Let The Tempest Come

The situation in global financial markets and the real economy remains tense. For another week, the most discussed topics have been the unfolding energy crisis that the war in Ukraine has further exacerbated, the rise of interest rates, and the looming stagflationary environment.

Since the Grand Financial Crisis, inflation has been considered a problem of the past, and central banks desperately tried to reach their inflation goal. When consumer prices finally began to rise in 2021, all central banks dismissed concerns and insisted that the rise in prices was due to transitory phenomena. However, at the beginning of this year, it became apparent that central banks have badly miscalculated. As a result, they faced rising pressure from the public and politicians.

While the Fed and the Bank of England already started to tighten monetary policy around the turn of the year, the ECB has been very cautious and tried to remain patient. Nevertheless, the consequences of Russia’s invasion of Ukraine threw a spanner in the plans of the ECB.

Since then, several statements from ECB officials have confirmed that the ECB has changed its course since then. Even the doves in the ECB’s governing council are now saying that the ECB should start to raise rates by July. After the PEPP (Pandemic Emergency Purchase Programme) ended in March, the ECB plans to phase out the APP (Asset Purchase Programme) at the end of the third quarter, which started in 2019, according to a blog post from Christine Lagarde on the ECB’s website.

In the post, Lagarde tried to outline the next steps of the ECB’s monetary policy, presumably to prepare market participants for it. Lagarde confirmed the statements of other governing council members that the ECB will indeed start to raise rates in July.

