Paralyzed

For the vacationers on the Thai holiday island of Khao Lak, the early morning of December 26th starts like any other day. The sky is blue, the sun is shining, and the sea is blue. Everyone is looking forward to another extraordinary Christmas holiday in paradise.

However, ten thousand kilometers away, the Pacific Tsunami Warning Center in Hawaii registers an earthquake in the Indian Ocean, one of the strongest ever measured. The scientists there know they need to warn someone, but they do not know whom, so they do not. The only others who take notice of the earthquake are the people of Sumatra, but it is already impossible to contact the outside world. Half an hour later, a gigantic tidal wave reaches the island and sweeps everything away.

Still, the people in Khao Lak do not know that a giant tsunami is coming. Nevertheless, some already notice strange anomalies, for example, many bubbles in the sea.

Suddenly, the sea starts to retreat more and more. The people on the island are fascinated by this natural spectacle, and many follow the water. As some amateur video footage shows, waves are already building up on the horizon.

Still, the people are paralyzed by sight and do not react as the waves come nearer and nearer. An hour after the earthquake, a giant water wall reaches Khao Lak, and although some may notice that something dangerous is on its way, they are still too paralyzed to react. A lot of them will respond too late, while others have enormous luck and can somehow save themselves.

The result of the tsunami was devastating. About 230,000 people were killed. Many of them probably could have been prevented if the signs had been interpreted correctly and the scientists in Hawaii knew who to contact.

The story tells us that interpreting the signs in the right way can save one from trouble. Additionally, there are also other analogies to economics, in my opinion.

On the one hand, economics is a bit like seismology. Like seismologists, economics mostly fail to give correct forecasts about when something will happen, and it only can forecast that something will happen. The seismologist can tell you more or less precisely what will happen if two continental plates slide on top of each other, but she will not be able to tell you when the pent-up forces discharge. However, one should take warnings from seismologists and economists too seriously and prepare accordingly.

Since the beginning of the war between Russia and Ukraine, forecasting the future path of the European economies has become very uncertain. Many economists warned that the consequences (primarily high energy prices and inflation) would lead to a tsunami of business failures and consumption, resulting in a drawdown of the European economy and a severe recession.

