I'm Not Jesus

It is not the case of choosing those which, to the best of one’s judgement are really the prettiest, nor even those which average opinion genuinely thinks the prettiest. We have reached the third degree, where we devote our intelligences to anticipiating what average opinion expects the average opinion to be. And there are some, I believe, who practise the fourth, fifth, and higher degrees.

- John Maynard Keynes

In 2011, Warren Buffett said that Chapter 12 of John Maynard Keynes's The General Theory of Employment, Interest, and Money is one of the most important chapters ever written on investing.

You don’t need to read anything else & can turn off your TV

In Chapter 12, Keynes compares short-term price fluctuations in the stock markets with a beauty contest in a newspaper where the judges are rewarded if they choose the person most readers consider the most beautiful instead of the one they think is the most beautiful. According to Keynes, this is how short-term traders in the stock market choose the stocks for their portfolio instead of picking them due to long-term fundamentals. Keynes says that traders behave just like gamblers in a lottery.

One is reminded of politicians and activists who condemn the stock market as a form of a casino, where fundamental data hardly play a role, and everyone is just chasing short-term gains. And indeed, sometimes, one cannot rationally explain developments in financial markets. Thus it is trendy to draw a narrative on why traders trade this and that, although from a fundamental perspective, one would have expected other movements.

On the other hand, Henry Hazlitt, who presumably wrote the most in-depth critique of Keynes's General Theory, called Chapter 12 an essay in satire, where Keynes mixes plausible with implausible statements, hoping that the latter will seem to follow the former. Among other things, Hazlitt uses British Railway and two ice firms to show that empirical data do not support Keynes’s anecdotal examples.

As a journalist in New York, who wrote about happenings on the New York Stock Exchange daily, Hazlitt knew what he was talking about. The mere truth is that Keynes tries to blame speculators and distinguish them from true entrepreneurs, while, in reality, both things are similar. Every human action in an uncertain world is a form of speculation.

Further, Keynes’s critique is even more ironic because, as Hazlitt also notices, suddenly, he seems to care about the long-term (emphasis added):

Keynes once derided economists who worried about results ‘in the long run.’ ‘In the long run,’ he said cynically, ‘we are all dead.’ It is amusing to find the same man complaining here that long-run considerations are minimized becaue ‘human nature desires quick results, there is a peculiar zest in making money quickly, and remoter gains are discounted by the average man at a very high rate’ (p.157)

In retrospect, it is easy to dismiss specific actions of market participants as crazy speculation. Basically, Keynes only detects that predictions are hard, specifically about the future, especially when the assumptions turn out to be overly optimistic at some point. In months like these, where stock markets are rising despite fundamental data pointing south, Chapter 12 is used again to explain certain events.

The German DAX briefly reached another all-time high this week, which one would not have expected looking at German economic data. However, suppose one remembers how bad the outlook for the German and European economies was back in Winter. In that case, it is not far-fetched to assume that investors assess the situation as improving and more positive. Back then, many (me included) thought a severe recession was imminent for Europe, but incoming economic data showed that that was not the case.

Nevertheless, one has to see that speculation plays a crucial role in price discovery in a market economy. Whether economic actors will be right or wrong is something that only time can tell. Yet, in one thing, traders and Keynes agree 100 %, namely that when the facts change, they change their minds.

This week’s published Flash PMIs for Germany, the Eurozone, and the US showed that both economies still expand despite the Fed and the ECB rate hikes. From this point of view, it should not be a total surprise that equity indices did not do that badly. While investors expected a rapidly cooling economy at the beginning of the year, the fact that the economy is still expanding influences investors’ sentiment.

