Master Of Puppets

Master? Master? Master?

After last week’s FOMC, the ECB holds its first meeting this year to discuss its future monetary policy. Everyone who knows a bit about financial markets knows that investors observe those meetings very cautiously because they hope to get hints about future economic developments and monetary policy. This post is not about yesterday’s policy decision since it was written before the ECB decision.

But central bank decision days are not only a challenging moment for markets. It also is a tough day for the chair of the central banks, like Jay Powell and Christine Lagarde. They have to choose every word wisely because one wrong word, one vague statement, and markets can get very shaky.

Their words lay heavy on market sentiment. They know that they move markets, and maybe it is why those press conferences become more and more meaningless. Even during the Q&A, it seems that the main task of a high-ranked central banker these days is to talk a lot without saying anything.

Apart from the ideal rate of inflation (which central banks set on their own) and (when it comes to the Fed), central banks have at least another crucial task: They have to guarantee a good sentiment among market participants, to make sure the can be kicked down the road for a little longer. Keeping this in mind, I often suspect that this has become the primary task for central bankers like Christine Lagarde and Jay Powell.

Just do not mess up economic sentiment!

It has been a while since central banks have made tough decisions. Unpopular decisions because it helps the economy to regain long-term strength. Long-term gain often comes through short-term pain, as we all know.

When Paul Volcker became Fed-Chair in 1979, US inflation was above 10 %. He was appointed by back-then US president Jimmy Carter, who told Volcker to fight inflation.

For years, former Fed chairs Arthur Burns and George William Miller had been too fearful in their monetary policy because they did not want to shake up the labor market. Back then, the Philips Curve was a sure thing, and everyone thought that there was a trade-off between employment and inflation. However, the 70s proved this theory to be wrong.

Nobody wanted higher rates because higher rates mean that the cost of credit rises. Politicians do not want higher rates because it hinders their ability to buy votes (social security spending), while businesses do not wish for tighter financial conditions. However, both fear economic turbulence.

The oil price shock caused inflation rates to skyrocket worldwide, and, against all odds, unemployment rose too. Today we all know this phenomenon under stagflation: weak growth, high unemployment, and high inflation.

Politicians got very old-fashioned to fight high inflation: President Nixon and later President Carter tried to bring inflation down through price controls, and they failed miserably. Whenever the price-controls got lifted, prices skyrocketed again.

After only two months on duty, Volcker acted right away and caused a significant downturn for the US economy. The dollar devalued, the economy shrank, and unemployment shot up into double-digit territory. It was a painful but necessary medicine to bring the US economy back on track. Volckers’ ambitious actions caused two brief recessions in the short term, but in the long run, it was one major factor to lay the foundation for the prosperous 80s and 90s.

1986 was Volckers’ last year at the Fed, and Alan Greenspan stood ready to take over in August 1987. Simultaneously, in 1986, the now US thrash metal veterans Metallica published their third full-length studio album, Master of Puppets. It was the last record with bass player Cliff Burton, who died in a car accident later that year.

The record title references people who are not in charge of their actions because a master is secretly moving them all in the desired direction. Interestingly, Alan Greenspan, who became Fed Chair in 1987, was called the Maestro later.

Under Greenspan, market participants became puppets. Greenspan (the Maestro) tried to influence their economic actions through his words, but in a different way than his previous statements on monetary policy would have suggested.

‚In absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value’

– Alan Greenspan (1966)

Greenspan was known as a hard money guy. He was in the inner circle of objectivist Ayn Rand (Atlas Shrugged), and his statements had been very critical about loose monetary policy until then.

People in charge change, and it became very apparent under Greenspan. The former Gold bug, who said that he was very nostalgic about the gold standard in 1978, changed his opinion soon after becoming Fed chair. As a result, he became a huge proponent of easy money.

Over time he mastered his ability to move markets in the direction he desired, and he quickly understood what had to be done to maintain the status quo—kicking the can down the road.

It only took two months for Greenspan to betray his own beliefs. His answer to the 1987 stock market crash was that the Fed would provide all the liquidity needed to support the economy and financial markets.

The Greenspan Put was born, and it became the Fed Put after Greenspan left office. It was a paradigm shift, as investors were not held accountable anymore for making bad calls because the Fed came to the rescue. However, the result was that investors got more and more risk-averse.

Greenspan’s loose monetary policy also led to higher investments into financial markets and diminishing real economic growth.

