Hearts Burst Into Fire

Retail buys the dip, while the Trump policies could unleash an economic slowdown.

I used to think that if there was reincarnation, I wanted to come back as the President or the Pope...But now I would want to come back as the bond market. You can intimidate everybody. – James Carville, 1994

If one thing has dominated the news cycle of Trump II so far, it’s undoubtedly tariffs. While tariffs were a fixture of his first term, the intensity with which he and his administration are pushing them this time feels markedly sharper.

Back then, the game was simple: Trump would threaten tariffs one day, only to tweet the next that “tariff talks are going well.” Eventually, markets stopped taking him seriously, dismissing it as a brash negotiation ploy he’d never fully commit to.

This term feels different—or at least it seems that way. I’ll dive deeper into the mechanics of tariffs and argue why they’re a terrible idea for the well-being of those involved in trade, despite Trump’s apparent attempt at some 3D chess strategy. But for now, it’s worth a quick mention in this weekly piece.

A 25% tariff on Mexico and Canada, tariffs on the EU, tariffs on China—Trump isn’t messing around this time. He’s also slapped 25% duties on all steel and aluminum imports. This Wednesday, he announced that he will implement a 25% tariff on automobiles manufactured outside the US.

His goal? To bolster America’s hollowed-out manufacturing base. My take: These policies might offer some upside, but they come with costs—and those costs hit consumers who now face higher prices for cars and other goods.

