Imperium

Disinflation Today, Directed Growth Tomorrow

There is nothing more difficult to take in hand, more perilous to conduct, or more uncertain in its success than to take the lead in the introduction of a new order of things. — Niccolò Machiavelli

While markets remained pretty calm on Monday due to Presidents’ Day in the US, various markets look as if they don’t really know where to move next. With last week’s strong NFP report and Friday’s good CPI numbers, the market still seems undecided about what to do with all this information. As I write this one day sooner than usual, I think that there is a chance that something is building up over the longer term.

US CPI: Further Short-Term Disinflation, But Potential Acceleration Later

Whenever the US Bureau of Labor Statistics publishes the latest CPI numbers, the same debate resurfaces about whether the figures actually reflect “true” consumer price inflation. One can certainly question methodology, weighting, or substitution effects, but I have largely stopped engaging in that discussion.

For markets, the decisive factor is not whether CPI perfectly captures price dynamics. What matters is that market participants treat it as relevant. As long as CPI shapes expectations for monetary policy and asset prices, the debate about statistical purity becomes secondary.

The latest report came in slightly below expectations, with headline inflation at 2.4% versus 2.5% expected. This was interpreted immediately as confirmation that the disinflationary process remains intact and that rate cuts are justified. As always, the report can be analyzed in multiple ways—trimmed mean CPI, supercore, shelter components—and, as always, one can construct arguments in either direction depending on the preferred metric. I am less interested in forecasting the exact decimal point than in assessing the broader direction of price dynamics.

