Live The Myth

It went differently than most observers expected: The conflict in Ukraine has turned into a war. The threatening gestures of the Russian bear were more than just saber-rattling.

In the early morning of Thursday last week, the Russian offensive began. The whole western world was in shock but impressed by the irrepressible will of the Ukrainian people to face the enemy and fight it. Overnight, president Selenskyj became a hero of the western world. After a brief phase of shock, the West begins to deliver war machinery to Ukraine.

At that moment, it is already clear that the West will impose sanctions upon Russia. Which one is still unknown, but Europe and the United States agree that it needs to be harsh, severe sanctions. Ursula von der Leyen says that there will be tough sanctions that will cripple the Russian economy.

First details reach the public: A block of Russian access to critical technologies and markets, a freeze of Russian assets, and no access to SWIFT for important Russian banks. Biden supports that idea.

Later that day, commentators criticized that the sanctions were not hard enough. As a result, the US and the EU reconsider imposing even harsher sanctions. Some unprecedented (at least on this scale) actions are discussed, as economic historian Adam Tooze reports in his Substack Chartbook #87. Sanctions against Russia, the Central Bank of Russia, and the West plan to freeze Russian FX reserves at the ECB and FED.

On Sunday, Ursula von der Leyen releases a press statement:

Under this package, important Russian banks will be excluded from the SWIFT system.

We will also ban the transactions of Russia's central bank and freeze all its assets, to prevent it from financing Putin's war.

The intentions of these actions are straightforward: To make Russia’s war as expensive as possible.

The extent of these decisions becomes apparent on Monday. The MSCI Russia lost 50 % of its value, and the Russian ruble lost 20 % against the dollar and the euro. The western sanctions have caused a Russian currency crisis.

Europe and the US have released their financial superweapon. However, this is also risky: Now China knows first-hand what would happen if it aims to expand its influence in the South China Sea, and they will look for alternatives if they have not already.

Another result is an explosion of wheat prices: Russia and Ukraine are Europe’s granaries and are responsible for more than 25 % of all global wheat exports.

The vast portion of these exports go to Africa, and thus the current war will probably lead to a lot more refugees who look for asylum in Europe than just the Ukrainians.

Although Russian energy exports are excluded from the sanctions, the situation in the energy markets is agitated. This Monday, European Natural Gas Futures reached a new all-time high at € 197.91/MWH. On the one hand, there is uncertainty whether Russia will continue to export oil and natural gas and, on the other hand, whether the Europeans will extend their sanctions to energy.

Nevertheless, it does not look as if president Putin is thinking about giving in. The big question will be how long the sanctions need to stay until he gives in. These sanctions are not only costly for Russia, but they are also for those who implemented them.

The Atlanta Fed has cut its GDP Nowcast to 0 % recently, which means that in real terms, the Atlanta Fed expects no growth in Q1. Simultaneously, inflation is running way above the Fed’s target of 2 % over the medium term.

Because of the slowdown of the economy that I had anticipated even before the war started, I expected inflation to peak in Q1 of this year and to come down to approximately 3 %. However, recent developments are a counter-argument against that.

At this point, I would like to clarify that I am not changing into the transitory camp, but I reject the idea that inflation is going up in a straight line. Inflation regimes come in waves, and this theory is supported by the last two significant inflationary phases of the 1940s and the 1970s. It is not that inflation will become deflation again, but that deflationary forces will take over in 2022, in my opinion.

For quite a while now, real wages in the United States have been falling and expectedly even more in Europe. As inflation eats away households’ purchasing power, their savings rate has to come down to keep the same standard of living.

At this moment, I still think that inflation will normalize a bit, even if energy prices rise further. Chart 3 is a rough calculation of how rising oil prices would affect the YoY change. To become inflationary, WTI would need to rise to 150 dollars.

The same is true for wheat. Wheat prices would need to rise above 1,500 dollars to continue to be inflationary, although the market would remain in an inflationary environment because of the latest spike. Though, I acknowledge that such prices are a possibility.

Western society is heavily supporting the government’s sanctions against Russia. Many companies announced that they would stop exporting goods to Russia or halt production in Russia. The result will be lower revenues for those firms. Now it depends on the duration of the sanctions. If they need to stay in place for longer, the businesses’ self-sanctioning may lead to more unemployment at some point. This would be genuinely disinflationary.

On the other hand, central banks are caught between a rock and a hard place (I know, I am repeating myself). Many analysts on Wall Street had expected the Fed to raise interest rates seven times this year (some even talked about 11 hikes in a row). Even at the beginning of the year, these expectations were pure illusions.

Most market participants even talked about a high probability of a 50bps rate hike in March. Powell himself denied that this Wednesday in front of Congress, saying that he supports a 25bps rate hike if inflation does not prove to be more persistent for longer than the Fed anticipates.

Recent numbers suggest that inflation may be here to stay because of the war. On Thursday, Eurozone PPI numbers showed a 30.6 % increase YoY and a 5.2 % MoM rise (exp. MoM increase: 2.8 %). The ongoing economic war makes it hard to make a long-term prognosis.

Powell also stated that there would not be a direct effect from the Russian sanctions on the U.S. economy. However, looking at oil imports from Russia shows that the U.S. is importing a lot more Russian oil than it did back in the early 2000s. Nonetheless, as the amount is still a tiny proportion of US oil, I think that this is still manageable.

