Dead Eyes See No Future

The measure of intelligence is the ability to change - Albert Einstein

In 1789, the French Empire faced a profound economic and societal crisis. Beginning in 1715, the French population grew from 21 million to 28 million. While the middle class nearly tripled during this time, economic prosperity distribution was uneven. The upper classes, particularly the mercantile and rentier classes, reaped substantial benefits, while poorer segments experienced declining living standards.

Whether you were a wage laborer or a peasant farmer forced to rent your land, you gained little from the overall increase in economic prosperity. This disparity alone would have heightened societal tensions. Still, the situation deteriorated further due to an economic recession in 1785, compounded by two poor harvests that resulted in soaring food prices and rising unemployment.

Therefore, it is not surprising that these conditions culminated in the French Revolution of 1789. The most prominent symbols of this divide were King Louis XVI and his wife, Marie Antoinette, the Austrian-born queen of France. Marie Antoinette became increasingly unpopular among the French public due to her extravagant lifestyle and love of luxury, fashion, and lavish parties, earning her the derisive nickname "Madame Deficit" as France's financial troubles deepened.

An urban legend, likely propagated by philosopher Jean-Jacques Rousseau, accused her of responding to the plight of starving French peasants with the phrase "Let them eat cake." Although the quote was fabricated to demonize her, it highlighted the widespread sentiment that the monarchy had become disconnected from the realities faced by ordinary people.

As the revolution progressed, she and Louis were imprisoned, and their attempts to flee France only fueled public animosity toward them. They were incarcerated in 1792, and one year later, they were executed. Despite its inaccuracies, the "Let them eat cake" legend persisted, encapsulating the image of an elitist monarchy that failed to understand or address the growing desperation of its citizens.

In contemporary discourse, critics of policymakers and mainstream economists frequently invoke the "Let them eat cake" narrative to suggest that many of these figures have similarly lost touch with reality, ensconced in their ivory towers and disconnected from the experiences of ordinary people. Moreover, many assert that the official economic data is manipulated to create a more favorable view of the economy.

Public surveys reveal a widespread belief that living standards have eroded, real incomes have plummeted, and the overall economic situation is much worse than in 2019. However, before delving further into this issue, it's important to note that research has emerged seeking to explain these perceptions.

This research has given rise to the term "Vibescession," referring to a phenomenon where, despite economic indicators suggesting resilience (or stagnation in Europe), a cycle of crises, bad news, and the rapid spread of information via social media contribute to a pervasive feeling of economic decline, even among those who may be better off than ever.

While official statistics on consumer price inflation, GDP growth, and employment indicate that the U.S. economy remains robust, many economic observers continue to predict an imminent recession or claim that one is already underway. However, a review of these commentators' track records reveals that they tend to portray a bearish narrative about 95% of the time.

As many point out, metrics such as unemployment, economic growth, and inflation depend heavily on measurement methods. These figures are invariably estimated using statistical methods and models. Last week, EJ Antoni and Peter St. Onge published a working paper in the Brownstone Journal to provide "a true understanding of inflation… and thus of true economic growth since 2019."

Those unfamiliar with Antoni and St. Onge’s social media profiles should note that they often lean towards a bearish outlook. Nonetheless, their analysis merits closer examination, regardless of whether one agrees with their conclusions.

Their paper presents valid criticisms regarding the accuracy of measuring economic activity and inflation. While they do not propose a definitive solution for improving the measurement of nominal economic activity, they focus on the question of whether the official inflation rate is accurate.

Why is inflation significant? It is used to derive real growth from nominal growth. If the actual inflation rate is higher than the figure the Bureau of Labor Statistics reports, then real growth is correspondingly lower. Indeed, several compelling arguments suggest that the consumer price index (CPI) is flawed in many respects, failing to accurately reflect real cost changes.

Antoni and St. Onge begin their critique of the official CPI with homeownership, primarily represented by the Owners' Equivalent Rent (OER) measure. They argue that while this is not problematic when rents and home prices rise in tandem, it becomes an issue when one rises significantly faster than the other.