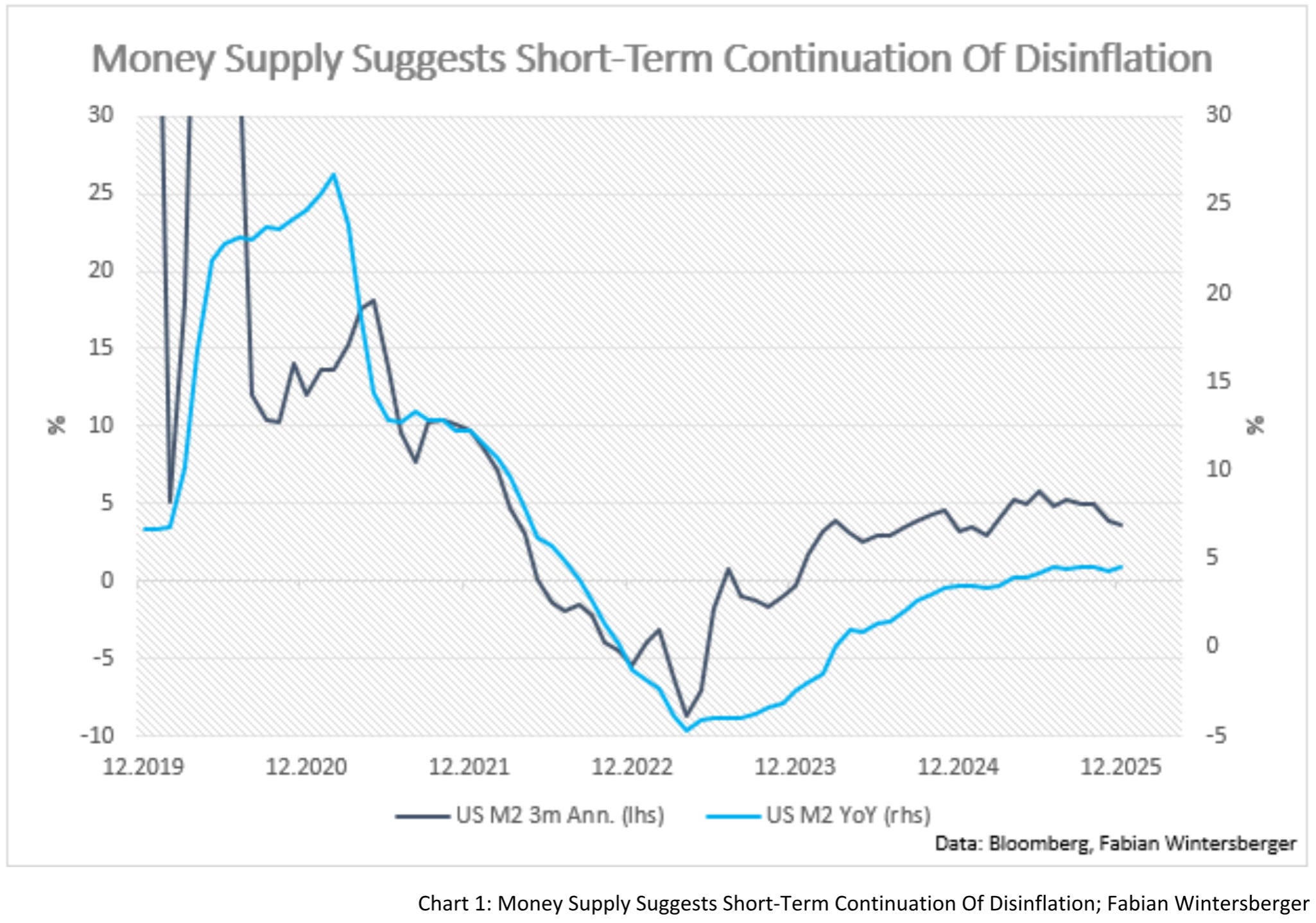

To evaluate that direction, I continue to focus on what ultimately drives average prices over time: money supply and money demand. While we lack a direct measure of money demand, proxy indicators such as the persistently low savings rate, robust consumption figures, and stable spending suggest that money demand has at least stopped falling. That distinction matters. The earlier phase of elevated inflation was not merely a function of expanding aggregates, but also of declining money demand following the distortions of the pandemic period.

If money demand has now flattened out, the inflationary impulse from that adjustment should fade in the short term. Meanwhile, M2 growth — although far from explosive — has been mildly expansionary for more than a year. The combination of stable money demand and moderate aggregate growth points toward further short-term disinflation rather than renewed acceleration. In that sense, current price developments are not particularly surprising.

Over the longer horizon, however, the picture becomes less clear. Government borrowing remains elevated, fiscal deficits are substantial, and the rechanneling of funds from financial markets into the real economy continues. If money supply growth persists and fiscal expansion remains structural rather than cyclical, inflation pressures could re-emerge later in the year. The present cooling phase, therefore, does not necessarily imply a durable return to the pre-2020 inflation regime.

For now, CPI remains in disinflation mode. But the underlying monetary and fiscal backdrop suggests that this phase may not be permanent.

Joint EU-Bonds Are Coming, But They Won’t Be The Solution

Recently, Emmanuel Macron once again pushed for joint EU bonds. Officially, the argument centers on strengthening Europe’s capital markets and creating a common, liquid benchmark safe asset.

What made this push noteworthy was not Macron. France has long advocated joint issuance. What was surprising was the support from Joachim Nagel of the German Bundesbank.

The European Central Bank’s policymakers, Nagel said in an interview on Friday, see “the benefits of creating a common European, highly liquid, euro-wide benchmark safe asset. Action is necessary.”

At first glance, the logic sounds compelling. If Europe wants a capital market that can compete in size and liquidity with the US Treasury market, it needs something comparable. A euro-wide safe asset could — at least in theory — play that role.

And if one believes that the dollar-centric system will eventually give way to something more multipolar, such an instrument would indeed be a prerequisite.

But that may not be the real story.

Nagel also pointed toward financing a joint EU defense budget. In other words, the capital market argument might be the wrapper — not the core.

Joint issuance expands fiscal capacity at the supranational level. And once borrowing is mutualized, allocation becomes political. The more debt is centralized, the more power shifts upward.

It is therefore no surprise that the European Commission has long been in favor of such instruments. Control over borrowing implies influence over distribution.

At the member-state level, the incentives are equally clear. Countries such as France and Spain benefit from raising borrowing constraints. As Stanford economist Hanno Lustig wrote on X:

Hey roommate, I’m bumping into my credit limit on my credit card. Let’s get a joint credit card?

That captures the political economy dynamic rather well. But even if joint EU bonds are issued at scale, a more basic question remains: why should global capital reallocate toward Europe?

The dominance of US Treasuries is not simply about supply. It reflects deep and dynamic capital markets, relative institutional stability, and a corporate sector that continues to innovate and generate growth.

Europe, by contrast, struggles with structural issues: regulatory complexity, demographic headwinds, and declining competitiveness. A liquid safe asset does not solve that. One cannot engineer reserve status through issuance alone.

