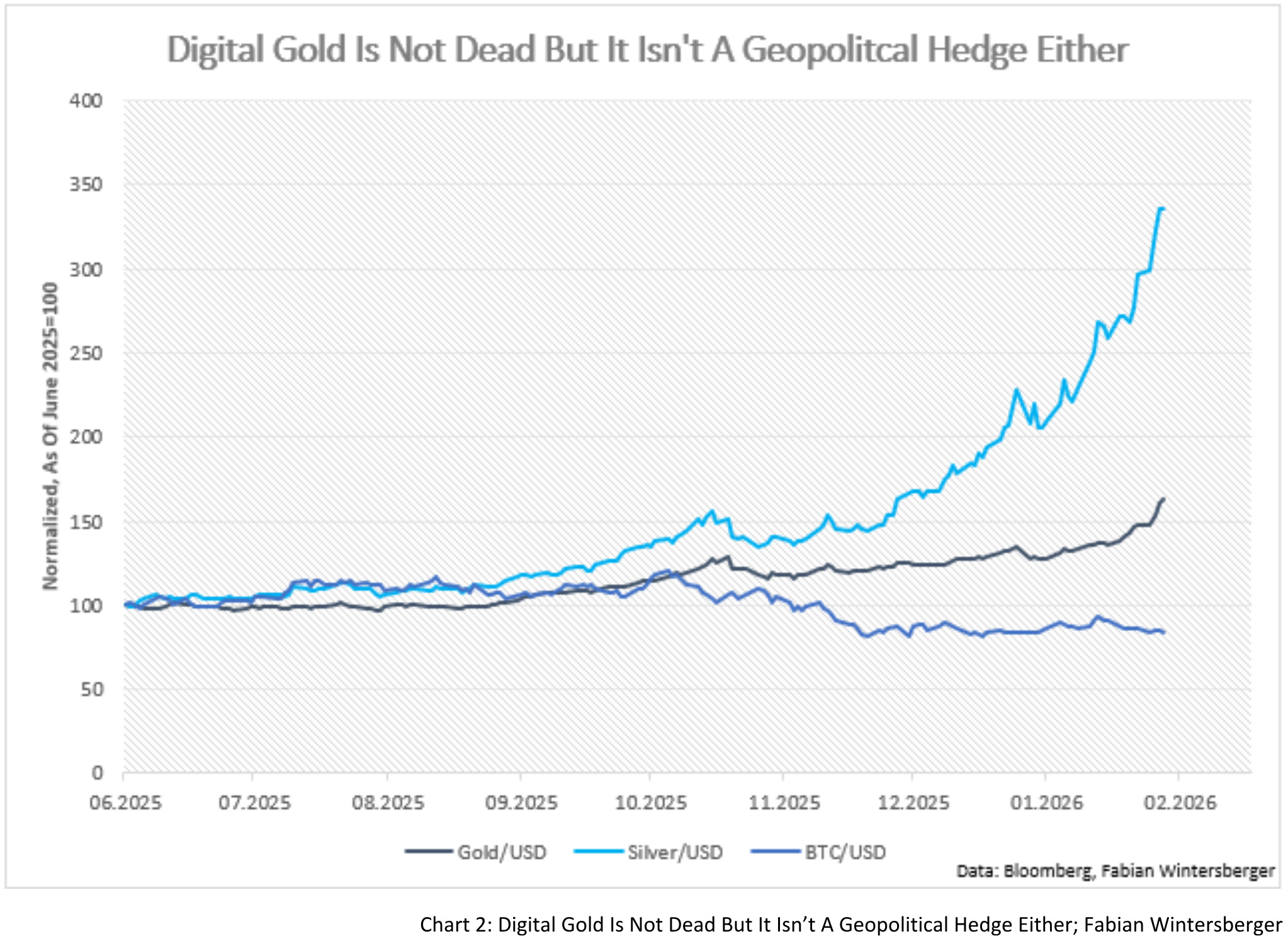

Gold & Silver Rally, But The Debasement Narrative Is Lacking Proof: What About Bitcoin?

