Hurricane

In the short run, the market is a narrative machine, but in the long run, it's a narrative debunking machine. – Benjamin Graham

When participants in financial markets seek out stocks for investment, they often prioritize fundamentals, a strategy commonly known as "value investing." This approach closely mirrors the investment philosophy of Warren Buffett, arguably the most revered investor globally, owing to his enduring success.

Buffett famously remarked that the opportune moment arises when a superb company faces transient challenges, likening it to acquiring assets "on the operating table." Investors widely adopt this perspective when evaluating individual stocks or even entire indices.

Expanding this principle to a broader scale, such as indices, entails identifying sectors or economies that underperform relative to their intrinsic fundamentals. However, it's crucial to heed the caution of John Maynard Keynes, who warned that "markets can remain irrational longer than you can remain solvent." Despite robust fundamentals, markets may defy logic and persist in unfavorable directions for extended periods.

Thus, while fundamentals wield substantial influence over the long term, their impact may diminish in the short and possibly medium term. In the theory of efficient markets, where economic actors are presumed to be rational beings (measured objectively), this discrepancy shouldn't occur. If markets indeed possess perfect information, as most economic theories propose, then worsening fundamentals should translate into falling asset prices, and improving fundamentals should lead to rising prices.

However, this overlooks that human actions are not solely dictated by objective rationality; emotions play a significant role. Furthermore, it's unsurprising that asset prices, including those in financial markets, are influenced by narratives.

Narratives significantly influence price discovery and shape market participants' expectations. Compelling narratives, a phenomenon well-known in the entertainment industry, heavily sway people.

Filmmakers use the phrase “Narrative Is Everything” to emphasise the importance of storytelling to their craft…Without a good narrative, even the best casts inhabiting the most wonderful characters risk failing to entertain. Great narratives can terrify you, warm your heart, or compel your attention.

When individuals encounter compelling narratives, they are more inclined to believe in their validity or potential realization. Familiar examples include narratives such as "AI is revolutionizing every aspect of life," "rate cuts will bolster asset prices," "gold possesses intrinsic value while Bitcoin does not," or "active stock picking is time-consuming and costly. Hence, passive investments are superior in the long run."

While these narratives aren't necessarily incorrect, one could argue that they are often exaggerated, leading to price overreactions and underreactions. However, investors should scrutinize the prevailing narrative and monitor emerging narratives in the short and medium term.

Consider the current state of the stock market as an example. Market participants are likely to express two primary narratives. Firstly, optimism regarding economic performance suggests that manageable interest rates may propel further stock market gains. Secondly, even if the Federal Reserve implements gradual interest rate cuts, it could potentially boost the stock market.

The past week has been eventful for financial markets. On Thursday, the European Central Bank (ECB) convened its monthly meeting to determine interest rates, which, as expected, remained unchanged. However, market participants hoped to glean insights into the potential timing of future rate cuts from ECB President Christine Lagarde during the subsequent press conference.

During her opening statement, Lagarde acknowledged the prevailing economic conditions, noting that inflation moderates while price pressures persist. Additionally, she highlighted the restrictive lending conditions, which could dampen demand and exert downward pressure on inflation. In light of recent data, the ECB revised down its growth projections for 2024 to 0.6%.

Delving deeper into specifics, Lagarde underscored the ECB's optimism for a modest economic recovery, elucidating the rationale behind their stance:

As inflation falls and wages continue to grow, real incomes will rebound, supporting growth. In addition, the dampening impact of past interest rate increases will gradually fade and demand for euro area exports should pick up.

Regarding inflation, Lagarde and her colleagues appear steadfast in their belief that the recent uptick in inflation was primarily driven by supply constraints, characterizing it as cost-push inflation. Consequently, the opening remarks offered little novelty for market participants.

This sentiment persisted throughout the subsequent question-and-answer session. Lagarde reiterated that policy decisions will hinge on "incoming data," refraining from indicating whether the ECB intends to implement interest rate reductions before June. In response to a query from a journalist, she directed attention to the ongoing influx of data:

Well, when you look at what will be published and what data we will have, in terms of activity, wages and profits, we will have a little in April, and we will have a lot more of that for our June meeting. It matters, because we are data dependent, and we are adamant that we will be data dependent.

Although not mentioned by Lagarde, another factor that could potentially influence the situation is the expectation that the Federal Reserve might also be planning to cut interest rates for the first time in June. It's widely understood within financial markets that the ECB typically follows the Fed's lead rather than vice versa.

