Disposable Heroes

The Inflationary Consequences of a Fragmenting Global Order

Government planning not only fails; it tends to produce outcomes that are the opposite of what its proponents say that they favor.— Thomas Sowell

This week, markets are once again caught between signal and noise, between the broader trend and the headlines that constantly attempt to obscure it. After a drop in stocks and bonds in recent days, Trump decided that it’s time to go back to jawboning the market.

On Wednesday, Trump touted the rumor that the US is in the final stages with Iran while also threatening Iran with another “big hit” if the deal falls short. Markets, as usual, focused on the good side of the story and neglected the bad, and a rally in stocks and bonds followed.

The takeaway for investors here is that one should at least become cautious if yields rise to a certain threshold and stocks are sold off, because, as we know, Trump is concerned about the stock market. It’s a major talking point for him to underscore how exceptionally well he is governing. As long as that works, he’ll use that method to influence the price action.

Indeed, a deal would be more than a sigh of relief for markets. The question is whether it can be achieved, because neither party involved, Iran and the US, is really interested in making concessions to the other. The checkmate goes like this: Trump cannot close a deal that is similar or worse than the JCPOA that Obama negotiated, and Iran thinks that it can answer any continuation of the bombing with attacks on the GCC and the destruction of more global oil infrastructure, which is definitely something Trump fears because it diminishes Republican chances at the midterm elections.

However, while the US definitely ran into problems on the surface, the broader geopolitical strategy seems to run in its favor, at least for those who draw up the plan on the whiteboard and formulate it in the National Security Strategy.

Back To The US(S)R

Rabobank (Michael Every & Joe DeLaura) published an interesting report arguing that the Iran War may not simply be another geopolitical conflict, but a possible precursor to a fragmentation of global energy markets into competing geopolitical blocs.

Their core argument is that energy markets are increasingly ceasing to function as a neutral global market governed purely by price. Instead, energy flows may increasingly depend on military protection, payment systems, swap lines, and political alignment.

In this framework, the UAE’s recent exit from OPEC is interpreted not as an isolated economic decision, but as part of a broader realignment toward a US-centered “energy stack” built around security guarantees, USD settlement, and financial backstops. The report essentially argues that we may be moving from OPEC toward “NOPEC,” a world of fragmented, politically managed energy systems rather than one unified global market.

The most interesting aspect of the report is not necessarily the specific geopolitical predictions, but the broader structural framework behind them. Every argues that energy, finance, and military power are increasingly merging into one strategic architecture. The US “stack” would consist of naval protection of shipping lanes, USD-based settlement systems, and swap lines, while China is attempting to build a parallel structure around refining capacity, CNY settlement, CIPS, and its strategic partnership with Russia.

Europe, meanwhile, appears structurally weak within this framework due to its dependence on imported energy, lack of hard power projection, and limited role of the euro in global commodity finance. Whether or not the report’s more extreme scenarios materialize, the broader direction toward geopolitical fragmentation, strategic supply chains, and politically managed trade flows already appears well underway.

Every’s work is useful because it attempts to place current market action into a broader long-term structural shift rather than viewing each headline in isolation. In times of war, “free markets,” as Every likes to frame it, become rather disturbing for policymakers, prompting them to increase their active involvement in the economy. Clearly, especially if one connects the dots as the Rabobank paper does, it is not at all far-fetched to think that the Iran war is part of a broader strategy.

The more damning question investors should ask themselves is: What are the implications for markets? I tend to think that the short- to mid-term implications do not really depend on whether the strategy is ultimately fruitful. If the strategy does not work out, policymakers will take more action and try harder to rig the economy in their favor, creating even more distortions and problems. That is what I call the “Intervention Trap“ framework, and the final result of such action will culminate in the decline of global powers and the rise of new ones.

However, these processes take time. Not years, but decades. And thus, the takeaways are clearly that we are in the midst of an attempt to “reshore” parts of global production back onto American soil and toward allied economies with the necessary resources, which receive favorable terms in return, such as military backing, financial support, and privileged access to the dollar system, exactly as described in the Rabobank paper.

