Curse

On AI, Cordination Costs, And Why Demand May Not Collapse

Sometimes, the narrative around markets changes fast. On Friday, the US Supreme Court ruled that the Trump-era tariffs were unlawful. By Monday, however, new tariff proposals of 10–15% were already being discussed, without any substantial effect on markets.

The financial media had already moved on before stocks suddenly sold off on Monday. On Tuesday, Bloomberg attributed the market sell-off to a renewed “AI scare trade,” writing:

The artificial intelligence “scare trade” erupted again on Monday as growing concerns about the disruptive power of AI dragged down shares of delivery, payments and software companies, and sent International Business Machines Corp. to its worst plunge in 25 years.

What the financial media identified as the source of the sell-off was a scenario analysis by the small research firm Citrini, which publishes its work on Substack.

Why AI May Expand The Division Of Labor

In the piece, the authors theorize about what would happen if “AI eats everything” — effectively eliminating a vast share of white-collar jobs, forcing workers into significantly lower-paid positions or unemployment. I will not repeat my critique here, as I already published a short rebuttal on X. In essence, while the piece is an interesting read, it neglects several basic economic principles in a way that echoes classical underconsumption theories. Nevertheless, it prompted me to consider an alternative scenario built on similar assumptions but leading to a very different conclusion.

While the Citrini piece argues that AI will allow certain companies to grow ever larger, creating mass unemployment, collapsing incomes, and ultimately an AI-driven dystopia, I would argue the opposite: AI could trigger the most profound economic transformation since the first industrial revolution — bringing development, in some sense, full circle. This is not my base case. But it is an intellectually worthwhile thought experiment.

If AI fundamentally reshapes the economy, disruption is inevitable. Some people will lose their jobs. If your role consists of processing large Excel files for eight hours a day, that position is likely at risk. But the first question one should ask is whether such work represents an aspirational equilibrium — or merely economic necessity. Most controllers do not reconcile spreadsheets out of intrinsic passion; they do so to earn an income and finance their desired standard of living.

The situation is not fundamentally different from earlier waves of automation. Few people performed 12-hour assembly-line shifts out of vocation. Technological change was disruptive — and often painful — but over time society became wealthier. The jobs that followed were, on average, more productive and often more fulfilling than those that disappeared.

Here, however, lies a crucial difference. The transition from manual production to mechanized assembly lines required massive capital investments; automation was capital-intensive and naturally favored scale and concentration. This time, the primary capital investment is borne by AI developers. Once the models exist, however, the end product — AI agents — behaves like software: high fixed cost, near-zero marginal cost. As adoption increases, the price for the individual user can remain comparatively low. That alters the economic calculus.

We now operate in an economy in which services dominate and industrial production runs largely on machinery. The increasing dominance of large firms over smaller ones has been driven by rising regulatory complexity, which increased administrative overhead, and prolonged periods of interest rates below equilibrium, which favored capital concentration — particularly for already established or rapidly expanding firms. These businesses operate with high fixed costs and benefit from low marginal costs once their infrastructure is in place.

AI may begin to shift that environment. If administrative and coordination costs fall meaningfully, the structural advantages of scale diminish. Compliance, bookkeeping, marketing, research, and operational coordination can increasingly be automated at low cost. As a result, the minimum efficient scale of many service businesses declines.

In the initial phase, displacement is likely. Certain roles will disappear. But displacement does not automatically imply permanent unemployment. A skilled workforce equipped with low-cost AI tools may reorganize production — shifting from salaried employment toward independent or small-scale entrepreneurial activity.

If the fixed costs of starting and running a business fall substantially, entry barriers decline. In such an environment, competition intensifies rather than concentrates. Established players face pressure not only from other large firms, but from a growing number of smaller, AI-enabled producers.

Media and financial analysis offer early examples. Large outlets historically benefited from administrative scale and distribution advantages. If AI reduces editorial, research, and coordination costs, smaller teams — or even individuals — can operate competitively. Platforms such as Substack already demonstrate how distribution advantages can erode when fixed costs fall.

