Necessary Evil

Society in every state is a blessing, but Government, even in its best state, is but a necessary evil; in its worst state, an intolerable one. — Thomas Paine

It was an eventful Pentecost weekend regarding news about the war in Iran. Whether it was again just Trump and his administration jawboning the market down through leaking stuff to various media outlets, one needs to see. However, it seems that the description that all parties are “close to a deal” is a bit misleading, given the fact that there were reports that the US navy also shot some Iranian ships which tried to lay some mines in the Strait of Hormuz.

But if one looks at the price action, one can clearly see that markets reacted positively to the news again. At this point, it seems that financial markets have moved on and assume that the Iran war is basically over. Everyone seems to expect a deal is in the pipeline, and setbacks are treated simply as a delay to a deal. Whether that turns out to be right needs to be seen.

Nevertheless, stocks and bonds reacted positively to the news while oil (Brent) dropped back to the mid-90s on Monday. US markets were closed on Monday due to Memorial Day weekend, but followed the DAX’s move from Monday and climbed higher.

Although the war has generated a lot of turmoil and confusion, so far, stocks have shrugged off all of these worries. And still, the disruption brought up some interesting twists and turns regarding Europe and China, while turning the rally into one of the most-hated of all time.

Europe Remains Stuck In The Mud & ECB Rate Hikes Won’t Help

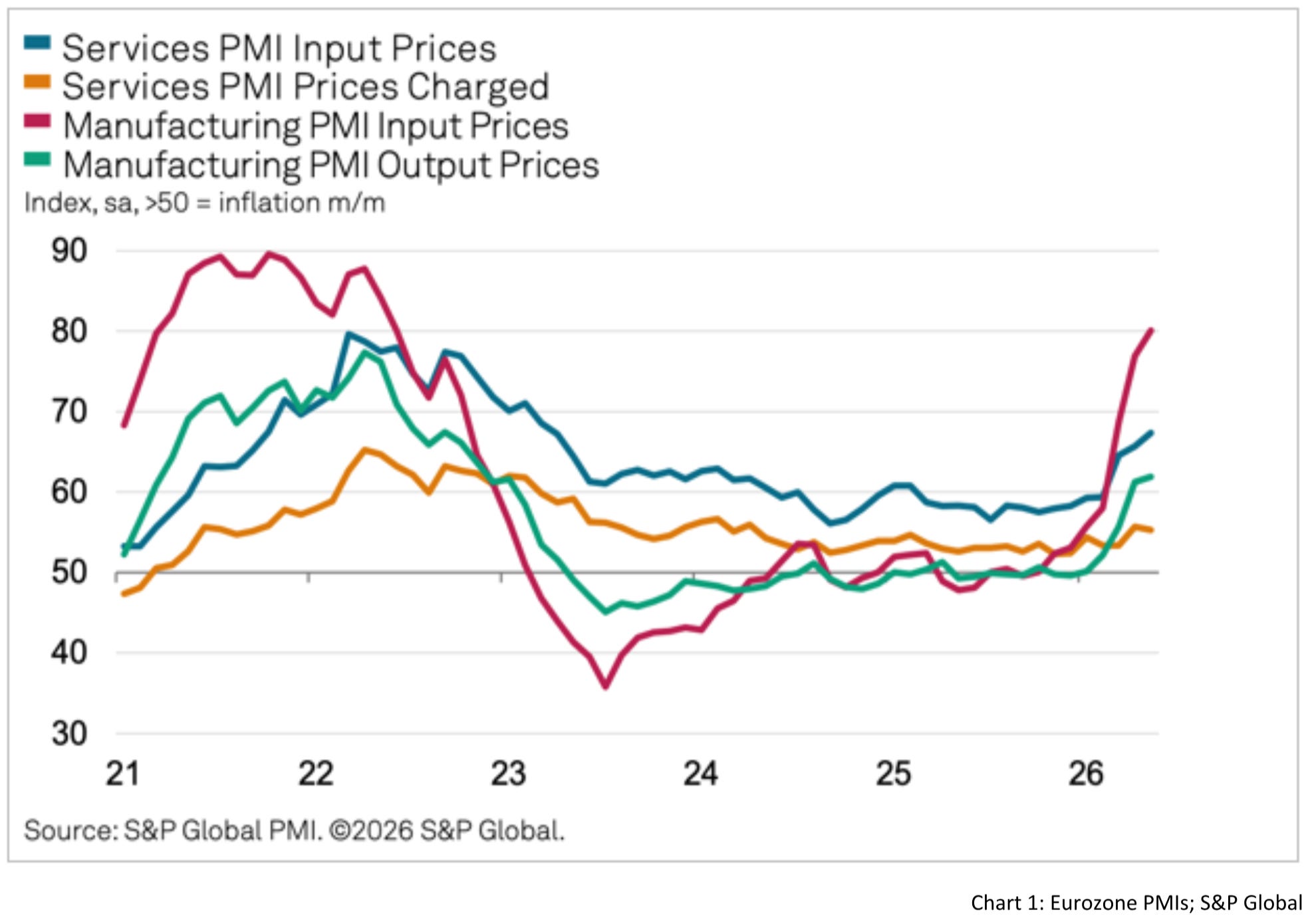

On Friday, we got the Eurozone S&P Global Flash PMIs for May, and the summary is that things aren’t looking good for the Eurozone. The data points to a rapidly deteriorating eurozone economy, with the weakness now broadening beyond manufacturing into services as well. The flash eurozone composite PMI fell deeper into contraction territory at 47.5 in May, marking the sharpest decline in private-sector activity in more than two years. Particularly concerning is that the services sector, which had previously cushioned the industrial downturn, is now weakening sharply under the weight of higher energy costs, declining demand and rising geopolitical uncertainty tied to the Middle East conflict. At the same time, input-cost inflation accelerated strongly again, suggesting Europe is drifting deeper into a stagflationary environment rather than a normal cyclical slowdown.

