Destroy Everything

How energy, logistics, and the dollar system are reshaping global power

Every intervention in the market sets in motion forces that lead to further interventions.— Ludwig von Mises

We’re close to entering the fourth week of the Iran war, and the market is still dominated by headlines of President Trump, the US administration, and to a lower extent, the response from the Iranians.

Still, the way Trump is able to jawbone the market doesn’t stop to amaze me because despite everyone knowing his relationship with the truth is somewhat “special,” every claim about a soon end of the war or a peace agreement in reach pushes oil down, stocks and bonds up.

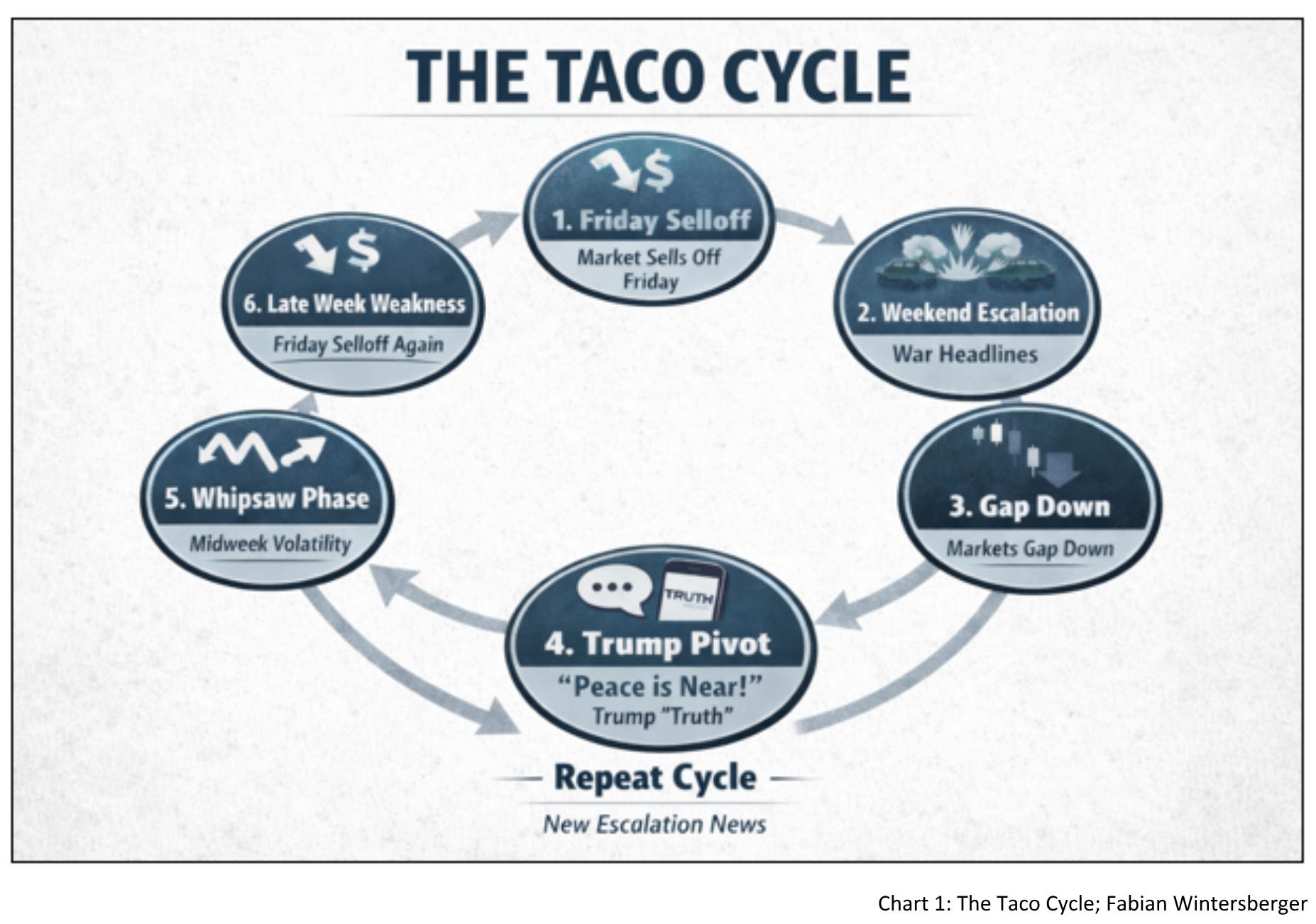

We can witness attempts to calm down the markets in real time, and with the headline driven, desperate attempts to find a sustainable market equilibrium, the price action remains influenced by the “TACO cycle”.

