Desperate Times, Desperate Measures

While the economic environment stays turbulent, the crucial topics remain the war in Ukraine, the consequences of (planned) sanctions in the energy market, and the rise in interest rates. As some members of the FOMC flirted with a 75bps rate hike before the May meeting, market participants eagerly awaited the Fed’s interest rate decision last week.

However, the Fed only hiked rates by 50 basis points, and Powell pushed back from speculations about future rate hikes of 75 basis points. During the FOMC-press conference, he said that a 75bps rate hike would be nothing the FOMC actively considered.

Regarding the shrinking of the balance sheet, the FOMC stated that it plans to shrink its holdings of US-Treasuries and Mortgage-Backed-Securities at a pace of 57.5 billion a month (starting in June) and will increase it within three months to 95 billion per month.

The market celebrated that message, and all US indices edged higher (about 3 %) while the dollar sold off slightly after the press conference, with interest rates on the long end of the curve also falling.

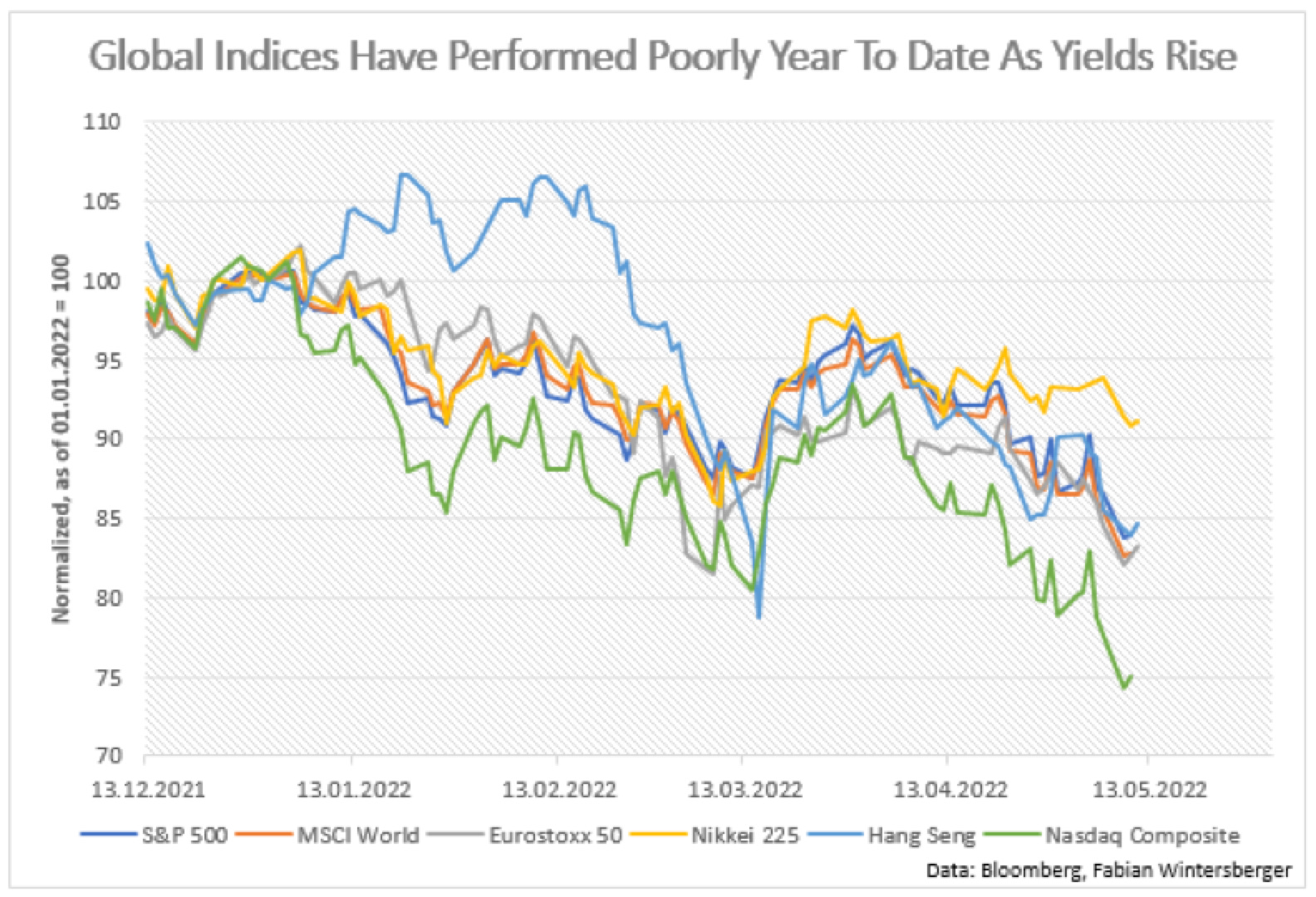

Nevertheless, the happiness was very short-lived, and already the next day, those movements reversed. The S&P 500 was down 3.6 %, while the Nasdaq fell more than 5 % and marked one of its hardest U-turns in history. Globally, equity indices have lost close to 20 % this year so far. Only the Japanese Nikkei lost less than 10 %, although the recent devaluation of the Yen probably plays a significant role here.

