Currently, news in the financial media is dominated by the war in Ukraine on the one hand and by the fact that the bottlenecks of supply chains are getting more severe due to China’s covid shutdown (the harshest lockdown since the pandemic has begun).

The highest price inflation in decades accompanies these events, so the scope for governments and central banks narrows. In times of low inflation, monetary and fiscal policy ran an easy playbook repeatedly: Covering problems with low/zero interest rate policy and running fiscal deficits. However, such a strategy can quickly become risky, even dangerous in current times. Suppose production levels are falling and money is poured into the real economy simultaneously. In that case, this is comparable to a fire brigade that is trying to put out a fire with gasoline.

Sanctions, war, and the result of high energy prices and supply-chain bottlenecks will be another drag on economic growth. This month, Deutsche Bank lowered its projection for world GDP by one percentage point from around four percent down to about three percent.

In Germany, all leading economic institutes (RWI, DIW, Ifo, IfW, and IWH) have lowered their growth projections from 4.8 % to 2.7 %. The German economy suffers from uncertainty regarding a potential ban on Russian energy. Stefan Kooths from IfW said that Germany would go into recession if Europe decided to widen its current sanctions on Russian energy. Another report from the German economic ministry says that uncertainty about future economic developments remains correspondingly high. However, Ifo expectations already suggest a high probability that Germany will be back in recession this year.

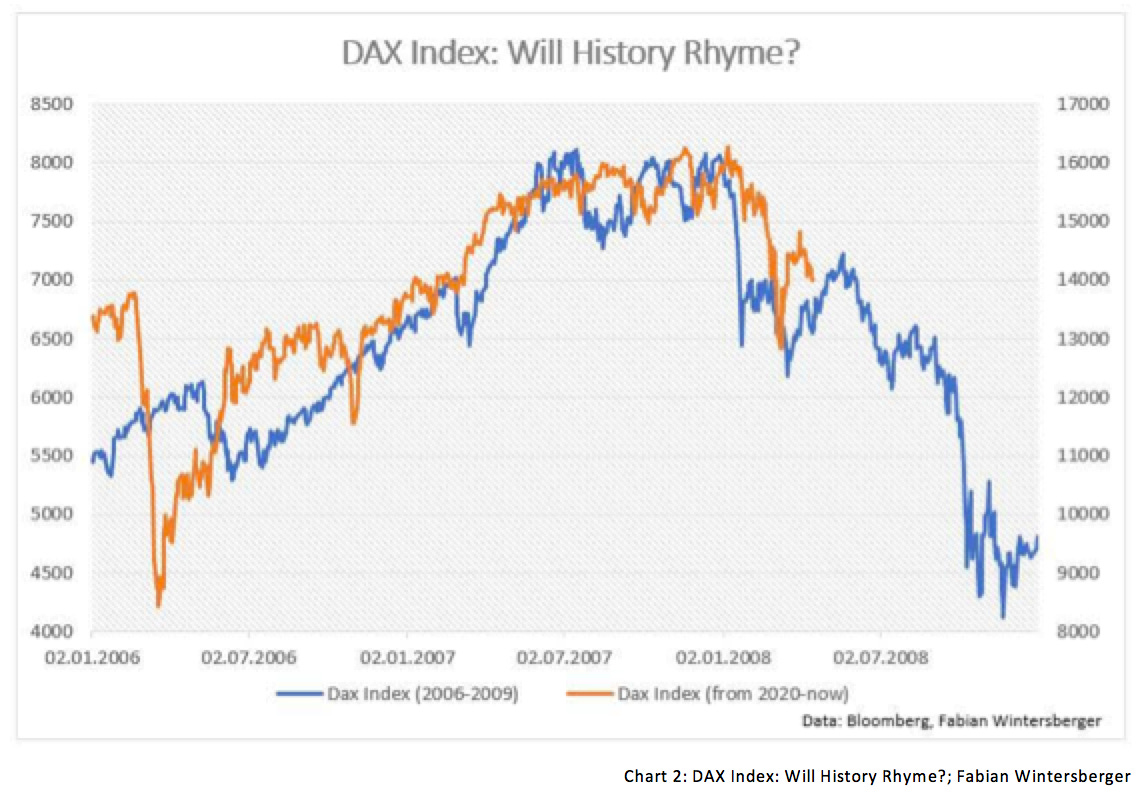

Similar to the preface of the financial crisis of 2008, expansionary monetary and fiscal policy generated an artificial, in my opinion unsustainable, boom. The recovery of 2020 and 2021 shows an interesting similarity to the preface of the GFC. However, it is always tricky to make such comparisons, but the chart suggests that history may rhyme once again.