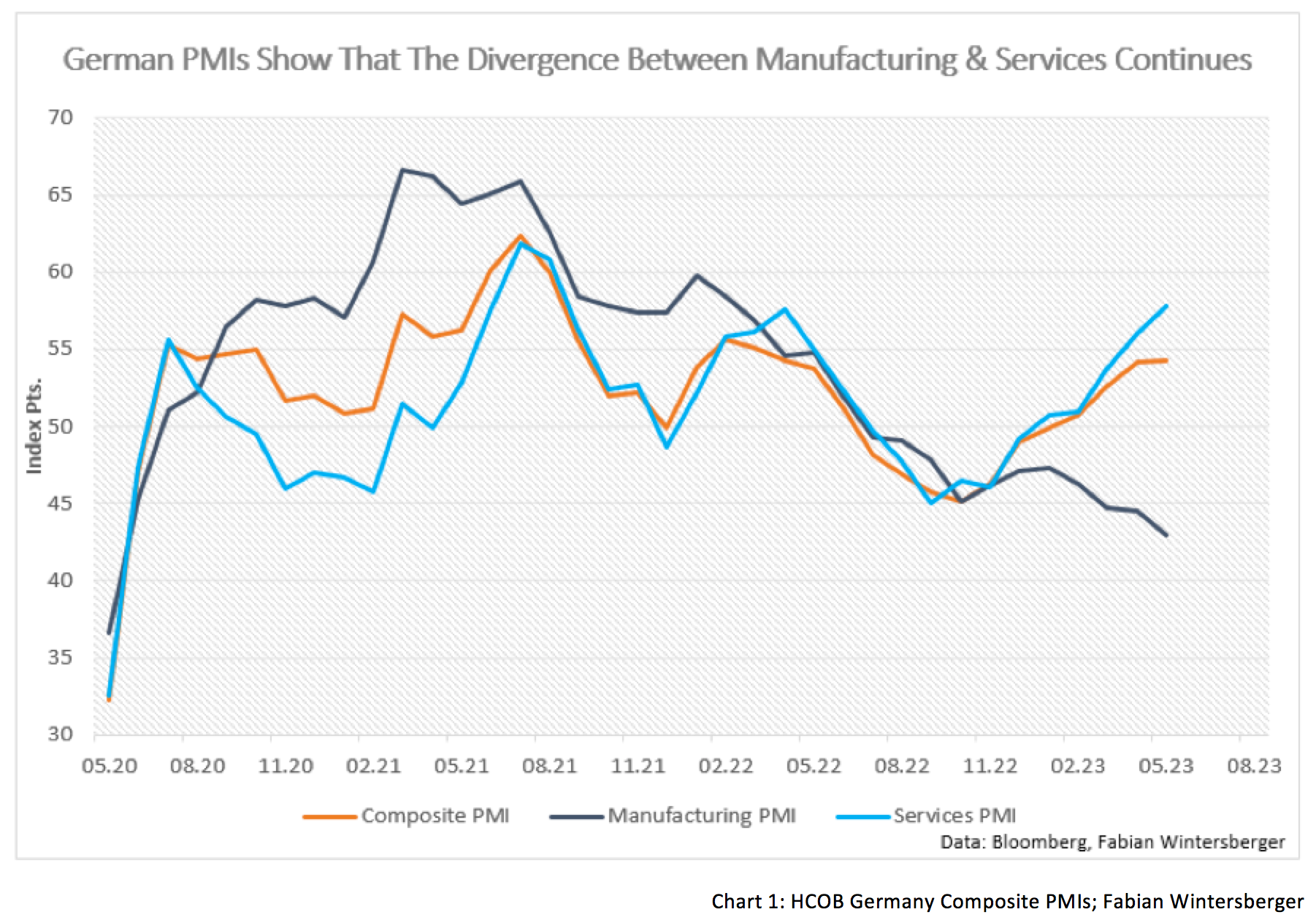

The German Composite PMI rose from 54.2 to 54.3 in April, a 13-month high. The expansion of the service sector is the reason that economic activity is still growing and the place where price pressures remain severe. While the German services PMI reached a 21-month high, manufacturing contracted further and reached a 36-month low.

The latest rise in workforce numbers extended the current sequence of employment growth to almost two-and-a-half years. The pace of job creation slowed from April’s 11-month high but was still solid by historical standards. Latest data did however show a continued slowdown in hiring activity in the manufacturing sector, with factory staffing levels posting only a modest rise that was the smallest for 27 months.

Manufacturing and services show a very unusual divergence, but since the service sector is more significant than manufacturing, it more than offsets the weakness in manufacturing. The situation is particularly bad for the German export industry, as, according to the report, foreign demand has virtually collapsed.

In services, falling input prices are not passed through to consumers. Instead, businesses have raised prices, which points to continued strong domestic demand. Wage increases and savings obviously are more than enough to keep consumption high, which will keep consumer prices elevated.

Still, this cannot go on forever. At some point, businesses will be unable to accept a continuous rise in wage growth because they cannot raise prices further. After all, higher prices at some point mean lower demand.

Eurozone PMI shows a similar picture. Services continue to expand while manufacturing slows. Most inflationary pressure comes from services, where rising costs (wages) are passed to consumers.

In Italy, the Meloni government has increased subsidies and caused a construction boom which is also driving the deficit higher, but currently, hardly anyone in financial markets seems to care. Italy, France, and Spain continued to grow during the Winter, and so did the eurozone as a whole.

However, the fact that Germany got better through the Winter than most expected is not all clear. Although recent data from the Ifo Institute show that the current assessment among businesses is still better than at year-end, expectations point to a continuous negative trend in Germany in the coming months.

While the business’s outlook improved during the Winter, it is not worsening again, which could slow the high-flight of the DAX. The bad sentiment is also influenced by the rigorous politics of German economic minister Robert Habeck, which is even causing disputes within the coalition because of his plans to ban fossil fuel heating. A recent study warns households that heat with fossil fuels will face an explosion in heating costs from 2026 onwards. The current government appears to be accelerating Germany's economic decline rather than slowing it down.

