Clouds Over California

Everyone who has grappled with the world’s current monetary system knows what happened on the 15th of August in 1971 and what it meant for the global monetary order. On this day, President Richard Nixon temporarily closed the gold window and ended the dollar peg to gold.

After World War II (the winning) countries agreed on a money order that put the dollar in its center. The dollar was pegged to gold (and thus, the dollar could be considered as good as gold) while all other currencies fluctuated (more-or-less) in value against the dollar. The United States got all the gold and agreed that other countries (theoretically, as the world would learn later) could exchange 35 US dollars for one ounce of gold.

However, because the US was fighting a costly war in Vietnam and Lyndon B. Johnson pushed his Great Society social programs forward, the US money supply expanded until it became more and more evident that the US would not be able to keep the peg. After some countries (led by France, governed by Charles de Gaulle) started to withdraw their gold from the United States and reduced their dollar reserves, Nixon had no other choice than to end the dollars peg to gold.

That had consequences for oil prices, back-then the most crucial energy source because oil was priced in US dollars. Because of the dollar's devaluation, in September 1971, OPEC announced that it planned to price oil against gold (see Taghizadegan, Stoeferle, 2014, p.87).

As the dollar devalued, the US trade deficit rose, and Nixon and foreign minister Henry Kissinger feared that this could end the dollar hegemony. On the other hand, oil-exporting countries experienced a sharp rise in their trade surplus. Legend has it that in the end, Kissinger could convince OPEC (headed up by Saudi Arabia) to price oil in US dollars again in 1975.

As a result, the monetary system changed. Instead of one with a dominant neutral reserve asset (gold), the dollar became the world’s primary reserve asset, and as you probably know, dollars can be printed into existence. As oil exporters demanded dollars, energy importers needed to expand their dollar reserves to pay for oil. Foreign demand for US-treasuries (dollars) rose, and the world economy checked into Hotel California (according to The Eagles, such a lovely place).

The latest significant shift in the global monetary order reestablished the supremacy of the US dollar in the fx-sphere. As countries needed to have dollars, demand remained high. The trade-off has been clear: The United States issues the dollars to keep the system afloat, and the rest of the world produces the goods.

Other countries that tried to weaken the dollar’s power in the international money order have failed so far. The Euro never had the potential to endanger the dollar’s position, and the Chinese Yuan (that some people consider the possible next leading currency) lacks foreign demand. The dollar was in a delicate situation to remain the global reserve currency for longer. The international dollar system is similar to the last line in Hotel California: you can check out any time you like, but you can never leave.

Additionally, the demand for dollars is not that high because most energy prices are quoted in dollars only. The US has the biggest, most developed, and most liquid financial markets. The recent issue of joint EU debt (NextGeneration EU) assumingly was also made to strengthen the European capital markets, but with very little success until now.

However, according to Luke Gromen (Forest For The Trees LLC), this might change in the foreseeable future. Before I jump into Luke’s arguments that he laid out in several podcasts recently, I want to add that it probably takes several years until his theory unfolds. In the near term, I expect the US dollar to benefit from the current economic environment and that there will be a heavy bid for dollars.

There are some Clouds Over California. The west’s reaction to Putin’s invasion of Ukraine may speed up things that have gone on under the surface for a few years now and probably will end the dollar regime in the coming years/decades. Luke argues that the West has opened Pandora’s box by deciding to freeze Russian fx reserves.

It already happened that the accounts of individuals were frozen. Take the actions of Justin Trudeau during the Trucker protests as an example. Nevertheless, now the US and the EU have set a precedent on a state level. For the first time, countries had to assert that the west would freeze their fx reserves if they considered them a bad actor.

As Luke Gromen correctly notes, over the years, many countries have been considered bad actors by the US: the Britons in the 50s, the French in the 60s, the Japanese in the 80s, or the Saudis some years ago (remember the Kashoggi-incident?).

Let us get back to February when the war started, and we will find out that there was an extensive discussion about the plan to freeze a country's reserves. Some major leaders in the financial industry, like JP Morgan’s Jamie Dimon, were against plans to exclude Russia from the SWIFT payment system. The editors of Bloomberg warned that

The example of Russia could prompt others — such as China — to turn to alternatives, fragmenting the payments system and potentially even undermining the U.S. dollar’s dominance as the global reserve currency. One could even imagine a future in which rival nations turned similar financial weapons against the U.S.