The dollar as a world-reserve currency also caused the Fed to save the Mexican Government. After the Fed raised rates in 1995, Mexican bonds got under pressure. As a result, American investors were in trouble because of their heavy exposure to Mexican bonds (To get re-elected, the Mexican government had issued a high amount of short-term debt in Peso, while it guaranteed investors that it would pay them back in US-dollars).

Only a 50 billion dollar bail-out (a laughable sum compared to nowadays), organized by Greenspan and President Clinton, could prevent further damage. However, in combination with further deregulation and the emergence of the New Economy, the next cut in interest rates laid the foundation for the dot-com bubble.

Although, these monetary policy measures also influenced the behavior of market participants.

On the one hand, a continuous fall in interest rates (that could never be raised back to pre-crisis levels) moved investors more and more out on their risk curve, and they took on more and more risk.

On the other hand, investors adjusted to speculate on potential backstops by the Federal Reserve and other central banks. Press conferences by the central bankers became more and more critical, and everyone tried to guess the possible market outcome.

One example is the Euro-crisis. After the GFC in 2008, southern European government bonds got more and more under pressure because, within the Eurozone, they could not regain competitiveness through devaluation. Simultaneously, debt levels in those countries rose, and they enjoyed much lower interest rates because they were part of the Eurozone.

But Draghi got it.

‘Within our mandate, the ECB is ready to do whatever it takes to preserve the Euro. And believe me, it will be enough’ - Mario Draghi (ECB), (July 26th, 2012)

It would have paid off heavily if one had placed a big bet that day. The demand for PIGS-government bonds increased enormously, and yields plummeted.

Right (or wrong) words can cause big moves in markets. Another example was Christine Lagarde in March 2020. When a journalist asked her about rising BTP-Bund spreads during the ECB press conference, she replied:

‘We are not here to close spreads, this is not the function or the mission of the ECB’ - Christine Lagarde (ECB), (March 12th, 2020)

Afterward, ECB chief economist Philip Lane had to ride out to calm down market participants and assure the market that the ECB will continue monitoring yield spreads from southern countries closely.

Additionally, besides getting more and more influence on financial decisions, how central bankers are influencing and moving markets has another effect: Big players who contact prominent bank officials repeatedly may be tempted to influence policymakers in their decision-making.

For example, in early 2021, the FT revealed that ECB chief economist Philip Lane had regular calls with Goldman Sachs, JP Morgan Chase, and Blackrock to discuss monetary policy decisions. Crooked…

While I would not criticize the banks and hedge funds to try to take influence (after all, this is just human). The problem here is (monetary) policy because they do not resist.

Further, I am not surprised that central bank press conferences become more and more meaningless, especially when journalists join them in a video conference.

Especially Lagarde looks like she is just repeating memorized phrases without any saying. A true politician, to 100 %.

Jay Powell seems to be a little more authentic, but even his answers to journalists are always the same. ‘Our policy can lead to this or that, and we as a central bank will do anything to be supportive to the economy, the labor market and to financial markets or something like that.

In my opinion, the tight relationship between big investors, big banks, and central banks is very problematic. I would not rule out that there is the possibility to front-run future central bank decisions.

For example, recently, Bill Ackman tweeted a lot on how the Fed needs to raise rates aggressively because they need to regain credibility within financial markets (I wrote about that in ‘Turning Point’).

However, Ackman is also a member of the Investor Advisory Committee on Financial Markets of the New York Fed and some other big hedge funds.

Last year, he gave a presentation where he laid down his central argument on why the Fed needs to tighten aggressively. Simultaneously, Ackman has accumulated significant payer swaptions since 2020 to bet on an interest rate increase.

And, what a coincidence, when the FOMC-minutes got published in January, US yields started to skyrocket, and Ackman closed his position.

Should things like this be possible? I think they should not. It is as if monetary policy is too close to big business, and small investors have a considerable disadvantage.

But probably, that is just how the current system works, and it works fine for big business and politicians like Nancy Pelosi.

Now that this piece is coming close to an end, I am not so sure who is the master and who is the puppets. Is it central bankers who move markets with their mere sayings?

Is it financial markets who try to guess future central bank decision-making and central banks are just reacting, especially when it comes to rate-hikes?