As the situation remains diffuse and the war could flip to a higher or lower level of escalation at any moment, the best approach in that regard is probably to stay largely sidelined and ready to deploy capital once the direction is clear. Therefore, this week’s note will again be a rather short one, with a short review of the ECB decision and the market reaction that signals a tightening regime before I continue to emphasize on the bigger picture of increasing signs that the US plan might indeed be partially grounded in a bigger geopolitical strategy and what Michael Every calls “Reverse Peristroika.”

ECB & The European Tightening

The ECB left rates unchanged at 2% for the sixth meeting, but the message was clearly not dovish. Lagarde emphasized that the central bank is “well positioned” to deal with the Iran war shock, even as it raises the risk of higher inflation and weaker growth — a stagflationary tilt. Updated projections already point to stronger inflation (especially into 2026) and softer activity, with risks skewed to the upside for prices and to the downside for growth, particularly if energy disruptions persist.

Interestingly, Lagarde did not push back against market pricing of further tightening, effectively validating a more hawkish reaction function. In that sense, this was a pause, but not a dovish one. On the surface, one could argue this increasingly points toward a tightening regime.

However, I’d be cautious about that, because anyone comparing this to the impact of the Russia/Ukraine war in 2022 misses one important difference. Back then, the war started after a period in which the ECB had sharply expanded the money supply to fight a crisis, and that liquidity was still working its way through the system when the energy shock hit. Therefore, it was the combination of prior monetary expansion and the supply shock that pushed consumer prices higher.

Today, the ECB has stopped loosening and short-term interest rates have remained steady, while European governments are planning to support the economy through higher fiscal spending. The fall in real yields since the beginning of the year already reflects a weaker growth impulse being priced into markets, assuming that this spending will not sustainably lift growth.

With the Iran war, inflation expectations initially moved higher, but partially retraced on hopes of a “TACO,” while real yields remained elevated. In my view, that signals tightening ahead of a growth downturn, especially if energy market stress intensifies. The Strait of Hormuz has effectively been closed for three weeks now, and the full effects have yet to work their way through the economy. Once this feeds into weaker growth, the obvious conclusion would be that real rates are too tight for the economic environment, acting as an additional headwind.

Combined with higher fiscal spending, which risks crowding out private investment rather than adding to it due to higher borrowing costs in real terms, I’m not so sure the ECB will look through that. Instead, frightened by the data, it may reverse course to support economic activity.

That is still highly speculative, and not an immediate action plan. But it is something to keep in mind when anticipating the future trajectory of markets. As we are all aware, central banks can become extremely creative — and may well come up with a framework that justifies such a shift even in the face of rising consumer price inflation. Raising the inflation target in times of war does not seem entirely out of the question.

Overall, Europe remains caught between a rock and a hard place, with the US as its primary supplier of liquefied natural gas, deepening its structural dependency. As no meaningful reversal of course appears to be on the table, Europe increasingly looks like a geopolitical plaything rather than an independent actor.

Planning the Global Economy

With Europe remaining in the lane of irrelevance, the global economic playing field is currently being reordered by three players: China, Russia, and the US, with the US still at the top of the food chain. Under that lens, the current geopolitical turmoil created by Trump’s erratic behavior may not be entirely random, but could, at least in part, follow a strategic logic.

I was more dismissive of such a plan, mainly because the economic theory behind it is vastly incorrect and, at first glance, nonsensical. It was hard for me to grasp why a superpower would follow a strategy grounded in the assumption that the rise of China’s economic strength has something to do with subsidies and centrally planned state financing, combined with initiatives like the “Silk Road Initiative” as a method to influence logistics corridors and shape China-centered trade routes.

However, once one separates economic logic from strategic intent, the picture changes. The logic behind it is not primarily economic — in the sense of sustainable growth — but one of global economic influence and power.

A country that has influence over logistical points, controls the supply of essential resources, and is willing to pursue economic policy at the expense of its population for the “greater good” seeks to extend its influence beyond traditional economic constraints. The Soviet Union showed that the buildup of such economic imbalances can take decades before their full impact unfolds.

Against that backdrop, one Washington Post article caught my attention. The article itself discusses the failure of the Trump administration to achieve its stated goals in the war, but in between, there was an interesting paragraph:

Instead, breaking Iran’s stranglehold on the strait could enable Trump to wind down the war while claiming victory, halt an expanding global energy crisis and deprive Iran of a potent deterrent against future strikes — which senior Israeli officials described as inevitable if Tehran resumes ballistic missile production or moves to develop a nuclear weapon.