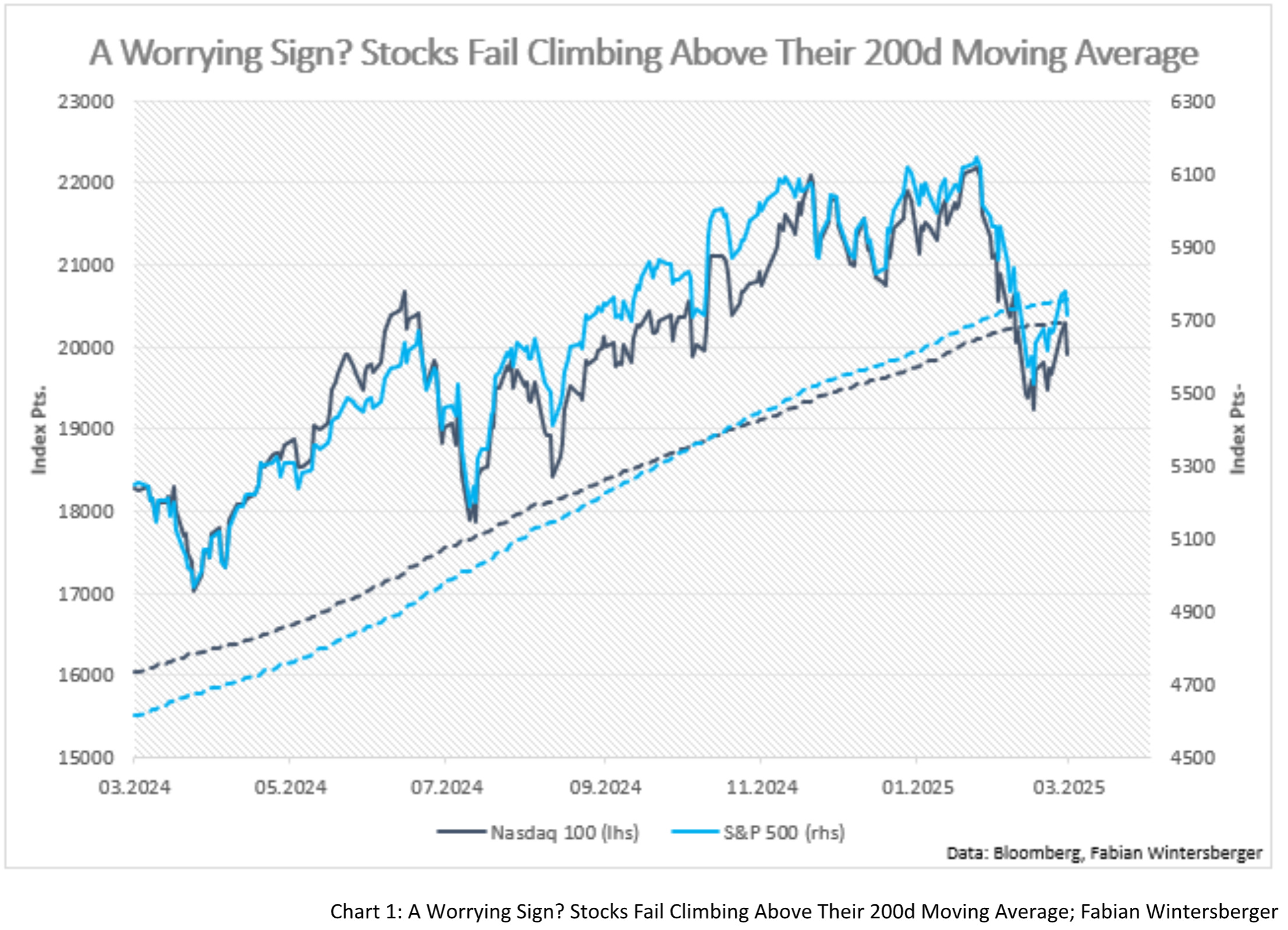

Stock markets jittered at the news, with the S&P 500 surrendering most of its weekly gains. It’s unclear whether the rebound from March 14 is already fizzling or if there’s enough cash on the sidelines to buy the dip. For now, February’s highs remain a distant memory.

I’m no die-hard chartist, but it’s worth noting that the Nasdaq 100 and S&P 500 failed to break above their closely watched 200-day moving averages—a signal some interpret as bearish. It might hint at more selling, though it’s far too early to call it.

Interest rates and bond markets stayed calmer this week. The US 10-year Treasury continues to trade in a tight range this March, while European government bonds have steadied after their recent slide. I still suspect European bonds could see a short-term upward correction. That said, as I noted last week, bond movements are heavily news-driven lately—any surprise from the EU or its member states or unexpected economic data could swing prices either way.

The euro’s rally has also stalled, with prices easing back after a sharp climb triggered by Europe’s big spending plans. Markets seem to overreact in every direction. Right now, sentiment has swung hard toward Europe over America, indicating how much times have shifted.

If we take these announcements at face value, the US is set to cut spending while Europe ramps it up—an anomaly this century, especially for Germany. Another shift: ECB hawk Robert Holzmann, Austria’s central bank governor, recently suggested the ECB might need to discuss supporting European defense spending down the line.

Asked whether he saw a role for the ECB to finance defence spending through bond purchases, Holzmann told an event in London: "we have not discussed it yet, we alluded to it."

Hardly a shock that the ECB might consider some form of QE to prop up member states, but hearing it from Holzmann, arguably the council’s fiercest hawk, raises eyebrows. His term ends soon, and he’ll be replaced by Martin Kocher, Austria’s current economic minister. Despite a stellar CV as a former academic economist, Kocher’s tenure has been underwhelming. Still, he’s likely less hawkish than Holzmann, so “QE for military spending” might find a fan in him.

With everyone bullish on Europe for now, the rally there might need a breather before it can push higher—or not. What’s certain is that expectations for European stocks have soared since the spending news hit.

Meanwhile, Trump’s spending-cut talk may be tempering US growth forecasts. Government spending has fueled profit margins in recent years; if Trump II pulls that lever away, margins could take a hit, at least in the short term.

Yet spending cuts could help lower US 10-year yields—a goal Treasury Secretary Bessent keeps hammering. His rhetoric has prompted banks to trim their year-end yield targets. The old “don’t fight the Fed” mantra has morphed into “don’t fight the Treasury.”

But one might raise an eyebrow and channel DOGE’s Elon Musk: “What have you actually done to make that happen?” So far, Bessent’s delivered little beyond words. Sure, the Treasury could limit new 10-year bond issuance to tighten supply and lift prices—ironic, given that’s what Bessent and Trump’s team slammed Janet Yellen for. And as I noted last week, DOGE’s spending cuts haven’t dented deficit spending. Still, the jawboning from Bessent & Co. has shifted expectations enough to spur bond buying and nudge yields down.

That can’t last forever. At some point, investors will demand real results to prove Trump’s team is serious about cuts. Noble as their aims may be, axing a few government jobs hasn’t delivered the hoped-for spending drop.

Look at equities, bonds, and the dollar: they’ve shed post-election euphoria and settled back to pre-vote levels. Growth expectations, sky-high after November, have similarly cooled.

The question is whether to take these policy signals seriously. If so, the downgrading of economic outlooks isn’t done—it’ll keep sliding. Immigration curbs, tariffs, and spending cuts all drag on growth, at least in the short term. If fully enacted, they could usher in far more weakness.