However, I would argue that this time could be different, mainly due to the current disparities between the Eurozone and the US economies. While the US is still experiencing genuine economic growth, growth in the Eurozone remains stagnant. Moreover, I remain skeptical about the extent to which the situation will improve significantly in the coming months.

Therefore, I believe there's a non-negligible possibility that the ECB may move before the Fed, a sentiment echoed by some ECB's governing council members recently. While more hawkish members, such as Austria's Robert Holzmann, have essentially ruled out a rate cut in June, others, like François Villeroy de Galhau of the Banque de France, have not ruled out a rate cut in April.

Furthermore, although I anticipate the Euro will struggle to maintain ground against the dollar, an earlier move by the ECB could initially be interpreted as bullish for the Euro. If the prevailing narrative is that rate cuts will stimulate economic activity and growth, the Euro may appreciate against the dollar in the short term. However, as I've emphasized repeatedly, monetary policy today won't impact the economy until at least a year later, potentially leading to a shift from optimism to pessimism. Therefore, I don't anticipate the European economy benefiting significantly from the forthcoming rate cuts, at least not this year.

As a result, the recent uptick in the Eurozone economic surprise index relative to the United States should be viewed with caution and not overinterpreted. The index merely indicates whether incoming economic data exceeds analysts' expectations, not necessarily whether the data itself is positive. Until the underlying data shows consistent movement indicative of economic expansion, the surprise index merely suggests that the data surpassed previous expectations.

Now, let’s briefly recap last week's NFP report, released on Friday. Once again, payrolls surged significantly beyond expectations, totaling 273,000 (expected: 200,000). While this should have driven yields notably higher, this time, it didn't. The most apparent reason for this was the downward revision of January's numbers by over 100,000, from 353,000 to 229,000.

Manufacturing payrolls decreased by 4,000, with January's figures revised down from 23,000 to 8,000. Meanwhile, the unemployment rate increased from 3.7% to 3.9%, potentially signaling a weakening labor market, although it's important to note that this figure remains relatively healthy. Year-over-year average hourly earnings growth slightly declined but remains robust at 4.3%.

Conversely, as highlighted a month ago, average weekly hours increased marginally from 34.2 to 34.3. In a scenario of continued economic momentum, this trend is expected to improve further in the coming months. Overall, however, NFPs still indicate a resilient US economy with no recession on the horizon, providing a comfortable situation for the Federal Reserve.

While the outlook appears favorable for large corporations benefiting from borrowing long-term at low-interest rates, recent data concerning small business owners paints a less optimistic picture regarding the prospects of a successful economic expansion.

Even though many market participants overlook the National Federation of Independent Business's Small Business Report, I believe it offers valuable insights into the broader US economic landscape. After all, as per the Bureau of Labor Statistics, the majority of businesses employ fewer than 20 workers.

While analysts anticipated a slight uptick, the NFIB's Optimism Index actually declined further from 89.9 to 89.4. The report highlights that "this is the 26th consecutive month below the 50-year average of 98." It's evident that small businesses harbor a different perspective on the economy than advocates of a "soft landing."

Delving deeper into the report, businesses expressed increasing difficulty in finding skilled workers, although they found it relatively easier to recruit for unskilled positions. Furthermore, their intentions to fill open positions diminished further, with only a net 12% planning to create jobs in the next three months, as per seasonally adjusted data.

The sharp decline in small businesses' hiring plans historically indicates potential labor market weakening ahead. Presently, initial jobless claims do not indicate any signs of mounting stress. However, the discrepancy between initial claims and small businesses' hiring plans warrants close observation in the coming weeks.

The labor shortage experienced in 2023 prompted businesses to invest in labor-saving technology, yet capital spending remains subdued. Overall, investment activity is contracting, with businesses scaling back their plans for further capital outlays. The report underscores that long-term investment spending will remain tepid as long as business sentiment remains subdued.

Moreover, more businesses reported lower nominal sales, with a net negative of 13%, while a net negative of 10% anticipates reduced sales in the future, reflecting prevailing pessimism. Additionally, the report indicates a rise in excess inventory. Plans to increase compensation hit their lowest level since March 2021, and businesses cite persistently challenging borrowing conditions due to elevated interest rates, with the average short-term rate at 8.7%.

Regarding inflation, fewer owners intend to raise selling prices despite inflation remaining a primary concern for them. This suggests that passing on higher input costs to consumers could become increasingly challenging. One contributing factor here may be the increase in the minimum wage, which was implemented in 20 states across the United States.

From my perspective, the report indicates that substantial improvement in small business owners' conditions and sentiment is necessary to realize a "soft" or "no-landing scenario." While certain macroeconomic indicators indeed indicate this possibility, micro-level data continues to present a mixed picture.