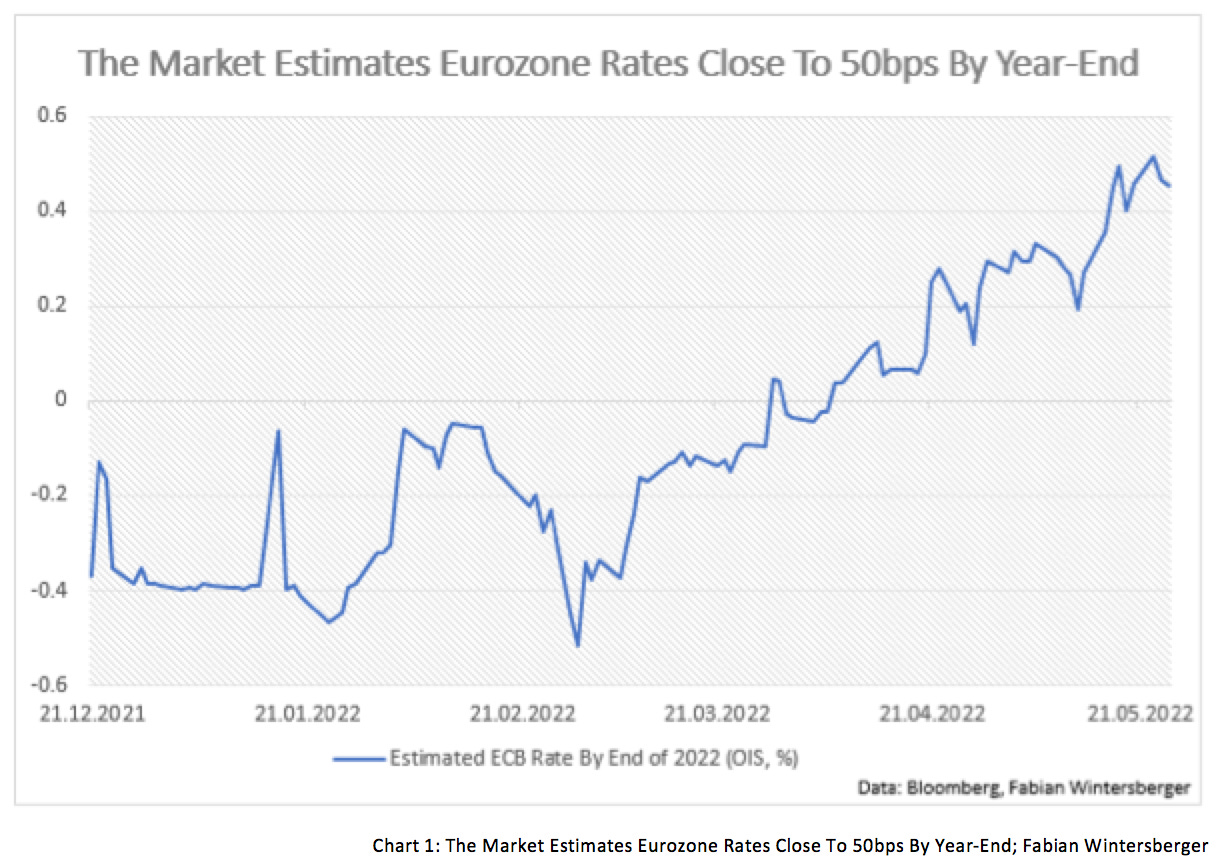

Market participants now expect that the ECB will raise rates to around +50 basis points until the end of the year, while in March, they were still expecting negative rates at the end of December. However, starting at the ECB’s March meeting, the rhetoric changed and became much more hawkish. Lagarde affirmed that the ECB plans to raise rates above zero in September in her blog post.

If the ECB will stick to plain, as markets are thinking, remains unknown for now, primarily because it reacts much slowlier than the Bank of England or the Federal Reserve.

Meanwhile, Lagarde participated in this year’s annual meeting of the World Economic Forum in Davos, where she told Bloomberg that the ECB would not rush into withdrawing stimulus.

Previously (also in Davos), Banque de France governor Francois Villeroy told the press that there is no consensus about a 50 basis point rate hike within the governing council. The ECB plans to adjust monetary policy gradually, Villeroy said. In the blog post that I have mentioned above, Lagarde also announced that the ECB plans to normalize policy cautiously and that adjustments will be guided by the prevailing economic environment at the time.

Monetary policy is difficult in the current economic environment because a large proportion of price increases are due to constraints on the supply side, where central banks’ decisions have hardly an influence. A more restrictive monetary policy is designed to bring down (excess) demand, as correctly noted by several governing council members. Central banks can bring down demand, but they cannot print goods and services, and hence demand-oriented economists (Keynesians) are skeptical about rate hikes. In my opinion, the ECB is acting with patience because it worries that a fast tightening might stall the economy.

Currently, strong price inflation in the energy sector is spreading throughout the economy, probably already causing diminishing demand because budget constraints force households to limit consumption. However, it is not true that the ECB cannot be held accountable for the recent price spike because the whole world economy suffered from problems on the supply side. Still, some countries, for example, Switzerland, did not ease that much and faced much lower consumer price inflation than the Eurozone.

In contrast to the United States, real rates remain profoundly negative in the euro area despite the latest rise because of falling inflation expectations. Market participants possibly already expect weakening price inflation because of an economic downturn.

While the ECB is trying to fight inflation, fiscal policy in eurozone countries goes in the opposite direction. It actively counteracts those attempts, as they are trying to cushion the impacts of inflation on low-income households via fiscal expenditures. Especially debt-champion France plans to spend close to 2 % of its GDP on such measures.

Another problem is that the ECB plans to tighten much slower than the Fed, and this might also put pressure on inflation rates because one can expect that the euro will continue to devalue against the dollar and commodities will get more expensive for countries of the Eurozone because they are priced in dollars.

The sanctions that Europe and the United States put in place against Russia have started to show some results. While in financial terms, Russia has enjoyed a rise in income from oil exports, oil production in Russia has dropped, and hence the total supply of oil is falling. However, the ongoing relaxation of China’s lockdown policies and the White House’s plans to refill the SPR will keep oil demand elevated, suggesting that the rise in the oil price is far from over.