No Signs Of Demand Destruction

Many observers are focusing on a deflationary crisis, with demand collapsing, production faltering, and the Fed responding with looser monetary policy to address it. Understandably, as a “this time it’s different” approach usually does not bode well for investors.

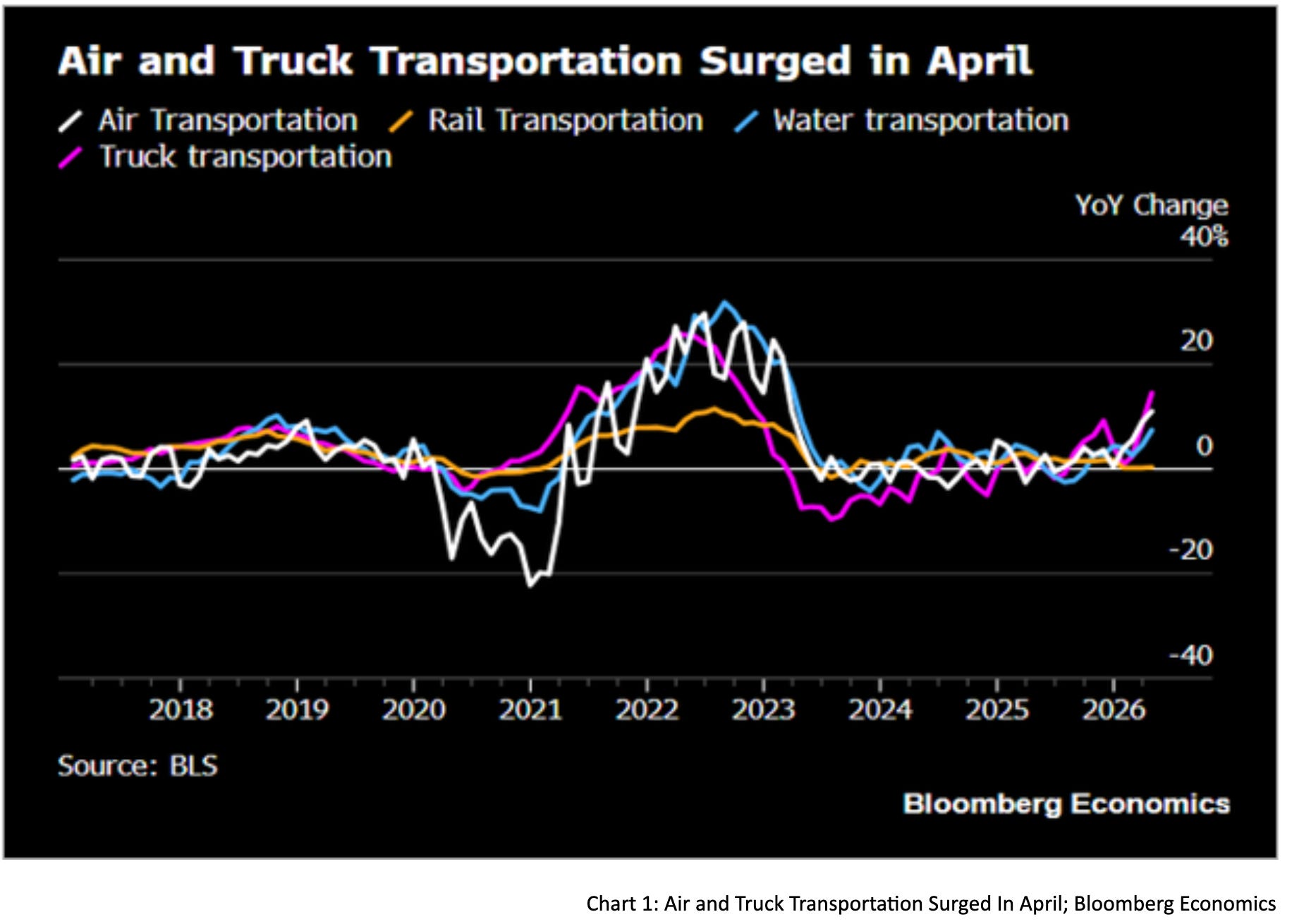

But if one looks for signs of a deflationary downturn in the US economy, disappointment follows quickly. Transportation numbers accelerated in April, which I interpret as a sign of strong consumer demand.

