Learning To Survive

Weather forecast for tonight: dark ― George Carlin

Nostradamus, born Michel de Nostredame in 1503, is one of history’s most famous figures in the realm of forecasting the future. He was a French astrologer, physician, and seer whose prophecies have captivated people’s imaginations for centuries. His most notable work, Les Prophéties, was first published in 1555 and contains hundreds of quatrains—short, four-line poems—that are believed to predict future world events. Nostradamus’ predictions have been associated with everything from natural disasters to the rise and fall of empires, cementing his place as a lasting cultural figure in mysticism and prophecy.

Nostradamus' approach to prophecy was rooted in a combination of astrology, historical patterns, and possibly personal intuition or visionary experiences. His quatrains often used vague, symbolic, and metaphorical language, which allowed for broad interpretations. This ambiguity has played a crucial role in the longevity of his reputation; since his predictions lack specific dates or detailed descriptions, they can be retroactively linked to various historical events. This adaptability is key to why his work intrigues readers, scholars, and believers.

Some of the most famous prophecies attributed to Nostradamus include events like the Great Fire of London in 1666, the rise of Napoleon Bonaparte, and even Adolf Hitler’s reign. For instance, one quatrain mentions a figure rising to power "born near Italy," which many associate with Napoleon, born on the island of Corsica. Another verse describes a figure "from the depths of Western Europe" rising to bring evil, which some interpret as a prediction of Hitler’s ascent to power in Germany.

However, critics argue that these connections are often tenuous and made in hindsight, emphasizing Nostradamus’s vague language. Nonetheless, his work has left an indelible mark on popular culture and the idea of prophecy, influencing everything from literature and film to modern interpretations of world events.

Critics of economic forecasts often ridicule economists' models, comparing them to Nostradamus’ astrology, saying they’re vague in their predictions and frequently follow consensus views. Regardless of whether this critique is fair, it’s widely acknowledged that predicting the future, especially human behavior, is inherently tricky.

Still, just as Nostradamus looked at the stars to predict future events, economists look at the yield curve to gauge the economy's future trajectory. The yield curve reflects market participants' expectations about future interest rates, including their outlook on real economic growth, inflation, and the term premium compensating for the risk of holding long-term bonds.

Overall, the yield curve has proven to be a fairly reliable tool for forecasting recessions. Every U.S. recession since World War II has been preceded by an inversion of the yield curve, suggesting it's a strong indicator of an upcoming downturn. When inflation is assumed to remain constant, an inverted yield curve reflects diminished expectations for future economic growth.

However, it's important to remember that these data points are merely predictions and are not guaranteed to come true. Therefore, one should never rely solely on the shape of the yield curve but instead, use it as a guide—a starting point for analysis that must be validated with other economic data.

The reason I’m discussing this topic is because incorrect expectations from market participants can paint an inaccurate picture of the future. Recent events are a good example of how things don’t always—or arguably most of the time—unfold as expected by the markets.

The US's current yield curve inversion (the 10-year minus the 3-month yield) has lasted for over two years, making it the longest since World War II. An inversion is typically viewed as a strong signal that a recession is near, which has triggered multiple recession predictions. So far, however, these predictions have been wrong, and the yield curve has adjusted several times during this period. In my view, this is a crucial reason why so many bond bulls and stock market bears have been incorrect for so long.

Historically, being bearish on the stock market has been riskier than being long, and the past two years have been no exception. However, as parts of the yield curve begin to revert, many again argue that a recession is imminent, which could explain the heavy demand for long-term treasuries from fund managers and investors since May.

Nearly everyone expects long-term bonds to perform well going forward, whether the economy experiences a soft landing or a recession. In the event of an economic downturn, the Federal Reserve is anticipated to have to cut interest rates sharply, leading to a bull steepening of the yield curve as short-term rates drop faster than long-term ones.

However, betting on long-term bonds is not always a sure win in the event of a reversion. Before this current inversion, the most prolonged inversion occurred between March 1973 and May 1974 (14 months). While some aspects of the current environment, such as the 2022 energy price shock and geopolitical tensions, resemble that period, there are notable differences.