Lower administrative burdens also make formal entrepreneurship more accessible. Tax structures and accounting mechanisms that previously required scale become manageable for smaller entities once compliance costs decline. The distinction between “employee” and “owner” becomes less rigid. As more individuals operate as businesses rather than salaried labor, they gain access to the same structural advantages — expense deductibility, retained earnings, capital formation — that previously required scale.

In such a scenario, supply expands. Competition increases. Prices face downward pressure. Consumers benefit through higher real incomes, even if nominal wage structures shift. Some professions will contract — certain tax specialists, compliance roles, or research-heavy law practices may face pressure — while others adapt or emerge.

Instead of “AI eating all jobs,” the more accurate description may be “AI compressing coordination advantages.” What weakens are not human capabilities, but the structural barriers that protect incumbents.

Adam Smith argued that the division of labor is the central driver of productivity and rising living standards. Viewed through that lens, AI is not necessarily a destroyer of demand, but a catalyst for a more granular, decentralized division of labor.

Social media democratized distribution and communication. AI has the potential to democratize production and entrepreneurship. This remains speculative. But unlike the demand-collapse narrative, it rests on a clear economic mechanism: falling coordination costs, declining entry barriers, and a more granular division of labor.

Weaker US GDP Report Signals Underlying Strength — But Are Interest Rates Too High?

