Last Resort

This month, the Federal Reserve will start to shrink its balance sheet, although I have to disappoint those who think that it already started this Wednesday. In fact, the Fed will begin to tighten on July 15th.

Better late than never, one might say. In 2021, inflation was way higher than the Fed’s declared 2 % goal. In September of last year, CPI was at 5.4%, while the Fed’s favored inflation metric, Personal Consumption Expenditure (PCE), was more than double the Fed’s 2 % goal, at 4.4 %.

Back then, central bankers insisted that inflation was only transitory because of supply chain disruptions. If the Fed hadn’t hesitated and would have started to normalize monetary policy in September 2021, it probably could have prevented inflation from rising further. It was already clear that various rounds of stimulus payments artificially fueled consumption.

In recent months, inflation has reached the general public and pressured politicians to do something about it. High inflation rates have led to negative real wage growth and forced people to expand their credit card spending to keep consumption levels high.

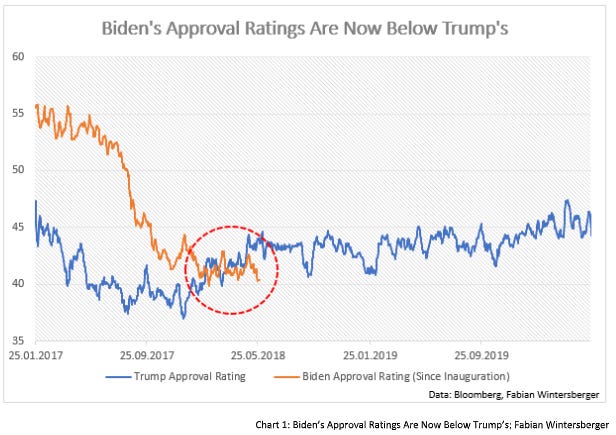

The public became furious about high inflation. Therefore, the Biden administration reacted and put pressure on the Fed in recent months because the Democrats have to defend the majority in both chambers of Congress in the coming mid-term elections.

While it is still some time until the elections occur in November, the current position hardly could be worse. Because of high inflation rates, Biden’s approval ratings are lower than those of his predecessor Donald J. Trump.

So, it is more than understandable that Joe Biden declared ‘fighting inflation’ the most important goal, and I am sure he assured Fed Chair Jerome Powell of that in one of the rare meetings between a president and a central bank chair this week. According to economic advisor Cecilia Rouse, the US president has instructed Powell to do everything needed to bring inflation down.

I conclude that the Fed will not stop its, compared to the ECB, very aggressive tightening path, and thus I do not expect that equity prices have bottomed already. The Fed Put that the Maestro, Alan Greenspan, introduced is likely far below current prices.

While the situation within energy markets was somewhat worrisome before, Russia’s invasion of Ukraine and the west's reaction put more fuel to the inflation fire.

Demand is so strong that neither releasing parts of the US’s SPR nor the weaker than usual demand for oil from China because of lockdowns brought prices down significantly. Excluding Russia’s oil from the market exactly had the predicted results of my piece from May 6th, ‘Take A Look Around’. Falling demand for Russian oil caused a rise in demand for oil from other producers, like the US, which fueled price increases because of the lack of spare capacity.

Rising foreign demand causes domestic price increases because producers supply less oil to the domestic market, given that production levels remain more or less constant. As a result, the Biden administration has started to think about restricting oil and fuel exports to stop the price increase.

The oil futures curve is sloping down, which means that current demand is higher than future demand. Usually, backwardation is a sign of low inventories because producers make more money by selling it immediately instead of storing it.

However, the situation is different today because of the loss of Russian supply. Demand exceeds supply, and market participants try to buy as much oil as possible to store it to have it available in times of future scarcity. As I already mentioned above, the US has begun to sell parts of its SPR to the market, while Chinese demand has been lower than usual because of lockdowns. Chinese demand is starting to come back, and I assume prices may have more room for the upside.

The general saying that the cure against high prices is high prices because higher prices lead to a fall in demand probably is not that accurate for energy, as data from the UK shows. Despite the latest increase in fuel costs, consumption remained more or less constant. One might assume that instead, people lower their consumption of other goods.

If we assume that energy prices likely continue to rise, we can conclude that the situation in asset markets remains turbulent. That is probably what the Fed wants to see, as the former NY-Fed chair Bill Dudley stated recently. The Fed will have to accept falling stock prices and higher unemployment to fight inflation, Dudley said.

Joe Biden also published a piece in the Wall Street Journal where he outplayed the administration's plan to bring inflation rates down. Primarily, this should be achieved by lowering budget deficits. Still, at the same time, Biden talks about increasing investments in renewable energies and plans to build a million new houses to make housing more affordable. This is to be financed by introducing a global minimum tax for companies.

Nevertheless, it is more than questionable if a global minimum tax can achieve that. The proposal was made more than a year ago at a G7 meeting. Back then, Daniel Lacalle wrote:

Rising corporate taxes will not reduce the debt burden. The reality of the budgets and financial position of most G7 and G20 countries shows that deficits continue to be elevated even in growth periods and after periods of tax increases because government spending rises above all revenue increases.

Rising corporate taxes will not improve growth, jobs, or productivity as shown by the above-mentioned examples but also by our recent history, specifically in the European Union, nor generate a substantial improvement in tax revenue that, in any case, will not even scratch the surface of the existing debt.

Rising energy demand from China and a refill of the US’s SPR will pressure oil prices. Meanwhile, Arab oil producers apparently are not interested in increasing supply, and it seems that they tend to stay on Russia’s side.

The Fed can only influence demand via monetary policy. Hence, I think the Fed will succeed in bringing inflation down by hiking interest rates. However, the side effects of an aggressive rate-hiking path might be a sharp slowdown of growth at best and a recession at worst. Markets already expect the Fed to pause the hiking cycle next year.

Meanwhile, the member states of the EU agreed on another package of sanctions on Russia that foresees that the EU will cut Russian oil imports until year-end by more than two-thirds by abolishing imports from Russian oil coming in vessels. Additionally, the EU plans to cancel insurance for oil vessels transporting Russian crude, and the goal here is to hinder Russia from selling the oil to third countries.

These sanctions will lower the supply of oil and elevate prices further. Moreover, oil prices have a strong correlation with yields, and therefore I expect that yields may have more room to rise and might not have topped, as I wrote last week. That is especially the case for European yields because despite higher than expected inflation rates, the ECB still only wants to normalize policy gradually.

Because of that, the probability of a 50 bps rate hike in July, as the governor of the Austrian Central Bank, Rober Holzmann, called for, might have risen but remains unlikely.

It is well-known that the doves in the ECB’s governing council have the majority, and those continue to argue that a normalization of monetary policy has to be gradual. This Tuesday, Ignazio Visco (Banca d’Italia) and Francois Villeroy (Banque de France) reaffirmed that. Especially Visco pointed out in his statement that the ECB will have to keep a close eye on government bond spreads because the latest developments show that public debt is still a source of significant vulnerability.

Honestly, I do not know what data must be published to let the data-dependent ECB conclude that it has to normalize faster. Further, the EU Commission around Ursula von der Leyen still thinks it is possible to solve problems that result from the sanctions against Russia can be solved with additional spending, despite already record-high debt/GDP ratios.

The strategy that the sanctions would bring Russia quickly to its knees utterly failed. On the contrary, Russia profited from rising oil- and gas prices while the European economy was getting into more trouble.

Firstly, the commission wants to diversify the supply of fossil fuels and plans to buy gas from other suppliers for all member states. Additionally, it plans to expand the European infrastructure for natural gas and boost investment in renewable energy.

I do not know why the west does not try to boost the global supply of oil and gas because this would lower prices on the one hand and, on the other hand, would hurt Russia because of falling export revenues. I can only assume that this is not done because it would be against the agenda of the green revolution.

Von der Leyen is correct that buying natural gas jointly leads to a higher negotiation power for the buyer. Still, I think that the need for additional bureaucracy is consuming this advantage quickly because history has shown that governments, or government unions, are bad entrepreneurs. However, what is achieved is that the bureaucracy in Brussels can further expand its influence.

Furthermore, additional infrastructure spending will set a reallocation process in motion and weaken the private sector. If the benefit is greater than the costs remains to be seen. The production of renewables, which are needed to expand the green energy supply, will probably take place in Asia, and I doubt this will boost European growth rates in the near future. At the same time, it definitely will lead to other dependencies.

Finally, I want to look into the future to see what the current situation will mean for markets. Rising rates will continuously put pressure on equity and bond prices and probably soon become a problem for housing prices.

Cutting off Russian oil from the market reduces the total supply, while transfer payments dampen the impact of the price increases and keep demand steady, which will probably drive oil prices higher.

Because rising energy prices have consequences for all other prices because energy is needed for production, inflation will also remain elevated. However, I expect that inflation will fall slightly throughout the year, and however, it will stay way above the 2 % goal of central banks.

Inflation will continue to stay the dominating narrative in the near future until recession fears gain the upper hand and lead to a change in the narrative that forces central banks to reverse course.

Still, I do not think that this will happen soon. Higher than expected inflation data from Europe this week only strengthened the inflation narrative, and because of that, I revise my assumption from last week that rates might have topped.

Apart from energy markets, other commodities likely will also rise in prices. On the one hand, prices for metals that are needed for the production of renewables, and on the other hand, agricultural goods. According to YARA, the global supply of fertilizer has fallen by 15 % since the sanctions against Russia and Belarus were implemented. The problems with supply chains and rising gas prices only make the situation more severe.

The situation might benefit emerging economies with high commodity reserves, while the economic situation in the EU will continue to stay worrisome. That is also true for the US, where the aggressive normalization of monetary policy will lead to a market shakeout of unproductive companies that was long overdue.

The dollar will continue to gain strength in the foreign exchange market, especially compared to the Euro. In economic turbulence, the world’s reserve currency remains the ‘save haven cash’.

The economic situation remains turbulent, with no sign of a calming situation. If inflation were low, central banks would have started to ease already, but in the current environment of high inflation, an aggressive tightening path might be the Last Resort. However, it might have some severe side effects caused by central banks doing nothing or too little during the last decade.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)

Appreciate your "look to the future" section as this is certainly not an easy part of current econ situation analysis and its implications for the future - interesting even rather sad esp. from the view of EU citizen.