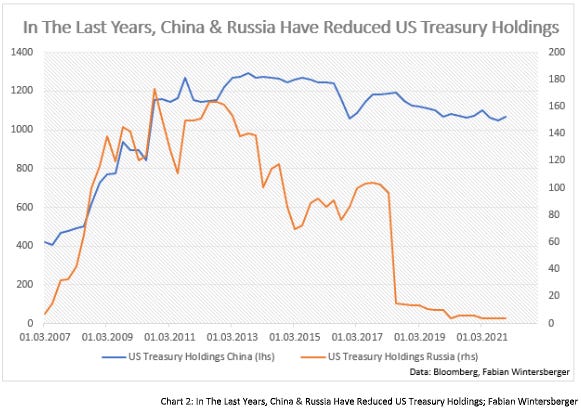

However, there is no way that the West could implement the same sanctions against China because it is the world's manufacturing superpower, as Luke rightly points out. The world cannot go without Chinese products. According to Luke, this is another result of the dollar being the global reserve currency. The elevated demand for US treasuries (dollars) appreciates the dollar against the Yuan and has led to more and more production facilities being transferred from the West to China.

The events in Ukraine, or more specifically, the implementation of the actual sanctions, may signify that the US and the EU underestimated Russia’s leverage once again. When the Ruble started to cripple because of the sanctions, every political commentator assumed that the fall of the Russian bear would only be a matter of time. But although morally, it was indeed an obligation to do something to punish Russia for violating international law, one could throw in the argument that no one thought of unintended consequences, for example, Russia’s reaction to it.

Firstly, there was Russia’s Volcker moment, where the Bank of Russia ramped up interest rates to 20 % (recently, it lowered rates down to 17 %) and put capital controls in place. Later, the Russian government announced that it plans to demand rubles in exchange for supplying gas to the hostile states. Additionally, the Russian central bank started to buy gold for the first time after two years. Until the 8th of April, the central bank guaranteed credit institutes to pay 5,000 rubles/gram to ensure the proper functioning of the domestic gold market.

We know now that the talks about an implosion of the ruble were premature. Where the ruble trades, it trades higher against the dollar than before the invasion. I agree with Lukes's conclusion that the EU and the United totally miscalculated Russia’s ability to defend the ruble through gold- and energy markets.

So, how will things play out further? Luke also has some fascinating theories about that. If those will come into reality (and no one really knows), it supports my argument from last week that the world is splitting up into two big blocks again.

Luke speculates that the next step could be to (indirectly) peg the ruble to oil and gold. The question is, how? Russia demands rubles for gas, but no country has any rubles, and the market is pretty limited because of the sanctions. Gazprombank offers its clients to pay in Euro, and the bank buys rubles with it, which props up the ruble's value.

Another option, according to Luke, could be to buy rubles from the Bank of Russia directly in exchange for gold. Assume the central bank would guarantee a fixed exchange rate and sell energy at a discount. That would lead to a risk-free arbitrage that would get bigger the stronger the ruble gets against the dollar. This way, Luke notes, Russia could weaponize energy, the indispensability of energy itself to defend the ruble.

It is highly probable (almost certain) that the West would not use this arbitrage, but it is also true that other countries would not hesitate to do that. India has recently said precisely that. Because it is all about energy and food (you probably know that Russia is one of the leading exporters of agricultural products), countries like India do not have a choice.

But most western economists say that the danger of an energy ban is neglectable because of Russia’s low GDP, right? I agree with Luke that this is wrong, especially for energy importers like China, India, and (surprise!) Europe. He says that Europe acts disillusioned because Europe cannot forgo Russian energy as an energy importer while the United States can. After all, they are an energy exporter.

I also have written a lot about the fact that Europe is acting short-sighted and that I assume that the sanctions may do more harm than good. It is challenging because, from a moral standpoint, it is absolutely true that Europe should stop buying, but it does not mean that it is the right thing one should do.

Luke also lays out ways how to solve this. Either one sanctions Russian energy out of the market, abolishes gold and puts capital controls in play, or ends sanctions and comes to some sort of agreement. Obviously, the only way would be the first option, but this would probably lead to an economic collapse.

I agree with Luke that the recent events will lead to countries' reviewing the composition of their reserves and trying to become more independent from the US dollar. I tend to agree with him that gold, or some other neutral reserve asset, will play a more prominent role in the future. Therefore, I think that gold might strongly appreciate this decade, especially if gold gets tied to energy.

Somehow, it seems that Putin speculated on such a situation, and the current economic turmoil is playing into his hands. He said inflation would heap pressure on western politicians about two weeks ago. If one looks at France, where Macron got reelected, current inflation problems might be one cause why a politician like Marine Le Pen can receive 44 % of the vote (combined with the fact that a lot of French dislike Macron).