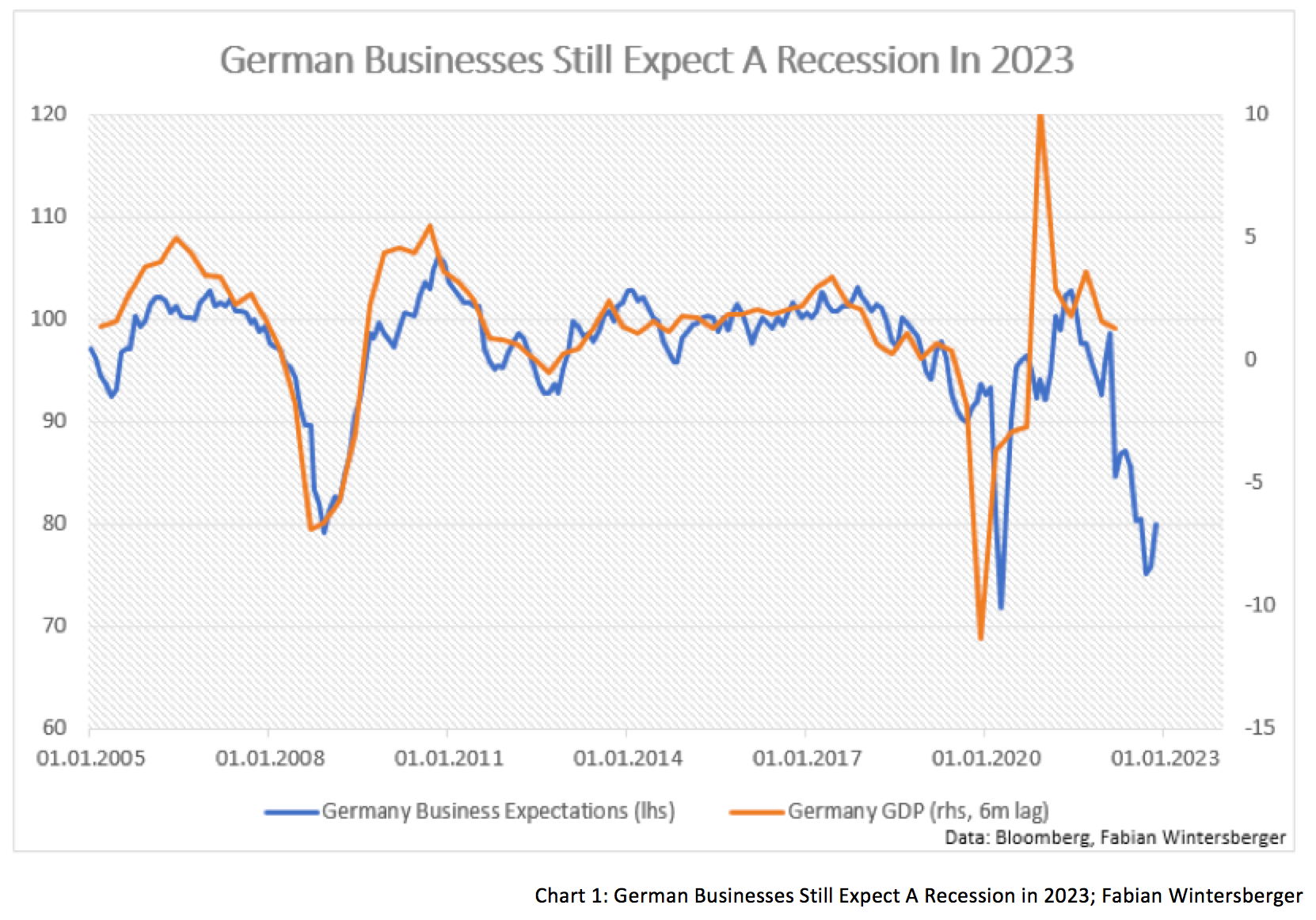

Indeed, business sentiment is terrible, as numbers from the German Ifo-Institute show. If we take business expectations as a guide, it is clear that a recession is highly probable in Germany and the Eurozone.

On the other hand, one could argue that one could conclude that already during the summer, where some economists and analysts speculated, Europe will already be in recession in the winter. However, despite all signs, there is none.

As a result, one may question if the recession will even become as severe as the Ifo numbers might suggest. Is it possible that the bad is not reflected in reality, and Europe may face only a mild recession? What I know from bank officials is that businesses are still investing, despite recession fears and rising interest rates.

For some, the fact that the Euro-Area is still experiencing economic growth is surprising. What also surprises is consumer sentiment. Although the sentiment is by far not positive, last week’s numbers showed that sentiment is getting better. According to numbers from the EU Commission, consumer sentiment reached a five-month high.

European stocks are also benefitting from better sentiment. Since September, European indices have performed better than US indices.

Is business sentiment worse than reality? If one took a walk through Austrian shopping miles and visited Christmas markets, as I did, one might get that impression. Everywhere one looks, it does not look different than before covid. If I relied only on what I have seen, I would not assume that Europe is facing an energy crisis and inflation is at its highest level in decades.

Do consumers have a wrong feeling of security? European governments did a lot to dampen the consequences of inflation, especially energy price inflation. On the other hand, they tried everything to secure the energy supply. Since the beginning of the crisis, European countries have allocated about 700 billion euros to achieve that.

Expenditures for supporting measures account for 7.4 % of GDP in Germany, 5.11 % in Italy, 3.55 % in the UK, and 2.79 % in France. Assuming that problems with energy supply can last for longer, this is probably just the beginning.

Apart from subsidies, there is another aspect of why the European economy looks more resilient than one might have assumed. European consumers mostly have long-term energy contracts, which means they are secured from fluctuating energy prices. This week, the domestic statistic agency in the Netherlands stated that it might have estimated energy inflation too high because it calculated it based on new contracts. As a result, measured inflation in November was much lower than in the previous months.

The support of consumption via subsidies to dampen energy price pressures and direct payments to consumers obviously caused higher profit margins for businesses because they could pass on price increases. That might be another reason why the mood in markets improved recently.

Another cause for reassurance could be the dollar’s latest pullback from its highs after signs increased that the Fed might start to slow its rate hikes. A recent statement from Jerome Powell at Brookings Institution caused another stock market rally on Wednesday.

The ECB did not reach that point yet. Last week, Isabel Schnabel said that incoming data suggests that the room for slowing down the pace of interest rate adjustments remains limited. As the ECB continues to hike interest rates, that could signify a short-term euro appreciation against the dollar.