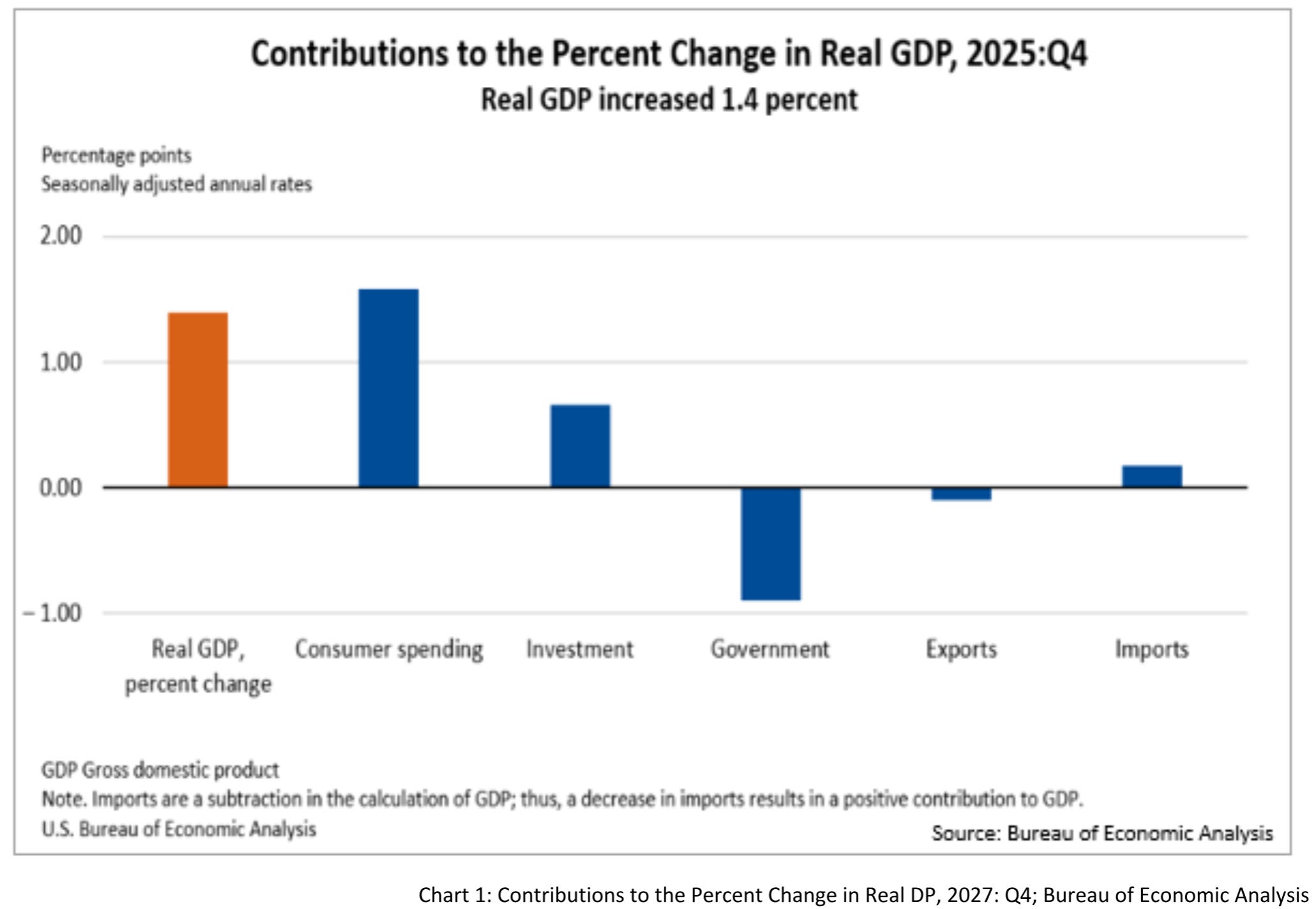

Last week, the US GDP numbers for Q4 were released, and markets were unimpressed. According to the Bureau of Economic Analysis, the economy grew at an annualized rate of 1.4% in the fourth quarter of 2025, well below the 2.8% consensus expectation. Predictably, bearish commentators were quick to interpret this as evidence of a sharp slowdown.

A closer look at the report, however, paints a more nuanced picture. The primary drag came from government spending.

This raises an important question: Does higher government spending necessarily strengthen real economic activity? While the figure was partly influenced by the brief government shutdown, a moderation in public spending is not inherently negative. From a structural perspective, lower government outlays can free up resources for private investment and consumption — the more sustainable drivers of growth.

Indeed, private-sector demand remained relatively stable. Consumption and private investment grew at a combined annualized rate of 2.4% in Q4, only slightly below the 3% recorded in Q3. That does not suggest a collapsing economy.

More revealing is the divergence between non-cyclical and cyclical components of GDP, as highlighted by EBP Research’s Eric Basmajian. Non-cyclical GDP — primarily services consumption — grew at a solid 2.9% annualized in Q4, largely resilient to the current interest rate environment.

By contrast, cyclical GDP — including durable goods consumption, residential investment, and business equipment investment — expanded by just 0.3% annualized. These sectors are highly sensitive to financing conditions and tend to generate most of the economy’s volatility. As Basmajian notes, the three cyclical sectors “generate all the fluctuations in the economy.”

Growth in these areas has slowed markedly from roughly 6% in Q2 2024 to 0.3% in Q4 2025. The implication is clear: monetary policy may now be restrictive for interest-rate-sensitive sectors, even if broader services activity remains firm.

This raises the possibility that the Federal Reserve has misjudged the lagged effects of its tightening cycle. Rates that appeared neutral or only mildly restrictive in one macro environment can become significantly tighter as growth momentum fades. Financial conditions can shift quickly once cyclical sectors stall.

If that interpretation proves correct, interest rates may end the year lower than currently implied by market pricing.

Such an outcome would also align with the broader monetary backdrop. Money supply dynamics no longer provide a tailwind for inflation, suggesting limited upward price pressure into year-end. In that context, the case for rate cuts strengthens.

Ironically, if tariffs temporarily boosted inflation relative to a no-tariff scenario, they may have complicated the Fed’s ability to ease policy — delaying precisely the lower rates that their political proponents might prefer.

Germany Scraps Its Heating Law – Only To Come Up With More Central Planning

A brief look at Germany: the governing coalition has agreed to abolish the strict ban on new gas and oil heating systems introduced under the previous government. Friedrich Merz has thus fulfilled one of his campaign promises — though the reform stops short of a full repeal. Instead of an outright ban, the coalition agreed on a “green gas quota,” requiring gas suppliers to blend an increasing share of renewable gases into heating systems. The move is likely to stabilize housing prices for properties with existing oil or gas systems, which had been under valuation pressure.

What Merz conceded in return appears to be the agreement on the “Bundestariftreuegesetz,” which ties federal public contracts to compliance with centrally defined wage standards. At a time when the government plans large expenditures for defense and infrastructure, the law carries significant economic relevance.