France remains the clearest weak spot within the bloc. The French composite PMI collapsed to 43.5, its lowest level since late 2020 and the sharpest contraction in more than five years. Services activity deteriorated particularly aggressively, while manufacturing also slipped back into contraction. Survey respondents cited falling new orders, weaker consumer demand and the surge in energy and transport costs as major headwinds.

Germany is holding up somewhat better than France due to relatively firmer manufacturing activity, but the broader trend there is also deteriorating. German PMIs have now rolled over again after the brief stabilization seen earlier this year, with weakening domestic demand and slowing export activity increasingly offsetting any benefit from fiscal stimulus expectations or inventory rebuilding.

All in all, that data therefore underscores the view that Europe is sliding into a far more classical stagflationary slowdown, where activity contracts even as price pressures reaccelerate. The prices component is moving in the opposite direction as the headline number.

What’s concerning here is that these numbers reveal that the European spending packages have been wasted, or at least only helped to avoid an even bigger downturn. The German auto industry is in tatters, and now more and more suppliers also have to cut their workforce due to diminishing orders and competition in Southern and Eastern Europe.

The only part of the German economy that profits is the defense industry, but it’s too small to absorb the workforce that is freed up due to the economic struggle in other sectors. I remain skeptical that the hope that a continuous rollout of Chancellor Merz’s spending package will turn the situation around is justified. First, because regulations are slowing down the pace of the funds being spent, and second, because government funds usually aren’t spent in an efficient way. Down the road, that might leave only one choice, namely an increase in planned spending. And what that does to the German debt/GDP ratio and bond yields should be known.

It might be that Ursula von der Leyen’s EU Commission comes up with a plan to attract investment. Maybe the result will be another round of joint debt. However, the latest post-pandemic recovery fund didn’t achieve much either. After news that Spain used some of the fund to pay out pensions, the FT now reported that the money for Italy also failed to achieve much except more debt. Despite being the largest recipient of the recovery fund, Italy’s growth remains behind its European peers.

And above all that comes the pickup in inflation due to rising energy prices and the lack of possibilities for European companies to cut costs and increase efficiency. Despite some demand destruction regarding the high oil prices, it’s by far not enough to bring consumer price inflation down to target.