Hopes that other oil producers will be able to compensate for the fall in the supply of Russian oil are not valid. OPEC is running out of spare capacity and shows the disastrous consequences of years of low investments because hardly anyone wanted to invest in an environment where the west has pushed for the green revolution.

Although the problem in spare capacity is coming up now, policymakers could have noticed it quite some time ago. In September of 2021, Josh Young wrote about it in his article The Myth of Opec Spare Capacity.

Meanwhile, the US is planning legislation that would enable the government to open an anti-trust case against OPEC. UAE energy minister, Suhail al Mazrouei, warns that the proposed bill could push oil prices by as much as 300 %.

But it is not only the oil market where the situation remains tense. The same is true for the natural gas market. As the EU plans to cut Russian gas imports by two-thirds, demand for LNG rises. According to Bloomberg, this might trigger a supply crunch in the LNG market in the coming winter. The lack of spare capacity plays a role here as well.

A storm is brewing in the economy as an inflationary spiral spreads from energy markets meets shrinking liquidity (due to restrictive central bank policy) in an already negative economic sentiment. High debt levels of advanced economies are narrowing the scope for governments.

For the last decade, the situation in the Chinese economy has been a leading indicator for the US economy. The coming months might be sobering for the US if we look at China’s PMI.

If the Fed does as it says, it will tighten monetary policy much faster than the ECB. As I noted two weeks ago, several indicators suggest that the US consumer is not as strong as it seems. Moreover, it appears that US consumption remains elevated because people ramp up credit card spending. In a rising interest rate environment, this could end very abruptly.

