Dancing With The Enemy

It is February 13, 1998, the day of the Nagano Olympic Downhill race. For days, the supreme discipline in alpine skiing has been repeatedly canceled due to bad weather, and skiing fans all over Europe have gotten up in the middle of the night in vain on several occasions. Now, the day of the race has finally come, and as it turns out, the day will go down in the history books.

One of the top favorites for the gold medal is the Austrian Hermann Maier, who is in his second professional season. 2 years prior, he was accidentally noticed by the Austrian Ski Association when he was a precursor for the Giant Slalom in his hometown, Flachau. If he had been in the rating, he would have finished in 12th place on that day. This year (1998), he already won in two downhill classics, Bormio (ITA) and Wengen (CH). Now, he wants to make his dream of Olympic gold a reality in Japanese Pyeongchang.

When Maier starts the race as the fourth runner, the French Jean-Luc Cretier is in the lead, and Maier’s determination to win the race is writ large on his face. In the deepest downhill position possible, he passes the first gates of the trail. Then, after 18 seconds, at the seventh gate, it happens: After an S-curve, Maier loses the ground after a bump, and he flies about 40 meters through the air. When he takes off, he is probably about half a second faster than Cretier, the later gold medalist.

The impact is hard, and when his body stops whirling around, he has torn several security fences. Yet, the worst is avoided, and a few seconds later, Maier signals all clear. However, his body is full of bruises from the fall. There is only one picture of Maiers flying through the sky, shot by the American photographer Carl Yarbrough.

The following discipline, Super-G, that should take place the next day is Maier’s parade discipline. Although his body clearly is not ready for racing, he assures every functionary of the Austrian Ski Association that he will start, no matter what.

However, the weather is making another monkey wrench in the works, which is not to Maier’s disadvantage. The race takes place three days later, leaving Maier some time to cure his injuries. Yet, from a rational standpoint, the idea that he might win a medal is very doubtful.

But Maiers unconditional will makes the impossible possible. Sensationally, he wins the Super-G with a lead of more than half a second. The fairy tale is complete when he wins the Giant Slalom a few days later. From this point, Maier is well known worldwide, and the world gives him the nickname Herminator, inspired by the movie character Terminator, played by the born Austrian Arnold Schwarzenegger.

Since then, Maier has been a legend in professional sports and has become one of the most successful in his profession. The way he skied down the trails was uncompromising, and every run literally was a dance with the enemy, the track he wanted to combat as fast as possible. This week, Hermann Maier became 50 years old and can reflect on a turbulent life. However, the days around February 13, 1998, made him immortal.

A saying is that only sport writes such stories. However, in financial markets, investors daily have to act similarly and estimate risks within moments to make the right decision. They, too, are influenced by things they cannot control, just like a downhill racer. While for downhill racers, there are things like the wind, the weather, and the conditions of the trail, in financial markets, it is central banks, politics, and the actions of other actors.

Just as every Friday in the new month, US Nonfarm payrolls got published last week. As the US is still experiencing extraordinarily high inflation, the numbers should hint at the future path of the Federal Reserve’s interest rate policy. After all, several members of the FOMC have repeatedly stated that the conditions in the labor market are crucial to bringing inflation back down to target.

Yet, the numbers showed that the labor market remains very tight, and Nonfarm payrolls increased by 263,000, 63,000 higher than expected by analysts and economists. Average weekly earnings rose 5.1 % year-over-year, and the unemployment rate remained at 3.7 %.

On the other hand, one could argue that this is only one side of the truth because the number of full-time jobs has decreased since March this year while part-time jobs more than compensated for the decrease. Yet, market participants have cared primarily about the overall NFP number and not about composition for years. And one can conclude that the Fed might follow its tight monetary policy standpoint for longer than some might like.

Last week, in his speech at the Brookings Institution, Jerome Powell said that the demand for labor is still exceeding its supply and the pace at which nominal wages are increasing is well above what would be consistent with 2 % inflation over time. Obviously, the Fed cannot lower the labor supply if it wants to rebalance the labor market; its only tool is reducing labor demand via interest rate increases.

The latest CPI numbers showed that goods inflation is decreasing, but service sector inflation is getting sticky. That is a result of the tight labor market because companies have to outbid each other to get the workers as they compete for labor. Nonetheless, wages are a much higher cost factor in the service sector than in the production sector. The higher the cost of labor, the higher the price for the service sector good, as companies pass on the increase to consumers.

Although, if one looks at the total labor supply, it shows that the US labor force did not grow for a while now, and it has grown well below its multi-year trend since the pandemic started because of excessive retirement.