As a result, the ECB - still in fear of repeating their mistakes during the pandemic - will likely raise interest rates at its next meeting. I continue to believe that this would be a mistake, because governments could achieve a lot by scrapping excessive regulations, subsidies and opening up the market instead of regulating it more. And different to 2022, this isn’t an environment where demand is increased due to excessive money creation.

At least the companies which have a lot of export business or business in the US are still holding up the major European indices, as they enjoy stable demand from there.

Rising Call Volume Isn’t A Sign Everyone’s Long

With the bad state of the European economy and the uncertainty around the Iran war and the future trajectory of oil prices, the latest rally leaves many investors behind. They are in bright disbelief of this bull market in stocks and look for more reasons to argue that the price action is moving in a different direction.

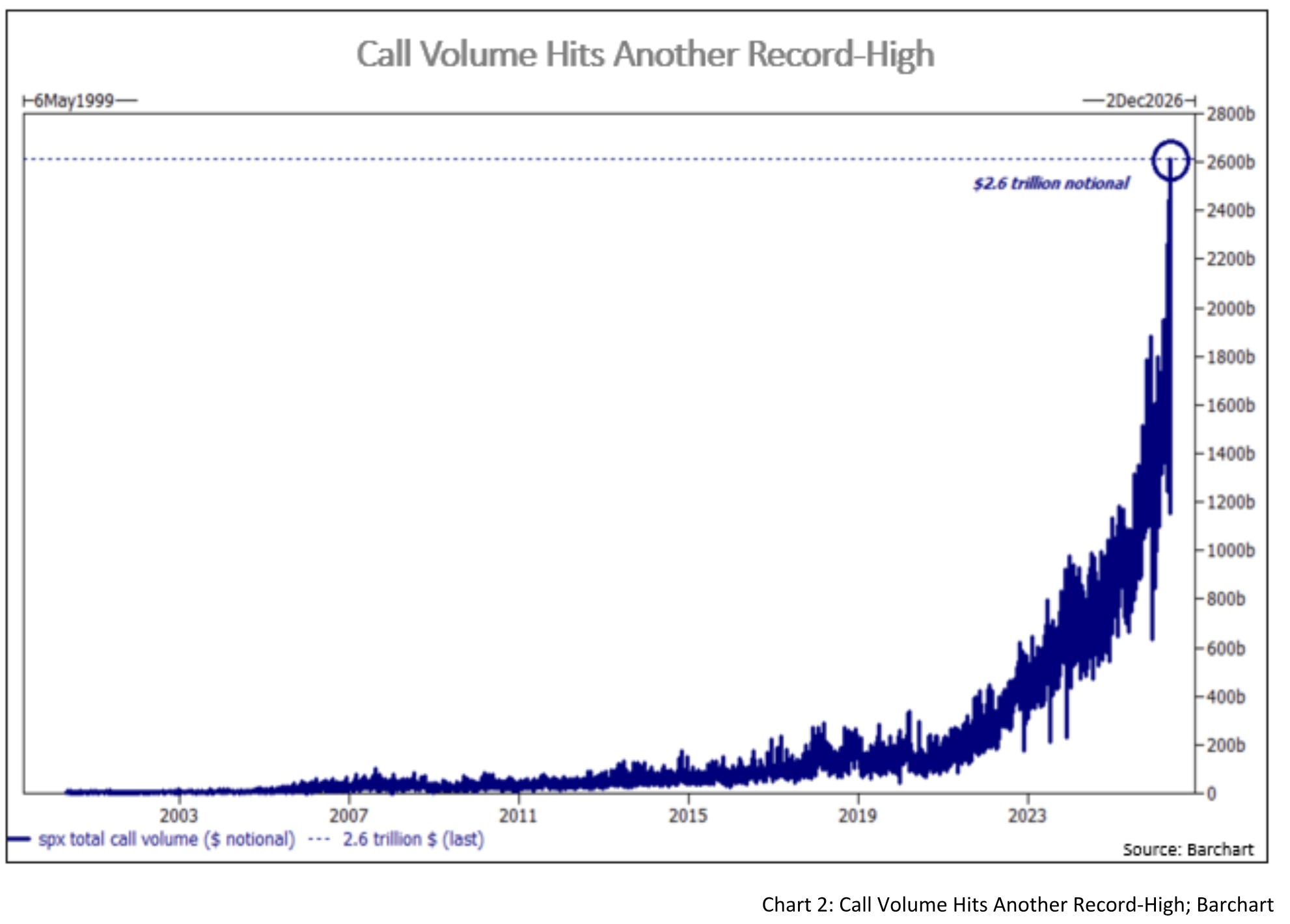

That coincides with various people claiming that the majority of market participants is hyperbullish on the stock market. One argument is the S&P 500’s total call volume, which recently shot up to $2.6 trillion, another all-time high.

The claim is that this is proof how bullish the market is in general. The main tell is that due to excessive call buying, dealers are short calls and have to delta-hedge the position by buying the index. The higher the market goes, the more shares dealers need to buy to remain delta-neutral. That creates a gamma-squeeze where excessive call buying drives the market.

