My Own Grave

If Christine Lagard thought that her latest press conference would have enormous consequences? I am not so sure.

No more NIRP in the Eurozone is the assumption of many news stations, analysts, and some economists. Now, after the Bank of England and the Fed have already thrown the towel, it seems that the ECB has capitulated too.

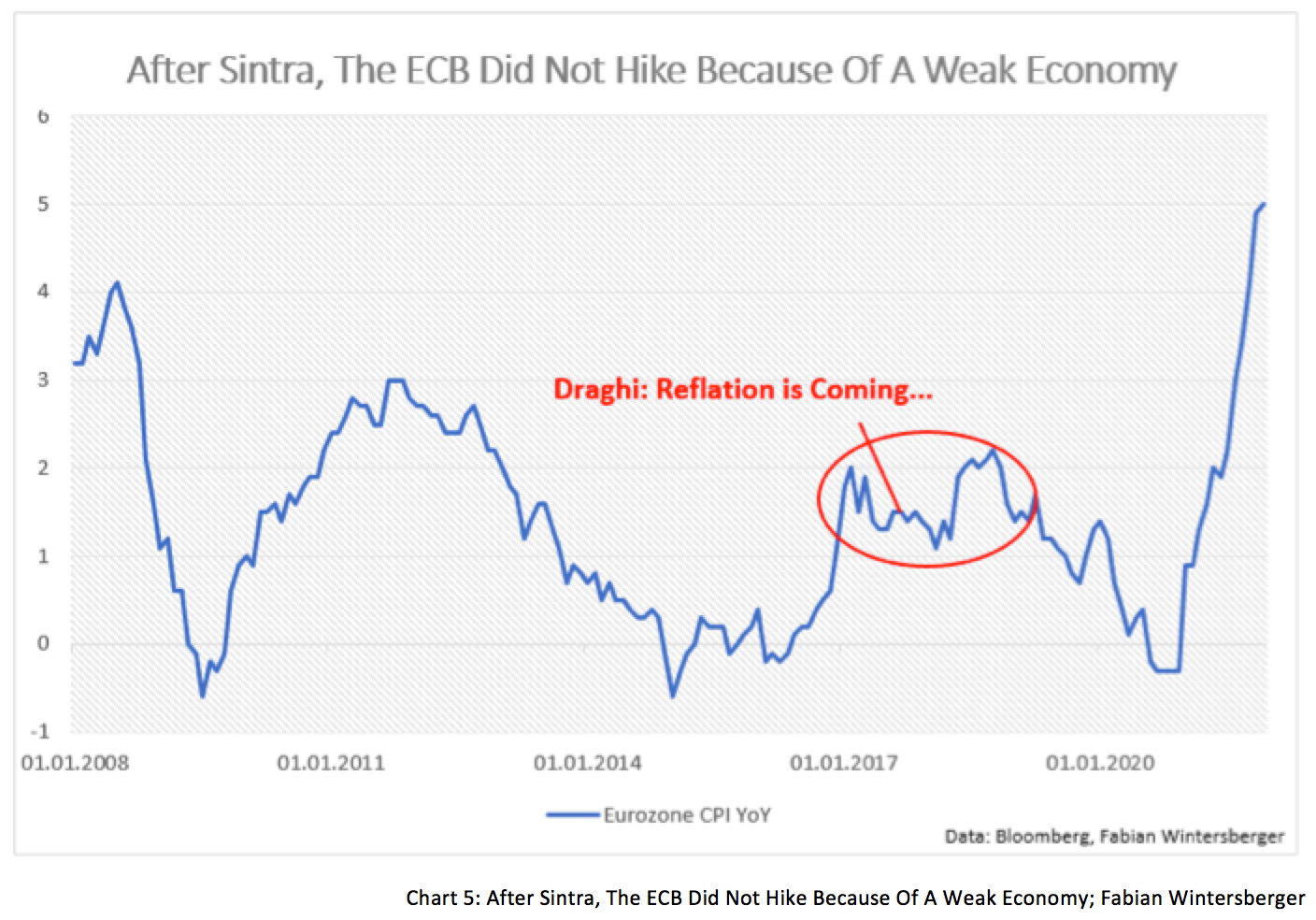

Higher inflation, longer than we previously thought, is one of the main reasons the ECB is more serious about thinking about a tighter monetary policy standpoint. Even more severe than Mario Draghi in Sintra in 2017.