The PMI numbers for the eurozone are lousy news for Christine Lagarde and her colleagues at the ECB. If the ECB wants to continue to fight high consumer prices, more rate hikes are probably needed than market participants currently anticipate. I still stick to my thesis that the terminal rate will be above 4 %, which is higher than most investment banks expect, although the most prominent hawk within the governing council, Robert Holzmann (OeNB), stated last week that rate hikes above 25 basis points are probably not possible now.

The picture in the United States is similar. US Flash PMI data shows a growing divergence between manufacturing and the service sector economy, and flash Composite and the services PMI reached a 13-month high. And just as in Germany, US manufacturing is confronted with further shrinking foreign demand.

Yet, domestic demand remains solid, even though it has decreased slightly since January. This is supported by a statement from Mastercard CFO Sachin Mehra in last week’s earnings call:

So when you take something like the US market, which obviously is a big market from a spend standpoint, we had talked about how through the last couple of weeks of March and into early APril, we had seen a slight slowdown in spending driven by lower tax refunds primarily in lower gas prices. And - but otherwise, I would say the consumer remains remarkably resilient.

Currently, the strong service sector, increased factory capacity in manufacturing to work through order back-logs, and unemployment at record lows make for an extremely tight labor market. While initial jobless claims are slightly up from their previous lows, they are still at a low level, which caused Jerome Powell to argue that in the current hiking cycle, we probably will not see a rapid rise in unemployment.

So far, the labor market has remained remarkably resilient even though the business cycle is probably in the contraction phase, as its proxy, the ISM, suggests. Low labor supply leads to businesses bidding up wages to attract workers from other companies, who then quit their jobs.

In an article from February last year, economists Aaron Sojourner and Emily DiVito argue that the tight labor market has driven the economy's expansion. Back then, quits were at a record high, while firings and discharges were at a record low.

They argue that the ratio of both, the Worker Leverage Ratio, gives a good picture of the tightness of the labor market. If quits increase (everything else equal), businesses demand more workers than are currently available, leading to rising wages. But if firings and discharges rise, and companies demand less supply of workers, one can assume that wage pressures will decrease.

If one analyses the year-over-year change of the Worker Leverage Ratio with the ISM index (the business cycle), one sees that since the data exists, both correlate. The only exception is observable during the Trump presidency, where tax cuts improved business sentiment. Currently, the Worker Leverage Ratio is back to levels where it was during the Great Financial Crisis, and thus one can assume that wage pressures will come down later this year.

If the labor market eases, as one could assume due to the Worker Leverage Ratio, then wage growth in the United States should edge lower in the coming months. This normalization should lead to a slow in consumer spending.

This can probably drag on until the third quarter, when it is estimated that the savings cushion from the pandemic will be gone. But until that happens, there should be no doubt that the Fed will continue with its current rhetoric. However, if the economy experiences a sharp slowdown in economic activity in Q3, the Fed will be tested if it is as committed as it claims and stays restrictive in its monetary policy stance.

Consumer price inflation likely will continue to slow in the coming months, and real wages will rise. However, credit card spending growth is still highly elevated despite the recent gains in real wages. This indicates elevated inflation until the labor market worsens significantly or people cannot afford 20 % credit card interest rates.

Therefore, the expected rate cuts in September do not seem very plausible. The labor market and consumer spending speak against a pivot, even though real retail sales have stagnated recently. Nominal retail sales have risen with CPI, confirming that consumption remains stable despite rate hikes.

In conclusion, it can be stated that the situation in financial markets remains highly uncertain, which points to increasing volatility. Yet, in my opinion, the low VIX signals that the upside in equities is not endless, but it does not mean that markets cannot go higher. I think one should not expect a sharp sell-off in the coming months. Investors will interpret better-than-expected economic data positively, while weaker data will be perceived as neutral if the Fed does not pivot. A Fed pivot would point to coming economic turbulences and hence a sell-off.

Strongly elevated consumer prices in Europe give no hint that either the BoE or the ECB will end their restrictive monetary policy anytime soon if we do not see a slowdown in economic activity. Still, it is implausible that the ECB or the BoE will be more restrictive than the Fed. As a result, I expect a continuation of the rise in interest rates in the US and Europe, a rising dollar, and consistent or slightly lower precious metals and commodity prices.

It needs to be seen if my forecast is correct, as both bears and bulls can bring up some good arguments these days. That is the nature of short-term speculation on price movements - uncertainty. And we all know the saying that it was evident in hindsight. The future is still uncertain, and forecasters are not Jesus.

When your world comes crashing down, I want to be there

(If god is looking down on me), I’m not Jesus, Jesus wasn’t thereApocalyptica feat. Corey Taylor - I’m Not Jesus

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! If you like my writing, you can subscribe and get every post directly into your inbox. Also, sharing it on social media or liking the position would be fantastic!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice. I may change my view the next day if the facts change)

Well, it seems we are of the same opinion as I wrote essentially the same ideas this morning. good weekend