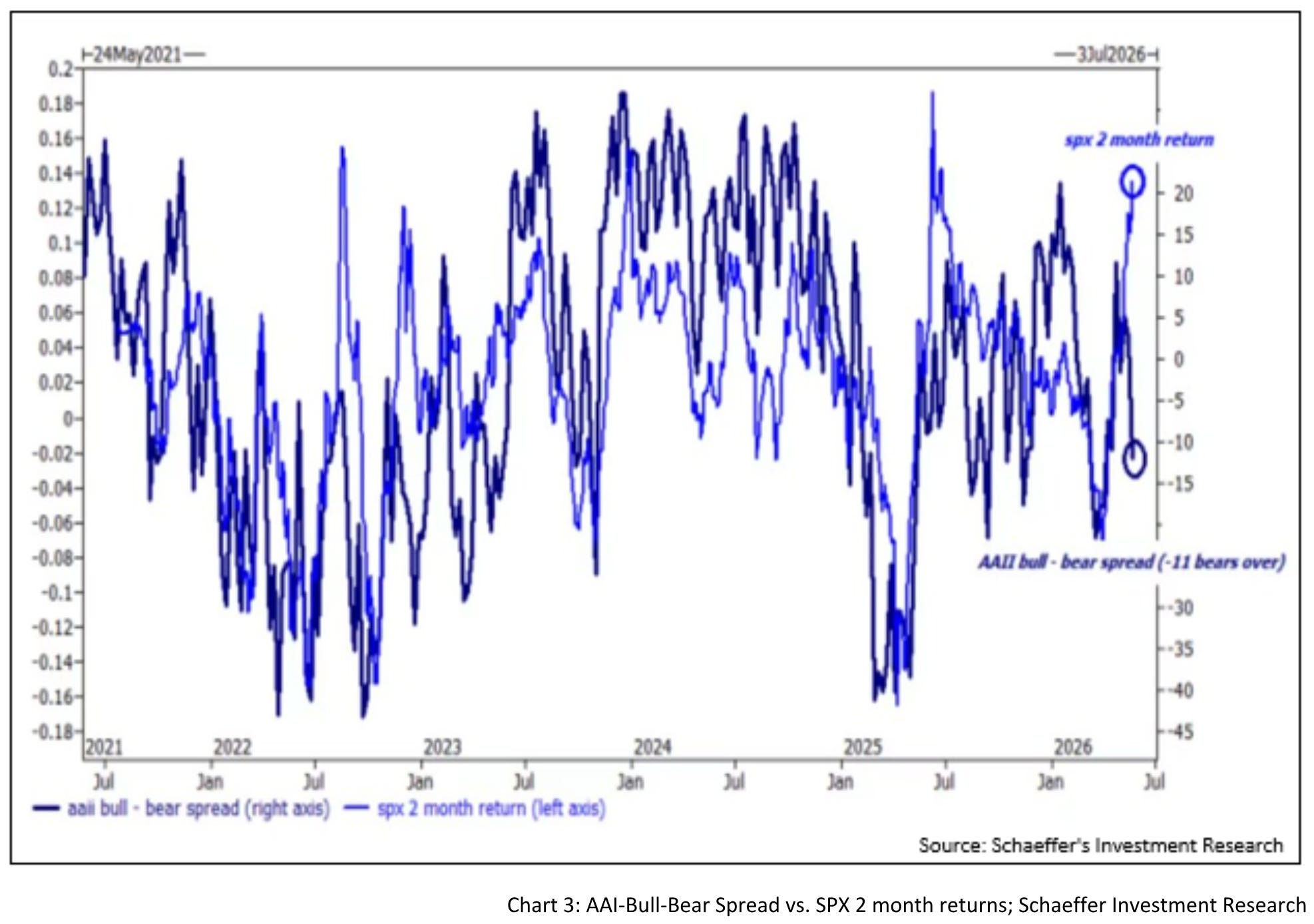

But in fact, it can be interpreted as the exact opposite. First of all, the AAII sentiment remains negative despite rolling 2-month returns of the S&P 500 ramping higher.

Therefore, I’d like to come up with an alternate explanation for the record amount in call volume that fits with the negative sentiment. If sentiment is negative, one could interpret it that institutional investors are not fully invested and net-short. To hedge their position, they need to buy calls, which drives call volume up. Dealers, on the other hand, are short gamma (they sold calls) and need to buy stocks if the market pushes higher (similar to the situation described above).

The result is a market that pushes higher despite bearish overall sentiment and becomes more fragile in case the market suddenly turns and hedging flows abate. Combined with the still strong economic data coming out of the US, the excessive government spending and consumer prices rising due to strong demand, I don’t think that there’s solid evidence that a top is near. It looks more as if the bull market still has legs.

What could change that would be another strong increase in oil prices that leads to demand destruction in the US and stops inflation. But the Cleveland Fed nowcasts a 4.18% US CPI for May, signaling no demand destruction at current price levels.

One reason that global oil prices haven’t pushed higher is that demand from Asian countries hasn’t increased as much as expected. Japan’s SPR releases and plunging Chinese oil imports appear to have offset part of the geopolitical risk premium. As Bloomberg’s Javier Blas wrote on X:

The difference between Chinese oil imports (plunging, heading into May to a 10-year low) and Indian oil imports (surging to the highest May ever) can not be more striking...Effectively, Beijing (and Tokyo using the SPR) have saved the day for the whole region.

Especially the divergence between China and India appears odd. Journalist Izabella Kaminska recently came up with an interesting thesis that could potentially explain it.

China: A Shadow-Layered Oil Standard?