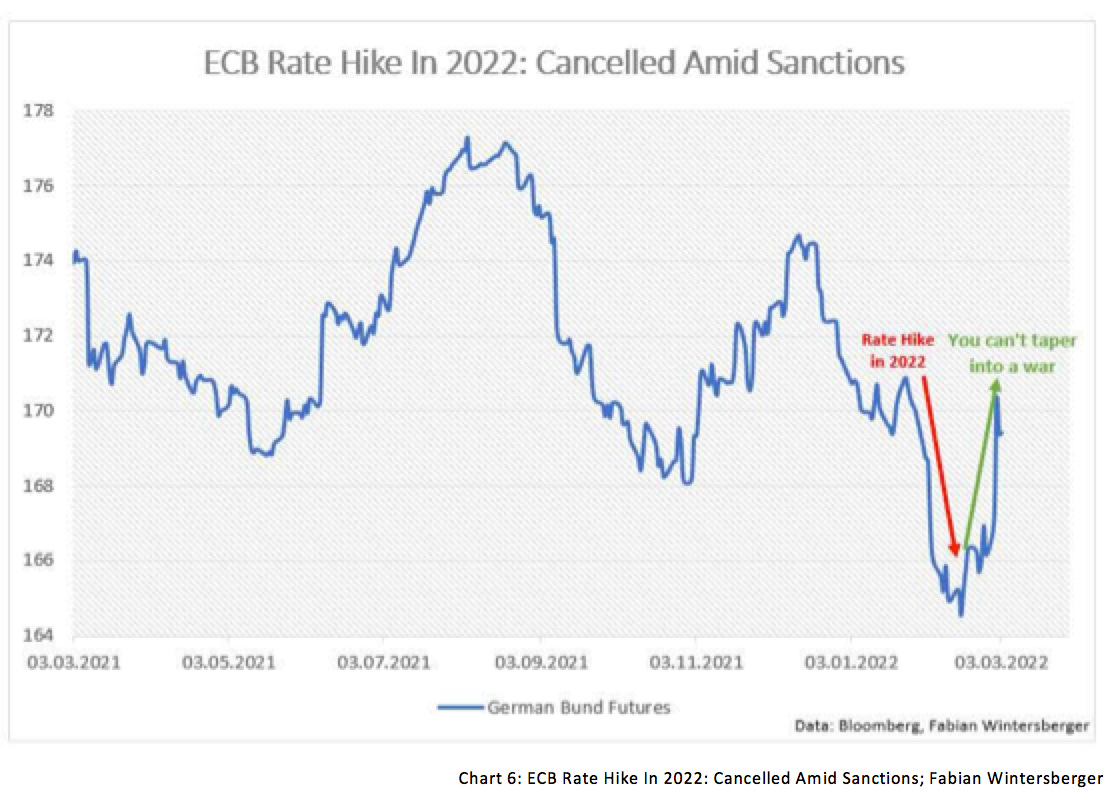

In Europe, the situation is clear, and an ECB rate hike in 2022 is undoubtedly off the table. Recent uncertainty caused investors to rush into save-heaven assets like German Bunds, despite continuously high inflation.

When the sanctions were announced, they caused long queues in front of ATMs all over Russia, with many of them running out of banknotes. With the exemption from SWIFT, the only way for ordinary people to transfer money to western countries is through crypto.

However, Bitcoin and Ethereum also play a role when it comes to financing Ukraine:

If we move towards a period of stagflation, will it be the end of the low-interest rate environment? Not necessarily. High debt levels of governments, businesses, and households made economic actors extremely vulnerable to higher rates. To pull a brake on inflation, one needs to raise interest rates above current inflation rates drastically.

However, I think that it is unlikely that central banks will raise rates to solve our long-term economic problems, as it is way too painful. Much likelier, the theory of Russel Napier will play out: governments will force institutional investors to buy government bonds at a negative real rate to keep rates low. Everything will be blamed on the war, even though the economy was already stagnating before. In the 1970s, the Fed blamed inflation on high oil prices (although inflation started in the mid-60s). In the 2020s, inflation may be blamed on the new cold war.

But, could our sanctions backfire? What happens if Putin does not give in and we have to keep them in place longer? It seems that we have tried everything we could to make war as expensive as it can get. The West confiscated a vast proportion of the Bank of Russia’s reserve. The only reserves available are the ones stored somewhere in Moscow: gold.

But gold is hard to use as a form of payment? Well, not necessarily, as Zoltan Pozsar from Credit Suisse pointed out in the latest Odd Lots Podcast from Bloomberg. Theoretically, he said, Russia can just repo its gold reserves with a central bank willing to do so. So, if the Bank of Russia finds another central bank ready to hand them dollars in exchange for gold repo, Russia can get dollars.

The latest trump of Europe and the U.S. probably is to stop all energy imports from Russia, but this would be very costly for them as well. Germany would need to have finished the installments of LNG towers already, and there need to be suppliers who ramp up their deliveries. As Europe wants to speed up the green transition, there is another problem: Most renewables are produced in China. In the current economic environment, greenflation is one of the things you do not want to have, though.

China and Russia already implemented an alternative to SWIFT. Do they also work on a new monetary world order? On February 28th, Russia announced that it will continue to buy physical gold on the domestic market. Nevertheless, the probability of a change in our global monetary system has risen since last week.

At the beginning of the year I had two main theses:

The economy will slow and thus long term duration bonds will rise in value. I still hold that view, despite recent inflation surprises.

The dollar will gain value against the euro throughout 2022. The trend will continue, in my opinion.

My prognosis about the conflict in Ukraine from two weeks ago was wrong, along with my thesis that Russia is used to sanctions and thus cannot be hit hard. It turned out to be a myth. That’s life on the trading floor: sometimes you are right, sometimes you are wrong.

Central bankers and politicians, according to their definition, cannot be wrong: they Live The Myth!

Have a great weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)