Europe is the current sore spot of the world economy, especially the industrial parts of Europe. Contrawhise, it looks like the peripheral countries will grow above expectations this year. I had a chat with an economist from a bank from one of the PIGS states recently, who told me that he sees no scenario where the peripheral economy does not grow because of the low base from the year prior.

As always in difficult times, countries within the Euro area are debating whether fiscal rules of the monetary union need to be softened or changed. This time it was an unusual alliance of the Netherlands and Spain. They want to reform the rules that, according to euronews.com, it will be easier to enforce if governments are "empowered" to come up with their own fiscal plans that take into account national needs and characteristics. Not surprisingly, part of the plan is that green investments should lead the European economies back to high, sustainable growth.

While Europe is heading for recession, the situation in the United States is better but far from great. Economic data suggests that the economy is already slowing. Since June 2021, industrials have performed poorly (a sector sensitive to the business cycle) while utilities (usually seen as recession-proof) performed well. This is another sign that the US economy is heading into a slowdown or already in one. So, it is not only the 2s10s spread that points to future economic trouble, although the spread has widened recently and the curve steepened, which always happens after an inversion.

All this happens while inflation numbers are chasing from one new high to another. Rising inflation and economic stagnation usually remind everyone of the 1970s. Now and then, there was a price shock in energy, and both times, the energy price shock resulted from a political decision. In the 1970s, Arab countries decided to lower oil output due to the Yom Kippur war, while there have been economic sanctions against Russia these days.

However, one difference is crucial if we want to order our thoughts on inflation and its future path. In the 1970s, credit growth in the US was a solid 10 % YoY, while it currently stocks at 5 %. If we look at recent upward ticks in inflation, we observe that a rise in inflation accompanied by weak credit growth led to a fall in the inflation rate. Thus, I suspect that the situation is more similar to the 1940s when the US experienced big spikes in price inflation but no structural inflation.

Nonetheless, I think that the significant challenges in the current century will be inflation and economic growth. However, I might add that many advanced economies have suffered from weak economic growth for quite a while now, especially Japan and the European continent. In Europe, increasing regulation and the implementation of the euro are two of many causes why Europe is falling back compared to other countries like the United States. The dependency on Russian energy has exacerbated the problem recently.

So, the question is how the western economies can return to higher growth rates. In the previous decade, policymakers tried to achieve that through the channel of expansive monetary and fiscal policy, but growth did not return, and debt levels rose. The Keynesian dogma that the economy can grow out of a crisis by lowering interest rates and creating more money was proven wrong, without a doubt.

Low interest rates and bond-buying programs by monetary authorities have kept unproductive businesses alive. Those businesses tie up resources (land, labor, capital) and weaken growth potentials. Debt/GDP ratios rise, and capital no longer flows into real economic activity but into financial markets, and thus money velocity (basically GDP/money supply) falls.

Somehow, most people have forgotten that economic growth in the future requires a current lack of consumption. There is a lovely story from the father of gold bug Peter Schiff, Irwin Schiff, called How an economy grows and why it doesn’t, explaining this mechanism for a closed economy without money.

The story starts on a lonely island with three fishermen, Able, Baker, and Charlie. All three catch two fish per day, which they consume in the evening before repeating everything the day after. However, one day, Able decides that he wants to be able to catch more fish and decides that he needs to tie a net. While he is producing the net, Able isn’t able to catch fish, and thus he has to sacrifice current consumption to catch more fish in the future.

After two days without eating, Able finally finishes the net while Baker and Charlie continue to go fishing and catch two fish per day. Now Able can catch four fish per day and save the fish he does not consume. He made the economy grow and now can save for a rainy day.

Some days after, Baker and Charlie see that Able is enjoying much more time of the day under a palm tree and still can catch double as much fish as they do. They also want to tie a net, but they are unwilling to sacrifice current consumption. Therefore, Able is offering them some of his savings, which they can consume while working on their net. He just wants them to return the number of fish he lent them during that time (Ables investment), plus a premium (interest) of two additional fish.

Of course, the story is oversimplified, and our current economic system is much more complicated, but the mechanism remains the same for economic growth. Further, the story shows that economic growth would naturally lead to falling prices and hence is deflationary because the ratio between goods produced and a constant amount of monetary units causes prices to fall.

