Meddler

In the whole western world, there are discussions about energy prices. Last week, Ursula von der Leyen and the EU Commission made some proposals to bring prices back under control. Ideas range from price windfall profit taxes to mandatory energy savings. Simultaneously, nation states advise on similar solutions while they plan to make additional transfer payments to the public to dampen the effects of high inflation.

Although, this week, several EU countries stated that they opposed the proposal of a price cap on Russian gas imports, as the Guardian wrote:

EU member states that import large amounts of gas from Russia, including Hungary, Slovakia and Austria, have spoken out against a cap on Russian gas because they fear the Kremlin would halt all gas flows, plunging their countries into recession. The Russian president, Vladimir Putin, has already threatened to halt energy exports to Europe if such a plan is agreed.

On Wednesday, von der Leyen revealed some more details in her State of the Union speech. The EU plans to put a windfall profit tax on energy producers and fossil fuel companies. According to von der Leyen, this will raise more than 140 billion euros. Additionally, she stated that the EU would spend another 3 billion euros to help build a future hydrogen market.

All the above underlines my forecast that the EU Commission will intervene more in the energy markets’ price mechanism. Therefore, I decided to write about the functioning of the price mechanism and why meddling around with it never is a good idea.

Before that, I want to recap the ECB rates decision of last week and this week's US inflation data. While Christine Lagardes’ rhetoric turned 180 degrees, the United States consumer prices spread throughout the economy.

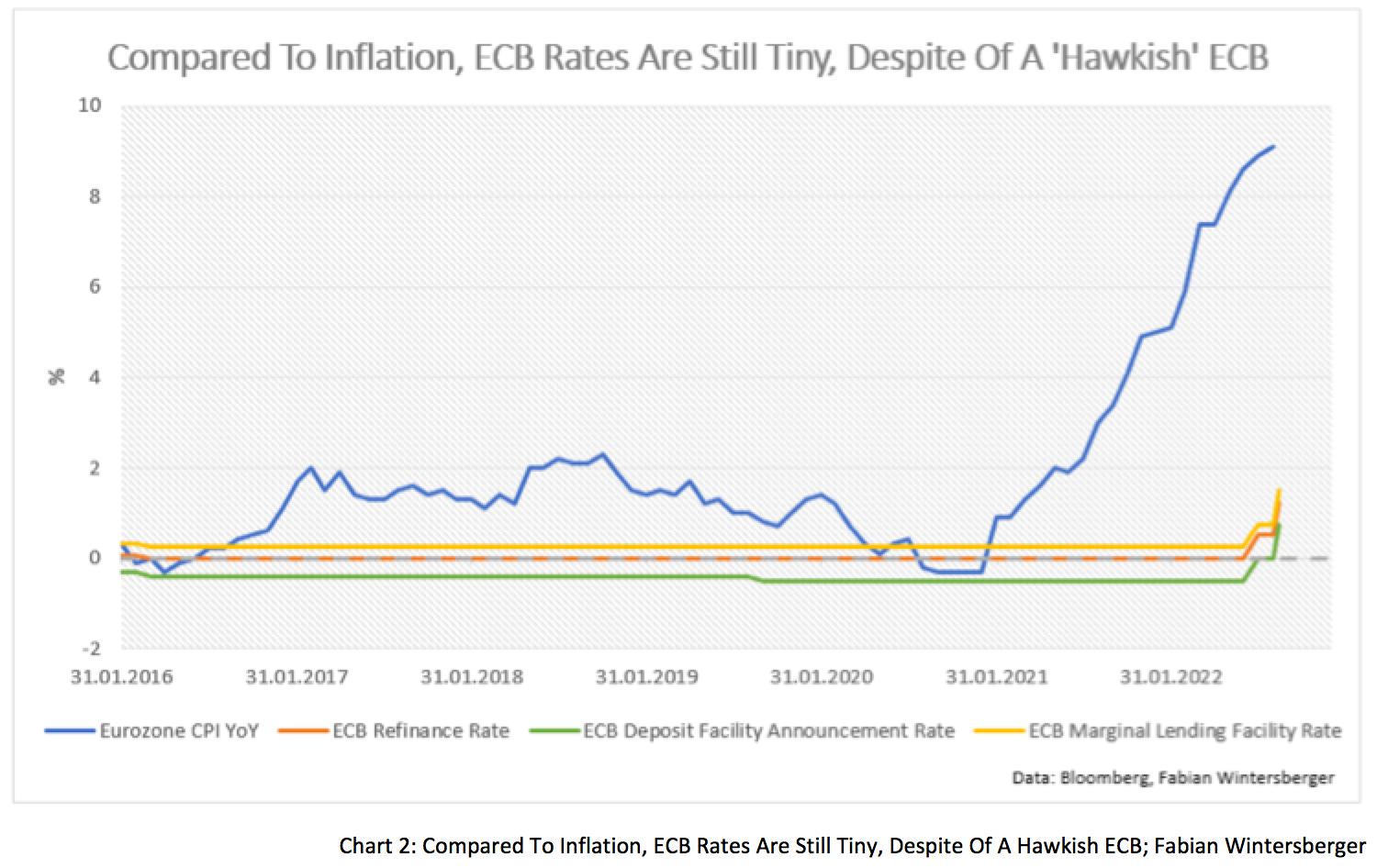

Let us start with the ECB decision from last week. As I assumed last week, the ECB raised all key rates, the deposit rate, the marginal lending facility rate, and the main refinancing rate by 75 basis points to .75, 1.50, and 1.25%.