Unlike 1973, gas prices have since come down, whereas they remained elevated throughout the 1970s. The oil price spike back then led to a deterioration in growth, which is only slowly declining now. Furthermore, the situation differs because, in the 1970s, inflation was accelerating, whereas today, it’s trending downward, and economic growth remains solid.

Additionally, the 1974 recession occurred while inflation was still rising, and the yield curve remained inverted for most of that time. During the recession, the Fed cut interest rates despite ongoing inflation. Even after inflation started to decline, 10-year yields remained high and never returned to pre-recession levels, despite the drop in the Fed Funds Rate.

In October 2023, the pricing of the 10y-3m spread in the US was less negative than it is today, and at that time, some might have interpreted the data as signaling that the reversion had already begun. However, the recession remained elusive, as inflation trended sideways before falling further from June onward. Despite this, real growth remained robust, rebounding to 3% in the second quarter and likely holding steady in that range, according to forecasts from the Atlanta Fed.

This suggests that while inflation is declining, efficiency gains might contribute to higher real growth, meaning longer-term bond yields could rise again or at least not fall as much as market participants expect. If short-term inflation doesn’t ease as anticipated due to shifts in relative prices, inflation expectations may increase, pushing yields higher.

If the US Fed is forced to cut interest rates at a slower pace, market expectations will need to adjust, resulting in another repricing of the yield curve and potentially causing the curve to bear steepen. I touched on unemployment last week, so let's now examine the latest economic data to assess the state of the Eurozone and US economies.

On Friday, S&P Global published their Flash PMIs for European countries, highlighting the ongoing economic concerns of many market observers. While the positive effect of the Olympics in France has faded, the report paints a grim picture of the German economy, where growth is already lagging behind the euro area.

September saw Germany’s private sector economy sink deeper into contraction...Business activity in the country fell at the quickest rate for seven months, with a sharp and accelerated reduction in manufacturing production compounded by a near-stalling of growth in the service sector.

According to the report, a technical recession in Germany seems inevitable, as it forecasts a 0.2% contraction in economic growth for the third quarter compared to the second. Interestingly, while businesses report a darkening outlook and an increasing willingness to lay off workers, the unemployment rate dropped further to 6.4%, the lowest since the euro's introduction.

However, recent news from German car manufacturers about upcoming job cuts suggests unemployment may trend higher in the near future. VW also announced plans to end its three-decades-old employment protections next year. Considering European traditions, one can expect that government programs will be introduced to mitigate the rise in unemployment. Nevertheless, the announced job cuts will likely have ripple effects throughout the eurozone, where many auto part suppliers are based.

Meanwhile, the Ifo Index has not improved, with German business sentiment continuing to worsen for the fourth consecutive month. This supports the PMI’s assumption that Germany is back in recession. However, it's worth noting that the correlation between GDP and the Ifo Index seems to have weakened considerably in recent years, as the index would suggest a much deeper economic slump.

On Monday, we received the Flash PMI data for September from the United States, where the economic outlook remains much brighter than in Europe. The Composite PMI came in slightly higher than expected, driven by strength in the service sector, while the manufacturing sector weakened further, dropping to 47 from 47.9 in August (expected: 48.6).

US business activity growth remained robust in September, according to flash PMI survey data from S&P Global, signaling a sustained economic expansion over the third quarter. Only a small loss of momentum was evident in September, but growth disparities persisted. A further solid expansion of the service sector contrasted with a second successive month of modestly falling output in the manufacturing sector.

The report highlighted that businesses are becoming increasingly uncertain due to the upcoming Presidential elections in November, dampening expectations. However, expectations of falling interest rates fueled optimism for sales growth and investment.

In terms of employment, the report noted a slight easing in the labor market. The uncertain outlook contributed to hesitation in the service sector in replacing departing workers, and manufacturing payroll cuts reached levels not seen since June 2020.

While US economic activity is clearly slowing, it appears to be more of a normalization process rather than a sign of outright deterioration. Therefore, betting on a rapid recession and significant rate cuts may still be a tough call.

Despite some cautionary signals from S&P Global, the report indicates that the US economy experienced solid growth in the third quarter:

The sustained robust expansion of output signaled by the PMI in September is consistent with a healthy annualized rate of GDP growth of 2.2% in the third quarter. But there are some warning lights flashing, notably in terms of the dependence on the service sector for growth, as manufacturing remained in decline, and the worrying drop in business confidence.