‘All signs now point to a strenthening and broadening recovery in the euro area… deflationary forces have been replaced by reflationary ones’ - Mario Draghi, Sintra (2017)

Back then, Draghi shocked markets and caused a spike in government bond yields because everyone then expected a regime change. Don’t look back in anger, I would say.

Today we all know that it went differently. However, now it should be serious, right? But how is the situation compared to 2017? Is it time for a regime change?

The ECB balance sheet was at 4 trillion Euro when Draghi commented in Sintra. Until today, the balance sheet has nearly doubled, although the year-over-year change was about the same. At the peak of the crisis, the YoY change was at about 50 %. So, liquidity injections are already shrinking.

Interestingly, the ECB had to ramp up asset purchases just as it stopped widening its balance sheet. As soon as the balance sheet YoY growth approached zero, the ECB loosened its monetary policy.

Admittedly, the ECB had to act this way, given how harsh the draconian measures by all governments have been when they shut down the economy back in the spring of 2020. Together with the Federal Reserve, they had to keep markets alive by injecting billions into it.

But Madame Lagarde made it clear last week that the ECB may have to act sooner than it previously thought because of the high inflation rate. According to Lagarde, it cannot be ruled out that inflation will stay above the ECBs’ 2 % target for longer.

Honestly, the ECB has buried its own grave, and there is no one else to blame. It made it possible for European governments to go deeper and deeper into debt and to, as a result, blow up debt/GDP ratios. In 2020, the situation got even worse than back in 2017.

You may have noticed that Eurozone debt/GDP went down from 2014 to 2020. That is mainly because of German Austeritätspolitik and not because the states who needed to be more prudent were (as we can see in Chart 2).