Recently, I also discussed US bank credit growth and its impact on money supply. These numbers can also be interpreted as a sign of strong demand, as more money in people's hands means more money available to buy goods, services, or financial assets. If one connects this to Brent crude still hovering around $100 to $120 per barrel, I would argue that demand destruction is simply not happening at the moment.

Industrial production in the US also picked up in April. Instead of an expected 0.3% monthly increase, we got 0.7%. Earnings season, so far, has been nothing short of remarkable for US businesses.

Trader Danny Dayan made another point on X:

Food services and drink category of retail sales is the most discretionary services one we have. Going out for dinner is the first thing you cut if you want to crimp spending...The monthly run rate remains exceptionally strong.

And finally, a look at consumer confidence numbers for planned vacations outside the US, another useful proxy for discretionary spending, shows a rebound to 20% in April, more than twice the level during the 2000 to 2020 period.

The bottom line is that there are plenty of signs that do not point to demand destruction in the US. They point toward an economy that is still running hot.

Which brings me back to the question: “Is it different this time?”

I think it is, or at least for now. The broader geopolitical transition that Every describes, combined with the current state of the US economy, Europe's struggles, and the rise in global interest rates, fits remarkably well within such a framework.

The Inflationary Side of The Empire

In the global financial system, with the dollar at the top of the monetary pyramid, the currency can be weaponized much more easily than under the gold standard, because the US controls the production elasticity of the ultimate trade-settlement asset.

The US strategy effectively comes down to: “let the rivals suffer more.” The goal is to shift relative competitiveness back in the United States’ favor and to reward its geopolitical allies.

That is exactly where the swap lines with the UAE come in. They guarantee that in times of stress, dollar collateral remains available and dampen the economic impact of a crisis because economic actors inside the system can still access dollars at relatively stable rates. Outside that framework, however, the settlement asset must be acquired on the open market amid intense competition.

In periods of financial stress, everyone suddenly bids for the same collateral at the same time. The result is a sharp rise in dollar funding costs for those outside the system, while those inside the network remain comparatively insulated.

The thesis is that the US is not facing a deflationary crisis as in 2000, 2008, or 2020. The buildup we are witnessing increasingly points toward the opposite: an inflationary runaway.

To lay it out, we have to connect the prior two sections and translate them into economic consequences. In the background, there are US tax cuts that have lowered the burden on businesses, geopolitical tensions around energy chokepoints, and the establishment of dollar swap lines. One is a domestic policy aimed at improving relative competitiveness, while the others involve securing cheap energy and greater control over its global flow.

If policymakers want to bring production back to the United States and revive the industrial sector, the financial takeaway is that the US aims to collect “offshore dollars,” or “eurodollars,” meaning dollars circulating outside the US, and pull them back into its domestic economic sphere.

The process is somewhat analogous to the Spanish gold inflows from South America during the 16th and 17th centuries. The crucial difference is that the US does not rely on finite gold inflows. It controls the elasticity of the global reserve asset itself. An inflow of dollars into the US for economic production, driven by changes in relative competitiveness, regulation, and lower taxes, will contribute to a dollar shortage outside the United States.

Swap lines are key here: central banks with access can swap their own currencies, effectively derivatives of the dollar system, for dollars at predetermined interest rates. Foreign capital then flows into the US, finances production, wages, and investment, and, in the process, creates inflationary pressure within the US while contributing to dollar shortages abroad.