Although the US economy continues to exhibit remarkable resilience to higher interest rates, some economists are beginning to voice concerns about the level of interest rates and are urging the Fed to expedite rate cuts. However, the Fed finds itself in a delicate position, as it perceives itself as a key player in preventing a "soft" or "no-landing" scenario. For instance, Isabella Weber recently asserted in an interview that central banks should initiate interest rate cuts immediately.

It's worth noting that economists like Isabella Weber argue that the experienced inflation stems from so-called "cost-push" inflation, wherein producers faced supply chain challenges and subsequently raised prices.

This comes as a surprise following Tuesday's recent release of the US Consumer Price Index (CPI). The report indicated a 0.4% price increase compared to January or a 3.2% increase compared to February of the previous year. Notably, shelter, the most significant component of the CPI, and gasoline prices surged, contributing to over 60% of the overall increase.

However, the increase in food prices away from home, which spiked in January, moderated in February, rising by only 0.1%. Nevertheless, the slight uptick exceeded analysts' expectations, prompting market jitters following some dovish remarks by Jerome Powell last week.

At this juncture, one could analyze various sub-indices of the CPI to argue either that the Fed is on the brink of a significant error or that inflation is already yesterday's news. However, in my opinion, both perspectives can overlook the broader context. While it's true that the "super core" services CPI reflects an uncomfortable increase for the Fed, it's also true that the shelter component within the index lags behind market prices and is expected to decline in the months ahead.

Nonetheless, as I've emphasized in previous discussions, sustainable changes in the general price level are better assessed by examining past shifts in money supply and money demand. Both factors do not indicate a re-acceleration of inflation, as money supply growth has slowed and even turned negative, while money demand appears relatively stable.

There's an argument that money demand has recently declined (indicating rising velocity), but it seems this was more a consequence than a cause of rising inflation. Moreover, asset prices reaching all-time highs can also be interpreted as robust "monetary" demand, suggesting that a re-acceleration of inflation would require a substantial decline in asset prices.