Breaking Iran’s stranglehold on the Strait of Hormuz would imply direct US influence over one of the world's most important chokepoints for global trade. While I would not go so far as to argue that this was the grand plan all along, it is plausible that such considerations played a role within parts of the US strategic apparatus. As US General John J. Pershing once said, “Infantry wins battles, logistics wins wars.” If we are in a global trade conflict, it may ultimately be decided by logistics — and thus by control over critical supply routes.

From an Austrian economics perspective, this initially sounds highly questionable. But if one considers the theory of the “interventionary spiral,” it becomes more understandable. Governments tend to solve self-inflicted problems with further intervention, rather than unwinding previous mistakes.

Everyone knows that Trump’s stated goal is to bring production back to the United States. And while one could point to a wide range of economic and monetary policy factors that reduced US competitiveness and incentivized the transformation into a more financialized economy — and why a structural rethink of these policies might be the more sustainable path — the current approach suggests that the administration has instead chosen to move further down the interventionary path.

If you don’t move back to sound economic policy — perhaps because the unwind of existing imbalances is seen as too painful — you may attempt to enforce that adjustment through geopolitical means. You want to change the relative cost of production not by improving your own cost structure (laws, regulation, etc.), but by making production more expensive for everyone else.

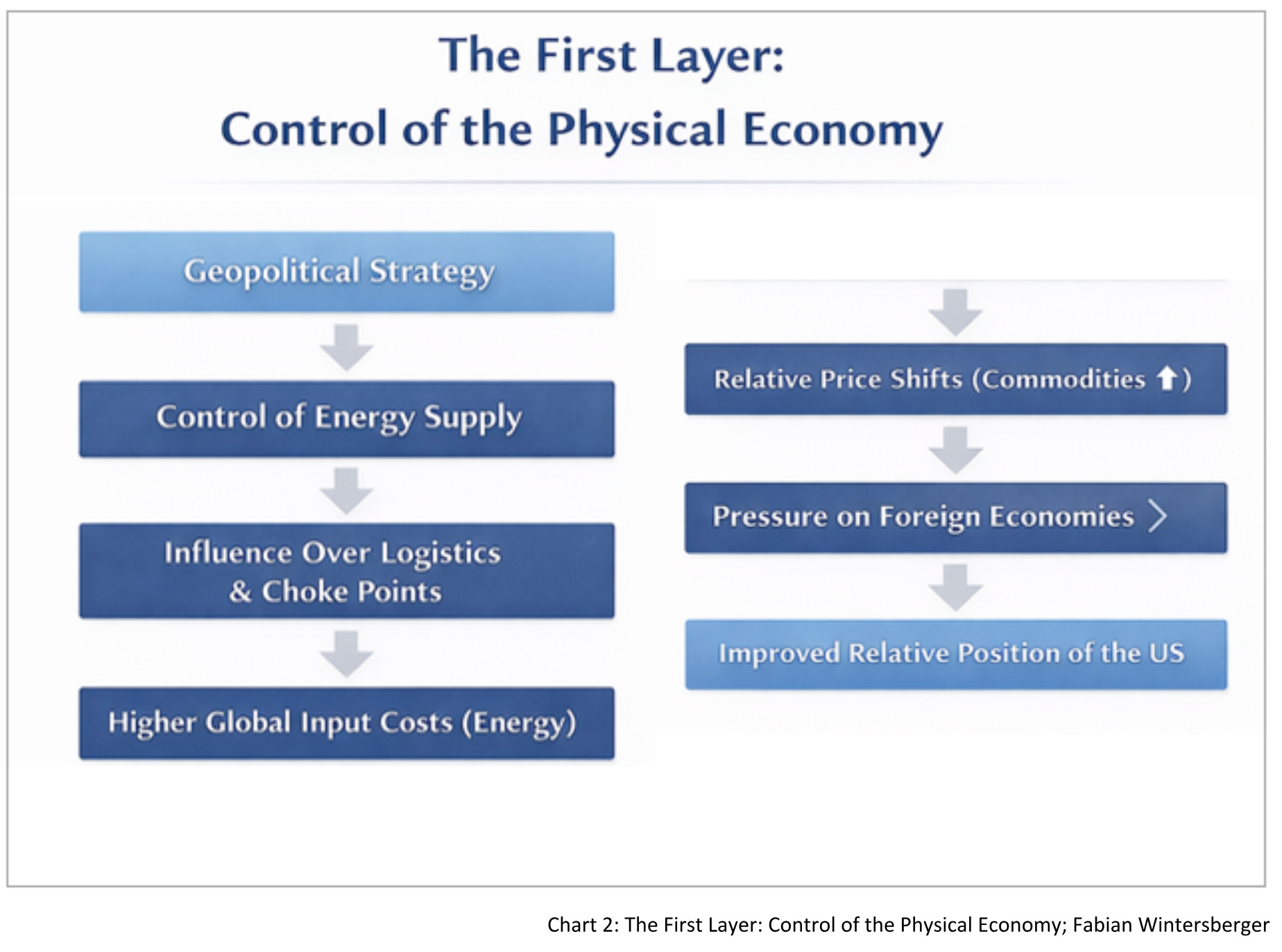

Given the US pursues such a strategy, the main leverage is that it is a global net energy exporter and the largest producer of energy. Economic policy could then be seen as a vehicle to ensure relatively lower increases in energy prices in the US, while using military power to influence and control global energy supply and, in turn, increase energy costs for competing powers. If there is such a strategy, this would be the first layer of the pillar.

Dollar Dominance 2.0

Yet, such a strategy would have significant implications for the US dollar and therefore requires a second layer that addresses the financial side of it.