The Federal Reserve's recent dot plot showed significant uncertainty among voting members about the future path of short-term interest rates. Market expectations are even more dovish than the Fed’s median outlook, anticipating aggressive rate cuts due to falling inflation and slowing economic activity.

However, PMI findings raise a potential issue that could complicate the Fed's plans:

The September survey also showed average prices charged for goods and services rising at the fastest rate since March, representing the first acceleration of selling

price inflation for four months. The upturn lifted the rate of inflation further above the pre-pandemic long-run average. Rates of selling price inflation moved up to six-month highs in both manufacturing and services, in both cases running above pre-pandemic long-run averages to point to elevated rates of increase.

Although the recent trend in money supply growth makes it doubtful that inflation will re-accelerate sustainably from this point, mid-term fluctuations are still possible. Businesses tend to set prices based on their short-term inflation expectations, and if they experience rising costs, they may increase selling prices, driving inflation higher in the short term.

However, these new prices often create disequilibrium. As prices rise, consumers may not be able to keep up, leading to lower demand. For businesses to maintain their sales volumes, prices would eventually need to come down, causing inflation to abate. This process doesn't happen immediately—it takes time to unfold.

If inflation overshoots for several months, it could influence inflation expectations among both the market and the Federal Reserve. As a result, interest rates may not fall as quickly as currently anticipated, and bond yields may need to adjust. Moreover, it's worth noting that money supply growth has already started to accelerate again. In an economically uncertain environment, this could lead to increased volatility in inflation and potentially higher long-term interest rates due to a rising term premium.

Therefore, despite clear warning signs—such as rising loan delinquencies and a sharp decline in the labor market differential, which fuel the widespread bearish sentiment on the economy and bullishness on long-term bonds—the situation remains complex.

Bianco Research recently highlighted an interesting point from the consumer confidence survey, which revealed that 20% of respondents plan to take a foreign vacation—a historically high level. Bianco argues:

I've argued that this is the ultimate discretionary spending item. Absolutely no one needs a foreign vacation, but absolutely everyone wants a foreign vacation...If you believe your finances are "iffy," or you're worried about potentially losing your job, this is the first thing to cut, as such a vacation can run thousands of dollars...This is not falling, is still at a historically high level, and indicates a healthy economy.

The stock market seems to support this argument, often acting as a leading indicator. Historically, the stock market tends to roll over when the economy heads into recession, as seen in 1981, 2000, and 2008. Currently, the S&P 500’s chart suggests a potential "melt-up" heading into the final quarter of the year.

As things stand, I do not expect the US economy to enter a recession this year. Economic activity will likely continue to normalize, with inflation edging lower but possibly experiencing short-term volatility, which could support bond yields.

Money supply growth is also accelerating again in both the US and the eurozone. Year-to-date, M2 money supply has grown by 4% in the eurozone and 2% in the US. Some of this new money will flow into the real economy, pushing corporate profits, prices, and wages higher. If a recession does occur, monetary growth will accelerate further, building inflationary pressures for the future. Government spending will also increase in the event of a recession, although it may take longer to materialize, which could negatively affect government bonds.