Without stronger productivity growth and a more attractive environment for private capital, joint EU bonds risk becoming primarily a funding tool — not a structural solution. Liquidity is not the same as dynamism.

Strategic Capital & The Flexibility Of The Private Sector

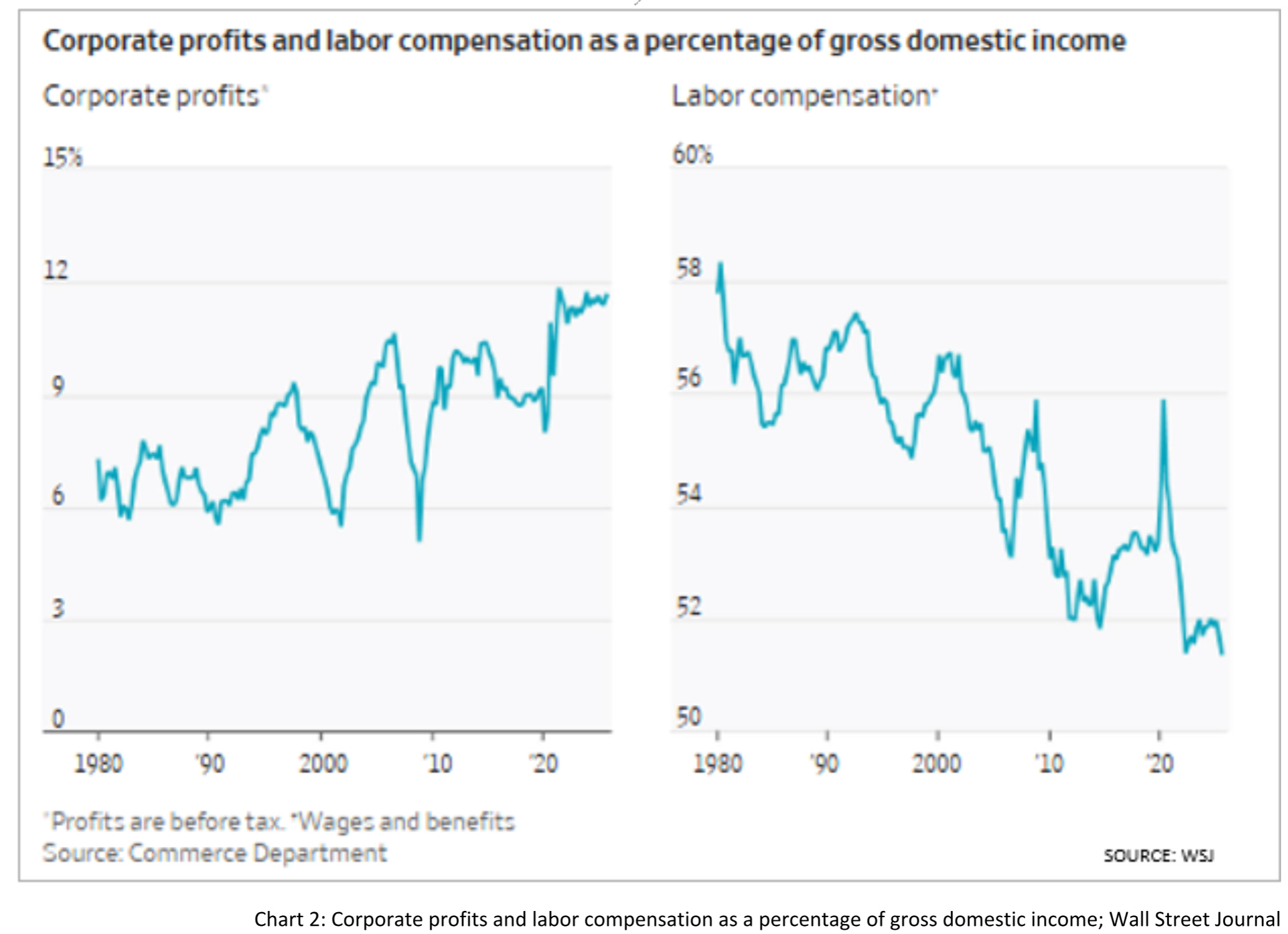

Last week, the Wall Street Journal ran a piece arguing that capital investment has become a dominant contributor to corporate profits. At the same time, labor compensation as a share of domestic income has declined.

