Legendary

(Note: the article was written on Thursday, March 3)

In 2020, Incrementum AG published a special of its yearly published In Gold We Trust Report, titled The Boy Who Cried Wolf. In the report, the authors Ronald Stoeferle and Mark Valek expressed their thesis that inflation will return in the years to come.

The title refers to an old fable of the same name, in which a young shepherd boy is guarding over sheep. Jokingly, he starts to cry wolf repeatedly, but every time the locals rush out to help the boy to fight the expected wolf, they discover that there is no wolf around, and they return to the village. The authors analogize that part of the fable with repeated warnings during the 2010s that zero percent interest rates and Quantitative Easing would end in a rise in consumer price inflation.

However, when the boy meets a pack of wolves and cries wolf again, the locals do not respond because they assume that the boy is joking again, resulting in the wolves killing all sheep.

As we know today, Stoeferle and Valek’s thesis was correct. When consumer price inflation started to pick up in 2021, warnings that inflation had returned were largely ignored. Everyone remembers statements from central bankers in 2021 that the rise in consumer price inflation would be transitory or that inflation looks like a hump that will eventually come down in 2022.

However, as soon as it was evident that the path of consumer price inflation was not a return to 2 %, the Fed reacted and started to raise interest rates throughout 2022, something hardly anyone expected at the year-end of 2021. The Federal Reserve never hiked interest rates at such a pace in the last 40 years, and the eurozone even experienced the fastest increase in interest rates in the history of the ECB.

While The Boy Who Cried Wolf, a fable from ancient times, perfectly described the development of consumer prices in 2021 and 2022, the current economic environment reminds me of a screenplay from the 1950s.

In 1953, the Bavarian Radio Bayrischer Rundfunk played a screenplay called The Arsonists (orig. Biedermann und Brandstifter), written by the Swiss Max Frisch. In the first scene, the wealthy businessman Gottlieb Biedermann reads reports of a series of arson attacks in the newspaper.

The actions of the perpetrators are always the same. Disguised as peddlers, they nest into the houses of their victims and then burn them down soon after. A few moments later, Mr. Schmitz knocks on Biedermann’s door, and Biedermann allows him in and shelters him in the attic. The next day, Biedermann also allows Schmitz's comrade Eisenring to move in.

Although Biedermann’s wife is begging her husband to throw them out repeatedly, Biedermann cannot, even as he discovers that Schmitz and Eisenring have stored several petrol barrels in his attic. In his fear that the two men will do something to him or his family, he also helps them to measure the correct length of the fuse.

When the Biedermanns and their guests are eating dinner, they hear sirens, and at first, Biedermann is relieved that it is not his house that is on fire. However, Eisenring explains this is to lure the firefighters away from the actual fire. Ultimately, Biedermann even hands them the match, which is used to set his house on fire.

According to the usual interpretations, the story refers to the rise of Communism in the Czech Republic or German National Socialism. However, the story also shows that considering something for sure that is obviously not true can have severe consequences.

Proponents of the theory that the Fed is making a policy mistake by raising interest rates further point to the negative rate of change of the M2 money supply on a year-over-year basis, which is contracting for the first time since the data was first published in 1960. In the euro area, the M2 money supply is still growing on a year-over-year comparison, as the ECB started to raise interest rates later than the Fed. Thus, one can expect that the year-over-year number will also become negative in the coming months.

Nevertheless, if one looks at the change of M2 on a month-over-month basis, one observes that the money supply rose in January compared to December 2022. That supports the argument that the monetary expansion supported the rise in equity and bond prices in January.

The Federal Reserve received criticism recently that its decision to slow the pace of interest rate increases was premature. Larry Summers, who said the Fed is making progress a few weeks early, flip-flopped again and now calls for an interest rate hike of 50 basis points in March.

In his congressional hearing on Tuesday, Jerome Powell stated that the Federal Reserve might have to raise interest rates higher than previously anticipated because the latest economic data came in stronger than expected, indicating that a faster tightening is warranted. Although he also said that the Fed would have to look at the coming economic data, the statement clarifies that the terminal rate will be higher than market participants previously expected.