Unfortunately, the cost of owning a home has risen much faster than rents over the last four years and the CPI has grossly underestimated housing cost inflation.

They also address the "bias related to regulation," touching upon hedonistic adjustments, where prices are often adjusted downward due to "quality improvements," potentially overstating nominal gains in quality.

Another interesting point they make concerns price changes that consumers indirectly bear:

Premiums are used both to pay for the actual cost of providing the service of insurance (risk mitigation) and for medical services and commodities. The CPI neglects both, and instead imputes the cost of health insurance from the profits of health insurers.

Thus, if insurer costs rise while their profits decline, this would be recorded as a decrease in health insurance costs, even though consumers still pay the same amount. This leads to the core of the authors' analysis: if BLS estimates of consumer price inflation are too low, then inflation-adjusted real numbers do not accurately reflect consumers' experiences.

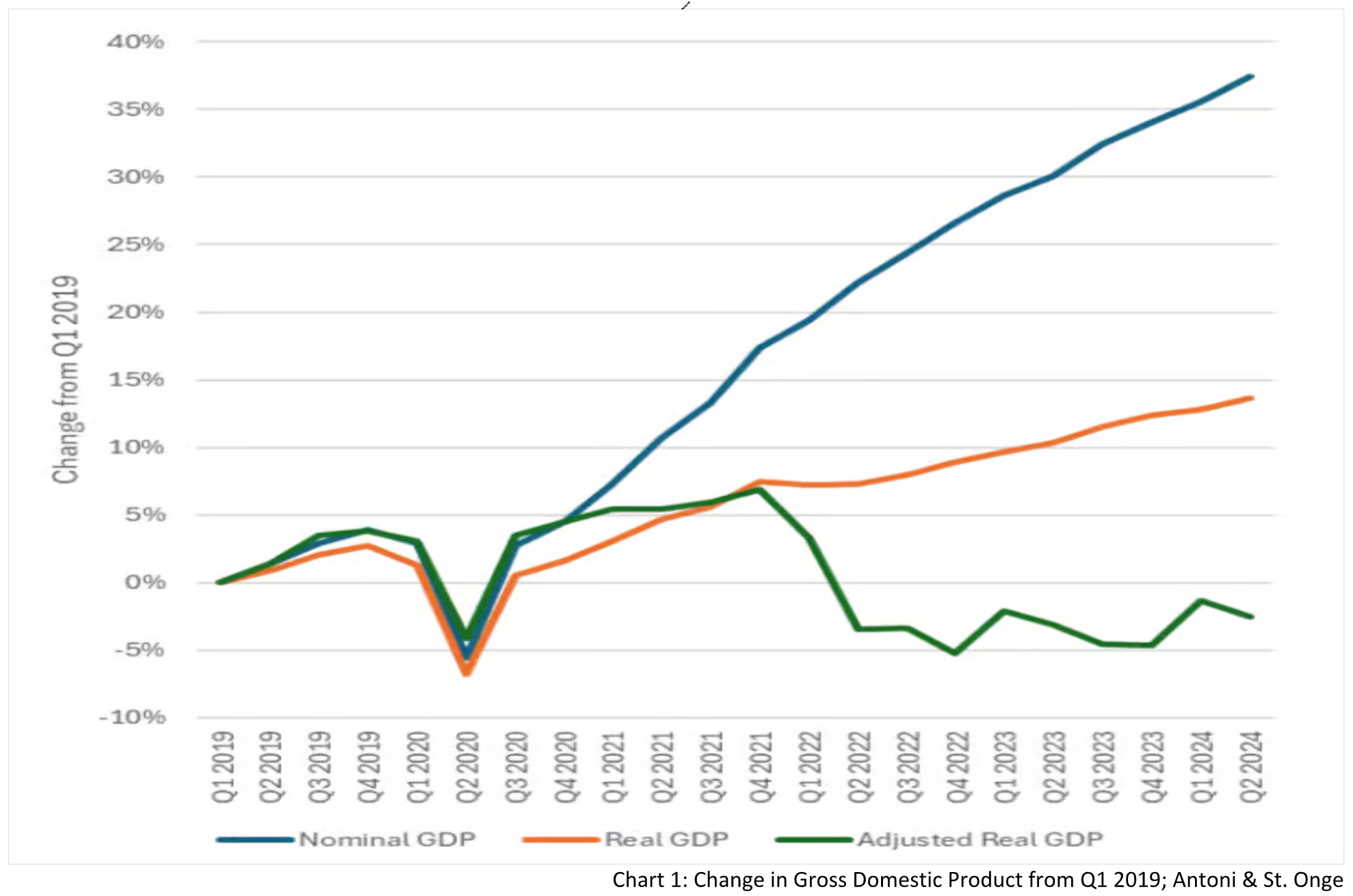

The authors recalibrate real incomes using what they consider a "more appropriate" inflation metric, incorporating their previous criticisms. They find that while official figures suggest real income growth, their adjustments show it has been negative since 2022. The adjusted housing component of the CPI had the most significant impact on their findings. Interestingly, their analysis indicates that deregulations during the Trump era also contributed to a falling cost of living that was not captured in the official CPI.

Additionally, they substitute their adjusted figures for the GDP deflator to derive the "adjusted" real Gross Domestic Product. Remarkably, until the third quarter of 2021, the adjusted and official real GDP figures tracked closely together, but the subsequent inflation wave caused a significant divergence, with adjusted real GDP turning negative compared to 2019.

Even without considering population growth and per capita GDP, the adjusted real GDP values imply that the nation entered a recession in the first quarter of 2022 and remained in that contraction through the second quarter of 2024. In just three of those ten quarters did adjusted real GDP increase (with one being only a marginal increase) and none of the increases occurred in consecutive quarters.

As a result, these adjusted figures support those who argue that the U.S. economy is already in recession, albeit the authors suggest this has been the case longer than most proponents of that view claim. At the very least, the paper challenges the official narrative that the U.S. is experiencing a robust economic expansion.