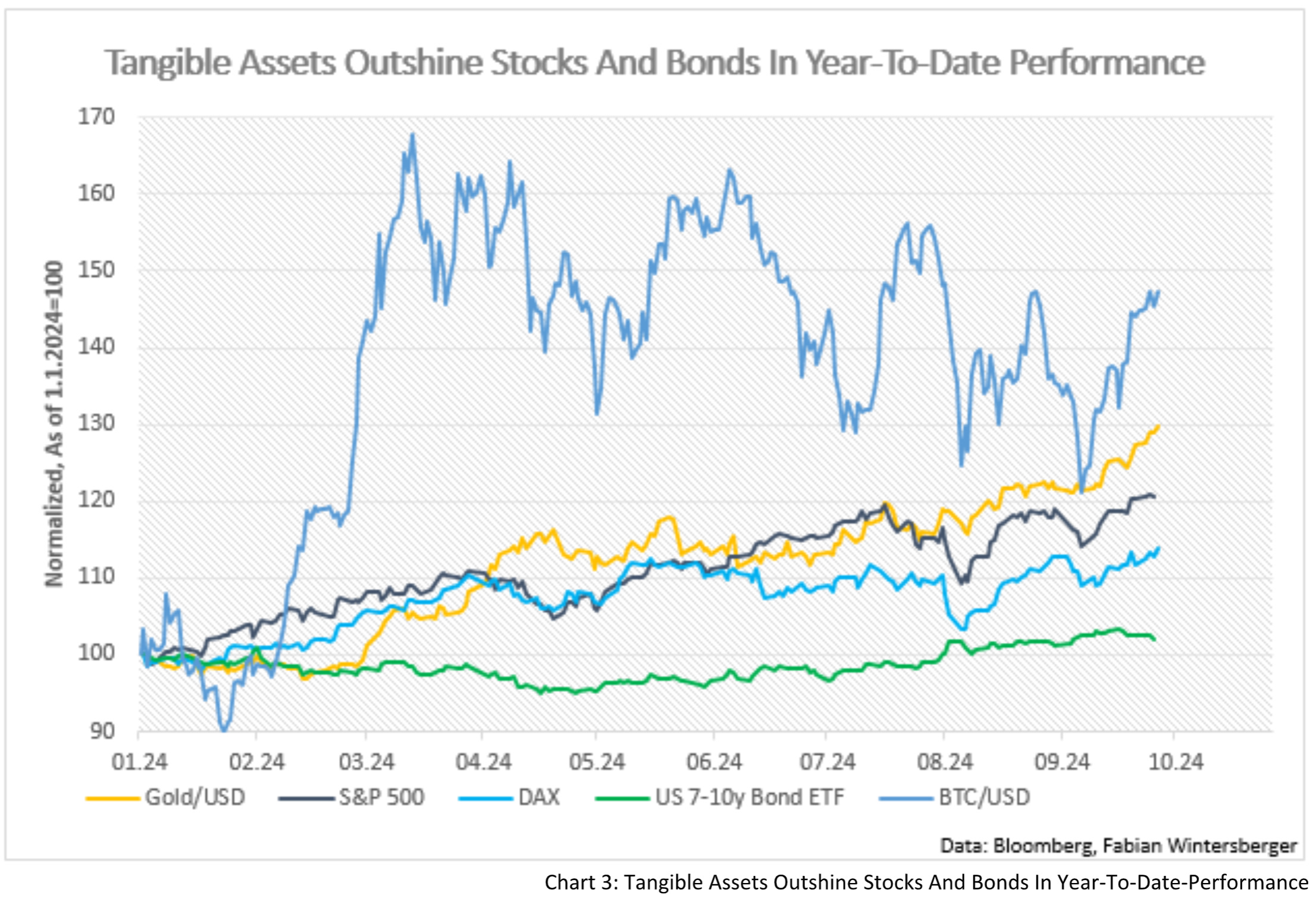

Tangible assets, meanwhile, are already rising, reflecting investor anticipation of this scenario. Gold has outperformed stocks and bonds year-to-date, with only Bitcoin showing stronger returns. However, Bitcoin is far more volatile and has declined since March.

The situation in the markets remains complicated, but in my view, short-term expectations are once again overly dovish. Many investors may soon face another reality check.

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. They do not constitute investment advice, and my perspective may change over time in response to evolving facts. It is strongly recommended to seek independent advice and conduct your own research before making investment decisions.

Well said Fabian. One of the things that I have seen, I think George Robertson made the point, is that the Fed's balance sheet purchases have distorted the yield curve dramatically compared to the way it used to be when the inversions in 1981, 2001 and 2008 signaled a recession. the fact that they have removed so much supply from the market could well be the reason that long end yields have been as low as they have. while I cannot model the impact, I believe there are several models that indicate it could be as much as 150bps, which would mean the curve never inverted, or certainly not for as long as has been discussed..

With that in mind, I suspect that the fed, and all the central banks, have decided that 2% is the new inflation floor, and will quickly add liquidity and cut rates if growth starts to sink. and if growth remains robust, the rationale for rate cuts is also suspect. I would not be long duration at this point, that's for sure.