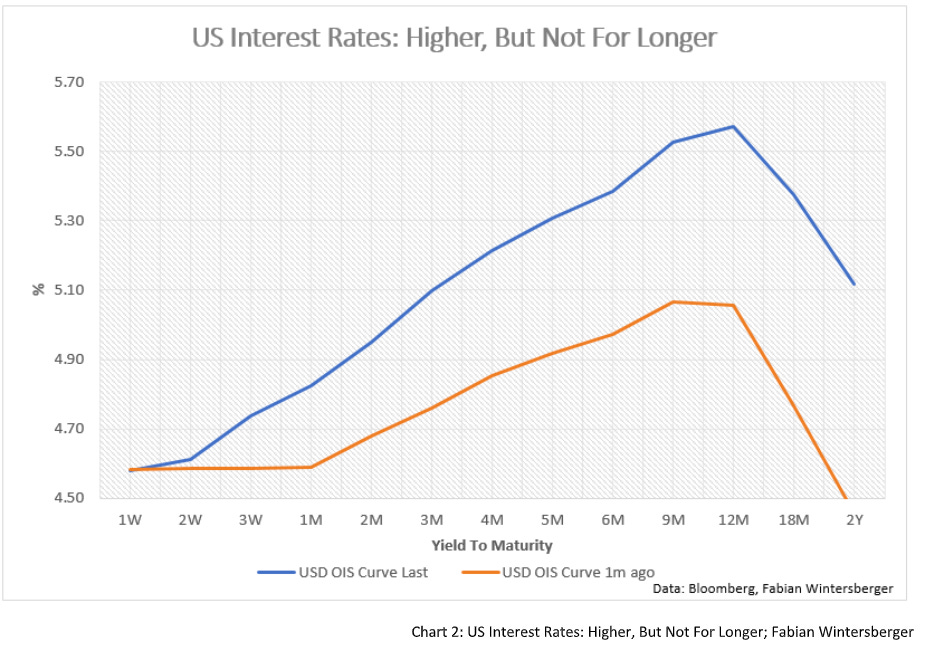

As a result, the expectations of market participants adjusted, and they now expect that the Fed will raise interest rates above 5.5 % this year. The USD OIS curve shifted upwards, but longer-term interest rates did not. This indicates that bond market participants are still not buying the longer in Powell’s announcement that interest rates will be higher for longer.

In the eurozone, market participants also adjusted their expectations. Still, in contrast to the US, they also expect a higher terminal rate (above 3.8 %) and that the ECB will cut interest rates later and slower than previously expected.

Both central banks suffered criticism from analysts and economies because of contradictory statements from various members of the FOMC and the ECB’s governing council. However, I think those different statements are intended and aim to orchestrate a soft landing.

For example, on Monday, OeNB governor Holzmann said that he would vote for a 50 basis point rate hike at the following four ECB meetings, and got criticized on Wednesday by the head of the Banco d’Italia, Ignazio Visco, who pointed out that the governing council has agreed to decide meeting by meeting without forward guidance.

In the United States, the Federal Reserve faces the problem that loans and leases in bank credit still rose more than 10 % year-over-year and keep the economy going. The US labor differential (US Conference Board Jobs Plentiful - Jobs Hard To Get) also points to a very tight labor market.

Month-over-month, bank lending decreased slightly, that lending started to slow from now on. Yet, lots of US zombie companies used the fall in yields in January to issue bonds to refinance their debt, which enabled them to procrastinate potential payment difficulties. The Wall Street Journal reported that junk-rated companies issued almost as many bonds in January and February as they did in the entire second half of 2022. Assumingly these companies hope that the spike in interest rates is temporary and that interest rates will fall again in the coming years, as the yearly volume of bonds to mature will not exceed 100 billion US dollars before 2025.

While I expect that the latest rally in equities will come to a halt, I am skeptical that the stock market will experience a substantial correction shortly, as some people assume. There have been many comparisons of the current bear market with the bear market in the early 2000s, when equity prices declined gradually over two years, interrupted by several sharp bear market rallies, which always fueled hopes that they marked the beginning of a new bull market.