So far, the strategy would point toward upward pressure on commodities, driven by supply constraints and geopolitical risk, while at the same time creating a more fragile environment for the financial system, financial markets, and fixed-income assets. It would likely lead to short-term consumer price inflation, driven primarily by relative price changes and reinforced by rising inflation expectations rather than monetary policy (assuming the policy stance remains the same), which — similar to the ECB — could put the Fed under pressure to react, especially as long as Kevin Warsh is not appointed.

On the other hand, injecting liquidity into a “neo-mercantilistic-style” economy would be highly inflationary while simultaneously reducing the real burden of global dollar-denominated debt held by foreigners. The result could be a further increase in US domestic assets held abroad, as global trade might be increasingly controlled by the US, while parts of the financial benefits are still reaped elsewhere.

Hence, if one lays out such a strategy, one must also address the financial architecture. Because this creates a fundamental tension: while the US would aim to improve its relative production costs, it would risk strengthening the dollar through higher demand, which would work against that goal.

Therefore, one needs a mechanism that allows divergence between domestic and foreign borrowing conditions — effectively increasing borrowing costs for foreigners relative to domestic borrowers — to create a financial incentive for domestic production. One part of this is already evident in Trump’s tariff policy, which aims to make US production more attractive, even if the results so far have been mixed.

A central planner facing such a scenario might look to create a “two-layered borrowing structure,” in which the rest of the world pays a premium for access to dollars, while the US operates domestically under more favorable financial conditions. At the same time, a full restriction of foreign access to US assets would be counterproductive, as it would remove a key source of demand for financial markets. The system therefore requires continued foreign participation — either through sustained capital inflows or through mechanisms that redirect newly created liquidity into both production and asset markets.