Risk assets like stocks have been falling since last Friday, and while long-term bond yields are at about the same level as before the Nonfarm payrolls were published, short-term yields are notably higher. It seems as if market participants are waking up to the fact that their hopes for an end of the hiking cycle probably were a bit premature.

However, the fact that long-term bond yields have fallen might hint that the current inflation rates are not signaling a reversal in the trend and that the Fed will succeed in bringing inflation back below its 2 % goal.

Still, no one should be surprised that years of monetary and fiscal expansion have left traces. The additional currency units continue to circulate in the economy and keep demand for goods and services elevated, which could lead to stickier inflation. The recently published numbers for durable goods orders support that: while they have fallen since their peak last year, they are still very high, and one could assume that the Fed still has not succeeded in its aim to destroy demand.

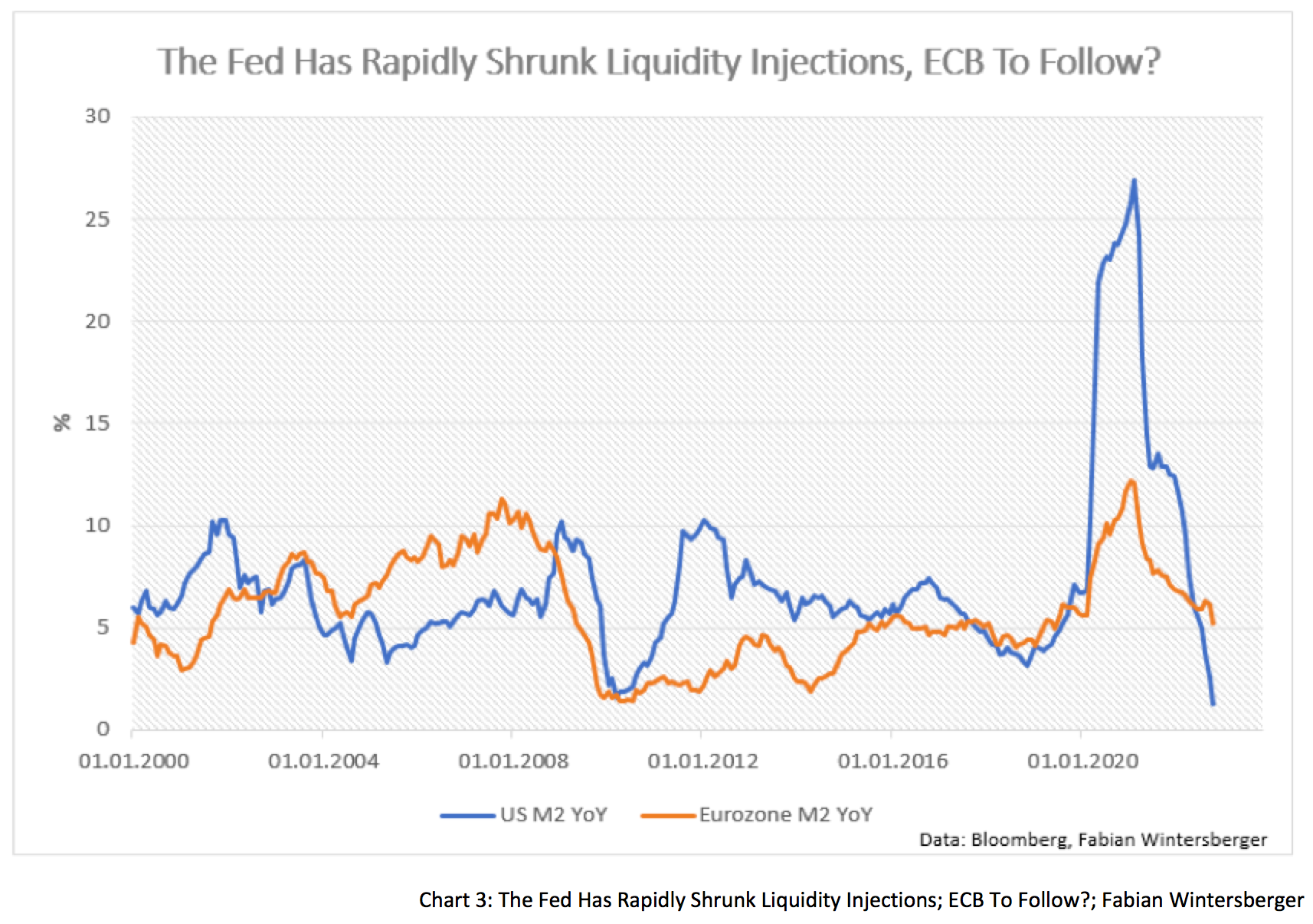

Around the globe, central banks are trying to get inflation back under control, and market participants still believe they will undoubtedly succeed. M2 YoY has fallen rapidly, so central banks are taking liquidity out of the system. The fall in M2, hence a withdrawal of liquidity, is pulling asset prices down, which have become increasingly dependent on additional liquidity over the years due to expansive monetary policy.

