Liars & Thieves

To be led by a liar is to ask to be told lies. — Octavia E. Butler

The market remains a news-driven machine front-run by flows. And so far, the Trump administration still manages to steer market pricing despite making little visible progress in negotiations with Iran. I have lost count of how often Trump, or any news outlet quoting a “person familiar with the matter,” has announced that a deal with Iran could be close.

What matters, however, is that markets continue to react to it. Wednesday brought another Axios headline and, once again, oil collapsed while equities and bonds rallied. Of course, one can debate whether that is just another lie, half-truth or simply wishful thinking. But regarding price action in markets, this is secondary. What matters for portfolio managers is the P&L. And therefore, although the situation remains unclear, I’d like to remind you of what I wrote in my market assessment on April 17:

With markets pricing marginal improvement in the Middle East, the setup for equities has shifted. In the short term, the pain trade remains higher as long as the situation does not deteriorate. Momentum suggests the potential for new highs.

Combined with the bullish fundamentals discussed last week, it should not be surprising that markets continued to trend higher. More “peace headlines” like Wednesday’s simply accelerate that move.

The ECB’s “Hawkish Hold”

Last Thursday, the ECB delivered what was effectively a hawkish hold. While rates were left unchanged, Christine Lagarde made it very clear that a hike was seriously debated and that the Governing Council increasingly sees the euro area moving away from the baseline scenario. The central issue remains the war-driven energy shock. Lagarde repeatedly emphasized the “duration, depth and propagation” of higher energy prices and their potential spillover into broader inflation through supply chains, wages and selling prices.

What stood out most was that the ECB increasingly appears to view this as a classic negative supply shock rather than something it can simply look through. Unlike the Fed, which still seems relatively comfortable tolerating some energy-driven inflation, the ECB sounded much more concerned about second-round effects becoming entrenched. At the same time, Lagarde acknowledged that financial conditions have already tightened and that growth momentum is slowing. The ECB therefore decided to buy time until June, mainly because policymakers still do not yet see meaningful second-round effects in wages and underlying inflation data.

Still, the direction of travel was fairly obvious. Lagarde explicitly said that “directionally, I know where we’re heading,” which markets will likely interpret as a signal that hikes remain the default path unless there is a rapid de-escalation in the Middle East and a reversal in energy prices. The ECB clearly believes it entered this shock from a relatively strong position, but the longer the war and the energy squeeze continue, the more likely it becomes that inflation pressure broadens out into the rest of the economy.

Here, I can only reiterate that additional ECB hikes carry substantial risks for an already fragile euro area economy. This week’s S&P Global PMIs showed that among the major euro area economies, only Italy still appears to be on a path of expansion. France, Germany and Spain all point toward decelerating activity.

That ultimately shows the ECB’s dilemma. Yields are already restrictive, yet a prolonged war in the Middle East could still push prices materially higher. At the same time, rates at current levels or above may increasingly become a drag on growth, potentially creating the conditions for a stagflationary environment, regardless of whether Lagarde wants to use that term or not.

Yet the euro area’s low-growth problem remains primarily structural rather than monetary. Excessive regulation, weak productivity growth and increasing state intervention continue to weigh on private sector dynamism. Over time, those inefficiencies will likely spread into the very government-driven growth engines many analysts are now hoping for, namely defense spending and infrastructure programs.

My stance remains that these programs will primarily lead to rising debt levels while producing only limited improvements in long-term productive growth.

Money Creation Through Collateralization

With the central bank decisions behind us and my assessment of the continuous divergence between Europe and the United States, I think it is a good time to take a step back and discuss the dynamics driving these developments.