Under the compromise, the Labour Ministry will determine, via executive ordinance, which collective wage agreements firms must follow to qualify for federal contracts. The stated goal is to prevent “wage dumping with taxpayer money” and strengthen collective bargaining coverage, which has fallen to roughly 50% of employees.

The proposal already faces legal scrutiny, and its economic effectiveness remains uncertain. Similar rules at the state level have not prevented the continued decline in collective bargaining coverage, while smaller firms have often been discouraged from bidding on public contracts.

In effect, while regulatory pressure in the housing market is reduced, a new layer of administrative steering is introduced in public procurement. Germany is not necessarily deregulating — it is reallocating regulation, shifting intervention from one sector to another amid expanding public spending.

Now, let’s assess the further trajectory for markets.

Bonds & Interest Rates

The bond market continued its upward move this week, extending the countertrend rally that began in February. Although momentum has slowed since Tuesday, the short-term price picture on the long end remains constructive. That said, price action has been choppy, which warrants caution when drawing strong directional conclusions.

Slowing inflation in the US and Europe does not, in itself, create headwinds for bonds. Growth dynamics are more relevant. In the Euro Area, real yields continue to drift lower, suggesting that market participants question the effectiveness of expanding fiscal spending in generating sustained growth.

The US picture is more nuanced. Growth remains comparatively resilient but faces increasing uncertainty, particularly in interest-rate-sensitive sectors. The key variable is monetary policy. If the Fed concludes that rates should be lowered despite inflation remaining above target and headline growth appearing stable, the long end could extend its rally. Conversely, if policy remains geared toward sustaining above-trend growth, the current rally in US Treasuries may encounter resistance.

Overall, the bond outlook has improved, but the environment remains highly sensitive to incoming data and policy signals.

Stocks

The broader equity picture remains largely unchanged despite recent volatility. As long as price action remains constructive, there is little reason to adopt a defensive stance.

US equities have underperformed relative to global peers this year, which is notable. Whether that trend persists is uncertain. My base case continues to favor a broadening of the rally, with smaller-cap stocks maintaining relative strength.

FX, Gold & Bitcoin

Gold has defended the $5,000 level following the tariff developments, and the technical picture remains constructive. Bitcoin, despite a strong mid-week rally, would need a sustained move above $73,000 to reverse its broader bearish structure.