In our current monetary system, money comes into existence when commercial banks lend. When banks lend, newly created money is transferred to businesses (and individuals) bank accounts, and the firm hopefully invests it properly and leads the economy to grow.

Therefore, many people think that inflation is a natural concomitant of economic growth, respectively that an economy grows faster in an inflationary monetary system. That is why central banks call two percent inflation stable prices.

However, the mechanism remains the same, with one difference: Because additional money is created, purchasing power is transferred to the debtor. As the Cantillon Effect (Cantillon 2010, p. 155; Bordo 1983, p. 242) perfectly describes, those who receive the new money can buy additional goods and services in the marketplace at old prices and cause a rise in demand. As a result, prices adjust, and other market participants now face a loss in purchasing power.

One argument why this leads to higher economic growth might be that riskier economic actors, who are more likely to engage in business, are rewarded for taking risks to make an economy grow. In contrast, risk-averse economic actors lose purchasing power but enjoy the fruits of a growing economy otherwise (for example, because they have a job that the entrepreneur created).

If the investment is thriving and more goods and services are offered in the marketplace, the general price level probably remains the same, and inflation would be zero percent. Admittedly, this is not the case in our economy because the rise in the quantity of money in the real economy mostly does not lead to an adequate surge in production.

Another factor is that in our current monetary order, investments do not equal the available amount of savings (in a monetary sense). Banks can lend much more money than their clients’ amount in their checking accounts, although banks are restricted (theoretically) because they are obligated to hold a certain amount of reserves.

Of course, savings can and are used for investments in the real economy—for example, a business issues a bond to build a production facility. Private investors can buy this bond and lend money to the business. However, this does not affect the quantity of money in the economy, and the money merely changes hands.

Though, in our current low interest rate environment, many businesses do not invest in the real economy because they consider it a risk that is not worth taking. Due to low interest rates, market participants now have a higher time preference, meaning they value current consumption higher than future consumption of similar goods.

It is more likely that businesses issue a bond by buying back stock, leading to higher demand for the company’s stock and thus a rise in its price. Shareholders are satisfied, and CEOs are too because they earn a nice bonus (for many CEOs, their bonus consists of call options on the company’s stock). Thus, it should surprise no one that stock buybacks rush from one all-time high to another.

If the last decade proved anything, then higher government debt does not lead to a revival of economic growth. The state is a lousy investor because the people in charge do not have to fear any consequences for bad decision-making. The saying is that governments do not invest but merely spend for a reason.

Before I get back to recent events, let me further examine the argument that an expansion in the quantity of money pushes economic growth upwards. It probably is not untrue, but I would argue that this would drive growth at the expense of future growth because fiscal spending and subsidies simply bring investments forward.

However, suppose this money flows into usually unproductive projects that are only profitable because of low interest rates. In that case, it is a drag on growth because other projects cannot be financed then.

Further, I agree with the argument of Richard Werner (Princess of the Yen) that low interest rates are a drag on growth in general because if rates are low, the incentive to invest in riskier but productive projects will fall. Investors are pushing back from such investments because the interest they earn is not worth the risk.

Currently, the world economy is on the edge of an economic downturn, partly because war and supply chain problems lower demand and because bad policy keeps demand high and pushes prices higher. It is an explosive melange, and fighting the downturn through more spending might create more problems than it solves.

A food crisis because of falling agricultural production and rising commodity and fertilizer prices is already a certainty for some developing countries. Simultaneously, a situation of similar proportion to the Great Financial Crisis of 2008 will push the US dollar higher (at least at first). It is no coincidence that Sri Lanka recently halted dollar debt payments to spend the money on food instead.

Meanwhile, the Europeans are putting sanctions on Russia and sharply driving up their energy costs. As energy is part of every production process, expect production costs in Europe to rise. The idea that the green transition will spur economic growth may be accurate at some point in a future far, far away, but it will not do anything in the near term. Those renewables will be produced in China, not in Europe.

Recently China pushed back on its own climate goals and plans to build more coal plants to keep energy costs low. This means that the Chinese prefer to work on sustaining their new wealth instead of trying to destroy it as the Europeans do. It seems that there are tough times ahead for the Europeans. The danger that Europe will become the victim of the world’s two superpowers, China and the US, is high.

Happy Easter to you!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)