While the paper is undeniably intriguing, it raises the question of what investors should make of its findings. After all, the market appears to disagree with the authors, having trusted the official numbers. However, I believe there’s a critical nuance to consider that counters the bearish case many people present. Regarding the stock market, most bears act like people with dead eyes who see no future.

If the authors' figures are accurate, the Federal Reserve may have inadvertently replicated a strategy it employed a century ago during the "Forgotten Depression" of 1920. During that period, under William P.G. Harding, the Fed raised interest rates amid a recession, which escalated into a full-blown depression. However, this depression eventually subsided, paving the way for significant economic growth during the "Roaring Twenties."

Looking at the S&P 500 chart since 2020, it appears that stock prices have indeed signaled the onset of the "recession" identified in Antoni and St. Onge's analysis. The S&P began to decline at that point, bottoming out in the third quarter of 2022—just one quarter after the authors’ calculations indicated that real GDP had begun to recover (as illustrated by the red line in Chart 2).

Examining the GFC, we see that the S&P 500 began to decline precisely when the recession started and only started to recover when real GDP hit its lowest point. A common counterargument is that interest rates also fell during the GFC, as the Federal Reserve cut rates in response to the recession.

In contrast, the current situation is different: the Fed began raising interest rates precisely at the onset of the recession, mirroring its actions in 1920. This increase has made conditions more challenging for businesses with high short-term debt while benefiting those that refinanced long-term and took advantage of the previous low-interest-rate environment.

Consequently, it is unsurprising that the proportion of companies within the Russell 2000 reporting negative earnings is nearing record highs. This outcome aligns with expectations following a period of negative real growth, which has slowly begun to recover as high interest rates compel the economy to restructure.

While it’s difficult to quantify whether ongoing government spending has interfered with this restructuring or misallocated resources, it’s clear that the private sector has had to adapt to the new economic landscape characterized by high interest rates. If the authors are correct in their assertion that a recession or depression is already underway but has already bottomed out, then optimism should improve, as indicated by the latest Empire Manufacturing Survey.