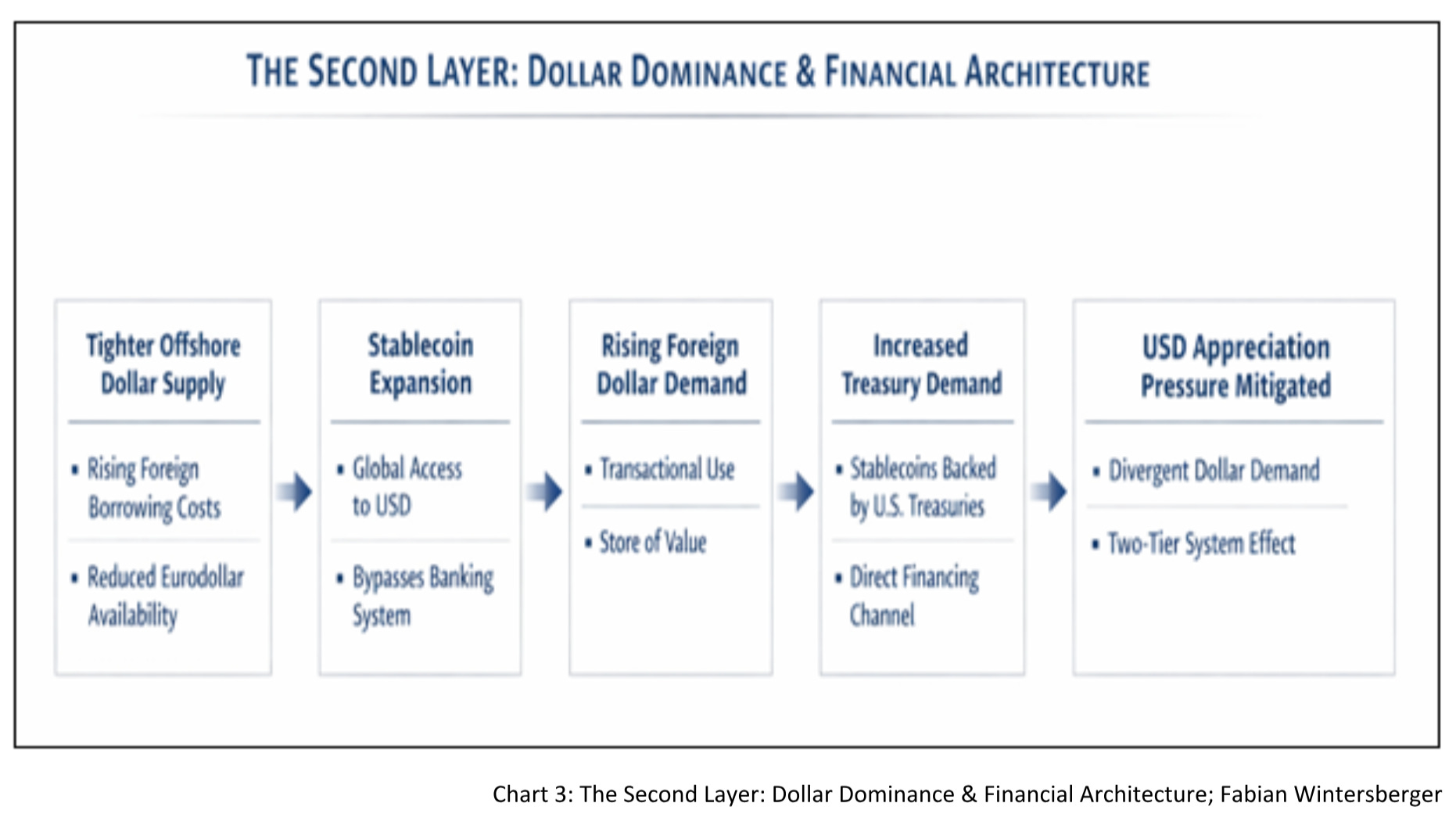

Under that lens, recent developments around stablecoins become more interesting. The push for USD stablecoins can be interpreted less as a domestic financial innovation and more as a tool aimed at foreign dollar users. While tighter borrowing conditions reduce the supply of offshore dollars, expanding access via stablecoins increases foreign demand for dollar-denominated liquidity.

These stablecoins, in turn, are typically backed by US Treasuries, effectively channeling foreign demand for dollars directly into government financing. At the same time, they allow foreign users — especially in weaker currency regions — to hold and transact in dollars without relying on the traditional banking system.

Additionally, consider the implications of lower US interest rates. A reduction in yields would normally weaken foreign demand for US assets. However, if access to dollars increasingly shifts toward stablecoin-based systems, foreign demand can be maintained through transactional and precautionary demand for dollars rather than purely yield-driven investment flows.

The result is a system in which foreign demand for dollars is preserved, capital continues to flow into US assets, and the upward pressure on the currency is partially mitigated. In that sense, financial architecture becomes an extension of geopolitical strategy — complementing the control over logistics with control over settlement and capital flows.

In that sense, what appears to be a series of disconnected policy moves begins to resemble a more coherent structure — one that links control over physical supply to control over financial settlement. And while the effectiveness of such a strategy remains uncertain, its implications for markets are anything but.

Market Assessment

As laid out in the introduction, my market assessment from last week still stands:

My outlook for bonds remains bearish, equities are neutral to bearish, and the dollar is likely to strengthen further as long as the war continues.

What would change that view is the reopening of the Strait of Hormuz. For financial markets, one can largely ignore the noise of armchair military analysis and focus on that single variable. Once that happens, forward-looking markets will begin to price in a recovery. Otherwise, it remains a whipsaw market.

Conclusion

Within the turmoil and fog of war, it could be that the market is undergoing a more structural change rather than being solely tied to geopolitical events. Central planning often leads to pursuing overconfident ideas, like the control over energy and logistics on one layer of that shift, and control over the dollar and the financial architecture on the other.

For markets, this creates an environment in which short-term price action remains dominated by headlines, but underlying dynamics become increasingly unstable. Regardless of whether such a strategy can be sustained without creating further distortions, unintended consequences and bigger problems, connecting the dots increasingly points into that direction.

If it’s pursued, markets may have to adapt to a world in which capital, prices, and trade are shaped less by coordination and more by geopolitical strategy and force.

“Destroy Everything,” and rebuild what follows.

Cleanse this world with flame

End this, cleanse this

Rebuild and start again

Obliterate what makes us weak

End this and embrace the destructionHatebreed - Destroy Everything

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.