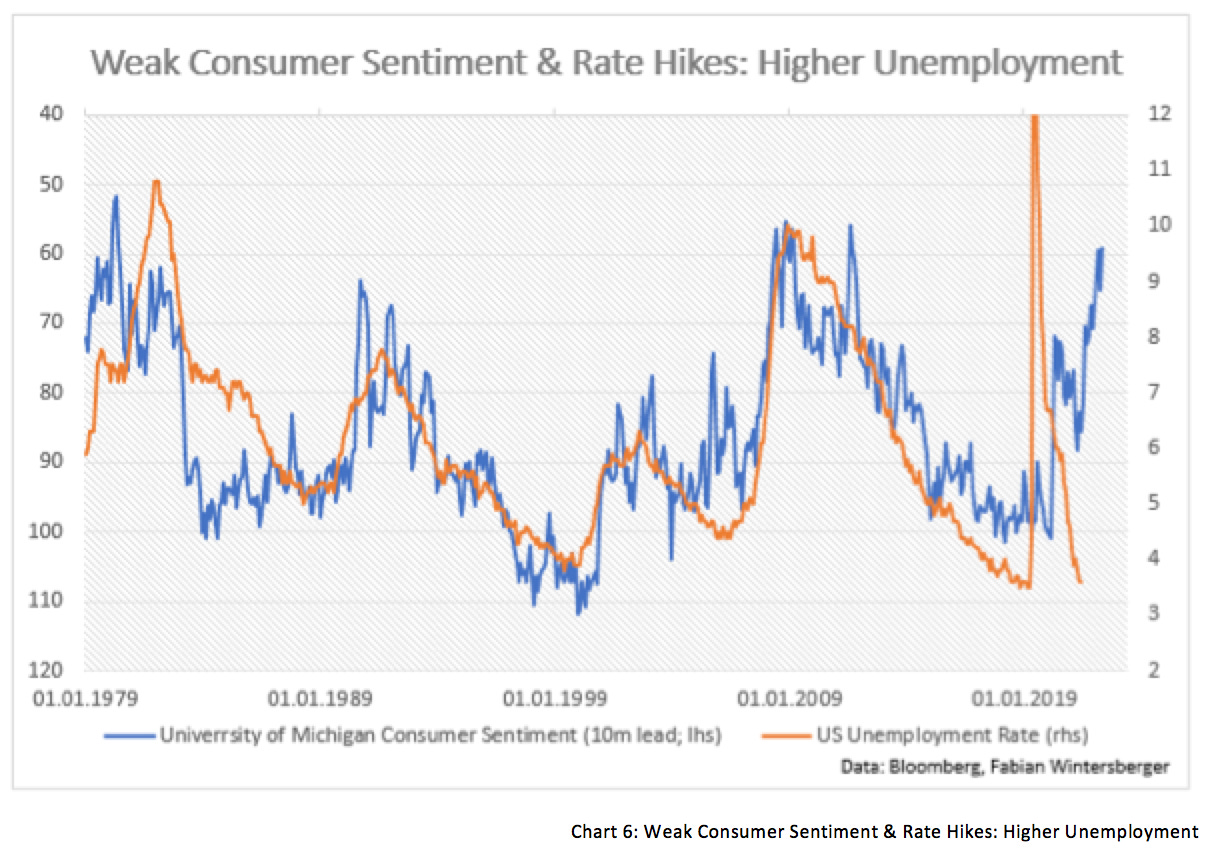

Weak consumer sentiment in the US supports this argument. In the future, the US might face a rapid rise in unemployment. Falling consumption levels lead to declining revenues for businesses, and as a result, job cuts will probably follow.

While the real economy is slowing and points to a possible recession later this year or next year, there is another problem: rising pressure in our global financial system. This week, investors parked more than 2 trillion dollars at the Fed’s reverse repo facility. The widespread assumption is that investors have been drowned in liquidity since 2020 and do not know what to do with it. However, a different explanation might be that there is some fear of systemic risk because interest rates have been held artificially low for too long.

In Desperate Times, Desperate Measures, I mentioned that the US treasury announced the issuance of fewer Treasuries than market participants had anticipated. Regulation obligates Banks to hold a part of their reserves in Treasuries, and they need it for derivatives trading as collateral.

Collateral was a problem during the Great Financial Crisis as well because banks suddenly realized that, apparently, those AAA-rated MBS were not as good collateral as they initially thought. Banks did not accept them as collateral from their counterparties anymore and asked for more secure collateral, such as T-bills. That caused the price of those T-bills to spike. Because of that, some people say that the problem was not sub-prime; it was the absence of good collateral that resulted in a global dollar shortage.

Today, one can observe a similar anomaly. Yields of 1m T-bills trade at a discount (higher price) than the Fed’s reverse repo rate (Jeff Snider explains this much better in this video with Emil Kalinowski). If it were only about investment decisions, no one would accept a lower yield/higher price for a 1m T-bill if one could earn more for just parking the cash at the Fed. That might be a sign of another shortage of collateral and that another systemic risk event might come up in the future.

All those things suggest that the storm we are currently facing in markets is just the beginning. The war in Ukraine, a rising interest rate environment, energy costs that subdue the outlook for the real economy, and finally, signals of stress in financial markets imply that there might be tough times ahead.

I think that we already see the beginning of a shift in the narrative. Away from yields will rise indefinitely to oh my god, growth is going to crash down. Probably the latest consolidation in longer duration yields points to the possibility of a coming drop in yields. However, it needs another catalyst that this will happen, either a dovish shift from central banks or a spike in negative headlines in the financial media. Overall, the situation in the bond market remains challenging, and things could play out in both ways (bullish/bearish).

As a fall in economic activity becomes more evident, a correction in commodity markets is also probable, although I still think that over the medium-/long-term, commodity prices will climb further. In the short run, however, pullbacks are possible.

In the stock market, I do not see signs that the latest turbulences are over and hence expect that the main correction has not even started yet. Bad earnings from consumer staples are another sign that inflation has already led to some destruction of demand and that demand is close to falling from a cliff.

In the eye of the storm, cash will continue to be meaningful. And patience. In this spirit: LET THE TEMPEST COME!

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)