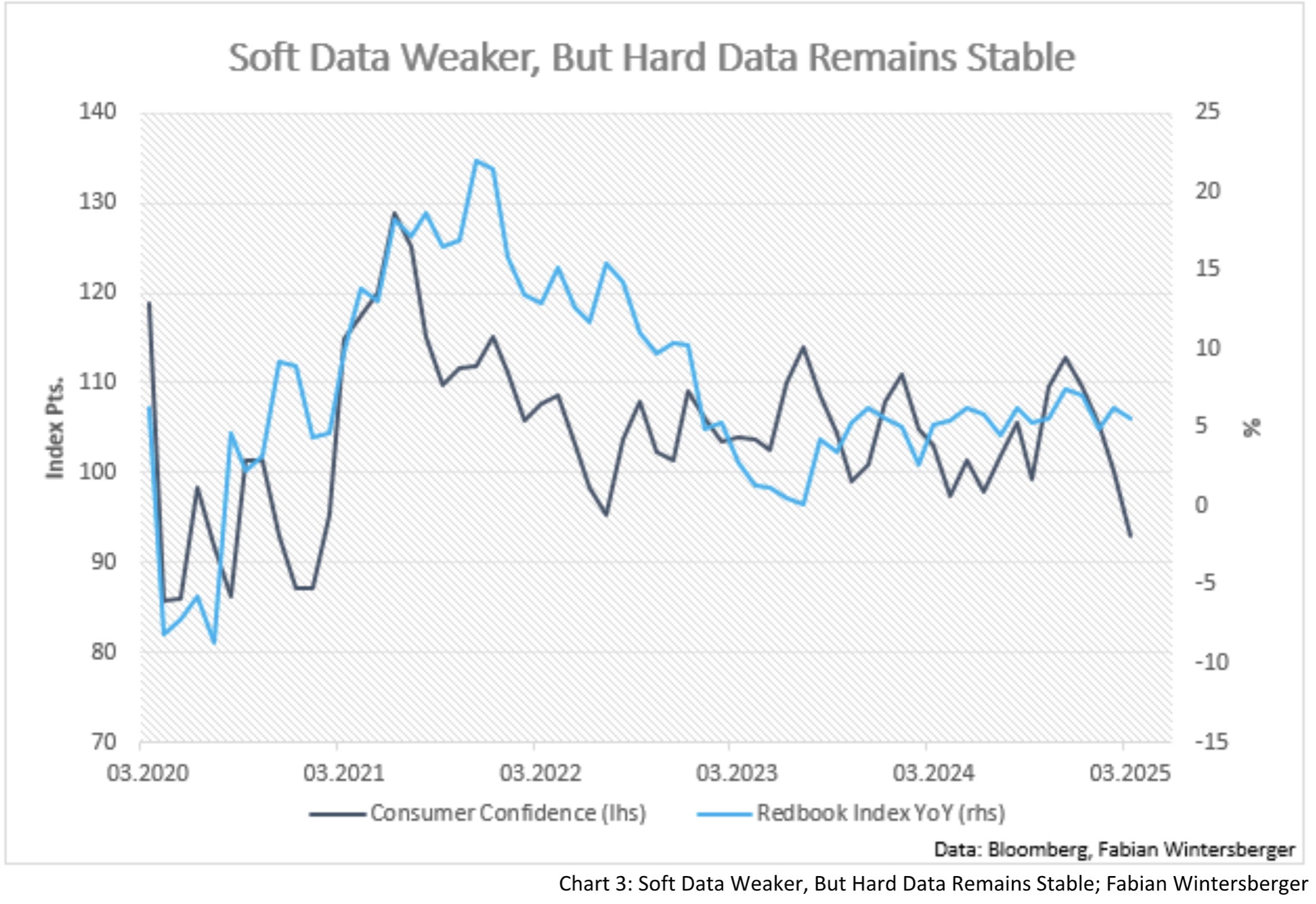

Still, there’s a flicker of hope for bulls: hard data hasn’t yet followed the softening in soft data. This week’s retail sales figures suggest the economy’s holding up decently, backed by strength in the Redbook Index. However, consumer confidence has tanked in recent months, reflecting rising uncertainty around Trump’s policies.

That said, JP Morgan's credit card spending data shows a slowdown, hinting that real retail sales might’ve turned negative. As the US’s biggest card issuer, that bolsters the bear case.