Both claims rest on weak foundations. As argued last week, the dominant driver of current market behavior is geopolitical uncertainty, not monetary debasement. In such environments, investors reallocate the safe portion of their portfolios away from assets such as government bonds toward alternatives they perceive as stable and time-tested. Gold and silver have demonstrated resilience over centuries of political stress.

Bitcoin does not — not yet. Since its inception, geopolitics has not been the primary macro driver; instead, Bitcoin thrived as a speculative hedge against negative real rates and monetary experimentation. That history explains both its long-term appreciation and its failure to function as a crisis hedge today. Bitcoin isn’t dead — it’s simply not the asset investors reach for when uncertainty, rather than inflation, dominates.

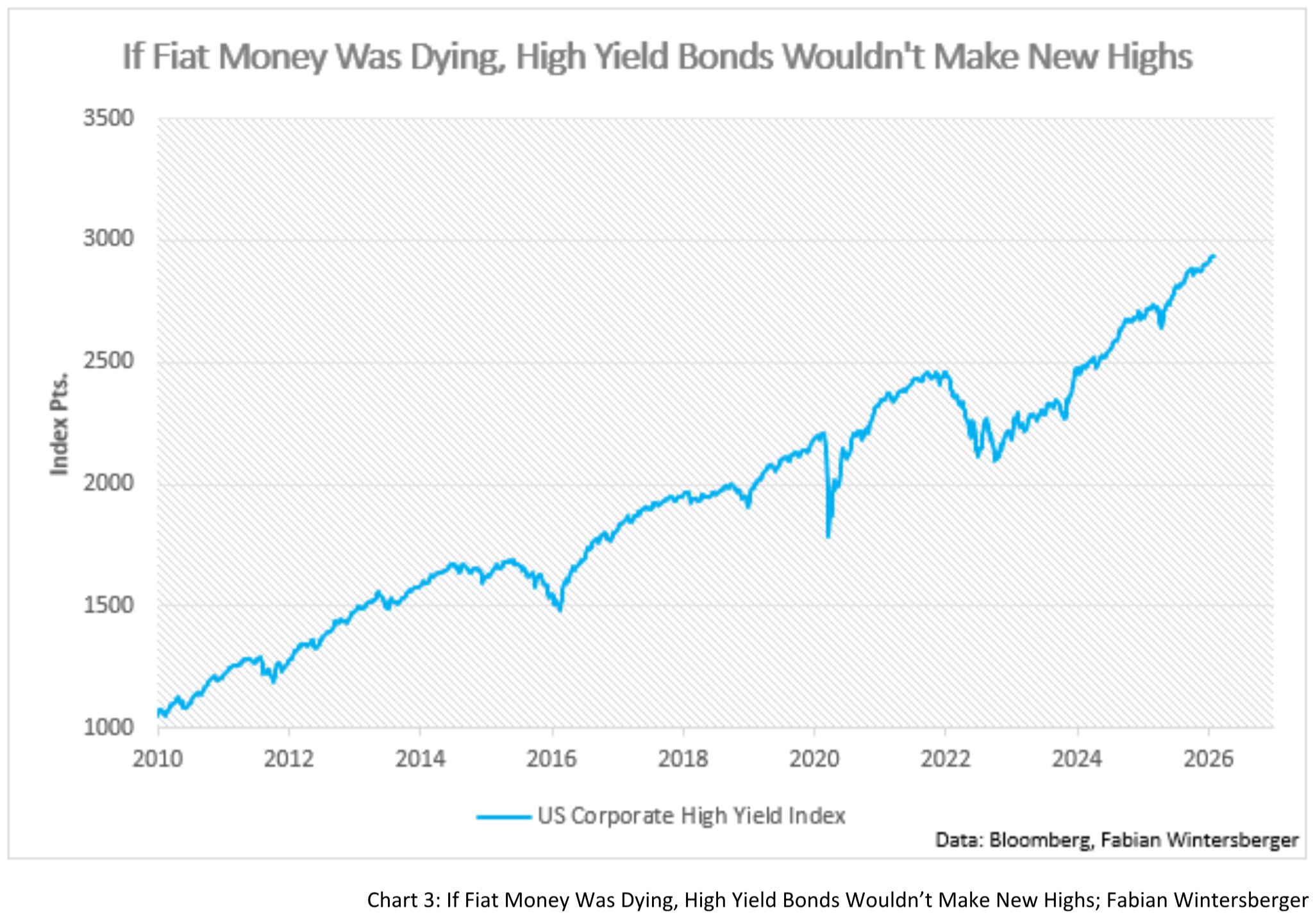

The claim that the rally signals the death of fiat collapses even faster. A glance at investment-grade bond prices immediately contradicts it. If confidence in currency were breaking down, capital would be fleeing fixed income in favor of equities, commodities, or tangible assets. Instead, demand for high yield bonds is rising, pushing prices higher. That is not a rejection of fiat — it is renewed demand for it. Precious metals may be rallying, but the bond market makes clear that this is about risk aversion, not currency debasement.

Germany & Europe: Still Unable To Kickstart Its Economy

Recent PMI data have revived hopes that Germany’s economy is finally gaining traction, aided by the prospect of increased fiscal spending. December’s composite PMI and the stronger January readings encouraged commentators to argue that Germany — and by extension Europe — may be emerging from stagnation.