Further, the ECB lowered its growth forecast significantly. For 2023, the ECB now expects only a slight GDP growth of .9 %, down 1.2 percentage points from July’s 2.2 % projection. That is as recessionary as it can get from a central bank.

In her press statement, Lagarde explained the ECB governing council’s decision and stated that

inflation remains far too high and is likely to stay above our target for an extended period. This major step frontloads the transition from the prevailing highly accommodative level of policy rates towards levels that will support a timely return of inflation to our two per cent medium-term target.

I cannot say that I have ever witnessed a press conference by Lagarde that was that hawkish. She noted that inflation is spreading, and although the ECB will decide meeting by meeting, one should not conclude that the ECB will stop to hike interest rates anytime soon. According to Lagarde, rates are still far from a level to bring inflation back to the ECB’s 2 % target.

So, we can conclude that several rate hikes from at least 50 basis points will follow at the next couple of meetings from today’s perspective, if not higher. Apart from Lagarde’s rhetoric, one could also conclude this because interest rates are still meager compared to inflation. So, if the ECB’s serious, it must do much more.

My hunch is that the ECB needs to raise interest rates until they are above the inflation rate. It will be interesting to watch whether the ECB can achieve that because doing so will lead to a painful restructuring process of the economy.

Now let us move away from Europe to the other side of the pond, where US inflation numbers for August were published on Tuesday.

On a year-to-year basis, consumer prices rose by 8.3 %; economists expected a decrease in the rate of change to 8.1 %. However, core CPI accelerated to 6.3 % from 5.9 % the previous month because falling energy prices mainly drove the disinflation of consumer prices.

The reason why energy prices fell is simply the drawdown of the US’s Strategic Petroleum Reserve, which the Biden administration uses to dampen inflation.

However, Median CPI and 16 % Trimmed Mean CPI from the Cleveland Fed show that price inflation is getting more broadly based. The times when Paul Krugman dismissed inflation fears as unfounded by pointing at those two numbers are long gone. Median CPI rose to its highest level since the beginning of its calculation in 1983.

After the numbers were published, US yields spiked again. The US 2y yield is now at its highest since 2007, and the 10y is back close to its June highs. Market participants now consider a 75 bps rate hike at the next FOMC meeting a certainty and an entire percentage point hike as possible. In my opinion, Jay Powell will not deliver any dovish message next week.

To sum it up, inflation will be here to stay way above the 2 %-target for longer, which is valid for Europe and the United States. Energy prices will remain higher than their multi-year average, and refilling the SPR might push them up again.

As expected, the high level of inflation, which is also partially driven by the war in Ukraine or, more specifically, by the sanctions policy pursued by the West, called politicians into action. With oversized fiscal packages, governments try to dampen the effects of it on their citizens, for example, still-Prime Minister Mario Draghi, whose Italian government readies another energy aid package worth about 13.5 billion euros.

Everywhere in Europe, there are discussions about windfall profit taxes for energy companies, which will probably be implemented at the EU level soon. To quote Ursula von der Leyen in her State Of The Union speech:

But in these times it is wrong to receive extraordinary record profits benefitting from war and on the back of consumers.

Further, von der Leyen announced that there would be discussions about the pricing system in the energy market, although one has to wait and see how this affects the current Merit-Order principle. Nevertheless, I am skeptical if the EU Commission thought about the unintended consequences of another interventionist policy.

Prices for X are way too high, is a famous saying in politics since its existence. However, it is a bit strange to hear it in times when elected officials always talk about the danger of rising populism. Friedrich von Hayek wrote in Road to Serfdom:

We shall not grow wiser before we learn that much that we have done was very foolish.

As we can be sure that politicians will intervene in price systems again, I fear we will again experience foolishness.

Of course, politics can set prices for specific goods through legislation. In this sense, the proponents of such policies are correct. Indeed, one should not fall for the illusion that meddling with the price system is without consequences. Probably, one cannot even estimate those because of the system's complexity.

Prices are essential signals of information within an economy. In a market economy, prices result from supply and demand and reflect preferences and scarcities.