The fact that bonds and equities have fallen points that market participants prefer to go into cash and hence into the King of Cash, the dollar, because of the current weak economic environment. While a recession in Europe looks very likely, there are still chances that the US can avoid a recession this year. However, the economies on both sides of the pond are looking less and less compelling and suggest at least a sharp slowdown in both economies.

Within commodity markets, prices have stayed at high levels, as the zero-covid policies by communist China have had a dampening effect on demand. At the same time, the US attempts to curb further price increases by releasing parts of its SPR. Simultaneously the EU has adjourned its decision on whether to ban Russian oil immediately from the market. The price of oil (WTI) is trading within a tight range between 100 and 110 dollars, and investors should remain cautious regarding a potential setback.

Although, the latest consolidation in oil prices only tells one part of the story. The consumer does not benefit from it, and lately, the prices at the pump have increased further. A recommended read by Javier Blas tells us more about the reasons.

Firstly, global demand has rebounded strongly after the pandemic and caused inventories to fall to a 30-year low. Secondly, despite the releases of SPRs, no considerable amount reaches the market in the form of refined products, and as Blas writes, only in Europe.

Another point is refining capacity has fallen over the years, and thus producers cannot produce enough fuel to keep up with the demand. This is another political failure because due to the planned coming ban on fossil fuels, the industry drove down investments, driving capacities down to a 30-year low.

Finally (because of the war), many companies self-sanctioned Russian oil on which, especially European refineries, relied upon. This means that Europe not only suffers from lower oil imports but also in production capacity, which is another argument why a western embargo on Russian oil might be disadvantageous.

Those who profit in the current environment are the big refineries whose margins have increased remarkably. Blas ends his opinion piece by saying that the only solution will be lower demand. But therefore, a recession is necessary.

But not only oil liquidity, the lubricant for the real economy, is drying up. The same is true for the financial grease of our economy, monetary liquidity. The war in Ukraine has exacerbated the dynamics that the pandemic put in motion.

The European and American public is already feeling the burden of inflation, and thus politicians put pressure on central bankers to put in the necessary monetary policy to fight it.

Because of the dollar system, the Fed’s monetary policy is significant for international financial markets. Especially the Anglo-Saxonian area is going forward in fighting inflationary pressures, as the Fed and the Bank of England have already started their rate-hiking cycle. Since then, the dollar has appreciated against all other major currencies and emerging market economies.

However, the European Central Bank is still hesitant about a normalization of monetary policy. Recently, some European central bankers have signalized that the ECB might raise rates in July while it plans to end asset purchases in June. Although, if one compares the Euribor Futures Yield Curve with the Eurodollar Yield Curve, one can see that markets expect the ECB to act much more cautiously than its US pendant.

Thus, I assume the depreciation of the euro against the dollar to continue, even though we might be in for a short-term setback if euro bulls can defend the critical resistance in the 1.04-1.05 range.

A stronger dollar, which one can expect due to the Fed's restrictive interest rate policy and aggressive balance sheet reduction, hinders both the financial markets and the real global economy. Especially emerging markets profited from a weaker dollar, as many local companies issued dollar-denominated debt and changed it back to local currency to invest in the domestic market.

If the dollar starts to rise, those currencies come under pressure, and local central banks have to sell their dollar reserves if they want to defend the exchange rate. A weaker domestic currency might trigger a flight of capital into the dollar as investors increase their demand for dollars. Further, this would put local companies who borrowed in dollars because their debt rises in value if the dollar appreciates.

Europe is also suffering from a depreciation of the euro against the dollar because investors will prefer to hold dollars instead of euros if the EUR/USD exchange rate drops. Additionally, the investors enjoy a higher interest rate, especially since real yields in the US have turned positive. In recent weeks, nominal 10y yields continued to rise while inflation expectations stagnated and started to fall this week.