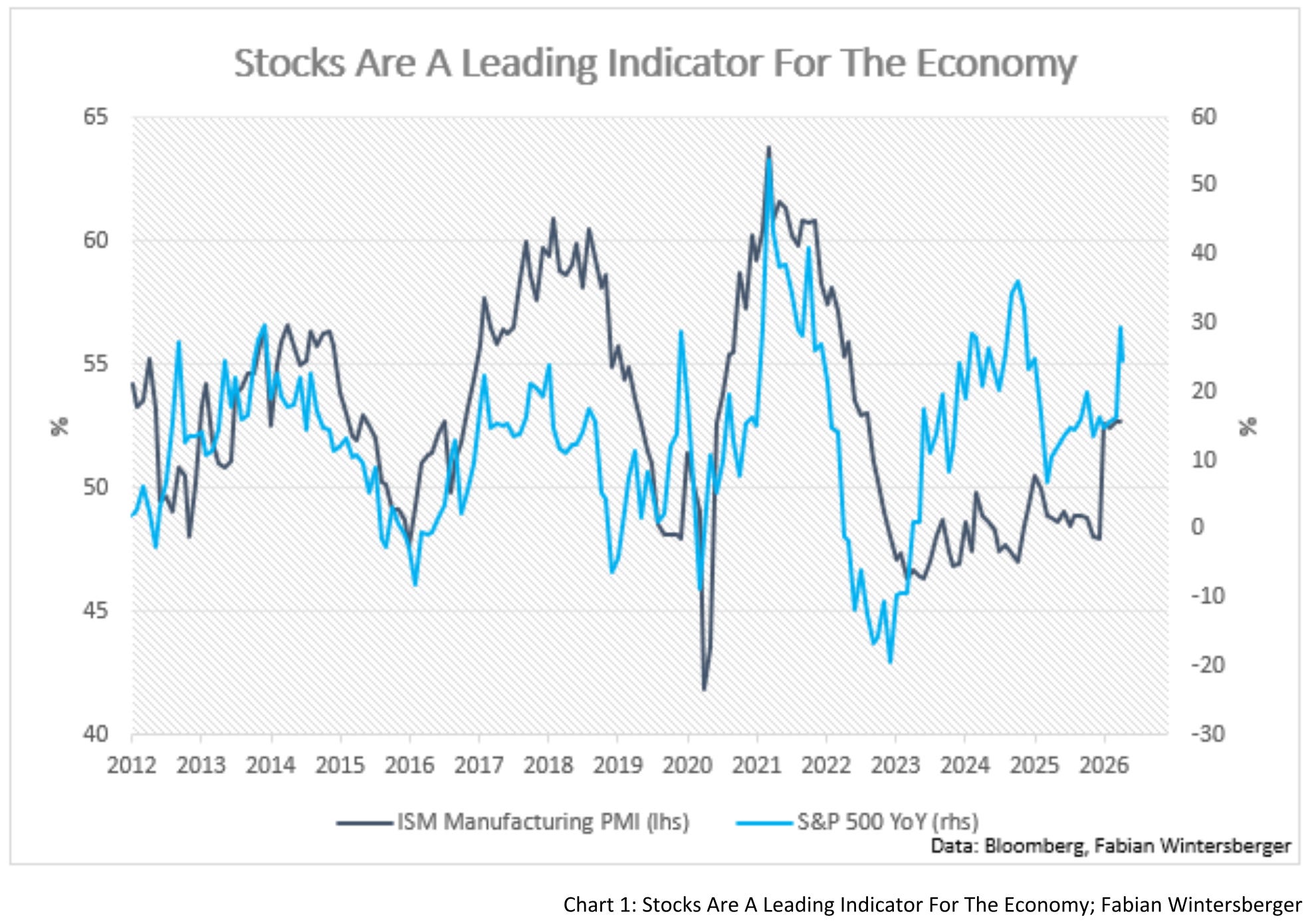

Last Friday’s US ISM Manufacturing numbers illustrate that divergence rather well. Despite coming in below expectations, the headline number still points toward solid economic expansion. I continue to argue that the stock market is a leading indicator for economic activity because rising asset prices loosen financing conditions and expand collateral values. Therefore, the continued strength in equities points toward stronger nominal growth ahead in 2026.

That should not be surprising. The driving force behind nominal economic activity remains the creation of money in the broader sense. Within the current monetary system, the dollar remains the central driver. At the top of the monetary pyramid sits cash and bank reserves. The layer below consists of credit money, money created through the channel of bank lending.

Here, however, I would emphasize a point that traditional discussions of monetary theory often underappreciate: the reflexive role of stock prices in the process of credit creation. Rising equity valuations expand collateral capacity and therefore expand the ability to borrow. Lending is not merely extended through the rollover of existing debt. It can also expand because appreciating asset prices improve balance sheets and financing conditions.

A highly indebted company can therefore continue funding operations and prolong unprofitable expansion as long as rising equity valuations keep financing channels open. Increasing market capitalizations strengthen access to credit markets, allowing firms to refinance obligations, raise additional capital and continue expanding business operations.

AI companies are a perfect example of this dynamic. While the actual integration of AI into productive business processes remains limited in many areas of the economy, investor appetite for the sector continues to drive equity valuations sharply higher. That strengthens firms’ standing in financial markets and expands their ability to borrow and invest. As a result, companies continue to hire, expand infrastructure, and build consulting and service businesses around AI implementation.