Given the prevailing narrative of an upcoming capex supercycle — driven by AI, reshoring, and industrial policy — one could easily conclude that this trend will simply continue. But there is a catch that many seem to overlook.

The dominant storyline today is that artificial intelligence will soon displace large parts of the workforce and push unemployment higher. Yet that narrative is not reflected in actual labor market data. Recent payroll figures were strong; participation increased; U3 and U6 unemployment declined; and employment quality improved. That does not appear to be a labor market on the brink of technological displacement.

The argument, in my view, misses something more fundamental: implementation. AI may increase productivity in theory, but such gains materialize only when firms successfully integrate new technologies into their business processes. That takes time, coordination, and managerial adaptation. Business solutions remain narrow, specialized, and unevenly distributed. The productivity revolution is not automatic.

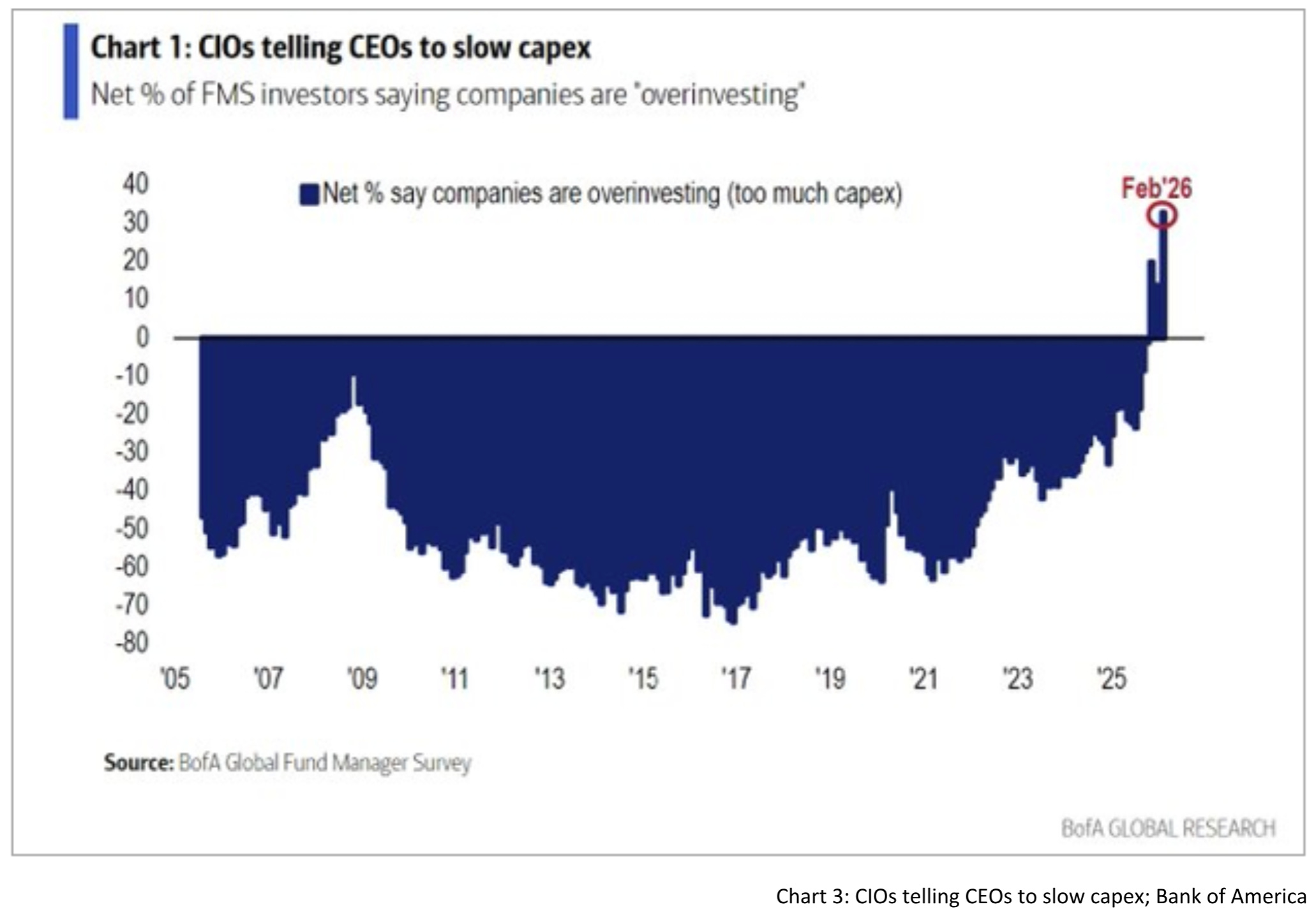

At the same time, investor sentiment toward capital expenditures appears to have shifted. Survey evidence suggests that many believe companies may be overinvesting.