Before we assess the implications of these findings for future asset price movements, it’s worth noting that U.S. nonrevolving consumer credit also supports the theory that economic activity and real economic growth are improving. In a contracting economy, the supply of loans typically decreases as banks implement stricter lending criteria, resulting in fewer individuals qualifying for credit.

As a result, nonrevolving consumer credit should reach its lowest point after the recession's trough and then begin to improve as economic conditions gradually stabilize. The Fed's recent decision to lower interest rates also facilitates borrowing for the private sector, which is likely to translate into increased loan activity. Current data suggests that nonrevolving consumer credit may already be starting to pick up again.

It’s somewhat ironic that the Federal Reserve may have inadvertently raised interest rates into a depression while simultaneously doing the right thing. Their primary objective was to combat inflation already baked into the economy due to the substantial increase in the money supply during 2020 and 2021, which ultimately forced an economic restructuring.

Moreover, the decline in the total labor force participation rate since 2019 can largely be attributed to many older workers exiting the workforce due to early retirement. I would argue that this trend is a significant driver of the labor shortage, which will keep wages elevated and compel businesses to innovate, restructure, and become more cost-efficient to navigate this challenge.

This perspective challenges the "vibecession" narrative and explains why many people feel worse off than before the pandemic and are dissatisfied with the current administration. While one might intuitively assume that rate cuts and a recession in the U.S. economy would lead to a stock market correction and a rally in bonds, my thesis is that such positioning may not materialize as expected.

With the Federal Reserve believing it has won the battle against inflation and concerned about a potential weakening of the labor market, it is now fully committed to cutting interest rates. The pressing question is how far it can lower rates in an economy where inflation is declining, and real growth appears to be picking up.

If Antoni and St. Onge are correct that the recession has been ongoing since 2022, and if real growth has indeed begun to improve, then long-term interest rates may have limited room to fall and could even rise. This scenario suggests a diminished likelihood of an immediate reaction in the U.S. stock market.

Monetary easing will likely provide a tailwind for stock prices, indicating a potential bull market continuation. Earnings reports thus far have been quite positive, particularly in the financial sector. The situation has improved for those with fixed-rate borrowings due to the high income growth caused by the previous inflation wave. As short-term interest rates begin to decline, borrowing should increase, even if long-term rates rise due to stronger real growth, since people can afford to pay a higher rate.

However, as the Fed eases in an environment of persistent real growth and falling inflation, these policies could steepen the yield curve and potentially increase long-term interest rates. Eventually, the money supply expansion will re-enter the real economy, causing inflation and driving long-term interest rates higher.

Observing the market and genuinely listening to its signals appears to tell the story I have outlined here. Gold prices have risen since Antoni and St. Onge's "real GDP" bottomed out, decoupling from real yields. One could argue that long-term real yields, or more accurately, expected long-term real yields, may be mispriced, as I discussed last week.

If this is the case, it is unsurprising that gold has risen despite the uptick in expected 10-year real yields, as those yields might still be too low. However, now that the Fed is cutting interest rates and expanding the money supply, it seems that gold is already anticipating a future rise in inflation.

Despite the prevailing belief that Fed cuts will push long-term yields down, this and the potential mispricing of R* may also drive nominal long-term yields higher and the dollar lower against tangible assets. Nevertheless, the thesis also suggests a rising dollar compared to other fiat currencies in the long run.

Therefore, I continue to believe that a current bearish outlook on stock prices is unwarranted and that bonds will likely perform poorly in both nominal and real terms. Additionally, I expect the recent outperformance of gold compared to stocks and bonds to continue.

The possibility that the Fed might have unintentionally made the right decisions could upend many established rules of financial markets moving forward. Just as "dead eyes see no future," stock market bears may be disappointed for longer than anticipated, as their pessimistic outlook clashes with a market that defies downturns and continues to push forward.

Dead eyes

See no future

Falling from grace

We are coming homeArch Enemy – Dead Eyes See No Future

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. They do not constitute investment advice, and my perspective may change over time in response to evolving facts. It is strongly recommended to seek independent advice and conduct your own research before making investment decisions.