Kaminska’s core argument is that China’s oil inventories may no longer merely represent physical energy reserves, but increasingly function as collateral underpinning a broader shadow-financing system. In that framework, warehouse receipts tied to commodity inventories effectively behave like a form of base money within China’s highly leveraged refinancing architecture. Liquidating large parts of these reserves would therefore not simply release supply onto the market, but potentially extinguish collateral supporting credit creation and trigger broader financial stress.

She argues that several recent developments are consistent with that interpretation. Despite collapsing Chinese oil imports, Beijing has not meaningfully increased refined-product exports to neighboring countries, even though doing so would help ease regional shortages and lower prices. Instead, China appears focused on preserving domestic supply. At the same time, refinery margins have collapsed as state-managed fuel-price controls prevented refiners from fully passing higher crude costs onto consumers. According to Kaminska, this increasingly resembles a system under financial strain rather than a country comfortably sitting on massive excess inventories.

The broader implication is that commodities may increasingly operate as monetary infrastructure within fragmented global financial systems. Rather than a traditional oil standard, Kaminska describes something closer to a shadow-layered commodity collateral system sitting next to the dollar framework. If correct, this would help explain why China appears reluctant to aggressively draw down reserves despite elevated prices and geopolitical stress. The reserves themselves may have become too financially important to liquidate without destabilizing the broader system they support.

Clearly, that’s a very speculative theory, but for the merit of it, let’s discuss it. I’m sure some might interpret such a system as a clever move to become less dependent on the dollar framework when it comes to domestic financing conditions.

However, if the hypothesis is even partially correct, I think China may have made a profound strategic error.