A rising euro lowers prices for energy imports within the euro area, which are paid in dollars. Recently, energy consumption remained below multi-year averages because of the warm weather, contributing to a rise in sentiment.

The question is if the recent rise in consumer sentiment, the fact that the economy is still growing, and the latest appreciation of the euro is a sign that the worst is over for the European economies. Or is it a false sign of security?

Changing weather could be the first harbinger of that. While the weather has been mild, it was easy to use lower energy consumption. For the following weeks, meteorologists forecast a coming cold wave that is already driving the price of natural gas. The slowing wind also contributes to a rise in natural gas demand.

Support measures from European governments help that all this is not immediately affecting the budget constraints of European households. The European consumer did not cut back on expenditures as much as one would have thought. Therefore, the good sentiment might last until January or February next year.

Early next year, consumers will get price adjustments for their energy contracts and thus be confronted with reality. One can assume that many will get requests for additional payments and a massive increase in monthly payments.

However, government support might play a role here because of how prices are capped. There is no hard cap (energy prices=X), only maximum prices for consumers. If energy costs Y, and the cap is X, then governments will subsidize consumers per amount Y-X. This is an incentive for producers to raise prices to a certain extent.

If households face a considerable rise in energy prices, that might be the tipping point, where more and more will finally start to cut back on consumption. Real wages have dropped all around Europe already. For example, real wages year-over-year fell 5 % in Germany.

Chart 5 also shows that - currently - there is no danger of the so-called wage-price spiral that many economists fear. Furthermore, I would argue that the result of excessive wage bargaining because of inflation will result in rising unemployment, as businesses see that they cannot simply pass prices to consumers.

The latest inflation number might give some hope that inflation has reached its peak for now in Europe. Although it is hard to make a finite call for that, one can say that current government measures try to hold prices artificially lower than they otherwise would have been. However, if price caps are set below the equilibrium price, it will lead to lower supply quantities at some point.

Yet, not only might price caps lead to shrinking supply, but also the fact that the EU’s oil embargo against Russia will start soon. EU countries want to stop importing Russian oil and refinery products in the following weeks. Additionally, they want to set a price cap for Russian oil, although there is no agreement yet.

Russia is still the biggest diesel producer in Europe, and the few European refineries mainly refine Russian oil. It is not easy to switch to another oil, as it is not just oil.

Diesel is a crucial factor for modern economies. Farming and logistics only work because of diesel. Trucks and tractors run on diesel. There will be severe problems for agriculture and goods traffic when there is no diesel. Thus the embargo on Russian diesel on February 5th might have some consequences. Today, 50 % of all imported diesel in the UK and the EU is produced in Russia.

Switching to oil from another producer is costly, and governments will probably try to dampen its effects on producers by handing out more money. That implies rising costs for businesses and households, and another aspect is why sentiment could turn negative again very soon.

When it comes to Russian gas, there is no chance to exclude it from the European market anyway. Although imports through pipelines have diminished remarkably this year, European countries are still buying significant amounts of LNG from Russia, except the UK and the Baltic states are completely waiving Russian oil. For northwestern Europe, Russia is the second largest provider of Liquified Natural Gas, after the US but way before Qatar. This week, it was announced that Germany made a deal with Qatar and will receive about 6 % of its yearly natural gas imports in 2021.

Thus, one cannot conclude that the energy crisis in Europe is over. On the contrary, it is far from over, so the €700 billion governments spend might not be enough to overcome it. Governments will continue to spend, and at some point, financial markets might question the debt situation of European countries. That will be a big test for the ECB if it continues tightening monetary policy. Additionally, one can assume that state-guaranteed corporate credit for suffering companies will be expanded and put a floor on inflation because the money supply will be kept artificially elevated.

My hunch is that things will darken within the first months of 2023, and the positive sentiment will evaporate. At least all points I discussed above lead me to my conclusion.

That means that the latest appreciation of the euro will be short-lived, as it is grounded on the assumption that the ECB will continue to tighten policy while the Fed pauses. But the points from above make me think that the ECB will soon reach its limits.

the answers that I’ve found, are all the same

the uncovered questions, that still remainAs I Lay Dying - Paralyzed

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice)

It’s so true that markets appear ready to believe every story is positive without considering the reality underlying things. Well written here