In the United States, M2 YoY is already lower than during the heights of the Great Financial Crisis of 2008, but in the euro area, it is still growing at a faster pace year-over-year than during the 2010s. If the ECB wants to follow the Fed and continue to fight inflation, one can conclude that euro-area M2 is still too high and needs to fall further.

The fall in M2 has implications for the future development of inflation. In the US, inflation has already fallen for a few months, partially because of the fall in M2. If the money supply is shrinking/growing slower, prices cannot continue to rise as rapidly as before. At some point, businesses might face a situation where they cannot pass costs to consumers anymore.

Excessive savings accumulated during the pandemic are now concentrated in the highest income brackets, and one can assume that they will continue to fall. The savings rate in the US has already fallen substantially and has never been so low since 2005. Until now, companies could pass cost increases to consumers, which explains the strong earnings of US companies. However, if they cannot pass on costs anymore, earnings will go down, and more companies will have to cut earnings estimates. That will lower inflation but probably also equity prices.

When that moment occurs, one will see if central banks continue their uncompromising stance and do not, as rates markets indicate, lower rates again. Currently, market participants estimate that the Fed will already lower interest rates next year and that the ECB will also end its rate hiking cycle at around 3 %.

For the euro area, market expectations seem to be in line with recent comments from members of the ECB’s Governing Council, who - despite inflation north of 10 % - are saying that interest rates are already close to neutral. It appears that market participants believe the narrative seeded by the ECB, but should they?

The most significant junk of money in the real economy is money created by commercial banks. Banks lend money to consumers or businesses for consumption or real economic investment. Primarily, central banks hoped that slashing interest rates and buying longer-term bonds would stimulate real economic investments and that the rise in economic activity would drive inflation higher (to 2 %). Though, the result was that money was primarily used for financial investments, resulting in rising asset prices, or assumingly asset price bubbles, especially in the bond market.

After the worst performance in the bond market history, one can undoubtedly say that this is a sign that recent changes in monetary policy have already led to air coming out of the bubble. Yet, since summer, bonds have shown relatively resilient, and currently, long-term bond yields are clearly off of their year highs. At the moment, yields of longer-term debt look attractive compared to expected future inflation rates, at least if one presumes that expectations are justified.

However, the question is if the market expectations are correct because the rise in interest rates resulted in loan exposure becoming attractive again for banks. Yet, the interest rate environment is still disturbed because of monetary interventions. Thus, one can conclude that capital continues to be misallocated and will not strengthen real economic productivity.

In the US, loans and leases in bank credit rose 12 % year-over-year in Q3, which is about threefold the growth in 2018. Loan growth is also higher than 2020 when the US treasury generously handed out credit guarantees.

In the euro area, those credit guarantees are still in place, and one can observe accelerating loan growth. In the US and the euro area, year-over-year loan growth is higher than at any point during the 2010s.

Rising loan growth translates into a rise in the money supply in the real economy, and if the quantity of goods does not grow at the same pace, that is inflationary. The lack of labor supply is also inflationary, as discussed above. Therefore, it might be that market participants are underestimating inflation risks and are expecting a too-large decrease in inflation rates.

Additionally, the fall in consumers' real wages changes their consumption patterns. Walmart CEO Doug McMillon told CNBC that the retailer observes a shift in consumption patterns because of high inflation and that consumers are more selective about their purchases.

According to McMillon, consumers skip purchases of electronics and buy staples instead. Due to hedonistic adjustments, electronics are deflationary because they have become technically better over time. If the share of staples in total consumption expenditures rises while the share of electronics falls, one may assume that calculated consumer price inflation might become elevated.

As a result, one could expect inflation to stay higher for longer, longer than market participants are currently anticipating. As a result, the Fed and the ECB will probably have to run a more restrictive monetary policy for longer than now expected. If that is the case, one may observe a continuation of elevated inflation in consumer prices and simultaneous deflation in asset prices, especially if governments continue their fiscal expansion in such a scenario.

If one looks at what might happen until year-end, the latest expectations of market participants still hint that the bond rally continues until year-end. Despite the recent sell-off, I would not rule it out entirely for the stock market either. Given the current market environment, market participants will have to continue dancing with the enemy.

All that you have to do, is keep what you held onto,

This is where we dance, tonight, tonight, tonight.Still Remains - Dancing With The Enemy

I wish you a splendid weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity and are no investment advice)