It’s broadly acknowledged that China is heavily interfering in the domestic economy to keep the system afloat and subsidize key industries. And at first sight, the move toward a domestic parallel structure to loosen the burden of exchange-rate management against the dollar appears reasonable, especially from the perspective of policymakers. It buys short-term resilience through intervention, buffers and additional collateral.

Yet if such a system exists, the current reluctance to draw down reserves for their primary purpose (namely ensuring cheap and stable energy supply during disruptions) exposes a major weakness of such an “oil standard.” If warehouse receipts are increasingly used as collateral, then these receipts no longer merely represent claims on physical inventories, but become the basis for a leveraged fiduciary media system layered on top of commodity markets. These claims are likely heavily rehypothecated and integrated into a broader shadow-financing architecture.

That could potentially make the entire structure even more unstable than the traditional monetary system itself. Oil can no longer be freely drawn down without threatening financial stress, refiners are forced to absorb losses because of political interference, and economic incentives become increasingly distorted. China’s domestic economy has already experienced severe strains due to massive malinvestment in housing and persistent deflationary pressure. A shadow layer built around oil collateral may have eased some of these problems in the short term, but it also risks creating a much larger fragility underneath the surface.

If the recent reluctance to release reserves truly points in that direction, it would suggest that intervention is once again delaying the market-clearing process while simultaneously increasing the scale of the eventual adjustment. Rather than reducing dependence on the dollar system, China may instead have created a highly leveraged collateral structure vulnerable to confidence shocks and refinancing stress.

From a Misesian perspective, the problem is that such a framework increasingly disconnects credit creation from genuine market signals and market clearing. Intervention may delay the adjustment process for some time, but it also risks magnifying the eventual correction once confidence in the collateral structure itself begins to weaken.

Market Assessment

While my assessment on the stock market remains that the bull market remains alive and healthy enough to climb toward new highs, the situation in the bond market has changed a bit.

Due to the fact that European government bonds are more correlated to oil prices than US treasuries, a loosening of tensions in the Middle East might help German Bunds more than US treasuries. The price action in 10y Bunds suggests that a turnaround is already in the making. If that’s a global phenomenon, it could be that Bunds outperform treasuries because treasuries are also influenced by the stronger inflation pressures in the US due to strong economic demand.

Bitcoin weakened a bit lately due to the news cycle around the war, joining gold which trended lower since April. The bullish trend in Bitcoin seems to have disappeared and it might be that the market is ready for another down leg.

EUR/USD remains under pressure as markets might realize that the current environment makes it more and more unlikely that new Fed Chair Kevin Warsh can deliver an interest rate cut. He might fight the pressure to hike, but as noted in the past, a steady Fed Funds rate translates directly into looser financial conditions. If expectations for a hike increase, then the dollar might appreciate versus the euro.

Conclusion

The war between the US and Iran has increasingly turned into a sideshow for financial markets. Investors no longer ask whether tensions will escalate, but rather how quickly policymakers, central banks and governments will move to contain the economic fallout.

Yet beneath the surface, the current environment reveals something much larger. Europe is drifting deeper into stagflation despite massive fiscal intervention, the US bull market increasingly depends on liquidity flows and hedging dynamics, and China may have built an entire shadow-financing structure around commodity collateral and state-managed balance sheets.

In other words, the global economy appears to become progressively more financialized, leveraged and politically managed at the exact moment geopolitical fragmentation accelerates. The result is a system that looks stable on the surface, but increasingly depends on intervention, refinancing and collateral structures underneath.

Ironically, that may also explain why markets continue to rally despite widespread disbelief. As long as governments continue to intervene, liquidity continues to circulate and balance sheets continue to expand, the adjustment process can be delayed for longer than many expect. But for now, policymakers see interference as the “necessary evil,” either for stability (China), to fight the downturn (Europe), or to remain on top of the world (the US).

Looking for a way out but it’s all just in vain

Time won’t wait & there’s no sequel

Waste away to thread the needle

Weighed Down cause it all ends the same

Life is pain & love is lethal

It’s all necessary evilMemphis May Fire - Necessary Evil

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.

Nasty song choice, bud. 🙆🏻♂️🔥 I daresay this post suits more to CMND/CTRL of Deftones' song.