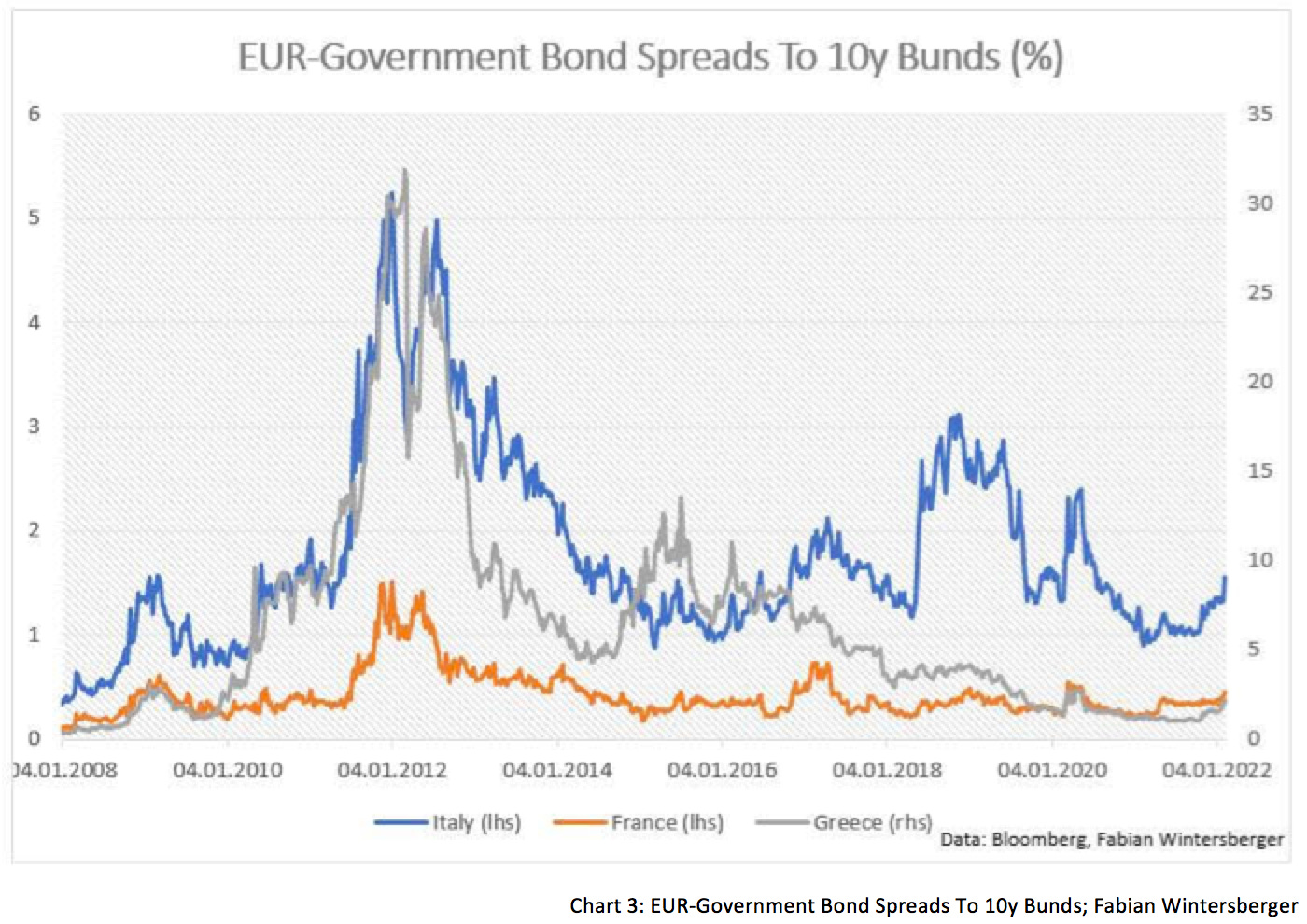

Lagarde’s comments last week have caused a widening of government bond spreads compared to german Bunds, although spreads remain ridiculously low historically.

Could a tighter monetary policy stance of the ECB cause a blow-up of government bond spreads? According to Arne Petimezas, an analyst at AFS group, no. In a morning note, he showed that the BTP-Bund spread blew up whenever Italy had political turmoil.

I agree that an ECB tightening probably will not blow up spreads, but I think that the problem will not be bond spreads but higher yields. European countries are heavily indebted and thus be highly vulnerable to a generally higher interest rate environment.

The ECB has kept rates below zero since 2016, and it did not have a very positive effect on economic activity. Money velocity in the euro area has fallen for more than three decades now, a sign that newly created debt is not used productively.

As debt levels rose, the marginal productivity of debt decreased. Hence, the European economy suffered from a high portion of zombie companies who the ECB kept alive via NIRP. Natixis estimated that (back in 2019!) about 20 % of businesses of the Eurozone were zombie companies. The pandemic most definitely made this situation worse.

The ECB and European governments heavily supported struggling businesses during the pandemic. However, many companies did not receive any support or very little. Those programs benefited mostly businesses close to governments, just as usual.

Additionally, corporate debt increased because of credit guarantees by governments. The question is if those companies can even survive a higher interest rate environment. In my opinion, this is a legitimate question. After Draghis’ Sintra speech back in 2017, the ECB did not raise rates because economic activity stagnated as asset purchases were lowered. Nevertheless, inflation is much higher today.