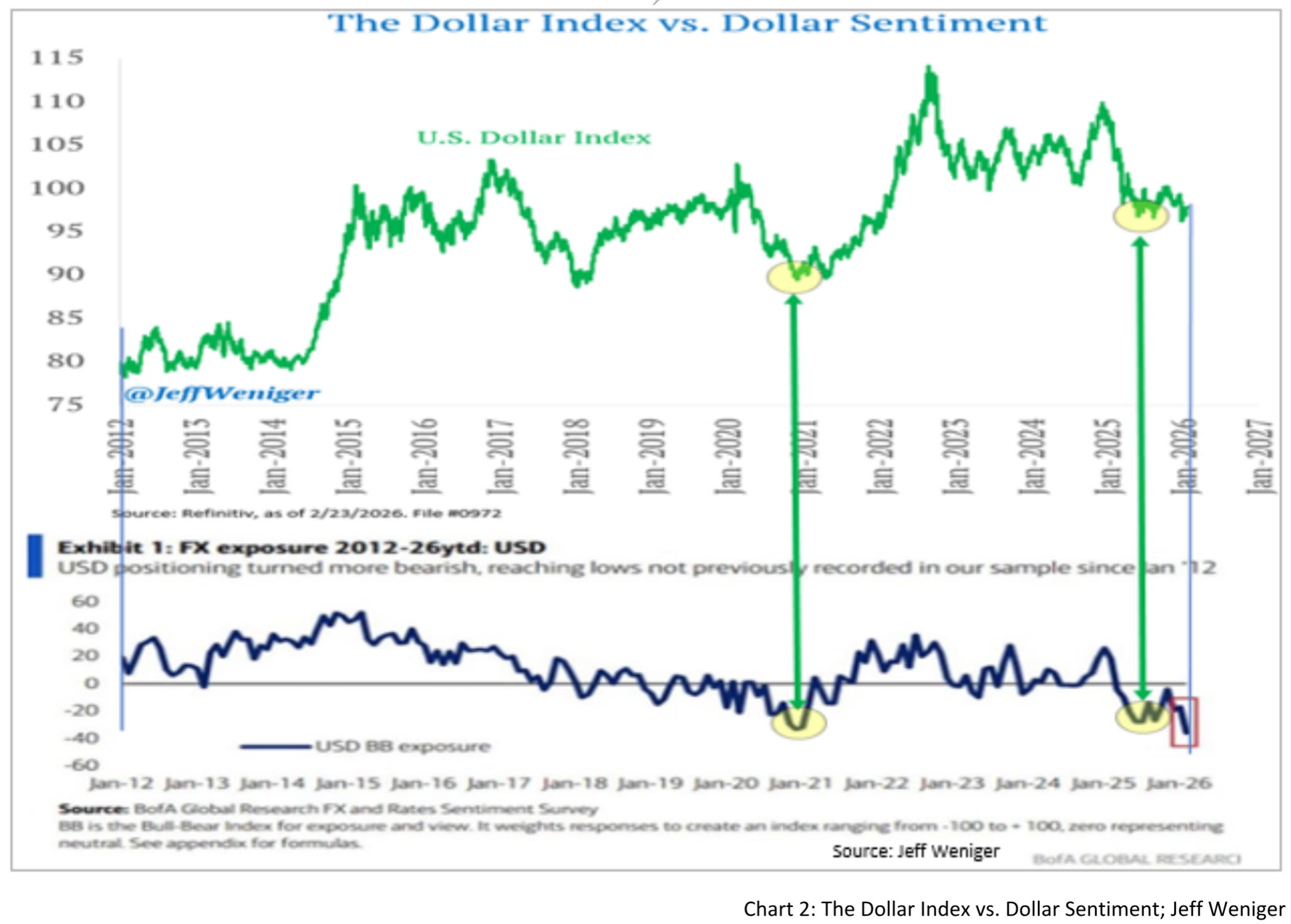

EUR/USD remains in a short-term uptrend. A sustained hold above 1.17 keeps the path open for a potential move toward the 1.20–1.25 range. However, dollar sentiment remains extremely bearish. The last time positioning reached comparable levels, a strong dollar rally followed — as illustrated in the latest chart shared by Jeff Weniger, which combines the BofA Fund Manager Survey with the DXY.

Conclusion

With the latest developments, my outlook for financial markets remains largely unchanged. I doubt that the tariff decision will have any meaningful impact on markets, and the same applies to the Citrini narrative, despite the attention it received in financial media. It is far more likely that the price moved first and the explanation followed. Narratives tend to chase markets, not drive them.

Stocks remain on an upward trajectory, while the bond market has improved. The extreme pessimism toward bonds made a countertrend rally increasingly probable, and that dynamic has played out so far. Overall, I remain broadly neutral with a slight bullish bias.

The broader debate around AI reflects a familiar historical pattern. Since Adam Smith published The Wealth of Nations, technological disruption has repeatedly triggered fears of systemic decline. Whenever productivity accelerates, it is quickly framed as a curse rather than a catalyst.

Whether AI ultimately reshapes economic structures remains uncertain. For now, its measurable macroeconomic impact is still limited. But history suggests that what appears to be a curse often turns out to be a reorganization of prosperity — a shift in how production is structured, not a collapse of demand itself.

I give you my word

In the times I’ve had enough

I still wish for the worst

As free as a bird

But the days keep crossing off

Heaven camе with a curseArchitects – Curse

Have a great weekend!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, I would greatly appreciate it if you could share it on social media or give the post a thumbs-up!

All my posts and opinions are purely personal and do not represent the views of any individuals, institutions, or organizations I may be or have been affiliated with, whether professionally or personally. THEY DO NOT CONSTITUTE INVESTMENT ADVICE, and my perspective may change over time in response to evolving facts. IT IS STRONGLY RECOMMENDED TO SEEK INDEPENDENT ADVICE AND CONDUCT YOUR OWN RESEARCH BEFORE MAKING INVESTMENT DECISIONS.