Access to those swap lines, therefore, becomes a geopolitical privilege. Allies, or vassals, regain access to dollar liquidity in exchange for integrating themselves more deeply into the US-centered production and trade system, while countries outside the framework gradually lose competitiveness and global market share due to structurally tighter dollar liquidity and higher funding costs. If one extends this logic further, it increasingly resembles an attempt to rebalance the global balance of payments system itself.

That increases dependency on the US for its allies. For example, the European economy risks being hollowed out from both sides: losing high-paying industrial jobs while simultaneously needing to borrow dollars to satisfy domestic energy demand. These economies would increasingly rely on rising debt, low inflation in domestically produced goods, and high inflation in imports. The US, meanwhile, earns dollars by selling energy or by guaranteeing the financial infrastructure required to acquire it, buys input goods to complete production domestically, and then sells finished goods both domestically and internationally.

I would not go so far as to say this will fully play out in such a linear fashion, but it lays the groundwork for the economic forces likely to shape the coming months and years. An attempt to restructure the global economy in this way would likely prove highly inflationary, both in the US and abroad, because of increasing pressure on offshore dollar markets. It would imply that the dollar no longer carries the same scarcity or funding costs inside and outside the United States. Such a bifurcation would likely push global inflation structurally higher, especially in the US.

Market Assessment

Although Trump once again successfully jawboned the market higher, my short-term view remains relatively unchanged. I continue to see further upside in equities, while bonds remain under pressure and increasingly fail to serve as an effective hedge against stock declines.

I continue to believe that oil will hover around current levels and serve as a better hedge than bonds. If buying equities is effectively a bet on stronger nominal growth, then buying oil may also be a more attractive hedge than shorting bonds, although I think that point remains debatable.

Gold continues to struggle in the current environment, and perhaps the consolidation is necessary after the strong rally during the second half of 2025. If we do run into an inflationary runaway, gold should eventually serve as a complementary asset to offshore dollar strength, meaning a lack of dollars abroad and an excess of domestic currency, which would likely attract demand. Long-term prospects for gold, therefore, remain intact in my opinion.

Bitcoin should also benefit in that environment over the long term, although, unlike gold, the short-term trend still appears favorable as well. The question is whether the consolidation around $80,000 has already resolved to the upside. If it breaks lower again, the mid $50,000 area could become a target.

Conclusion

With the Iran war still unresolved, the short-term question remains whether the conflict will be contained quickly or whether another escalation follows. A resolution would likely support both stocks and bonds, while further escalation would put additional pressure on them.

However, the pressure on bonds also stems from the broader geopolitical power shift and the rise of economic interventionism. At the moment, I would not place too much emphasis on another deflationary crisis down the road. Despite repeated warnings from many bears, equities continue to perform relatively well.

High nominal rates are also less restrictive as long as real rates remain near current levels, which, as I have repeatedly argued, are not truly restrictive. Inflation benefits debtors, so heavily indebted entities benefit the most. In 2022, it was US household deleveraging. The next phase may be an attempt to force US government deleveraging by bringing down the debt-to-GDP ratio through inflation.

The problem is that there is a tipping point where inflation becomes such a burden on the broader public that the political backlash against the “grand global strategy” begins to backfire electorally. Governments are not monolithic structures. They consist of competing factions fighting for influence and power. Voters reacting against the economic consequences of these policies may ultimately reshape the political structure itself.

Government plans often end badly because the people implementing them tend to overestimate their abilities and face few direct consequences for failure, since taxpayer money is at stake rather than their own capital.

I once read that after World War II, Paul Samuelson forecasted that the USSR would become the dominant global industrial superpower. Ironically, something similar increasingly appears to be the ambition of modern US policymakers as well. But if history rhymes, the current “heroes” attempting to bring production back to America could ultimately become the nation’s true disposable heroes, ending the American empire not by intention, but by consequence.

You will do what I say, when I say, back to the front

You will die when I say, you must die, back to the front

You coward, you servant, you blind man.Metallica- Disposable Heroes

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.