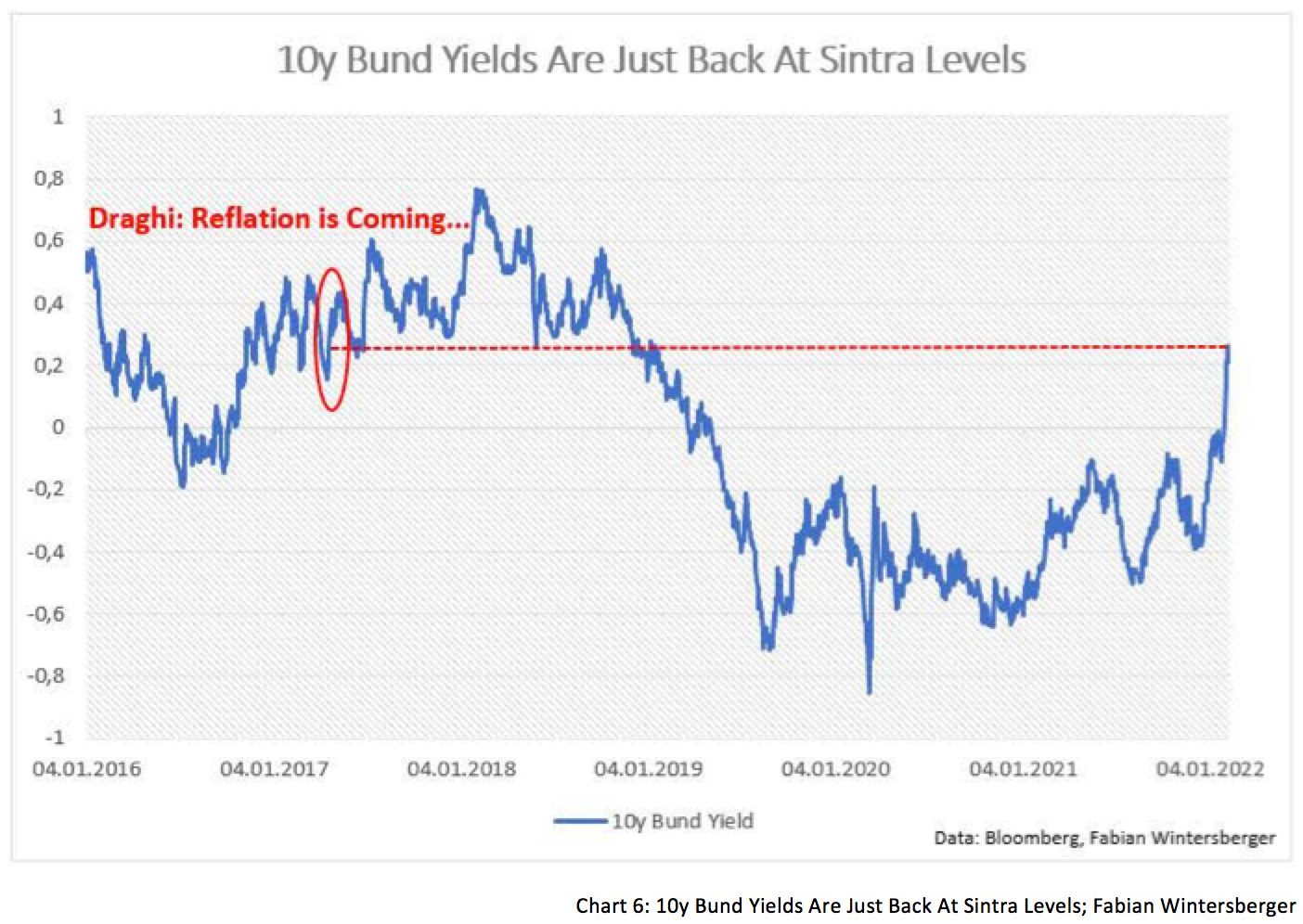

Markets showed a harsh reaction after Lagarde’s comments last week. The hawkish Fed already pushed Bund yields close to two percent, but during the ECB press conference, they rose by another 20bps. Now, 10y Bund yields are as high as back in 2017.

However, if one takes the ECB seriously (and the market does), the move in 2y yields was much more spectacular. 2y Bund yields are now at 2016 levels.

One should raise the question: Do you think the economic situation is better or the same as in 2017 when Draghi (wrongfully) called the reflation-trade?

Debt/GDP levels were lower back then, and corporate debt levels were lower. Looking at the MSCI Small Cap ETF for Europe, even a mild tightening by the ECB led to a stagnating economy.

The brief impulse at the beginning of 2020 was caused by the restart of loosening monetary policy in the fall of 2019 (remember? Not QE). Can SMEs even cope with higher yields? I am skeptical.

Only the unemployment rate makes some hope, at least at first sight. The unemployment rate in the Eurozone is now below pre-crisis levels, close to 7 %. Although it seems high compared to the US, one should not forget that Europe has a much higher labor force participation rate than the US.

However, the number is only low because of retention schemes of European workers who are not unemployed but work fewer hours than pre-pandemic.

Daniel Lacalle wrote an excellent article about that here. According to Daniel, 5 million people are still waiting to return to normal activity.

Further, inflation dampened the recovery in 2021 as real wages went down, as Daniel correctly notes. However, the idea that the EU’s recovery plan can bring the EU back to sustainable economic growth is not convincing.

A tightening of monetary policy is long overdue. I think that it should have happened a decade ago, at the latest. But I do not expect it to happen now. Probably we will witness a small hike here and a slight tightening there. But not more. The Fed will show the ECB that it is terrible to hike rates right into a slowdown.

Inflation will slow, regardless of what the ECB does. Liquidity is shrinking, so I think inflation will have a setback before its next big leg up (what will happen if government stimulus is making a comeback).

I have to admit that this assumes that supply chain problems will ease gradually this year, and they are the big IF. However, given how bad governments react to the energy crisis, I assume that if supply chain problems worsen, the reaction will be disastrous.

This will be the central question for the next two quarters: deflation or stagflation? We will see, and both scenarios are not suitable for the European economy. However, my prognosis is that a ‘monetary regime change will be short-lived.

Finally, I am a little bit surprised that it seems that hardly anyone is looking at France. Macron wants to get re-elected this year, and he will do anything to keep monetary policy accommodative. Will Lagarde throw him (and her home country) under the bus? I do not think so. Tightening will have to wait.

Have a great weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)