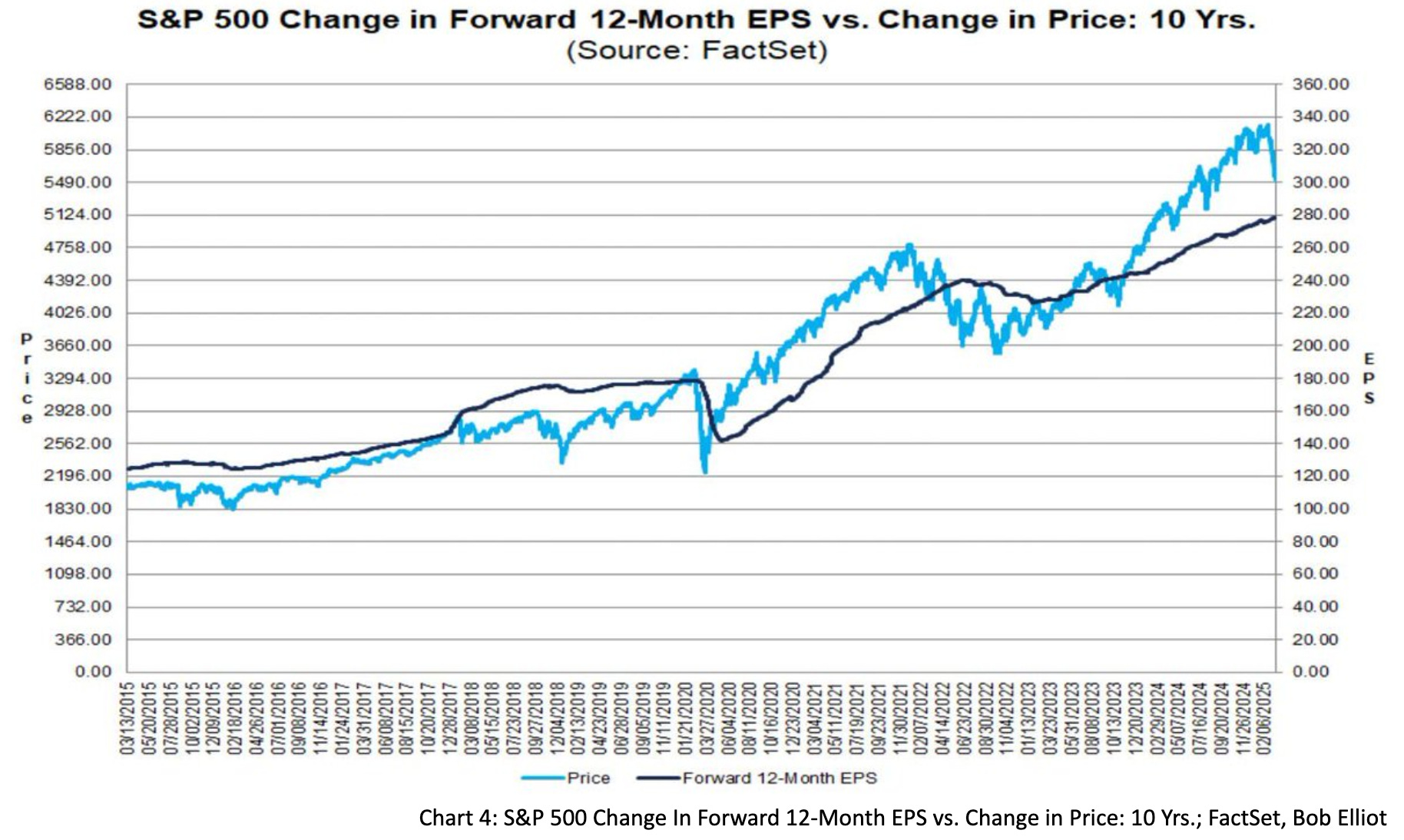

Time will tell, but hard data could eventually buckle if Trump II sticks to this path. If so, current EPS expectations a year out—still lofty despite the S&P’s drop—might prove too optimistic, spelling more pain for stocks.

On the flip side, this gloom could just be temporary uncertainty. After two years of expecting weakness only to be surprised by resilience, I’m not ready to call it a done deal. Still, I suspect this time might be different, with softening ahead.

So, what does this mean for assets? Gold and copper’s recent strength could fade if reports on both prove contrarian signals. Without new highs, a pullback looms.

Stocks-wise, retail investors are dip-buying—a strategy that’s paid off the past two years, with 7-10% drawdowns yielding gains. However, institutional buying is missing in action, and CEO confidence is scraping low.

If stocks keep stumbling, bonds could catch a tailwind. I’m sticking with my view that an upward move is likely. Beyond inflation—which I don’t see roaring back this year—the data favors bonds. The path might wobble, but I lean lower.

European bonds are murkier, but their recent stabilization—and my hunch that US weakness won’t instantly offset Europe’s euphoria—points to a near-term uptick unless Europe doubles down on spending again.

If US softening persists, stocks will slide further, and retail dip-buyers might face a new reality—unlike the past two years when they were rewarded. Then, plenty of “hearts [might] burst into fire.”

It hurts, wounds so sore, now, I'm torn, now, I′m torn,

I've been far away

When I see your face, my hearts burst into fire

Hearts burst into fireBullet For My Valentine — Hearts Burst Into Fire

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you shared it on social media or gave the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. They do not constitute investment advice, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.