The other aspect is that current debt/GDP levels make it very hard for Europe (and the US) to sanction Russian energy entirely. I mean that this is the cause why so many European politicians hesitate to call for a total energy ban, except for some who do not want to let this crisis go to waste and want to speed up the green transition.

However, one should acknowledge that Europe is spending 9.1% of its GDP on energy, and an embargo would quickly push this number into double digits.

Anyway, the latest sanctions are causing problems already, as an article in the Financial Times noted on Tuesday. The article said that Europe faces a critical shortage of metals needed for clean energy. I conclude that Europe's renewables for the green transition will not be produced in Europe but China, using dirty coal energy.

I think that Luke’s arguments are compelling, although I am not sure how fast/slow all this would play out and causes a change in the global monetary system. Without a doubt, current economic and geopolitical events have fastened things up, as the pandemic has done with work-from-home.

Luke held his position for quite a while now that the end of the dollar hegemony might be nearer than many people would assume. Personally, I think that the probability that this will happen within the next two to five years is still low. Actual events might have accelerated things, but we are still far away from the end of the dollar as the primary global reserve asset.

There is simply no alternative to the dollar. The Chinese do not want to use the Yuan (probably because they take advantage of a weak currency), and Europe is having too much trouble trying something with the Euro. Arguably, there is a way to replace the dollar with a neutral reserve asset, but this will take time. The dollar remains the cleanest shirt in the dirty laundry of fiat money.

For now, fiat money will remain dominant, and within that category, there is no alternative to the dollar. The Japanese Yen and the Euro have recently devalued against the dollar because both countries still do not want to tighten monetary policy or, put differently, the Fed plans to be way more aggressive than the BoJ or the ECB. The BoJ is already risking a currency crisis because it is keeping interest rates from rising (Yield Curve Control). If things continue, the Euro might be in a similar position soon.

Further, dollar strength is insufficient for emerging economies because many companies have issued much dollar-denominated debt to attract investments. Interestingly, currencies from countries rich in commodities, like the Brazilian Real, have appreciated or have done at least better than the yen or the euro against the dollar. The biggest beneficiaries of the current situation seem to be commodities and, paradoxically, the Russian ruble.

As all central banks in the West have declared to fight inflation at all costs (at least they claim), there is economic trouble ahead. According to Deutsche Bank, it needs a recession to bring inflation back down, which is not a good sign.

Whatever you think of Luke Gromen’s theory, I urge you to at least think about it. It is fascinating how he is connecting the dots, and even if it might be neglectable in the short term, his theses might gain importance over the long run. Apart from that, it is also entertaining. If you have 1.5 hours, I recommend the interview below that he did with Austrian journalist/blogger Niko Jilch.

Finally, let us wind back to Bretton-Woods again. The idea that the financial world order should be based on a neutral reserve asset is not new. John Maynard Keynes proposed this idea at that conference (BANCOR). However, the United States opposed this suggestion because they wanted to make the US dollar the epicenter of the global monetary system. In this case, we should have listened to the Author of the General Theory.

Have a fabulous weekend!

Fabian Wintersberger

Thank you for reading! You can subscribe and get every post directly into your inbox if you like what I write. Also, it would be fantastic if you shared it on social media or liked the post!

(All posts are my personal opinion only and do not represent those of people, institutions, or organizations that the owner may or may not be associated with in a professional or personal capacity.)

Thanks for this article! I'm always sceptical when someone predicts the imminent demise of the dollar, because it just shows how much they fail to appreciate the complexity of the monetary system. We're talking years or decades here: to assume the status quo can continue like this forever is foolish as well. The truth is somewhere in the middle and probably best defined by the timeframe we attach to it.

Fabian, this is such a fascinating subject and I think Luke makes some excellent points. objectively, there is no doubt that the Russians seem to be playing a far stronger hand than the West assumed. and ironically it was Angela Merkel and the European hatred of President Trump that helped them deal that hand to themselves. but the cards are what they are and now they must be played.

Ultimately though, the acceptance of a neutral reserve asset will be a long time coming I fear, as those countries that don't have it before the declaration will fight tooth and nail to allow it. whether that is oil or gold or a basket, commodity importers are going to be screaming to prevent such an outcome. Which takes us back to the dollar, as you aptly describe the cleanest dirty shirt in the laundry. I feel a little discussed consequence of being the reserve currency is that the US is effectively required to print them to satisfy the rest of the world's needs.

FWIW, which is probably not much, I feel like the first major step will be a debt jubilee of some sort, reducing the amount of leverage outstanding in the world. only then can a neutral asset with limited ability to be expanded be acceptable to the bulk of the world.

To me that argues that real assets remain the hold of choice and debt instruments are going to be a problem going forward.

have a great weekend