This creates an interesting tension. On the one hand, firms publicly commit to large investment programs. On the other hand, internal and investor signals suggest caution.

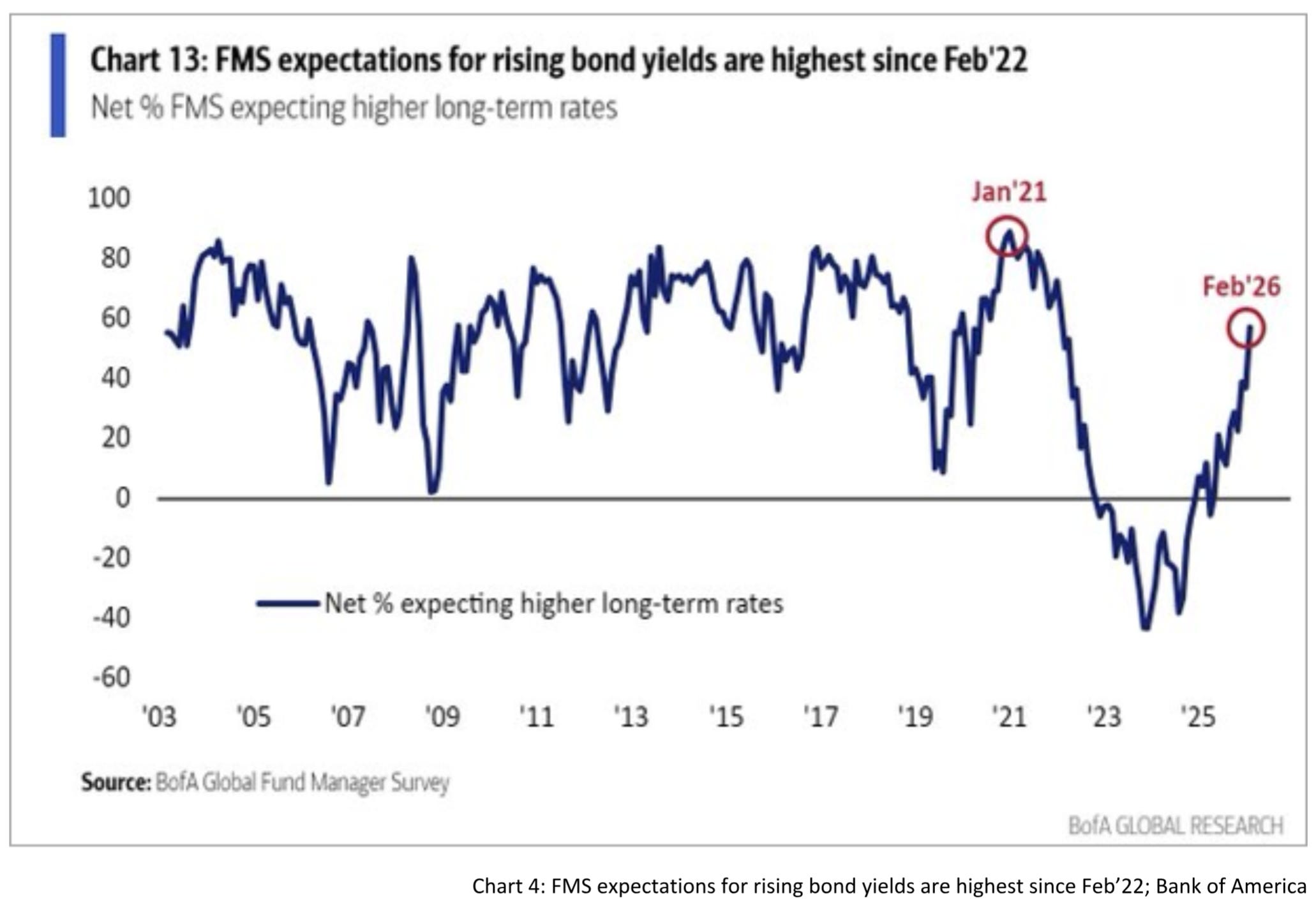

If we combine this with last week’s strong employment data, a different picture emerges. Businesses may be hiring in response to economic strength rather than accelerating capital commitments. That would not be irrational. We have moved from a regime of ultra-low rates to one of structurally higher real rates. In such an environment, long-duration investment projects face a higher hurdle rate. Labor, by contrast, remains comparatively flexible. It can be scaled up more gradually and adjusted more easily if conditions change.