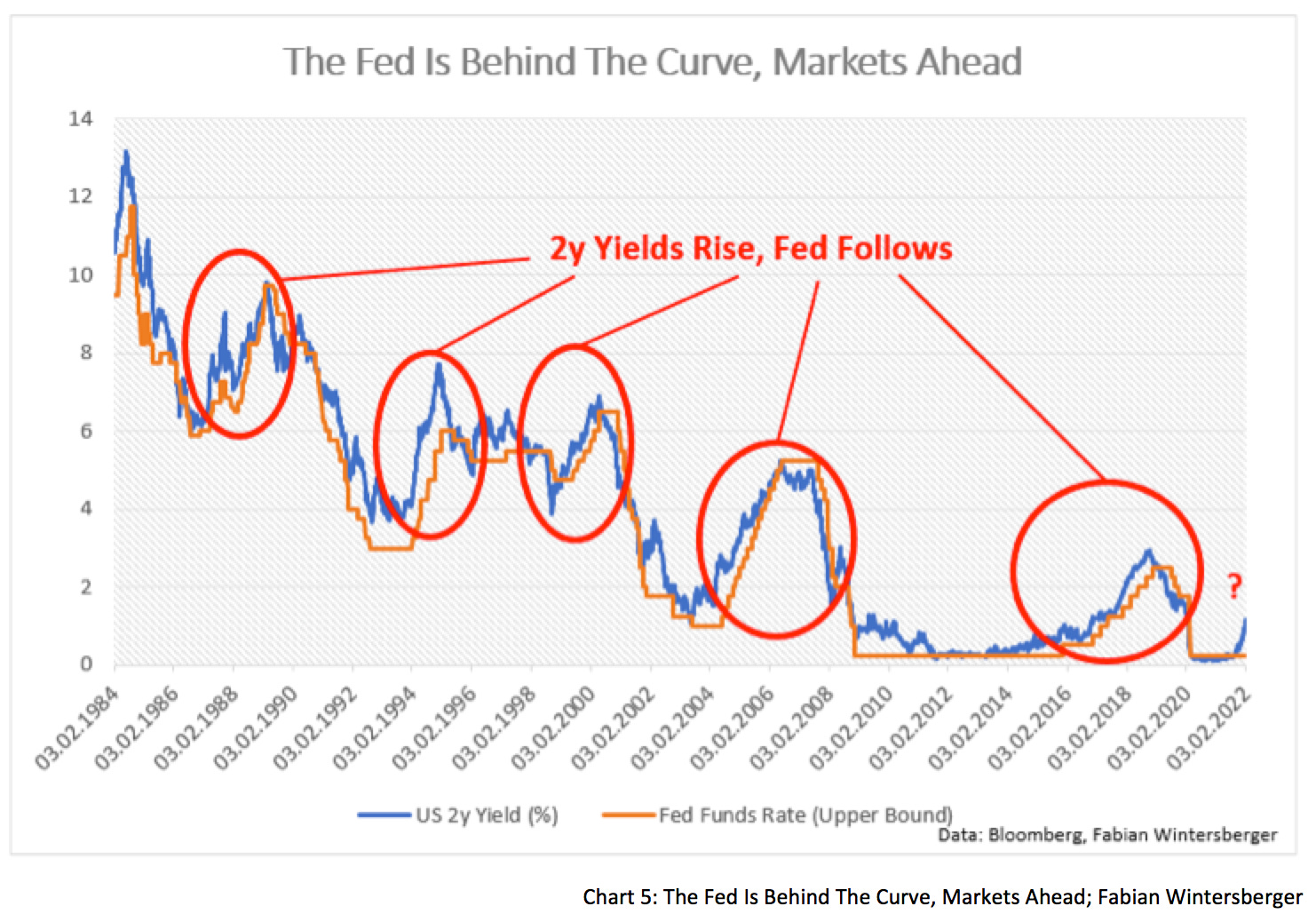

Nevertheless, chart five also shows that the Fed not necessarily raises rates as high as the market assumes, for example, in 1994. However, the current 2y yield implicates that there may be at least one or two rate hikes on the horizon (I'm afraid I still have to disagree with market expectations on that).

Or are the genuine Masters’ hedge funds and big banks who use all their abilities to influence the Fed and market participants? I will leave that question open!

‚Come crawling faster, Obey your master (Master)

Your life burns faster, Obey your Master!

Master! Master! Master!’ – Metallica, Master of Puppets (1986)

Have a great weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)