A more cautious reading, however, is warranted. The latest Ifo Institute survey quickly tempered that optimism. Business Climate, Current Assessment, and Expectations all fell short of expectations, with indicators either stagnating or declining month over month. High-frequency data tell a similar story: construction capacity utilization has dropped sharply, pointing to further weakness in output; services remain soft; and trucking data show no convincing uptrend in industrial activity. Weather effects may explain some noise, but the data do not support a rapid rebound narrative.

Nor does the fiscal story provide much reassurance. As Oxford Economics’s Oliver Rakau noted, actual government investment has fallen roughly 25% short of planned levels, undermining hopes for a meaningful fiscal multiplier. Taken together, the evidence points toward a disappointing first quarter rather than upside GDP surprises. The problem is not a lack of available capital, but a policy environment that makes investment prohibitively expensive through regulation and taxation. Injecting more money into such a system risks producing more frustration rather than more growth.

Now, let us move beyond the news and turn to the implications for price dynamics in financial markets.

Bonds & Interest Rates

Price action in the bond market remains unspectacular. Volatility is down and shows no indication of a price jump or a drop. Essentially, I’m holding onto my view that interest rates might have further room to run up, albeit slowly and steadily rather than abruptly. Current expectations for future monetary policy remain pretty consistent with the market picture. The economic outlook for the US remains stable, suggesting an acceleration in economic activity, while European government debt spending also supports the view that yields will remain elevated.

Stocks

European stocks have diverged a little bit from US stocks recently, due to the weakening dollar, which supports dollar assets (in dollar terms) while the stronger euro serves as a drag for European stocks. However, the bullish price picture still remains intact, and the economic environment of increased spending points in the same direction. Therefore, stocks should still be favored compared to bonds.