Just to be clear, the neoclassical equilibrium price, as we know it from the supply and demand model, cannot be observed in a real, dynamic economy because the preferences and actions of actors constantly change and cannot be reflected in a static model. Further, in the model, there are no profits. In a market economy, an entrepreneur can profit if she recognizes disequilibria and produces more cost-efficient goods than other suppliers in the market.

To produce the good, the entrepreneur can combine several input factors. In a classical sense, these inputs are land, labor, and capital. Prices for those inputs signal how abundant or scarce these are for producers.

The price mechanism also influences the selection of raw materials for production. If a chair is made of wood or plastic depends on the costs and if they are below the expected selling price. Thus, the producer will choose the cheapest, most efficient production factors that satisfy her quality requirements for the final good.

Based on their subjective value judgments, the consumer decides to buy or non-purchase whether the price corresponds to their subjective evaluation or if he subjectively estimates the value to be even higher. If he comes to this conclusion, he will purchase the goods; if not, he will not.

If demand for a good goes up, producers are incentivized to produce more of the good. In an unhampered market economy where actors' preferences do not change, higher demand will lead to additional production until profits are back at zero.

Currently, we are experiencing rising electricity prices. In a free market, this would signal entrepreneurs that they can make additional profits by producing electricity and channeling more investment into the market for electricity production with low marginal cost.

Now it becomes evident that a constructed market price system will never be as good as one developed within markets. The European energy market has always been highly regulated, with lots of government intervention and market entry barriers. Or, as Daniel Lacalle wrote recently:

European power prices are not expensive by chance, but by design.

Politicians constructed the pricing of European electricity. We all know that European energy pricing follows the Merit-Order principle, and the marginal cost for the last unit of electricity needed dictates the price. While most electricity demand is inelastic, a certain amount will likely be purchased at any price.

As far as I understand it (and you are welcome to comment if I am wrong), the system was made to incentivize renewable energy production because producers could expect higher profits. The intention was to spur investment into renewable energy production.

Further, in my opinion, there is another catch. Producers can maximize profits by producing the last unit of electricity needed with the most expensive power plant. So, if 100 units of electricity need to be delivered, producers make the highest profit if they produce 99 units with the cheapest source of energy and 1 with the most expensive one.

As a result, my feeling is that the Merit-Order principle possibly leads to rising electricity production via renewables. Still, it is designed in a way that it will never lead to 100 % renewables if we assume that this would be possible (currently, it is not). Germany, the champion of renewable energy, has produced about half of its electricity this year with renewables and 14 % with natural gas.

Additionally, Merit-Order led to higher electricity prices and thus laid the foundation for the current problem. Prices are higher than in a free market, where the price is set by supply and demand. Assume there are two producers of electricity, A and B, and both offer electricity on the market.

If A's electricity price is below B’s, A will push B out of the market. However, if A cannot produce all the needed electricity, it has to buy from B. As a result, the price of electricity will be higher compared to a situation where A can produce the whole quantity demanded but lower if B’s marginal cost sets the price.

Nevertheless, if nation states put a price cap on consumer electricity, another problem arises because electricity can be traded like every other good. As soon as the price cap is implemented, electricity will be purchased from foreigners and exported, as the example of Spain shows. If more electricity is exported, it means less is available domestically. Further, a price cap would signal consumers that enough electricity is available and that there is no need to reduce consumption.

Interventionism and meddling with price discovery will not solve the market's underlying problems; on the contrary, it will lead to unintended, probably disastrous, consequences. Price controls did not work for agricultural production in the European Economic Community, they did not work for gasoline during the 1970s oil crisis in the US, and they will not work in the European energy market.

Can windfall profit taxes solve the problem? Although Ursula von der Leyen proposed them, I doubt this will help. On the one hand, this would subsidize consumers and thus will hardly lead to lower electricity consumption. If people get transfer payments for electricity, prices for other goods will rise because companies would have to charge higher prices for their products if companies are not subsidized. However, this would ramp up government refinancing costs in an environment of rising interest rates.

For producers, windfall profit taxes are also the wrong signal. If high profits incentivize producers to produce more units of a good, fewer profits will lead to less production of low-cost energy. While the EU plans to put a windfall profit tax on the fossil fuel industry, one can expect fewer or slower growing production. Current regulation has already led to a lower supply of fossil fuels because companies cut back on investments, resulting in a lower capacity.

The only solution to lower energy prices sustainably is to expand supply. Therefore, it should be evident that regulations and taxes need to be lowered, national energy sources should be developed, and companies should be incentivized to invest in the sector.

Sadly, politicians decided otherwise, repeatedly. I fear interventionism will fail again and will not lead to the desired ends. Being skeptical about Ursula von der Leyens’ statement that the EU plans to reform the energy market should be common sense. The more politics meddles with the price system, the more problems are created, and the more solutions politicians will present—the classical Cobra-Effect.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)