More and more signs of recession are on the horizon, and more and more market participants in international financial markets are anticipating them. While current geopolitical and economic events do not point to a change for the better, many seem to lose confidence that the rate-hiking cycle could last for long.

While the market expects the Fed to raise rates aggressively during 2022, it is already expecting rate cuts in 2023. As recession signs have intensified in recent weeks, the market is showing signs of shifting the dominating narrative from inflation to recession.

While the number of people who expect a recession has grown steadily, this week’s published FOMC minutes from the Federal Open Market Committees’ last meeting show that participants do not think that a recession is imminent, although they acknowledged the possibility that things could slide. However, the committee points to the still-tight labor market and data that suggests that the economy is expanding in the second quarter.

Equity markets like the prospects of a coming recession, it seems. US indices have traded higher in the last two weeks. The S&P noted about 5 % higher from its low of the year in mid-June. It seems that everyone is convinced that the Fed will quickly come to the rescue and looses its monetary policy, just as it did during all troubling times of the last decade.

Nevertheless, the question is if the Fed will pivot as fast as some expect. Still, the Fed is highly influenced by the Biden Administration, where fighting inflation is the top priority. That the Fed would have to crash stocks (and the economy) to achieve that is something that people like Bill Dudley (and I assume the Fed so too) were not only aware of but also actively called for.

That was also confirmed by analysts Danielle DiMartino Booth (Quill Intelligence) and Jim Bianco (Bianco Research) this spring. Both said that if politicians want the Fed to fight inflation, the Fed would need to hit the brakes hard and bring the stock market down.

Since then, the Fed has raised interest rates three times, in June even by 75 basis points. Markets have already turned south, and commodities, leading indicators, are already falling. Lumber has lost about 45 % year-to-date, steel rebar has fallen 7 %, and aluminum 14 % year-to-date. Recently, oil prices started to fall, with WTI falling from 120 US dollars/barrel below 100 US dollars in a month. That could be a sign that disinflationary tendencies are taking over. However, year-to-date, WTI is still up about 30 %, and prices would need to fall to 70 dollars/barrel to erase this year’s gains.

In past weeks I speculated that commodities would come back from their highs because that happens when demand is cooling due to a fall in economic activity. The question that remains open is how low they will go.

However, the recent drop in oil prices and the basis effect that is coming may let one conclude that the peak in inflation might be in (NOTE: for now). Given that it is used heavily in industrial production, the price of copper is a good indicator of economic development. Year-to-date, the price has fallen about 23 %. Additionally, its ratio to gold is a good indicator for the development of 10y yields.

As you can see, the copper/gold ratio fell in 2018, and yields followed later. However, this time the situation is a bit different from 2018 because 2018 marked the end of the tightening cycle, and the Fed started its not-QE intervention in the repo market, while in 2022, we are at the beginning of the cycle.

I am not entirely convinced that the peak in yields is behind us for this year because as the Fed is shrinking its balance sheet, it takes liquidity out of the market, especially if recent gains in equities turn out to be the result of a bear market rally that sells off again.

Apart from falling commodity prices, the yield curve re-inverted for the third time this year, which only underlines the probability of recession. Additionally to the negative 2s10s spread, the 3-months10s spread, a lagging indicator, is also narrowing.

I assume that the recent spike in equity prices is indeed the result of a bear market rally, and we have not seen the lows in equities. Volatility divergence between stocks and bonds has expanded, and therefore, I think there is pain ahead for equities.

Now that I have discussed the situation in the United States, I would like to move on to Europe. Europe’s situation is far more complicated than the situation of the US because the continent heavily suffers from its imposed sanctions against Russia since Europe is an energy importer and heavily reliant on Russian energy.

Due to upcoming maintenance work on Nordstream 1, many fear that Putin will stop to deliver gas via the pipeline afterward. That and a short strike from Norwegian workers in oil- and gas fields have pushed gas- and electricity prices higher.

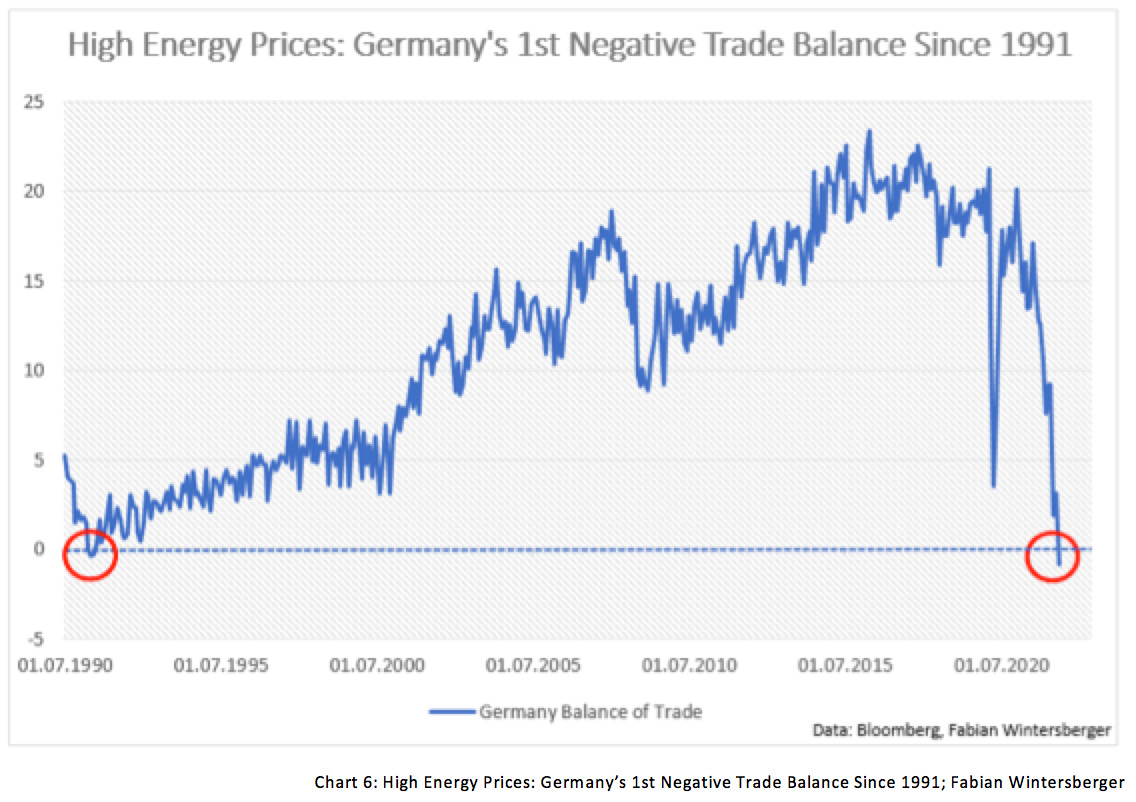

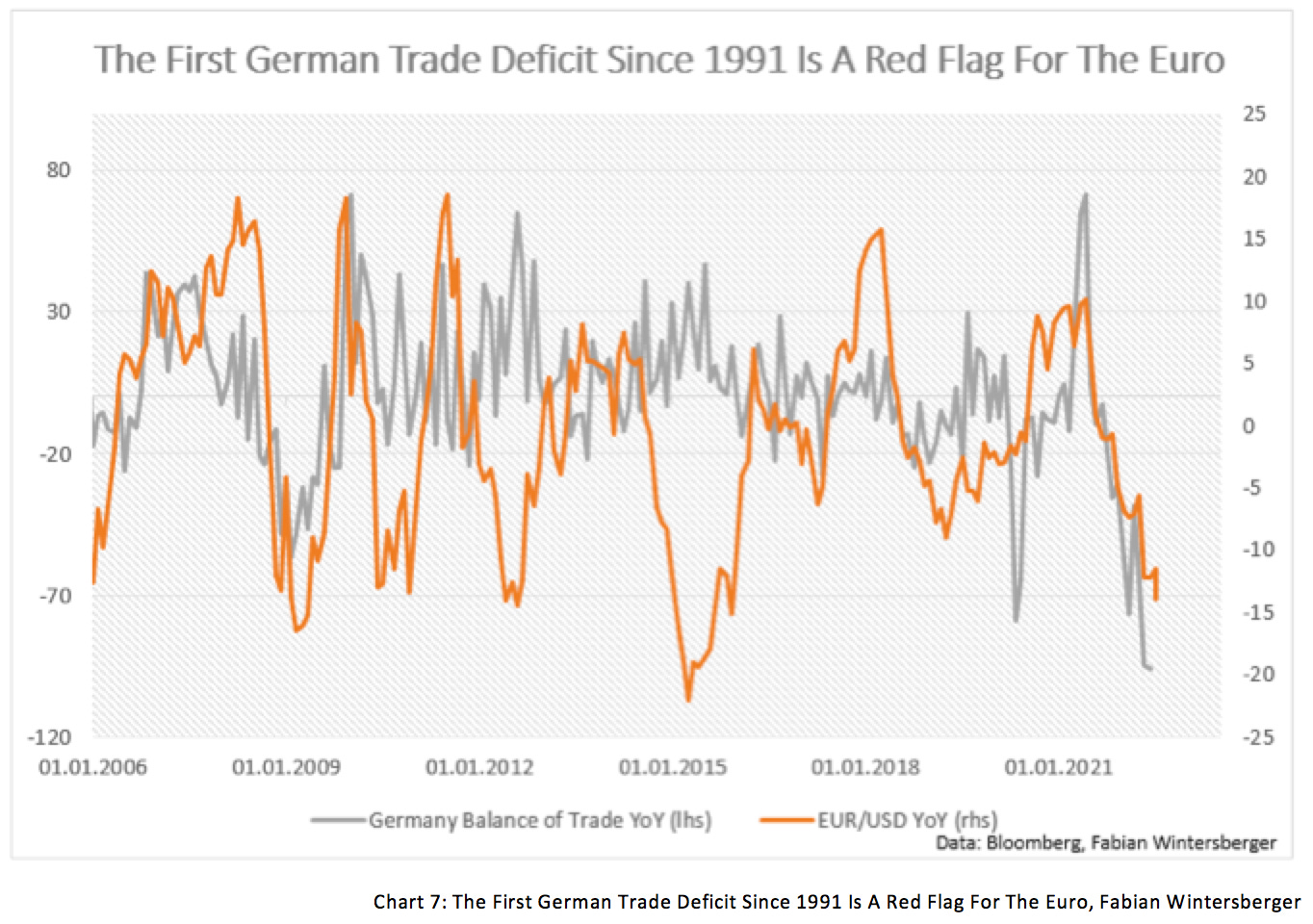

High energy prices are poisonous to the German export industry, which relied heavily on the availability of cheap (Russian) energy. But now that energy costs have risen sharply and import costs have gone up, Germany’s trade balance became negative for the first time since 1991.

Investors’ confidence in the euro has dwindled, not only because of the economic problems because of high debt levels from supporting the economy during the pandemic and the war but also due to the inactivity of the European Central Bank. The euro fell again this week, which will cause even higher import prices for commodities quoted in dollars. The German trade balance could stay negative for longer; thus, the euro might be poisoned for another move down. An exchange rate of 0.7 - 0.9 against the dollar seems possible.

High prices for energy imports, a weak currency, and falling investor confidence in the eurozone are a sign of a severe recession in the eurozone. Apart from that, it is very likely that political turmoil will spread all over Europe. Recently, dutch farmers started to protest against EU legislation which is threatening many farmers’ existence. In my opinion, such legislation is questionable during times when the global food supply is falling.

While the ECB seems busy with many things, such as working on a policy to ‘tilt’ corporate bond holdings to reflect climate risks, obviously, it has forgotten to fight the devaluation of the euro.

The reasons why the euro devalued are the expanded supply of euros due to fiscal and monetary stimulus to fight the economic consequences of the pandemic on the one hand and the fallen demand for euros because of rising economic uncertainty on the other hand.

Nevertheless, in such a case, it would be advantageous to have a central bank because the ECB could fight the devaluation by selling assets to extract euros from the market to stabilize the euro's value. However, this would have one side effect that I assume might explain why the ECB stands on the sideline and does not intervene. If the ECB sells assets into the market, it shrinks its balance sheet and raises the supply of bonds in the market, thus lowering the price/rising the yield for those bonds.

As a result, energy prices might become costlier for Europe, although the price is falling in dollars. One can only speculate if the energy supply for the fall and winter is secured for Europe. That could threaten the unified stand of the EU member states (apart from Orban’s Hungary, which does what it always does). At some points, the citizens might not accept that their governments are planning to spend billions on rebuilding Ukraine while sending its citizens into poverty. From a moral standpoint, it is understandable, but I fear the public will not accept that anymore at a certain point, and such things usually end badly.

The lecture that Europe is currently learning was avoidable, though. Instead of becoming dependent on Russian energy, Europe could have built up alternatives. For example, Europe could have exploited gas under its soil or built more nuclear power plants. But now, dependencies are there, and the shift will take years. In the worst case, some countries will opt out and follow their agenda. I expect economic and political uncertainty to increase rather than decrease in the coming years.

That leads me to my short-term market outlook and how all those things might affect financial markets.

While the sell-off in commodities was expected, given its sharp increase and rising recession fears, the question is how high prices could go, given that the energy market's situation remains tense. The US is planning to refill its SPR in the fall, and it seems that prices will stay elevated and not fall much further. The same is true for the European gas market, where supply is probably decreasing further. I am skeptical that paying people to save energy can calm the situation.

Rates might have plateaued for now and stabilize or fall due to the expected shrinking economy. In the long end, the rise in bond prices could mark a short-term upward countermove. The question, however, is if the market is speculating correctly and the Fed will pivot soon or if it is wrong. Nevertheless, in both scenarios, yields might rise over the medium term.

There is a dilemma in the making. Inflation will come down a bit due to the base effect and a fall in energy and commodity prices. One could argue that this is a success of central banks, but one should remember that a central bank pivot could quickly lead to higher inflation rates.

Equity markets might be in for a short-term but strong bear market rally because market participants are gambling on a Fed pivot. That is very shortsighted, and the rally could be over sooner than later. Due to lower liquidity during the summer season, this could take longer, though.

If the gains of the bear market rally sell off later, this, combined with central banks shrinking their balance sheets, could push rates back up, similar to what happened in 2020. In 2020, bonds started to rise sharply, and volatility picked up while stocks sold off, up to a point where suddenly market participants had to sell their bonds to cover their margin.

In 2020, bonds and stocks sold off until the central banks stepped in and flooded the market with liquidity. But we are far away from that point today. Nevertheless, regarding the narrative shift from inflation to the recession, one can say: it is on!.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)

Great article Fabian. You should jump on The Closingbell Show to discuss! We have 60,000+ in our community who'd love to learn from you. We recently had on Alex Morris, Ayesha Tariq and Tyler Okland :)