FX

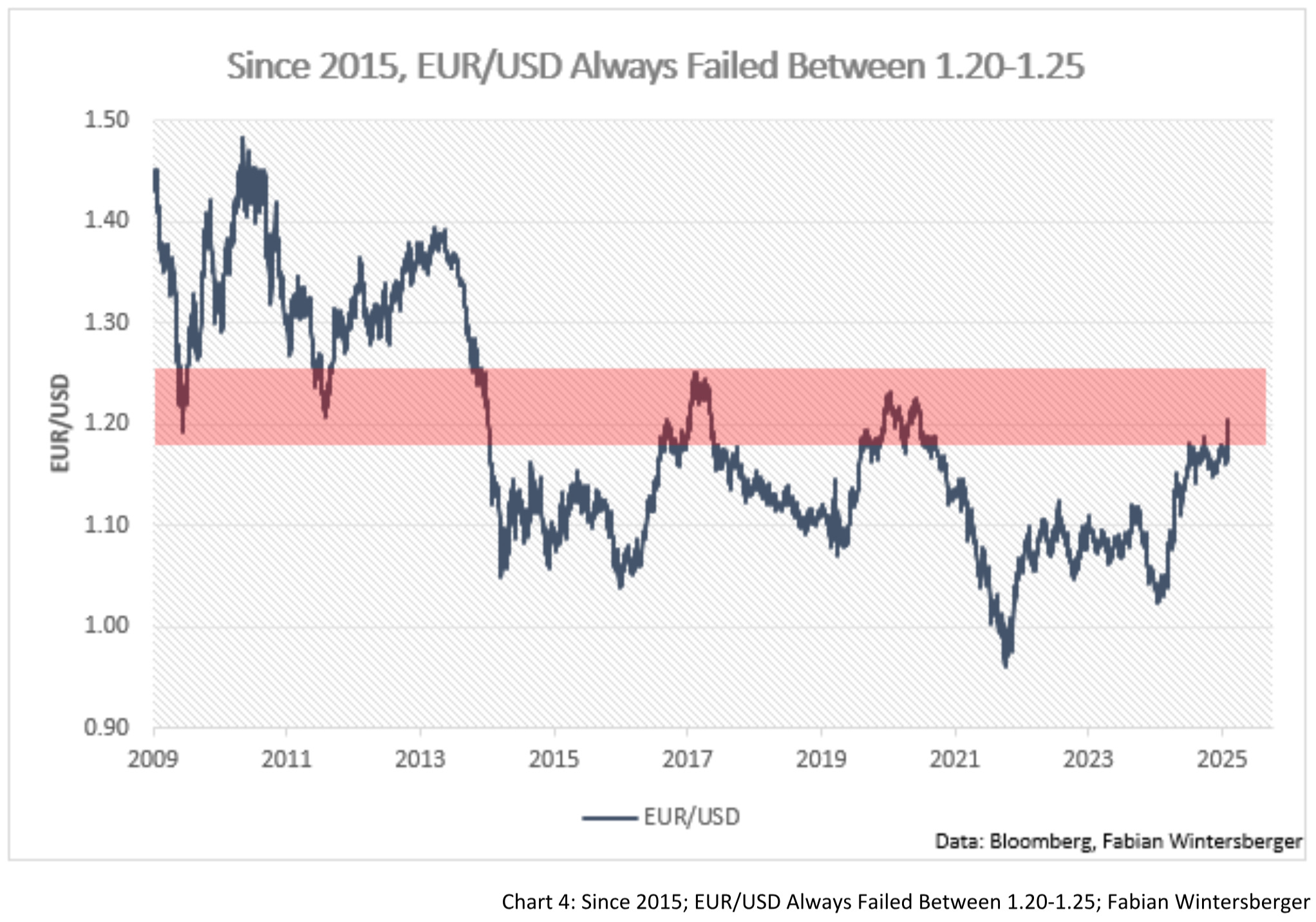

The major move this week occurred in the foreign exchange market, as the dollar continued to depreciate against its major peers. The Swiss franc has also benefited from geopolitical uncertainty and has appreciated 3% against the dollar since January 1. EUR/USD climbed to 1.20 briefly, but went back below after the FOMC.

Sentiment is heavily bearish on the dollar at the moment, and if one also considers the broad discussion of the “debasement trade,” then it could indicate that the dollar decline is nearing its end. That doesn’t mean that it won’t fall further, but at least in EUR/USD, the chart picture suggests that 1.20-1.25 is a broad resistance area where the dollar weakness always turned into future dollar strengthened since 2015.

Overall Assessment & Conclusion

After the geopolitical turmoil, it seems the market has weathered these stormy waters until Trump comes up with his next idea. But in financial markets, these events usually turn out to be a distraction from what really matters anyway. So far, as this week has been geopolitically calm, it has been a good time to observe the market through “rational eyes.”

What comes out is not surprising to me, and so far, close to my expectations for the year. Bonds are still no buy, stocks are still in a bull market, and the dollar has switched from sideways to slightly lower. The only surprise – and arguably most affected by geopolitics – was the continuously strong demand for precious metals. But with the assumption of a dovish new Fed chair, a Trump administration that wants to run it hot, and Europe trying to spend its way out of stagnation, the picture seems to favor those who buy assets instead of holding currency.

I can see this world is all alone

I won’t be a victim

I can feel the end of all I′ve known

I won’t be a victimThreat Signal - Rational Eyes

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.