Anthropic’s announcement on May 4 is one example of this process in motion:

Anthropic, Blackstone, Hellman & Friedman, and Goldman Sachs announced the formation of a new AI services company. The organization will work with mid-sized companies across sectors to bring Claude into their most important operations.

The continuous expansion of credit remains the driving force behind money creation. And as long as investor capital continues flowing into equities, companies can keep expanding their balance sheets and channel a portion of that expansion into the real economy. That also means that the level of interest rates is secondary for money creation. What matters more are the underlying financial dynamics driving collateral expansion and credit growth.

Given that credit creation continues to expand, as discussed last week, more liquidity is being created by rising financial valuations, which support additional borrowing. With the dollar at the center of the global monetary order, the dollar remains the driver of global liquidity and capital flows. Money continues flowing into the United States because Europe’s regulatory burden increasingly makes private investment unattractive without government subsidies.

The European defense sector may experience a revival through state spending programs, but private capital continues to look elsewhere for returns. As a result, demand for euros may remain somewhat elevated relative to a scenario without defense expenditures, but the center of private-sector dynamism remains firmly located within the dollar system, namely the United States.

And given that energy remains among the most important input factors of economic activity, the fact that it is priced in dollars, combined with the fact that global trade still largely operates through the dollar system, creates a structurally dollar-centric investment environment that favors the United States. Trump’s industrial policies further reinforce this dynamic by creating a relative improvement in industrial competitiveness within a financial architecture that already channels global capital toward the US.

Therefore, the Trump administration effectively has to pursue a strategy of keeping stocks elevated and rising. This environment increasingly resembles another fiat-driven credit boom supported by government policy, subsidies, and a more active role of the state in directing economic activity. At the same time, the global energy crisis strengthens the United States' relative geopolitical and financial position within the international monetary order.

That is what is increasingly reflected in the overall macroeconomic data and, as I argued last week, suggests that the Federal Reserve is already operating below the natural rate for the broader market. I think many bears are wrong in assuming this is the final stage of the boom. In my view, this is increasingly the beginning of a new boom, building on an unfinished recovery phase that continues to support both equities and broader business activity.

The side effect, however, is the uneven distribution of this boom. Credit creation, just as Richard Cantillon described with the gold miners of his time, benefits those who receive the newly created money first, while those receiving it later suffer from the consequences of rising demand for goods, services, and financial assets: higher prices.

What will become increasingly important to observe is how the situation evolves for the broader public in the United States. They are the ones experiencing the pressure from inflation and from wages that often fail to keep pace with broader cost-of-living measures such as housing and grocery prices, despite seemingly solid nominal wage growth. Those with substantial stock holdings are either accumulating wealth or at least preserving their purchasing power.

That is ultimately the political constraint Trump’s policies face. A loss in the midterms, which currently appears quite plausible, would significantly reduce the administration’s ability to continue pursuing this policy mix. Until then, however, both the capital misallocations and the average economic prosperity generated by the boom remain supportive for the US economy and its stock market.

Some capital will inevitably flow back to Europe, supporting export-driven sectors and their equity markets. But the center of collateral expansion, credit creation and private-sector dynamism remains the United States.

Market Assessment

My market assessment remains broadly unchanged from last week, with stocks being favored over bonds and commodities, mainly oil, serving as a better hedge for stock market drawdowns than stocks themselves.

The recent sell-off in oil, driven by Axios's report of a potential agreement between the US and Iran, reinforced that dynamic. It is no surprise that this also helped the euro relative to the dollar. As long as no deal is closed, however, EUR/USD is likely to remain within its 1.17-1.18 range.

Gold also profited from the news but, in my view, remains rather weak. Over the longer term, I remain favorable toward gold. Bitcoin also managed to rise above $80,000 and remains in a bullish trend, as already noted last week.

Conclusion

With the pain trade still pointing higher and the market taking any positive news at face value while hardly repricing it if those headlines prove untrue, it remains favorable to focus on flows and economic data. Neither suggests that the bears, despite seemingly representing the majority, are getting their will.

Money creation continues amid rising stock prices. And the underlying economic forces are fueling a further extension of the rally until “value investors” finally give in and join the buying. Fundamentals matter in the long run, but at times they can drag on investor performance. Currently, I think they are, and sentiment beats fundamentals once again.

You might call the current price action one of “liars and thieves,” but if joining the rally makes you money, who are you to judge?

Friendly fire

Truth is a thief

Faith is a liar

Get out of hell if you can’t take the heatArch Enemy - Liars & Thieves

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.