In Between

In the seventies, this is the tragic of American culture... That money became everything. And it has poisoned our culture to this day. It's poison ― Jerry Seinfeld

Many investors are engulfed by an unbreakable sense of euphoria whenever asset prices approach market tops. This same euphoria is vividly portrayed in films such as "The Great Gatsby" (2013), where director Baz Luhrmann brings to life the roaring 1920s in New York through the extravagant lifestyle of Jay Gatsby (played by Leonardo DiCaprio).

Gatsby is depicted as a mysterious and affluent figure known for his lavish parties and relentless pursuit of the American Dream. The film captures the essence of a society reveling in newfound wealth and freedom, experiencing a collective sense of euphoria and limitless possibilities. Gatsby's grand displays of wealth and his passionate pursuit of Daisy Buchanan (played by Carey Mulligan) reflect the emotional highs that often precede market downturns.

As the story unfolds, Gatsby's emotional peak transforms into a profound downfall, echoing the dynamics observed near market tops. Gatsby's relentless pursuit of wealth and status, driven by his desire to win back Daisy's love, symbolizes the excesses and illusions of economic booms. The film metaphorically explores themes of ambition, love, and the consequences of relentless pursuit, mirroring the optimism and exuberance prevalent in financial markets at their peaks.

In financial markets, emotional highs near market tops often manifest as a collective sense of invincibility and prosperity. Investors may display irrational exuberance, overlooking risks and believing in endless growth. This euphoric phase, characterized by extravagant spending and speculative behavior, is marked by a pervasive optimism about the future. However, a vulnerability that foreshadows the impending drawdown lies beneath the surface of wealth and success.

The anticipation of a market drawdown, akin to Gatsby's downfall, introduces a sense of foreboding in the narrative. The film portrays the gradual unraveling of Gatsby's dreams and illusions, echoing the sobering reality that follows periods of euphoria in financial markets. Similarly, investors may face harsh realities as market conditions shift and optimism gives way to uncertainty.

Through compelling storytelling and visual symbolism, "The Great Gatsby" is a cautionary tale about the consequences of hubris and misplaced faith in material success. The emotional journey of characters like Gatsby reflects the rollercoaster experienced by investors during market cycles. The film's narrative arc captures the essence of emotional highs near market peaks and the inevitable drawdown that follows, underscoring the cyclical nature of economic booms and busts.

The emotional dynamics portrayed in "The Great Gatsby" are a powerful metaphor for the sentiments preceding market downturns. As investors experience emotional highs and collective exuberance, the narrative reminds us of the transient nature of prosperity and the sobering realities accompanying economic transitions. The film's thematic resonance underscores the importance of prudence and perspective in navigating financial markets amid shifting optimism and uncertainty.

Currently, market sentiment regarding the short-term economic trajectory remains broadly optimistic, which is typical when equity prices are hovering around all-time highs. Despite signs of a slowdown in the US economy, it's important to note that this slowdown occurs after a period of exceptionally high economic activity driven by monetary policy expansion in the early 2020s.

This feeds into the optimism articulated by many investors, bolstered by confidence that the Federal Reserve's interest rate increases won't negatively impact the economy as initially feared when rate hikes began in early 2022. Economic growth continues at a solid pace, inflation has moderated (although it remains above the Fed's target), and job market data remains reassuring.

Across the European continent, PMIs are signaling that Eurozone countries have reached a bottom and are now experiencing economic expansion. This discrepancy has contributed to the Eurostoxx 50 outperforming the S&P 500 this year. Additionally, the ECB has indicated a potential interest rate cut before summer, contrasting with uncertainty in the US regarding the interest rate path due to persistent consumer price inflation in the early part of the year.

While the widening expected interest rate differential between the eurozone and the US has benefited the dollar, the recent euro appreciation against the dollar may have caught investors off guard. At first glance, the current economic environment might suggest that the euro should depreciate against the dollar as we advance.

However, the eurozone economy has started to exhibit positive surprises while US economic data has shown signs of increasing slowdown, shifting expectations for the interest rate differential. If this trend continues, it could lead to further appreciation of the euro relative to the dollar. In summary, market sentiment remains optimistic amidst high equity prices, tempered by US economic indicators signaling a slowdown from a robust period.

Meanwhile, Eurozone countries show signs of economic recovery, influencing currency dynamics and investor expectations regarding interest rate differentials between the eurozone and the US. Ongoing shifts in economic data and central bank policies will continue to shape market sentiment and currency valuations in the coming months.

While the market appears confident about the upcoming steps in the eurozone, there is far greater uncertainty surrounding the trajectory the Federal Reserve will choose, which is quite justified. The euro experienced a sharper inflation decline than the ECB anticipated, whereas the US has seen the opposite trend. Persistent consumer price inflation this year led to speculation about the Fed's need for additional rate hikes.

Another rate hike from the Fed would undoubtedly have exerted more pressure on US equities. However, since Jerome Powell essentially ruled out further hikes at the latest FOMC press conference, the current economic landscape suggests no immediate pressure on stocks. Moreover, the latest US data released on Friday was favorable.

Nonfarm Payrolls fell short of expectations for the first time since March 2023. In April, the US economy added 175 thousand jobs, 65 thousand fewer than expected. While this result was weaker than anticipated, it still reflects a healthy trend in the labor market, marking the 40th consecutive month of employment growth in the US. However, it was the most significant shortfall since March 2022.

The unemployment rate rose slightly from 3.8% to 3.9%, and average hourly earnings growth slowed from 4.1% to 3.9% year-over-year. On a month-over-month basis, hourly earnings grew at a 2.4% pace, aligning with the Fed's desired trajectory. Although this indicates a slight cooling in the labor market, the numbers do not support the assumption of imminent economic turbulence.

Following the data release, the market slightly adjusted its expectations for rate cuts, moving them forward. Nonetheless, based on current information, there is still little reason for the Fed to cut rates earlier or more than once this year, at least according to the headline numbers.

On the other hand, the data also does not suggest that the Fed will raise interest rates again this year. Therefore, the market's view is either correct in predicting no more than one rate cut this year or underestimates the potential future weakening of the US economy. Interestingly, Tavi Costa from Crescat Capital pointed out that the unemployment rate has risen above its 24-month moving average. Historically, this pattern has consistently resulted in a notable surge in the unemployment rate dating back to 1969.

While the US S&P PMIs support the assumption of continued economic growth this year, the ISM report indicates further weakening. Instead of the expected acceleration from 51.4 to 52, the ISM Services index dropped to 49.4, suggesting a shift from expansion to contraction in the service sector.

Concerningly, the prices paid index in the ISM report increased significantly from 53.4 to 59.2, suggesting intensifying inflation pressures that contradict assumptions of economic weakening. However, it's important to note that this index only reflects the number of respondents reporting price increases, not their magnitude.

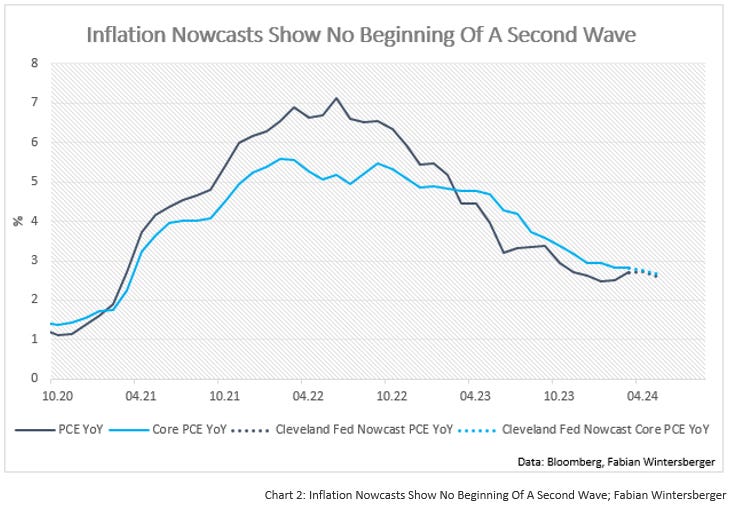

The Cleveland Fed's CPI Nowcast does not support the thesis of rising inflationary pressures, indicating that slowing money supply growth will lead to continuous disinflation. Forecasts for April and May continue this disinflationary trend, fueling hopes for a "Goldilocks" economy.

Combined with the Atlanta Fed's GDP Nowcast of 4.% annualized for the second quarter, the environment appears favorable for equities. Decelerating consumer price inflation alongside robust economic growth and a strong job market should provide support in case of further economic weakening unless such weakness becomes significant.

In summary, recent economic data suggests a slowing but not crashing US economy and falling inflation, which could alleviate pressure on the bond market. However, this also does not imply an imminent significant drop in yields, as the Fed is not rushing to act. Consequently, the upside potential for bonds may be limited, although short-term bonds could see gains if market sentiment shifts in anticipation of earlier rate cuts.

Currently, long-term bond yields are gradually rising, causing a reversal in the yield curve. This upward movement should be limited if the US economy continues to grow steadily. However, a deterioration in economic data could lead to more rate cuts than currently priced in, accelerating the yield curve inversion as both the short and long ends of the curve start to decline. This scenario, though, remains in the future.

As a result, the US stock market is likely to fluctuate around current levels, with potential dips being bought. It's probably not the time to significantly increase or reduce exposure to stocks, especially since the fear of additional rate hikes has dissipated. The slowdown in wage growth could additionally benefit business margins in the short term.

In addition, I have a strong suspicion that the recent increase in economic activity in Europe is partly attributable to the continued strength of the US economy. Eurostat data indicates that since the Russian invasion of Ukraine in 2022, trade relations between EU countries and the United States have intensified.

In 2023, the EU exported €502 billion worth of goods to the United States while importing €344 billion worth of goods creating a €158 billion surplus for the EU.

This positioned the United States as the largest partner for EU exports of goods, accounting for 19.7% of total extra-EU exports, and the second largest partner for EU imports of goods (following China), comprising 13.7% of total extra-EU imports.

Furthermore, EU countries have significantly increased imports from the United States, especially in the energy sector, as members sought to reduce reliance on Russian oil and gas. Total imports have nearly doubled since 2021, with a corresponding near-doubling in energy imports from the US during the same period. EU exports to the US increased by one-fifth.

However, the EU still faces economic challenges domestically despite benefiting from lower inflation, which has increased real incomes and supported domestic demand. Nevertheless, a doubling of mortgage rates has pressured the housing market, leading to decreased demand and house prices. The construction PMI in the eurozone recently dropped to 41.9, highlighting significant challenges in the construction sector.

Additionally, increasing regulatory burdens have dampened the EU's foreign investment appetite. Between 2012 and 2022, annual foreign direct investment into the EU decreased by $120 billion, while foreign investments into the US increased by $90 billion annually. Nonetheless, there are positive developments, particularly regarding Europe's position in global production. Chinese carmakers plan to increase sales of electric vehicles in Europe and establish manufacturing facilities to support this expansion.

The weak economic situation in China is also impacting Europe's economies, given that China is Europe's largest export market. Furthermore, the conflict between Russia and Ukraine has strengthened political and economic ties between the US and Europe. My thesis is that improvements in the EU economy will continue as long as the US economy avoids a recession.

Reflecting what is believed to be the beginning of a recovery, Deutsche Bank recently raised its growth forecast for 2024 by 0.5 percentage points to 0.3%, while Bloomberg increased its estimate of EU GDP growth to 0.6%. Although these forecasts appear promising, it's important to note that the economy would still grow well below its pre-pandemic trend.

Therefore, one should not mistake the current strengthening of the euro for a reversal of the long-term trend. Based on the abovementioned factors, the euro appears significantly overvalued against the US dollar over the medium to long term. However, given the prevailing negative sentiment towards the euro and the shifting relative economic strength between the eurozone countries and the US, the recent euro appreciation may continue as long as the US economy avoids recession.

Additionally, the current resilience of the US economy can be attributed in part to ongoing geopolitical developments that have brought the EU closer to the US. While EU countries primarily support Ukraine with weapons, ammunition, and financial aid, US assistance primarily benefits its defense industry.

Most of the money is being spent here in the United States. That’s right: Funds that lawmakers approve to arm Ukraine are not going directly to Ukraine but being used stateside to build new weapons or to replace weapons sent to Kyiv from U.S. stockpiles. Of the $68 billion in military and related assistance Congress has approved since Russia invaded Ukraine, almost 90 percent is going to Americans, one analysis found.

This implies that US aid for Ukraine is acting as an economic stimulus for the US economy, as the funds are reinvested domestically. This could be a driving force behind the Biden administration's efforts to secure increased support for Ukraine.

However, connecting the dots reveals that the US economy arguably benefits from the ongoing conflict at the expense of its closest ally, the EU. The war has stimulated business for US industries. In addition to the US funds allocated to Ukraine, the EU's plans to increase defense spending will further benefit US arms producers, as the US is the world's largest weapons exporter.

The US energy industry is another beneficiary of the conflict, as the EU shifts away from reliance on Russian energy supplies and increases imports of liquefied natural gas (LNG) from the US. In 2023, the US accounted for nearly 50% of all LNG imports into the EU and the UK.

Last year marks the third consecutive year in which the United States supplied more LNG to Europe than any other country: 27%, or 2.4 billion cubic feet per day (Bcf/d), of total European LNG imports in 2021; 44% (6.5 Bcf/d) in 2022; and 48% (7.1 Bcf/d) in 2023.

This raises the question of whether the US has any interest in ending the war in Ukraine, given that it appears to be benefiting economically from the conflict. A resolution to the war seems more distant than ever. Russia appears to have lost interest as it gains the upper hand on the battlefield, while Ukraine understandably seeks to maintain its territorial integrity.

Europe lacks significant influence as a geopolitical player, while China's approach appears ambivalent, primarily focused on pursuing its own interests. This situation leaves the US as the primary geopolitical actor capable of brokering any agreement between the warring parties, although its current interest may be limited from an economic standpoint.

However, if the softening of the US economy transitions into weakness and leads to a recession, US interests may shift. This remains a story for the future, akin to the current situation in financial markets, where euphoria and optimism prevail among investors and foreign policymakers alike.

I refrain from making geopolitical predictions as I am not an expert in that field. Regarding the economy, the current environment appears to be in flux between expansion and contraction. Unlike in 2023, when recession fears were widespread, the prevailing sentiment now leans toward cautious optimism, with few expecting a recession in 2024.

Up on the mountain, I see down below

It's easy to lose yourself, I know

Can't hear what you're shouting, I'm deaf to your show

It's easy to lose your self-controlBeartooth – In Between

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. They do not constitute investment advice, and my perspective may change over time in response to evolving facts. It is strongly recommended to seek independent advice and conduct your own research before making investment decisions.

Scary to thing that the US might not be interested to end the war in Ukraine. Especially because that can be extrapolated to any war, where the US is not directly involved in.

Thanks for the nice pre-weekend read.