Echoes

Those who cannot remember the past are condemned to repeat it.— George Santayana

As this week’s macro commentary is written on June 2, I’ll keep it rather short. Not because nothing has happened since Friday, but because a lot can still happen until publication day. The news cycle surrounding the Iran war was extraordinary once again. Until Monday, the dominant narrative was that a deal was within reach.

Then, almost suddenly, Iran announced it would stop all negotiations due to Israel’s bombardment of Lebanon. Markets immediately reacted nervously: oil spiked higher, while bonds and equities came under pressure.

At the time, I noted:

As grim as it looks, being an optimist has boded much better than being a pessimist in recent months.

And, indeed, just hours later, reports emerged that Trump had held a phone call with Netanyahu, allegedly urging him to stop the bombardment of Lebanon.

No matter how events unfold from here, one thing has become increasingly obvious: every bout of bad news is likely to trigger an attempt by the Trump administration to jawbone markets higher again through optimistic headlines and promises of imminent progress.

But that will be a topic for next week.

An ECB Rate Hike Risks Echoing Jean-Claude Trichet

Every reader of this macro-note knows that I remain skeptical about the growing market conviction that the ECB will raise rates at its next meeting. What surprises me even more is that the Fed appears far more reluctant to tighten further, although my interpretation of the data suggests the opposite should be true.

The inflation problem in Europe is not primarily demand-driven, but supply-driven. Europe remains structurally exposed to energy markets, geopolitical fragmentation, and weakening industrial competitiveness. While Trump’s latest jawboning temporarily eased pressure in commodity markets and oil prices declined month-over-month, the underlying vulnerabilities remain unresolved. Any renewed escalation in geopolitical tensions can quickly reignite price pressures.

But this is not classical monetary inflation in the strict sense. Eurozone M3 grew only 2.7% year-over-year in April, while money demand has likely remained relatively stable. What Europe is experiencing is largely a supply shock expressed through prices, not an overheating credit boom caused by excessive money supply growth.

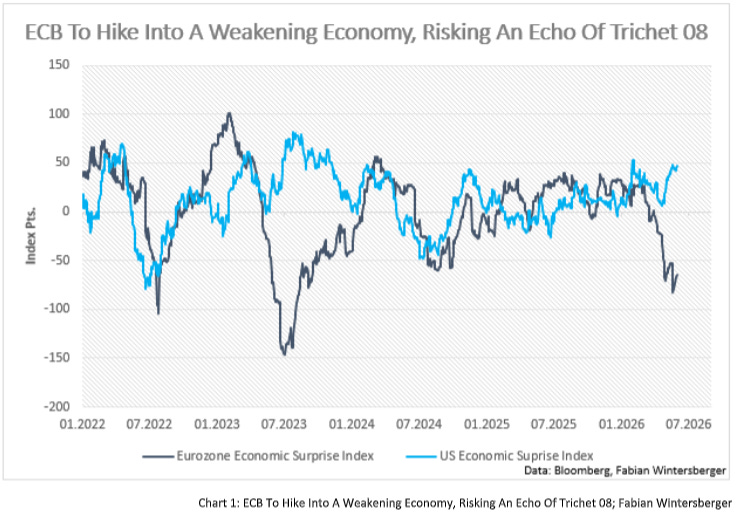

The divergence in Economic Surprise Indices between the United States and the Eurozone tells the story. Since the beginning of the war, the paths have separated sharply as Europe became increasingly exposed to energy-related headwinds and deteriorating industrial conditions.

A tightening of financial conditions will not solve these problems. Higher rates cannot produce more energy, repair supply chains, or improve Europe’s structural competitiveness. Instead, they risk placing additional pressure on businesses and households that are already operating in an increasingly fragile environment. Credit-sensitive sectors would weaken further, lending conditions would tighten, and growth expectations would deteriorate.

I continue to think that an ECB rate hike would likely flatten the yield curve further and push the European economy toward stagnation, ultimately forcing the ECB into aggressive rate cuts later on.

US Money Supply Is Rising: Will the Financialization Effect Drive Money Demand Down?

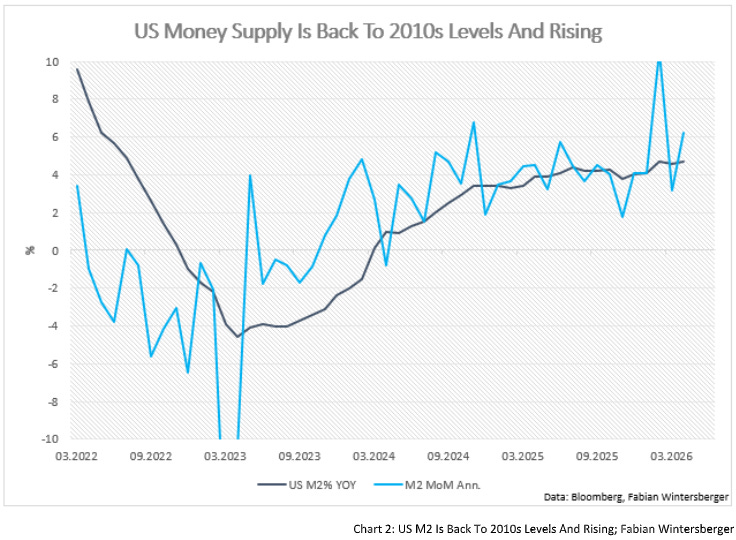

Money supply growth in the United States is accelerating again. US M2 rose at an annualized pace of more than 6% in April, while the year-over-year growth rate climbed back to 4.7%, roughly in line with levels seen during the 2010s.