In other words, firms may be choosing optionality over long-term commitment.

Stable consumer demand and improving employment quality justify expansion. However, uncertainty regarding the pace of technological change, the trajectory of real interest rates, and geopolitical shifts increases the value of flexibility. Higher real rates do not eliminate investment; they can delay it.

However, this does not imply that aggregate capital expenditure will collapse. The newest National Security Strategy heavily emphasizes state-directed investment in critical infrastructure, defense, and strategic industries. While private firms may hesitate at the margin, government-backed capital allocation is likely to remain robust. Unlike private actors, the public sector is less sensitive to financing costs — particularly if fiscal and monetary authorities coordinate to prevent yields from rising too far.

What we are witnessing, therefore, is not a simple slowdown in capital formation. It is a shift in composition. Private firms emphasize flexibility and labor expansion, while public policy increasingly directs capital toward strategic objectives.

The result is a peculiar mix: resilient employment, selective private capex, and structurally supported government-driven investment. The cycle remains heavily shaped by fiscal and monetary intervention. But rather than pointing toward an imminent collapse, this configuration may support further economic acceleration—albeit one increasingly shaped by policy rather than purely market-driven allocation.

The question, therefore, is not whether growth stops abruptly. It is what kind of growth we are producing — and at what cost.

Now, let’s assess the further trajectory for markets.

Bonds & Interest Rates

The picture for bonds has shifted over recent weeks. While the broader structural backdrop still argues against a durable bull market in fixed income, the recent combination of cooling CPI and resilient growth opens the door for a tactical rally. Both 10-year Treasuries and Bunds have recovered since early May, and price action increasingly suggests that positioning may have become too one-sided.

With fund managers still structurally underweight duration, even modest disinflation can trigger further short covering. The recent flattening of the yield curve reinforces the impression that we are witnessing a countertrend move rather than the beginning of a secular shift. For now, the balance of risks favors additional upside in bonds — but the fiscal and structural backdrop makes me skeptical that this is the final turning point.

Stocks

Equities have moved sideways since the beginning of the year, yet price action remains constructive. If the bond rally continues and real yields drift lower, this could act as a tailwind for risk assets. The key question is whether falling yields reflect a dovish central bank or a deteriorating growth outlook.

At present, the data do not indicate a sharp slowdown. Labor markets remain resilient, employment quality has improved, and strategic capital allocation continues to support activity. In that sense, the market may still be underestimating the possibility of renewed economic acceleration. For now, price action does not signal an imminent sell-off.

FX, Gold & Bitcoin

The latest dollar strengthening is not necessarily a structural turnaround so far, as EUR/USD remains in a broader bullish trend. However, as noted in prior comments, for a sustained higher continuation, EUR/USD must break the resistance area between 1.20 and 1.25. So far, that has not been achieved.

Meanwhile, gold failed to hold above the $5,000 level. If the price fails to reclaim that area convincingly, we could see further downside pressure in the short term. The same applies to Bitcoin, where — in my view — the broader bear market phase is not over yet.

Conclusion

At present, price action remains supportive of equities. In particular, the countertrend rally in bonds may serve as a short-term tailwind. Over the longer term, however, the picture looks different. If the US economy continues to reaccelerate, this could eventually put renewed pressure on bonds further down the road.

Consumer price inflation appears to be cooling further, although some upcoming CPI prints may surprise to the upside. Later in the year, the jury is still out. But with the US attempting to retain its global “Imperium,” the combination of flexible private-sector behavior and government-backed capital expenditures could ignite another phase of economic acceleration before more serious strains emerge.

Europe’s push for joint EU bonds, by contrast, does not address the continent’s structural regulatory and competitiveness challenges.

What currently appears calm on the surface may simply be the early stage of that buildup. The next phase will not be defined by whether growth slows — but by how it is directed.

Hear me now

I’m taking back the control

Of my

Life from society’s holdMachine Head – Imperium

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.