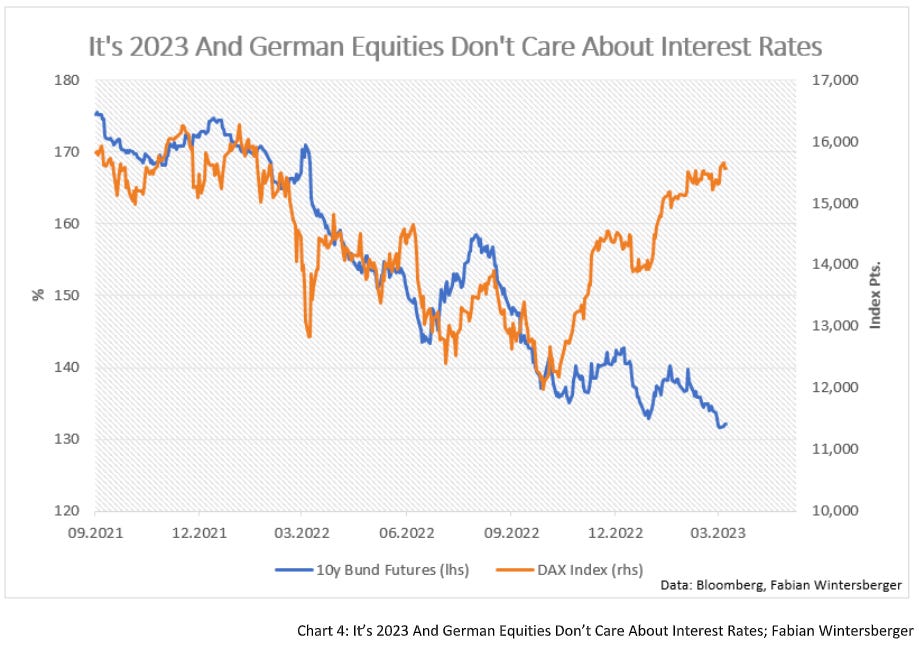

In Europe and the United States, equity prices strongly differ from bond prices. Especially in Germany, the divergence between the DAX and 10y Bunds looks extreme, as bond prices continued to fall while the DAX rallied back to its March 2022 levels.

Given the divergence, one can assume that the deviation adjusts, resulting in a declining DAX and a rise in 10y Bund prices. My thesis is that 10y Bunds will correct upwards in the short term before market participants realize that consumer price inflation will stay more elevated than previously expected, which causes inflation expectations to adjust upwards.

The probability of a recession is still high in Germany. Fitch expects that Germany and Italy will fall into recession at year-end but that the eurozone as a whole can avoid a recession. Fitch also expects the UK and the US to experience a recession in late 2023.

Yield curves in Germany, the United Kingdom, and the United States support that. In all these countries, the 10y-3m spread is in negative territory, which points to a potential recession at year-end or early 2024.

The coming recession could become a global one that affects all significant economies simultaneously. The contraction of the US M2 money supply and declining growth rates in other economies support that and the OECD Composite Leading Indicator of the G20 Nations.

This brings us to how various asset classes will perform in the coming months. I expect the dollar will continue to appreciate against the euro in the currency markets. The reason is that I do not think that any other central bank, neither the ECB nor the Bank of England, is in a position where it can out-hawk the Fed.

Jerome Powell’s statements indicate that the Fed will raise interest rates higher. Furthermore, there is an increasing probability that the Fed will continue to raise interest rates faster than the ECB, given the doves within the governing council get support from the neutral members. Economic data for the eurozone might hint at whether the doves or the hawks prevail. I still see EUR/USD falling back to parity at some point later this year. Further, the latest data from Eurostat shows that business bankruptcies reached the highest level since the start of the data collection in 2015.

In stock markets, one can expect a rise in volatility, partially because of the increase in the expected terminal rates in the eurozone and the US, if we assume that the thesis of a narrowing divergence between stocks and bonds is correct. For a short-term trade, I think that buying longer-term bonds is a better trade than shorting equities, as equity traders might continue to fade out the current developments in the bond market. In my opinion, the saying sell in May, and go away could be very accurate again.

A higher interest rate environment and higher expected terminal rates are also bad news for growth stocks, which performed very well throughout the 2010s and the pandemic. Value stocks seem like a better option in an environment of higher interest rates. However, I would clarify that I do not have a strong opinion on that because currently, stock market participants interpret bad and good economic data as bullish.

Commodity markets are still far below the highs from 2022, and there is no sign of a trend reversal. Oil (WTI) is trading in a 70 and 80 US dollar/barrel range, and US gasoline prices are just slightly positive year to date. It seems as if the Chinese reopening that supported the latest rise in European equity prices had no consequences for price developments in energy markets. Only copper is up 5 % year to date, down from +10 % at the end of January, which does not support a continuous rally either.

The current economic environment also indicates a bearish price development in precious metals. Long-term expected real rates have risen sharply since last year and turned positive, while gold, which usually correlates strongly with inverse real rates, has been trading sideways since 2020.

The expectation of coming interest rate hikes in the United States does not point to negative real rates anytime soon, which makes a decline in the gold price to 1,300 US dollars/ounce is not unlikely unless gold traders have a better assessment of the current situation.

Suppose we remember the events of Max Frisch’s The Arsonists. In that case, one might recognize that it could be the case that some market participants are acting like Biedermann and fade out evidence, while others give clear clues about future developments, like the Arsonists. However, it isn't easy to assess which asset class represents whom.

Are equity investors like Biedermann, while the Arsonists are on the side of central banks and bond markets, which hint that the latest equity price rally is based on false assumptions?

Or will equity investors be proven correct, and are the bears only looking at negative economic data while ignoring positive data? Although it is mostly the case that the bond market has a better assessment of the situation than the stock market, it could be wrong this time. But even if expectations about the terminal rate in the eurozone and the US are wrong, it is hard to argue that this would be bullish for equities.

However, given the big divergencies, the reversal could become legendary, no matter what asset class will be proven correct in the end.

Destiny is callin’ me, go down in history

Every day I’ll fight to be, legendarySkillet - Legendary

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! If you like what I write, you can subscribe and get every post directly into your inbox. Also, sharing it on social media or liking the position would be fantastic!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice)