Land Of Confusion

Jean Claude Juncker was not an ordinary politician. He was one of the most influential politicians in the EU area. And he was also a politician whose tongue was close to his heart.

In 2007, he was asked about political reforms and answered: We all know what we have to do, we just do not know how to get reelected when we do it. In 2010, the Economist took this quote to argue that if the EU wanted to thrive again, it would have to take steps to do similar reforms as Jaques Delors did back in the 1990s, which made it possible to leave the misery of weak economic growth and high unemployment rates of the 80s behind it.

Delors was one significant figure in shaping the monetary union, which is now known as the eurozone, back in the late 80s. The German Democratic Republic was just falling apart, and the Federal Republic of Germany was hoping to reunite Germany. However, France and the UK opposed the plans and urged the USSR to smash such goals.

On the other hand, Germany was not impressed by plans for a monetary union in Europe. It feared that it would diminish the sovereignty of the German Bundesbank and that monetary policy in the union would become more similar to weak-currency countries, such as Italy or France.

Mainly the Italian lira was devalued regularly to keep Italy’s economy competitive in international comparison. The devaluation lowered real wages but kept nominal wages at steady levels—an export policy on the back of Italy’s population, so to say.

Germany’s wish for reunification was Delors’ chance on which he capitalized. He offered Kohl a deal: Germany agreed to a monetary union, and France agreed to reunification.

The rest is history. Central banks of all members formed a union of European central banks. The union abolished exchange rate controls from July 1990, and the introduction of the euro was settled within the Maastricht Treaty.

At the end of the century, the euro became book money, and from 2002 the euro also became cash. Hopes were big that the euro would lead to higher economic growth and boost European integration.

During the first several years, everything went according to plan. Moreover, it looked like the euro was on a triumphal procession, especially against the US dollar. The euro appreciated enormously. A euro in 2001 was worth 85 US cents. Six years later, in 2007, it was worth 1.45 dollars. Alan Greenspan (Fed chairman at that time) feared that the euro might dethrone the dollar and was on its way to becoming the world’s first reserve currency.

No member could devalue her currency within the eurozone to raise competitiveness, and the only way left was to lower nominal wage rates. For example, if Italy wants to gain competitiveness of workers over Germans, it has to lower nominal wage rates or raise wages slowlier, as both countries use the euro.

Basically, the euro became some sort of gold standard within the eurozone, so it hindered countries from secretly lowering the purchasing power of their citizens through the backdoor to gain competitiveness for exports. As the Spain economist, Jésus Huerta de Soto put it:

Only when exchange rates are fixed are governments obliged to tell citizens the truth.

Primarily the European South benefited from the euro because of back then lower interest rates. Market participants trusted that the European Monetary Union would improve the ability of those countries to pay back debt. Hence, they accepted a lower risk spread for Italian, French or Spanish bonds. It seemed that the strong growth was proving them correct.

But everything changed when the Great Financial Crisis hit the world, and the euro experienced its first recession. Countries ramped up government spending to fight the recession and hoped to invest out of the crisis.

However, it had an enormous impact on government deficits, and the situation did not get better when the ECB raised interest rates in September of 2008. It drove up debt/GDP levels further as most countries were still hesitant to implement structural reforms.

As a result, the southern countries, where significantly lower interest rates led to capital misallocations, got underwater more and more. Spain, for example, had experienced a big housing boom until the bubble suddenly popped.

Risk spreads for government bonds ramped up, and markets started to question the smooth functioning of the euro. The situation became worse in 2012 when Draghi could cool down markets with his whatever it takes speech. Nevertheless, the time that Draghi bought them was poorly used, and hardly a country implemented structural reforms.

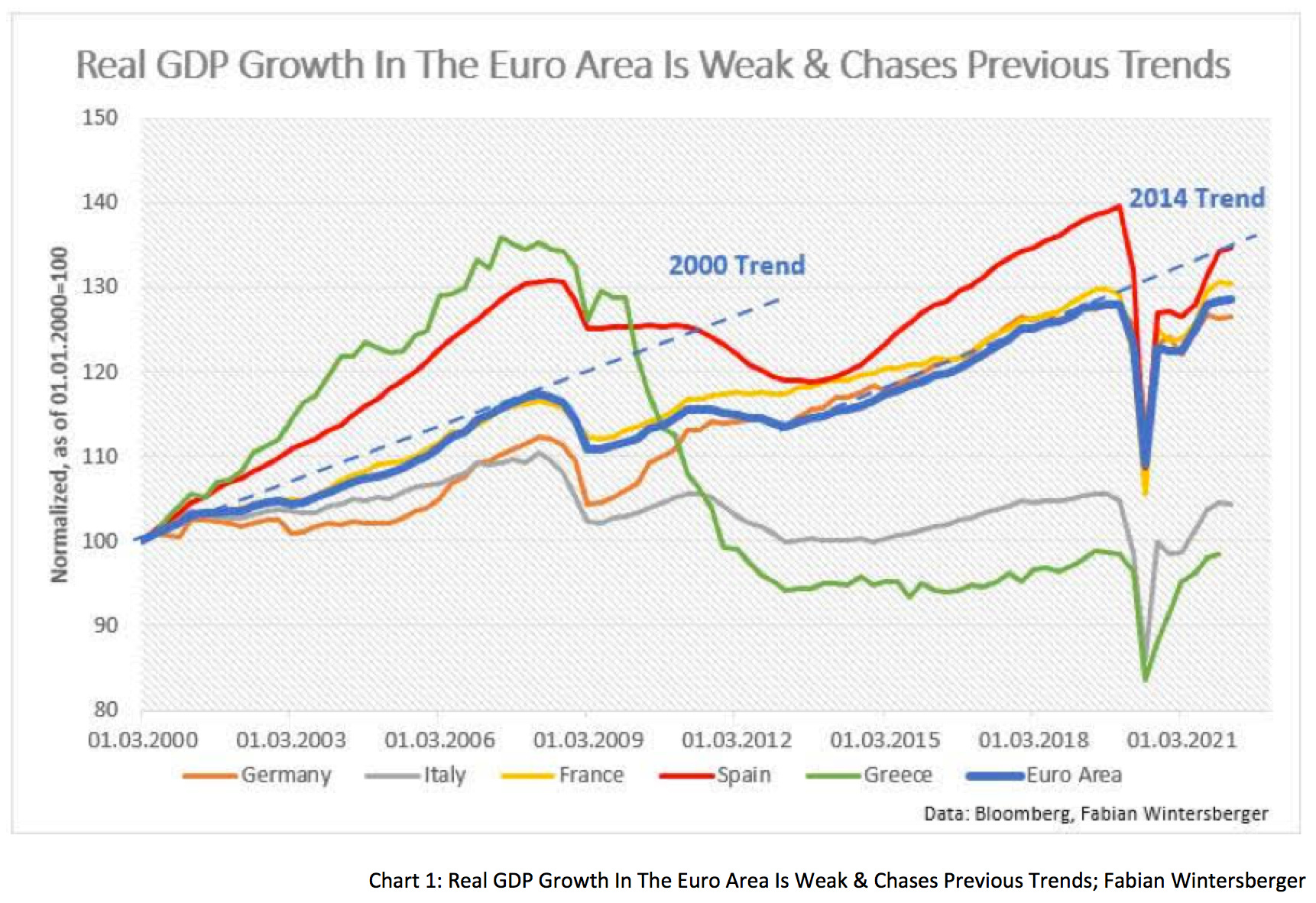

While Germany had been in economic trouble in the first years of the century due to regulations and high social expenditures, the Hartz reforms of the Schroeder government changed that. Now the south was the focus of market participants. Especially Italy and Greece fell into a deep stagnation and could not recover until this day. As a whole, the eurozone has been chasing former growth trends since the GFC.

In the early 2000s, the euro attracted capital to the region, and the exchange rate appreciated. When the GFC hit the world, this effect reversed, and since then, the euro has continuously depreciated versus the dollar. Debt to GDP ratios increased, except for a few northern countries, which put on a few reforms and decelerated wage growth to gain competitiveness. In the eurozone as a whole, debt levels are now slightly above 90 %, where they have risen further due to the pandemic policy.

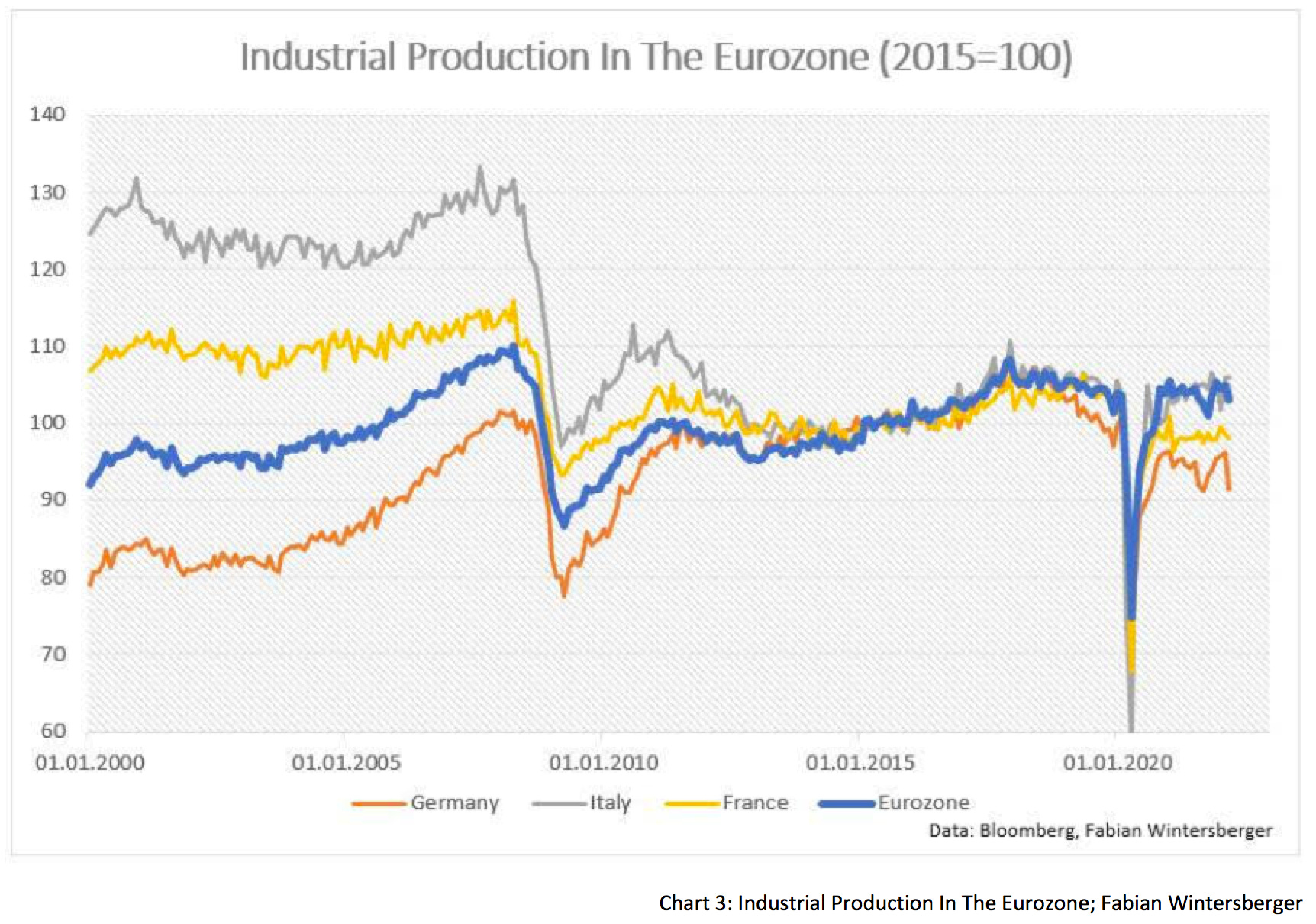

Additionally, zero interest rate policies from the ECB did not lead to higher growth. To lower costs, companies reallocated more production facilities to Asia. Industrial production increased only slightly after 2015. Germany, France, Italy, and the eurozone as a whole, have lower industrial production levels than before the GFC.

As measured by their share of GDP, real incomes have grown much slower in the eurozone than in the United States. While real incomes in the US are about 230 % higher than in 2000, they are only about 190 % higher in the eurozone.

The pandemic policies increased the debt levels of European businesses, governments, and households sharply while the US primarily stimulated the economy via increases in government stimulus. Combined with an even more expansionary monetary policy, this brought inflation back, and the ECB is now expecting it to be around for a more extended period.

The situation got further worse because of the war in Ukraine. European industries profited from cheap Russian energy and made higher wages possible. Rising production costs due to a lower exchange rate and the energy price shock will further weaken the European economy. In times of high inflation, it is unlikely that labor unions will hold back in wage negotiations.

High inflation and the resulting pressure of politicians to fight it through normalizing monetary policy led the ECB to fall in line with other central banks. Latest statements from several ECB’s governing council members point to a hike in interest rates between 25-50 basis points in July.

But this could be a problem for the highly indebted countries of the eurozone. As I mentioned last week, France is one of the most indebted countries globally (with a non-financial debt/GDP ratio of 371 %). Russel Napier recently explained:

The problem with an excessively high debt-to-GDP level is that it creates a financial system prone to crisis when cash flows decline or when interest rates rise.

Rising interest rates likely push risk spreads to government and corporate bonds higher. Currently, spreads are at their highest levels since the pandemic hit, and a more restrictive monetary policy likely leads to widening spreads and thus problems in refinancing for corporations. The European Central Banks is already aware of this. The more flexible Pandemic Emergency Purchase Program will likely be around for longer to prevent spreads from widening too much.

Additionally, politics will probably hinder economic growth. Strict regulations in European countries have already led to companies in the old world having to spend a lot of resources on unproductive administrative work. The European Union in Brussels uses regulations to widen its political influence sphere on the back of the economy.

The forcing of ESG by the Commission might be just another nail in the coffin. According to the German Wirtschaftswoche, the EU has presented a comprehensive set of rules for sustainability reporting on how companies should disclose what they are doing for sustainability in the future, on 400 pages. Many European family businesses are lean in terms of administration, which means that the new regulation will lead to extensive problems and cost increases. Large companies which can afford to run large administrative structures are the primary beneficiaries of rules as this may push some competitors out of business.

Due to the war in Ukraine, the EU decided to exit Russian gas and make it a European project. As DW/Reuters report, the EU plans to invest (=spend) 300 billion euros to make Europe unreliable on Russian energy imports. Ursula von der Leyen’s saying that this will be hard, but it has to be done might remind us of the old political saying that something has to be done, no matter what.

Especially renewables play a considerable role in this plan, besides the spending on LNG infrastructure. Additionally, the EU has raised its goal for energy efficiency from 9 to 13 %, although I am not sure if raising a political goal will help achieve anything.

The so-called REPowerEU Plan (at least the EU is good at finding catchy names) says that by 2030, 45 % of all energy consumption within the EU should come from renewables. However, I want to add that the member states cannot even agree on what renewables mean, for example, if nuclear power should be labeled as renewable.

However, the argument that more substantial use of renewable energy in the EU will achieve anything in combating climate change is feeble because of the sanctions against Russia. One needs fossil fuels or gas to produce steel and aluminum to build all the wind wheels and solar panels. Thus, I suppose that because of lower prices, the EU will buy them from Chinese suppliers who produce the stuff with the power from coal plants.

Rising demand will also drive prices up while debt/GDP get under pressure because of monetary tightening. Within the conflict of Russia versus the United States, Europe is between a rock an a hard place. The US is in a much different position and will probably be more able to cope with a ban on Russian energy and commodities than the EU, which definitely cannot. Russia knows this and therefore it weaponizes commodities while the West is weaponizing currency reserves.

The introduction of the euro 20 years ago is a significant contributor to the fact that the playing field is so narrow in the fiscal space. But still, the political elites in Brussels think that throwing a shitload of money at a problem will solve it. However, excessive fiscal spending (that the euro made possible for the southern countries) caused it in the first place.

Europe is a ‘Land Of Confusion’ with a problem: On the one hand, from a moral standpoint, Europe’s hands are tied to the United States, but on the other hand, Europe used its neighborhood to Russia to keep its industries competitive to other producers in the world. The economic advantage has disappeared, and therefore I assume that this decade will be a tough one for Europe.

Rising food prices around the globe will cause more political turmoil, especially in the MENA region, which additionally is on the transit route of Arabian oil and gas to Europe. Arab energy shall substitute a high proportion of the Russian imports that Europe (and the US) now do not want anymore. New refugee movements might also drive up social spending in European countries because, in case of a new refugee crisis, the refugees will end up in Europe.

This week, Janet Yellen announced that Ukraine would need a new Marshall Plan, and I assume that the EU will support those plans. All the factors point to the possibility that now, after ten years, actions will have to walk the talk of Draghi (Whatever It Takes), and the ECB will have to do everything to save the euro. Given the EU’s love for regulations, we can doubt that the EU will take the proper steps to improve the economic framework.

Probably Jean Claude Juncker was right: They know what to do, they just do not know how to get reelected.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)

Great description and the future of the single currency is dimmer by the day