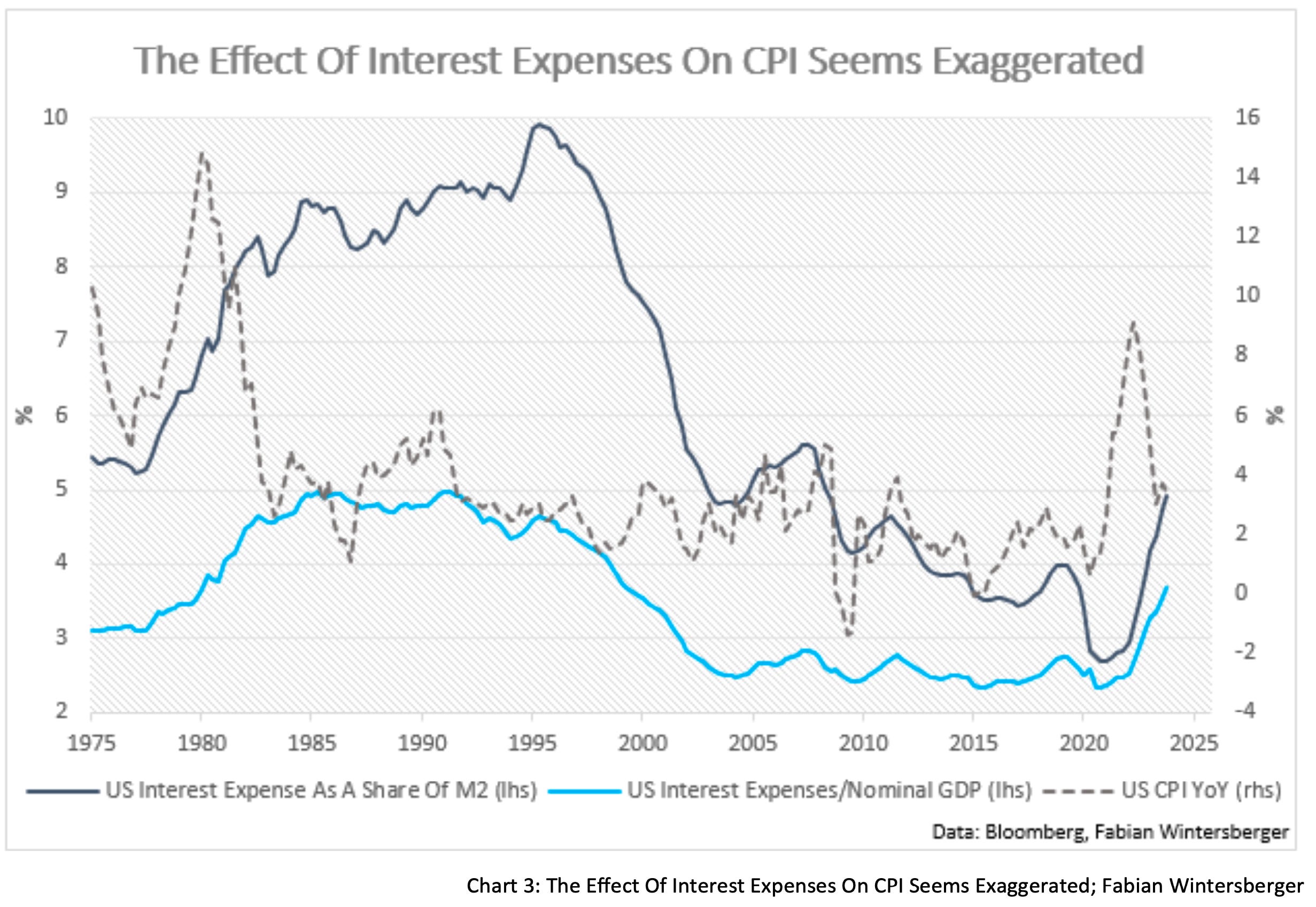

Let's pause here and consider another argument primarily espoused by MMT proponents, some analysts, and investors. They suggest that the sharp increase in interest payments by the US government is fueling inflation and perpetuating it as long as interest rates remain elevated.

According to this argument, individuals spend their interest income, and with higher interest rates, they have more income to spend, stimulating demand and sustaining growth and inflation. While this may hold true to some extent, the critical question remains: how significant is this effect?

Therefore, I examined the government interest rate expenses change relative to M2 and nominal GDP. The proportion of interest expenses relative to M2 demonstrates a stronger correlation with changes in consumer prices, suggesting that a one percent increase in interest expenses relative to M2 results in a 0.1322% increase in inflation.

Comparing this share to inflation reveals two key insights. Firstly, during the 1980s and 1990s, the share of interest expenses relative to M2 was much higher, yet the CPI remained at current or lower levels. Secondly, it appears that the rise in interest expenses results from an increase in CPI rather than the other way around, indicating that money supply plays a more significant role here.

Furthermore, another noteworthy aspect is the reallocation of funds if demand for government bonds increases due to higher interest rates for investors. Investors may need to sell other assets, such as stocks. The fact that the stock market is at record highs does not necessarily imply a preference for bonds over stocks. After all, selling stocks at a profit could be an equivalent of interest income, albeit a riskier approach.

This could imply two scenarios: either interest rates are still too low to persuade individuals to invest in government bonds, or most investors anticipate higher stock prices based on expected economic developments. Arguably, the Fed could raise interest rates to redirect funds from stocks into bonds. However, this could result in rapidly escalating government debt and a contraction of economic growth, particularly if the Fed believes that interest rates are already restrictive but transmission mechanisms are still active.

Considering this, the argument for a significant rise in interest rates from this point forward appears unconvincing. Presumably, the narrative of a growing economy continues to favor stocks over bonds, at least in the short term. Ultimately, a higher-for-longer scenario is contingent upon sustained economic prosperity.

Moreover, if market participants perceive interest rates have peaked, they are unlikely to sell the bonds they've acquired, reducing active supply. Should speculators persist in betting on lower bond prices, they could encounter headwinds. Therefore, as long as the economy signals relative strength, bonds may remain range-bound while stocks pursue new all-time highs.

I sense that the prevailing narrative of a "soft landing," or even a "no-landing," reinforces this scenario. The question arises: what transpires when the economy shows signs of weakening, considering that strength appears already priced in? In such a scenario, we might witness a shift from stocks to bonds and a significant short squeeze in the bond market, accompanied by a change in the narrative and possibly a new round of central bank easing akin to previous crises.

While one should never say never, a sustainable uptick in inflation and interest rates seems improbable here. The same holds for sustained economic strength, particularly one fueled by traditional Keynesian deficit spending. Should the prevailing market narratives shift, they could be impacted profoundly, akin to a hurricane.

It hit me like a hurricane, it hit me like a tidal wave

And I don't know why I drown my mind in everything they say

It hit me like a hurricane, it hit me like a tidal wave

And I don't know why I drown my mind, it got the best of meI Prevail – Hurricane

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. They do not constitute investment advice, and my perspective may change over time in response to evolving facts. It is strongly recommended to seek independent advice and conduct your own research before making investment decisions.