Within a rigid monetarist framework, one could argue that such growth rates do not necessarily point toward another major inflation wave. But I think there is an important caveat.

Money supply remains highly important when discussing inflation in the classical sense. However, modern inflation discussions revolve around changes in the price level, and prices are influenced by far more than just the quantity of money. They are shaped by the relationship between money and goods, by changes in subjective valuations, and by shifts in money demand itself.

Today’s environment is unusual because prices are rising largely due to supply-side rigidities and structural constraints. Labor supply growth remains weak, labor markets remain relatively inflexible, and businesses are finding it increasingly difficult to reduce costs. As long as demand remains stable, firms will continue attempting to pass higher costs onto consumers.

And demand has remained remarkably resilient.

One important reason is the massive increase in paper wealth generated by rising financial asset prices. Higher equity prices and stronger household balance sheets support spending directly through wealth effects, but also indirectly through easier borrowing conditions and expanding collateral values. Financialization itself increasingly sustains consumption demand.

At the same time, consumers who experienced large price increases over recent years may become increasingly willing to exchange money for goods, services, or financial assets sooner rather than later. In other words, money demand may be declining while velocity rises. Under such conditions, prices can accelerate even if money supply growth itself appears relatively moderate.

Combined with inflation itself loosening financial conditions through rising nominal incomes, asset prices, and collateral values, I continue to believe the US economy risks running into a second inflation wave.

A Falling Savings Rate Is Not A Sign Of Falling Economic Confidence

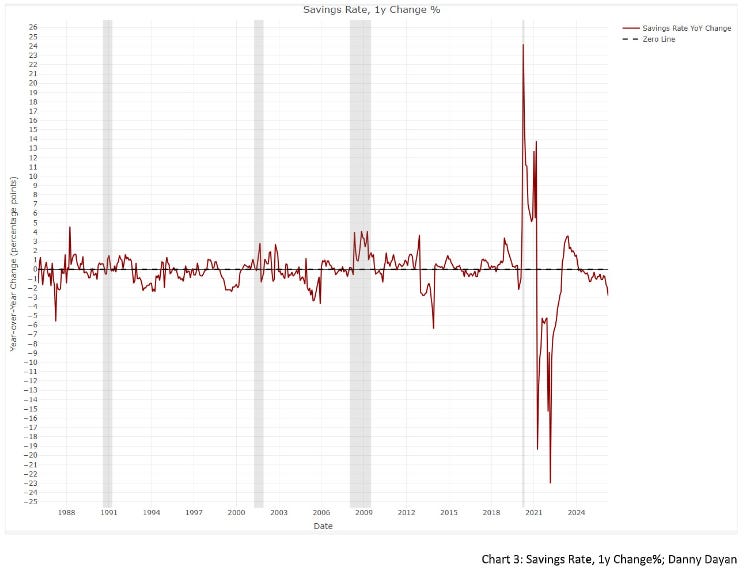

That brings me to another data point that has received significant attention recently: the falling US savings rate. Many observers interpret this as evidence that consumers are running out of money and that economic growth is approaching its limits.

Trader Danny Dayan recently flipped the argument around: what if a falling savings rate actually reflects improving economic confidence? His chart (Chart 3) shows that savings rates tend to rise during economic contractions, not before them.

From an Austrian perspective, this interpretation makes sense. A rising savings rate means that people increase their valuation of money relative to goods and services. Instead of exchanging money for consumption, they prefer holding onto liquidity for future use.

A falling savings rate implies the opposite. Consumers reduce their relative preference for money and increase current spending. Money changes hands more quickly, velocity rises, and money demand weakens.

One can therefore argue that falling savings rates occur either during periods of rising confidence or during phases of loosening financial conditions where borrowing becomes easier and consumers prefer satisfying present wants rather than postponing consumption into the future.

In that sense, a falling savings rate may not signal collapsing demand, but rather declining money demand: a dynamic that suggests inflationary pressures in the United States may prove far more persistent than many currently expect.

Market Assessment

My market assessment from last week remains largely unchanged. Bond prices still suggest that another move higher is possible. However, equities continue to look more compelling relative to bonds.

Gold and Bitcoin continue to appear relatively weak, while the US dollar still looks favorable relative to the euro.

Conclusion

The monetary divergence between the Eurozone and the United States continues to widen. While the ECB appears increasingly willing to tighten policy into a weakening economic environment, the Federal Reserve remains hesitant to respond aggressively to inflation risks that may increasingly be driven by declining money demand and rising velocity.

Meanwhile, the geopolitical situation surrounding Iran remains extraordinarily uncertain. Markets clearly continue to expect some form of eventual deal, but every negative headline now appears to trigger an immediate political attempt to stabilize expectations again through optimistic rhetoric and market jawboning.

In that sense, all major policymakers seem to be hearing “Echoes.”

The Trump administration hears echoes from recent weeks.

The ECB hears echoes from 2008.

And the Fed may once again be hearing echoes from 2021.

Hearing echoes, hearing echoes calling

(Echoes calling, call-calling me)

This is haunting, how it’s crushing me

(How it’s crushing me) it’s crushing meAs I Lay Dying - Echoes

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.