Falling inflation expectations might indicate that the market is indeed expecting that the Fed will succeed and can dampen inflation over the long run. But the inverse Eurodollar yield curve suggests that market participants are not so sure about the second part of the equation and that the Fed is able to achieve a soft landing. I assume that the market thinks the Fed will exaggerate its tightening path.

I believe that Europe will definitely experience a recession this year, and the recent Ifo-Index, which is a good proxy for the coming economic situation, supports that. Regarding the United States, there are two possible outcomes. At best, the US economy will only experience a sharp slowdown this year, and at worst, the US will also go into recession. In any case, the negative GDP number in Q1 does not bode well.

On the other hand, many journalists and Fed officials point out that consumption is still strong. While this may be true, I disagree that this signifies that the consumer is still in good shape. Rising credit card debt and a rise in mentions of weak demand in company calls support my assumption that the consumer is already in worse shape than many might expect.

As a result, we may conclude that the rise in real yields indicates that the Fed will probably succeed in bringing inflation back, but for the wrong reasons.

Debt/GDP ratios in the United States and the Eurozone are already at levels we have not seen since the Second Worldwar. A further appreciation of the dollar while the world economy is slowing could put even more pressure on debt ratios.

A stronger dollar not only hurts the rest of the world and is also poison for the US economy. It makes imports cheaper while domestic production becomes more expensive in comparison. Simultaneously we experience a situation where European competitiveness becomes weaker due to higher production costs because of the rise in energy prices.

Rising real yields combined with a fall in economic activity will cause debt/GDP ratios to increase further, hindering Europe and the US from putting in countermeasures to fight the slowdown.

Last year, the sharp rise in inflation rates had positive effects on debtors (governments, households, and businesses) because their debt burden shrank and hence the debt/GDP ratio. As I have pointed out several times on this blog here, debtors favor inflation because of that. However, as inflation has spread throughout the economy and the population now experiences it, governments are forced to pressure central banks to fight it, although they secretly welcome the rise in inflation.

A more restrictive monetary policy drives real rates up further because if central banks shrink their balance sheets, they actively raise the supply of government bonds and mortgage-backed securities in the market, and this will, all else being equal, lead to a fall in bond prices and thus result in a rise in the rate of interest. Bond spreads are already close to 2018 levels, where the Fed had to pause its last hiking cycle. And even if the central banks can prevent a further rise in spreads, yields will be higher anyway.

The question is how long monetary policy can be tight in times of such high debt levels. The latest rises in the inflation rate lead to record tax receipts in the US and many European countries, but especially in the United States, tax receipts are highly sensitive to stock prices. In an environment where stocks are going down, tax receipts will do too.

Not long ago, the US government announced that it plans to issue fewer bonds this year to reduce the deficit. But as institutional investors are obligated to hold government bonds because of regulatory reasons, lower supply will drive bond yields lower.

Higher yields can become a problem, especially in times of high elevated debt levels. Additionally, during the last decade, the loose monetary and fiscal policy has caused a shift from engagements in the real economy to more investments in the financial sector.

These high debt levels might be one of the major causes why the ECB is so hesitant when it comes to a normalization of monetary policy because the problem child in Europe is not Italy, as so many assume, but Christine Lagarde’s home country. Being economically weak because of high regulations and government spending, France has a total (government, households, and businesses) debt/GDP ratio of 361 %. Worldwide, this makes France part of the top 10 most indebted countries.

Therefore, I assume that not only we are at the beginning of a monetary tightening cycle, but we are already nearing its end. Admittedly, I also expect stocks to fall much further until the authorities take monetary and fiscal countermeasures. I guess that they have to go down to the lows of March 2020, but who knows.

But even then, it is not a done deal that equity prices can continue their long-term upward trend because I expect that central banks might follow the Bank of Japan and introduce a Yield-Curve-Control system, firstly in Europe.

However, I do not expect central banks to start to monetize the debt immediately. More probable, a change in regulatory measures will force institutional investors to buy government debt at a given yield.

If this situation appears, one can assume that we are only at the beginning of a prolonged equity bear market. If institutions are obligated to buy government bonds at a specific yield, they will have to sell something else first, and something equals equities.

But Desperate Times call for Desperate Measures.

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)

Great article, thanks!

I think you might have it wrong here, though: "Not long ago, the US government announced that it plans to issue fewer bonds this year to reduce the deficit. But as institutional investors are obligated to hold government bonds because of regulatory reasons, lower supply will also drive bond yields higher."

If supply dries up because fewer bonds are issued and demand stays the same for regulatory reasons, the price of bonds will rise and yields will fall instead of rise.

I think the regulatory changes are something that nobody is considering these days but is both likely and impactful